Home — Articles

- Limit value of the tax base for calculating insurance contributions Limit value for pension contributions

- Limit value of the base for contributions to the Social Insurance Fund of the Russian Federation

- The limit on the base for medical contributions is canceled

- The right to choose a funded pension is preserved

- Additional tariffs for companies that have not carried out a special assessment

- Who will lose the right to a reduced tariff

In the new year 2015, provisions of several federal laws regarding insurance premium rates and personal injury premiums come into force. There are several innovations. They relate to the application of the maximum value of the base subject to insurance premiums, tariffs and payment of contributions.

Limit value of the taxable base for calculating insurance premiums

Starting from 2015, there will be no single maximum base for the calculation of all types of insurance premiums.

Limit for pension contributions

The maximum value of the taxable base for contributions to the Pension Fund will be approved by the Government of the Russian Federation, taking into account the size of the average salary, increased by 12 times, and the increasing coefficient (in 2015 - 1.7) (Part 5.1 of Article 8 of the Federal Law of July 24, 2009 N 212-FZ, hereinafter referred to as Law N 212-FZ).

In the future, from 2022, the maximum value of the base for calculating insurance contributions to the Pension Fund, established for the previous year, will be indexed (Part 5.2 of Article 8 of Law No. 212-FZ).

In 2015 it is equal to 711,000 rubles. (Clause 1 of the Decree of the Government of the Russian Federation of December 4, 2014 N 1316). Above this amount, insurance premiums will have to be paid, as before, at a rate of 10%.

Limit value of the base for contributions to the Social Insurance Fund of the Russian Federation

For 2015, the maximum value of the taxable base for insurance premiums in case of temporary disability and in connection with maternity was established by the Government of the Russian Federation in paragraph 1 of Resolution No. 1316 of December 4, 2014 (clauses 4 and 5 of Article 8 of Law No. 212-FZ ) in the amount of 670,000 rubles.

The limit on the base for medical contributions is canceled

In 2015, insurance contributions to the FFOMS will need to be paid from the entire amount of wages, and not within the limit, as was the case in 2014. This procedure is determined by the new part 1.1 of Art. 58.2 of Law No. 212-FZ (Article 5 of Federal Law dated December 1, 2014 No. 406-FZ). It does not indicate the maximum amount of the taxable base.

The change will not affect policyholders paying premiums at a reduced rate and listed in Art. Art. 58 and 58.1 of Law No. 212-FZ.

Payers of insurance premiums and accrual base

Payers of insurance premiums on the basis of Article 5 of Law N 212-FZ are policyholders, which include, in particular, organizations and individual entrepreneurs both on the simplified tax system and on UTII, Unified Agricultural Tax and PSN, making payments and other remuneration to individuals.

In order to calculate insurance premiums, it is necessary to determine the object of taxation of insurance premiums and the basis for their calculation. Such an object is recognized as payments and other remuneration accrued in favor of individuals within the framework of labor relations and civil contracts upon completion of work, provision of services, under copyright contracts, agreements on the alienation of exclusive rights, licensing agreements on granting the right to use a work of science, literature, art.

In addition, the object also recognizes payments and other remuneration accrued by them in favor of individuals subject to compulsory social insurance in accordance with federal laws on specific types of compulsory social insurance.

The basis for calculating insurance premiums is the amount of payments and other remunerations included in the object of taxation, accrued by taxpayers in favor of individuals. The billing period is the calendar year, the reporting periods are the first quarter, six months, nine months of the calendar year, and the calendar year.

In turn, the basis for calculating insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity, paid to the Social Insurance Fund, Pension Fund and Federal Compulsory Medical Insurance Fund, must be determined separately for each individual from the beginning of the billing period at the end of each calendar month on an accrual basis .

General insurance premium rates

The current aggregate general tariff of insurance premiums of 30% has been retained (Part 1.1, Article 58.2 of Law No. 212-FZ). It consists of the following tariffs:

- 22% - tariff for calculating pension contributions;

- 2.9% - tariff for calculating contributions in case of temporary disability and in connection with maternity;

- 5.1% is the tariff for calculating contributions for compulsory health insurance.

General tariffs must be applied by all insurers, with the exception of those companies for which reduced tariffs are provided (Articles 58 and 58.1 of Law No. 212-FZ).

Note. The amounts of insurance premiums no longer need to be rounded. From January 1, 2015, insurance premiums must be transferred in rubles and kopecks (Part 7, Article 15 of Law No. 212-FZ). This will make it possible to achieve identical indicators of accrued and paid insurance premiums in Form-4 of the FSS and Form RSV-1 of the Pension Fund of the Russian Federation.

Contributions to the Pension Fund 2015 for individual entrepreneurs with employees

The bulk of innovations concern the timing and methods of reporting, the amounts of income from which contributions are calculated and methods of paying them. Along with organizations, individual entrepreneurs should take into account positive and negative changes. Entrepreneurs with employees must pay contributions to the Pension Fund of the Russian Federation in 2015 at the basic tariff rate of 22%, until the employee’s total income does not exceed 711,000 rubles. But for the FFOMS there are now no restrictions. Health insurance premiums will now be levied on all income. Entrepreneurs whose average number of employees exceeds 25 people are required to report to the Pension Fund only by email. A positive aspect in this situation is the shift in reporting deadlines. You can send the RSV-1 form via TKS until the 20th day of the second month after the end of the quarter. Previously, the deadline was the 15th. It will remain relevant for paper reporting.

Another important innovation is the possibility of deferring the payment of funds for individual entrepreneurs. Contributions to the Pension Fund 2015 can be transferred later than the established deadlines in the following cases:

- If the entrepreneur's company suffered as a result of a natural disaster or for reasons beyond his control.

- If business activity is seasonal.

Latest news: Individual entrepreneur contributions to the Pension Fund 2015 or to the Federal Compulsory Medical Insurance Fund, for which there are or will be overpayments, can be offset against each other. The basis for such a statement was a letter from the Ministry of Labor dated September 24, 2014. No. 17–3/B-451. And an insignificant, but still established by law, innovation - payment of insurance premiums to the Pension Fund must be made in rubles and kopecks.

What to do with a funded pension in 2015

Article 33.1 of Federal Law No. 167-FZ of December 15, 2001 (hereinafter referred to as Law No. 167-FZ) determines that the pension contribution rate is distributed among insurance and funded pensions. This norm remains relevant. However, in 2015 there is a special procedure for its application.

The right to choose a funded pension is preserved

Until December 31, 2015, insured persons born in 1967 and younger can choose one of two pension options - send 6% of contributions to finance a funded pension or send all 22% to an insurance pension (Clause 1, Article 33.3 of Law No. 167-FZ ).

If you choose the “savings” option, the employee himself must apply for the transfer, for example, to a non-state pension fund. The employer has nothing to do with this. Another point is important for him.

In 2015, there is a moratorium on accrual of contributions to funded pension

Regardless of the decision of the insured person to choose the “cumulative” option of pension insurance and his submission of the corresponding application, the entire amount of insurance pension contributions accrued for payments in favor of this person in 2015 is directed to the insurance pension.

The accountant of a company that applies a general tariff calculates pension contributions at a single tariff of 22% and transfers them in one payment document to the KBK of the insurance pension (Article 22.2 of Law N 167-FZ).

Contribution rate in case of injury

Federal Law No. 401-FZ dated December 1, 2014 retains the current contribution rates for injuries in 2015 (from 0.2 to 8.5%) (Article 1 of Federal Law No. 179-FZ dated December 22, 2005). Therefore, as before:

- The amount of contributions depends on the main type of economic activity. To confirm it, you must, no later than April 15, 2015, submit an application and a confirmation certificate to your territorial branch of the Federal Social Insurance Fund of the Russian Federation in the forms approved by Order of the Ministry of Health and Social Development of Russia dated January 31, 2006 N 55;

- There is no limit on the taxable base for them, so they are charged on all taxable payments.

If an individual entrepreneur employs disabled people of group I, II or III, payments in their favor, as before, are subject to contributions in case of injury at a reduced rate - based on 60% of the established insurance rate (Article 2 of the Federal Law of December 1, 2014 N 401-FZ).

Additional insurance premium rates increased in 2015

Additional contributions to the Pension Fund are paid by companies that have jobs with harmful (dangerous) working conditions and the right to early retirement. Contributions are calculated regardless of the maximum value of the taxable base (Part 3, Article 58.3 of Law No. 212-FZ, Clause 3, Article 33.2 of Law No. 167-FZ).

The types of work that give the right to early retirement were listed in paragraphs. 1 - 18 p. 1 tbsp. 27 of the Federal Law of December 17, 2001 N 173-FZ (hereinafter referred to as Law N 173-FZ) (clauses 1 and 2 of Article 33.2 of Law N 167-FZ). However, from January 1, 2015, many provisions of Law N 173-FZ do not apply.

Note. Federal Law No. 173-FZ of December 17, 2001 was applied only to calculate the insurance part of the labor pension in the period before January 1, 2015.

Now you need to use two Federal laws:

- dated December 28, 2013 N 400-FZ “On Insurance Pensions” (hereinafter referred to as Law N 400-FZ);

- dated December 28, 2013 N 424-FZ “On funded pensions”.

The types of hazardous work that give the right to early retirement are now specified in Law No. 400-FZ.

The rates of additional contributions for such companies will depend on whether they have undergone a special assessment of working conditions or not.

Additional tariffs for companies that have not carried out a special assessment

If a special assessment has not been carried out, companies must pay additional contributions for employees engaged in hazardous work at the rates given in table. 1 below.

Table 1

Additional tariffs for contributions to the Pension Fund in 2015. No special assessment was carried out

| Tariff 6% | Tariff 9% | Tariff 4% | Tariff 6% |

| Until December 31, 2014 | From 01/01/2015 | Until December 31, 2014 | From 01/01/2015 |

| For the types of work listed in paragraphs. 1 clause 1 art. 27 Law No. 173-FZ | For the types of work listed in clause 1, part 1, art. 30 Law No. 400-FZ | For the types of work listed in paragraphs. 2 - 18 p. 1 tbsp. 27 Law No. 173-FZ | For the types of work listed in paragraphs. 2 - 18 p. 1 tbsp. 30 Law No. 400-FZ |

Additional tariffs based on the results of a special assessment

The size of additional tariffs may change if companies have carried out a special assessment of working conditions. Depending on the established subclass of working conditions in 2015, policyholders must pay premiums according to the additional tariffs given in table. 2 below (part 2.1 of article 58.3 of Law No. 212-FZ and paragraph 2.1 of article 33.2 of Law No. 167-FZ).

table 2

Additional tariffs for contributions to the Pension Fund in 2015. Special assessment completed

| Class of working conditions | Subclass of working conditions | Additional tariff, % |

| Dangerous | 4 | 8 |

| Harmful | 3.4 | 7 |

| 3.3 | 6 | |

| 3.2 | 4 | |

| 3.1 | 2 | |

| Acceptable | 2 | 0 |

| Optimal | 1 | 0 |

New for individual entrepreneurs: contributions to the PRF 2015 for yourself

From January 1, the minimum wage is 5965 rubles. Consequently, individual entrepreneur contributions for 2015 will increase, because They are calculated based on the same minimum wage. In the new reporting period, you will need to transfer 18,610.80 rubles to the insurance part, and 3,650.58 rubles to the FFOMS. But this is only if the revenue does not exceed 300,000 rubles. Contributions from the excess amount will be charged at the rate of 1%. In this regard, nothing has changed compared to the previous year. The deadline for transferring funds is December 31. Over-limit contributions – until April 1 of the following year.

Another innovation for individual entrepreneurs without employees: it is legally established that if in the reporting year there are periods when the entrepreneur does not operate and is exempt from paying contributions, the amounts payable are recalculated. The fixed amount is calculated based on the actual time worked. These periods include:

- Completion of military service.

- Child care leave up to 1.5 years.

- Caring for a disabled person of the first group, a person who has reached the age of 80, or a disabled child.

- The period of residence abroad if one of the spouses performs diplomatic functions.

- Conducting military service by one of the spouses under a contract, in an area where there is no employment opportunity. But no more than 5 years.

Reduced insurance premium rates

Changes to the procedure for applying preferential tariffs in 2015 were introduced by Federal Law dated December 2, 2013 N 333-FZ.

Who will lose the right to a reduced tariff

In 2015, some companies that previously paid insurance premiums at reduced rates (Articles 58 and 58.1 of Law No. 212-FZ) will lose benefits (clause 1 of Article 1 of Federal Law dated December 2, 2013 No. 333-FZ):

- agricultural producers;

- companies using UTII;

- companies making payments to disabled people of groups I, II or III (clauses 1 - 3, part 1, article 58 of Law No. 212-FZ);

- Mass media (clause 7, part 1, article 58 of Law No. 212-FZ);

- engineering companies (clause 13, part 1, article 58 of Law No. 212-FZ).

Federal Law No. 333-FZ dated December 2, 2013 did not extend the effect of reduced tariffs for these policyholders to 2015.

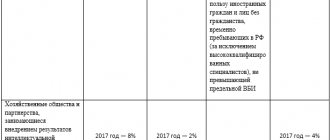

Consequently, starting from 2015, they must charge insurance premiums at the general rates established by Part 2 of Art. 58.2 of Law No. 212-FZ. All other companies that had the right to apply reduced tariffs in 2014 will continue to apply them in 2015 (Table 3 on p. 22).

Table 3

Reduced insurance premium rates in 2015

| Policyholders | Norm Art. 58 Law No. 212-FZ | Extrabudgetary fund | ||

| Pension Fund | FSS RF | FFOMS | ||

| Business societies | Points 4 - 6 part 1 and part 3 | 8% | 2% | 4% |

| Companies in the field of technology development activities | ||||

| IT companies | ||||

| Companies making payments to crew members of ships registered in the Russian International Register of Ships | Clause 9 part 1 and part 3.3 | 0% | 0% | 0% |

| Companies on the simplified tax system, the main activity of which is specified in clause 8, part 1, art. 58 Law No. 212-FZ | Clause 8 part 1 and part 3.4 | 20% | 0% | 0% |

| Companies paying UTII | Clause 10 part 1 and part 3.4 | |||

| Organizations engaged in the field of social services, scientific research, etc. | Clause 11 part 1 and part 3.4 | |||

| Charitable organizations on the simplified tax system | Clause 12 part 1 and part 3.4 | |||

| Individual entrepreneurs on a patent | Clause 14 part 1 and part 3.4 | |||

Such companies pay insurance premiums until the employee’s payments exceed the maximum base for calculating contributions. Excess amounts are not subject to contributions.

Changes in the calculation of contributions at reduced rates

These changes apply to pharmacies and individual entrepreneurs on a patent.

Pharmacies . Since 2015, pharmacy organizations and individual entrepreneurs with a license for pharmaceutical activities can apply reduced tariffs only to payments to employees who have the right to engage in pharmaceutical activities or are allowed to carry out pharmaceutical activities (clause “a”, clause 29, article 5 of the Federal Law dated June 28, 2014 N 188-FZ).

Note. Persons who have the right to engage in pharmaceutical activities until January 1, 2021 are listed in paragraph 1 of Art. 100 of the Federal Law of November 21, 2011 N 323-FZ.

Thus, the question of whether preferential tariffs apply to all workers, including those who are not directly involved in pharmaceutical activities, is finally resolved.

Individual entrepreneurs on a patent . The majority of insurers will be able to apply a reduced tariff only for payments in favor of workers engaged in the type of economic activity specified in the patent (clause “b”, paragraph 29, article 5 of the Federal Law of June 28, 2014 N 188-FZ).

This restriction will not apply to individual entrepreneurs who carry out the types of activities listed in paragraphs. 19, 45 - 47 p. 2 art. 346.43 of the Tax Code:

- retail stationary trade in a sales area of no more than 50 sq. m;

- retail stationary trade without trading floors and through non-stationary retail chain facilities;

- catering services provided in a customer service hall with an area of no more than 50 square meters. m;

- leasing (hiring) of residential and non-residential premises, dachas, land plots owned by an individual entrepreneur by right of ownership.

The new Classifiers OKVED2 and OKPD2 will not be used in 2015

Types of economic activity that give companies and individual entrepreneurs the right to apply the simplified taxation system (STS) (clause 8, clause 1, article 58 of Law No. 212-FZ) are classified in accordance with the All-Russian Classifier of Types of Economic Activities.

From January 1, 2015, it was planned to switch to the use of new Classifiers, which were approved by Order of Rosstandart dated January 31, 2014 N 14-st - OKVED2 OK 029-2014 (NACE Rev. 2) and OKPD2 OK 034-2014 (KPES 2008).

But now, by Order of Rosstandart dated September 30, 2014 N 1261-st, this period has been extended until January 1, 2021. Accordingly, this year policyholders must use the old All-Russian classifiers: OKVED OK 029-2001 (NACE Rev. 1), OKVED OK 029-2007 (NACE Rev. 1.1), OKDP OK 004-93, OKPD OK 034-2007 (KPES 2002), OKUN OK 002-93 and OKP OK 005-93.

FSS RF

- 2.9% within the established limit of the base for calculating insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity;

The maximum value of the base for calculating insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity, provided for in Part 4 of Article 8 of Law N 212-FZ, taking into account the growth of average wages, is subject to indexation from 01/01/2015 by 1,073 times and amounts to an amount not exceeding 670,000 rubles, which is determined for each individual on an accrual basis from 01/01/2015.