The need for due diligence

Exercising due diligence when choosing a counterparty is a category that is primarily of interest to tax authorities, who identify situations that entail the taxpayer receiving an unjustified tax benefit.

These points have acquired particular significance in connection with monitoring the reality of transactions taken into account when calculating 2 main taxes: profit and VAT. Of lesser (but also growing) interest in due diligence are:

- banks that are not only obliged to control certain transactions of their clients (Law “On Combating the Legalization (Laundering) of Income..." dated August 7, 2001 No. 115-FZ), but also interested in at least a stable financial position of persons who received a loan from the bank;

- business owners who want to run it with minimal losses (risks of buying and selling low-quality goods, late deliveries, non-receipt of payments, impossibility of recovering damages).

Why is due diligence one of the key issues directly for the taxpayer himself? Because entrepreneurial activity is carried out at your own peril and risk. That is, the negative consequences arising from the wrong choice of counterparty also become a taxpayer’s risk. And if the tax authority proves that the transactions were not real (that is, the transaction was fictitious), then additional tax charges will be inevitable.

What is due diligence

Let's consider this situation. Alpha LLC entered into an agreement with Delta LLC for the supply of materials. Based on the invoice received from Delta LLC, Alpha LLC deducted VAT.

During a counter-inspection carried out a year later, tax officials found that Delta LLC did not pay VAT on the amount of materials shipped. Moreover, this company has stopped submitting reports altogether and has no legal address.

The question arises: from whom should the VAT arrears be collected? It was not possible to find Delta LLC, so the inspectors accused Alpha LLC of conspiracy and obtaining unjustified tax benefits. The company, naturally, did not agree with this and went to court...

In the first half of the 2000s, many similar cases appeared, relating not only to VAT, but also to other “current” mandatory payments, primarily income tax.

Therefore, the Supreme Arbitration Court of the Russian Federation eventually generalized the practice and expressed its opinion (Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated October 12, 2006 No. 53).

According to the position of the Supreme Arbitration Court judges, in general, a businessman is not to blame for the fact that his counterparties do not pay taxes. However, if it is proven that he knew about the partner’s dishonesty, then the tax benefit may be considered unjustified.

It was in this resolution of the Supreme Arbitration Court that the term “due diligence” first appeared. It means that the taxpayer must check his potential counterparty and not work with those companies that clearly violate the law.

Prudence: legal basis

The concept of due diligence is not legally defined anywhere.

Read more about the current regulation of the concept of “tax benefit” in this article.

However, there are criteria developed by the Federal Tax Service of Russia (order dated May 30, 2007 No. MM-3-06/333), according to which the most likely candidates for an on-site tax audit are selected from among taxpayers. Among these criteria there is also such as conducting activities with a high level of tax risk, the description of which (clause 12 of Appendix 2 to the Federal Tax Service order No. MM-3-06/333) contains a list of characteristics that form the basis for assessing counterparties in terms of possible risks working with them.

For a complete list of criteria for selecting taxpayers for audit, see here.

Additional information about the signs of dubious counterparties can be found in the letters:

- Ministry of Finance of Russia dated December 17, 2014 No. 03-02-07/1/65228 - regarding the characteristics of one-day companies;

- Federal Tax Service of Russia dated February 11, 2010 No. 3-7-07/84 - about information that a taxpayer can request from its counterparties, and measures taken by the tax service to inform about persons unreliable for interacting with them;

- Federal Tax Service of Russia dated October 17, 2012 No. AS-4-2/17710 and dated March 16, 2015 No. ED-4-2/4124 - on available official sources of data on legal entities and individual entrepreneurs, as well as on the qualitative assessment of information reflected in the Unified State Register of Legal Entities;

- Federal Tax Service of Russia dated May 12, 2017 No. AS-4-2/8872 - on the study of certain characteristics of a counterparty when assessing tax risks.

However, formal adherence to the provisions of these documents does not always guarantee the taxpayer the absence of claims from the tax authorities. They are increasingly successfully proving the unreality of dubious business transactions reflected in the accounting, including using arguments that complement the criteria developed by the Federal Tax Service of Russia. And increasingly, the point of view of the Federal Tax Service is supported by judges.

We check whether your counterparty is a current taxpayer

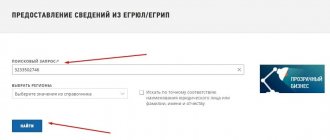

Option 1. We look at the information from the Unified State Register of Legal Entities from the Federal Tax Service website . You simply enter the TIN indicated by the counterparty on the Federal Tax Service website, make sure that its TIN is real and at the time of concluding the agreement there is no information about the exclusion of the company from the Unified State Register of Legal Entities. In one of its Resolutions, the Supreme Arbitration Court of the Russian Federation considered that this form of verification indicates the exercise of due diligence (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated 03/09/2010 N 15574/09). Some courts also decided the same (Resolutions of the FAS PA dated November 1, 2011 in case No. A65-2843/2011; FAS UO dated August 11, 2011 N F09-4478/11; FAS TsO dated July 25, 2011 in case No. A54-4250/2010C21 ; FAS MO dated 02/08/2011 N KA-A40/17851-10). Although, for example, the FAS VSO believes that this is not enough (Resolutions of the FAS VSO dated 08.18.2010 in case No. A33-19963/2009, dated 08.24.2010 in case No. A10-5604/2009).

For your information, you can check your counterparty’s TIN on the Federal Tax Service website www.nalog.ru -> section “Electronic Check yourself and your counterparty” (https://egrul.nalog.ru/).

By the way, the Federal Tax Service also recommends using its official website to check (Letter of the Federal Tax Service of Russia dated February 11, 2010 N 3-7-07/84): - whether the counterparty is one of the inactive legal entities in respect of which the tax authorities have decided on the upcoming exclusion from the Unified State Register of Legal Entities; — whether the director of the counterparty is a disqualified person. Such information will also help you confirm your diligence (Resolutions of the Federal Antimonopoly Service dated July 28, 2011 in case No. A57-13884/2010; Federal Antimonopoly Service of the Moscow Region dated September 9, 2010 No. KA-A40/10126-10).

Note The results of checking a counterparty via the Internet are best presented in the form of a screenshot (screenshot) of the information received. To do this, press the Ctrl and PrintScreen keys on your keyboard at the same time. Then open the Paint program in standard Windows programs and insert the image into the open sheet by right-clicking and selecting the “Insert” command. The resulting file should be saved in *.jpeg format using the “Save As...” command located in the “File” tab.

Option 2. We receive an extract from the Unified State Register of Legal Entities . Considering that providing an extract is a paid service, it is better if the counterparty provides it to you. Many courts consider the presence of an extract to be a sufficient manifestation of due diligence (Resolutions of the Federal Antimonopoly Service dated October 10, 2011 in case N A65-28269/2010; FAS Far Eastern Military District dated October 3, 2011 N F03-4402/2011; FAS Moscow Region dated March 14, 2011 N KA-A40/ 690-11; FAS SZO dated June 21, 2011 in case No. A05-11486/2010; FAS UO dated June 18, 2010 N F09-4486/10-C2). Although, again, there are those for whom this is not enough, since the fact that the counterparty is registered in the Unified State Register of Legal Entities does not mean that he is conducting real activities (Resolution of the Federal Antimonopoly Service of the Moscow Region dated June 22, 2011 N KA-A40/6036-11, dated February 22. 2011 N KA-A40/18297-10; FAS UO dated November 28, 2011 N F09-6952/11; FAS VSO dated October 19, 2010 in case N A19-3822/10).

Option 3. We request a copy of the registration certificate and the certificate of registration with the tax authority . The counterparty can provide you with certified copies of these documents, and without any effort on his part. And this will also be considered your due diligence (Resolutions of the FAS PA dated July 20, 2010 in case N A12-23566/2009; FAS MO dated November 30, 2010 N KA-A40/15207-10, dated October 24, 2011 in case N A40- 138664/10-127-789; FAS SZO dated 08/15/2011 in case No. A56-36565/2010).

From authoritative sources Kaftannikov A.A., CJSC AF “Audit-Classic” “It would not be superfluous to check the compliance of the information in the submitted documents with the actual information in the Unified State Register of Legal Entities, available on the Federal Tax Service website. This is necessary to ensure that the certificate is not outdated at the time of conclusion of the contract and is true. It happens that an agreement is concluded with a person who has already been liquidated. Moreover, there are often cases when unscrupulous counterparties simply falsify copies of submitted documents. In addition, on the website https://www.kartoteka.ru you can verify in real time that liquidation or bankruptcy proceedings have not been initiated against the counterparty company.”

Judicial practice: signs of lack of diligence

The approach to assessing the due diligence of a taxpayer has been formulated by the Supreme Court. You can learn more about it from the Review from ConsultantPlus. Trial access to the system can be obtained for free.

As for district courts, the following arguments are based on the court’s recognition of the counterparty as not meeting the criteria of a person actually conducting business:

- Lack of the resources necessary for this (assets, personnel), payment of taxes in the minimum possible amount or in incomplete amount (resolutions of the Arbitration Courts of the Moscow District dated 05.30.2017 No. F05-7043/2017 in case No. A40-181608/2016, dated 30.05 .2017 No. F05-6970/2017 in case No. A40-208019/2016, dated 05.15.2017 No. F05-5962/2017 in case No. A40-74889/2016, Far Eastern District dated 08.14.2017 No. F03-2718/2017 in case No. A51-27634/2016).

To learn how the volume of the tax burden is determined and what its values are considered to be underestimated, read the article “Calculation of the tax burden in 2021 - 2020 (formula)” .

- The presence of a mass registration address, the absence of expenses characteristic of ongoing business activities, the disproportion of cash flows on accounts and the amount of taxes paid (resolution of the Arbitration Court of the Moscow District dated May 29, 2017 No. F05-6622/2017 in case No. A40-119724/2016).

- The presence of a predominantly transit nature of the movement of funds across accounts, nominal property status with a significant variety of activities declared for implementation, lack of consistency in receipts and expenditures of money (resolutions of the Arbitration Courts of the Moscow District dated May 25, 2017 No. F05-6702/2017 in case No. A40- 166522/2016, Volga-Vyatka District dated July 17, 2017 No. F01-2731/2017 in case No. A43-21051/2016).

- Lack of personnel, necessary assets (office, warehouses, equipment, transport, including leased ones) and documents confirming the provision of delivery services, presence of signs of one-day existence of counterparties, presence of a transit nature of cash flows, filing of tax reports indicating the minimum data in it, distortion of information when issuing permits to carry out activities (resolutions of the Arbitration Courts of the Moscow District dated 05.19.2017 No. F05-6215/2017 in case No. A41-66000/2016, Far Eastern District dated 08.09.2017 No. F03-2797/2017 on case No. A73-9509/2016, Northwestern District dated August 10, 2017 No. F07-5611/2017 in case No. A66-5287/2016).

- The presence of one-day companies among the counterparties, non-payment of taxes, lack of the necessary labor and property resources necessary to conduct business expenses, the presence of transactions with significant sums of money that are not confirmed by the counterparties (resolutions of the arbitration courts of the Moscow District dated 04.05.2017 No. F05-5426/2017 in the case No. A40-143250/2016, Central District dated 08/03/2017 No. F10-2817/2017 in case No. A09-9845/2016).

The arguments taken into account by the courts indicate that the justification for exercising due diligence should not be limited to asking the counterparty for constituent documents, a copy of the latest statements and an extract from the Unified State Register of Legal Entities. It is also necessary to collect other information about him. For example, check what his business reputation and solvency are, assess the presence of a risk of non-fulfillment of obligations, make sure that he has real resources to actually carry out the activities agreed upon in the relationship and has the right to conduct them.

Article 54-1 of the Tax Code of the Russian Federation and due diligence

After the workshop and discussion on the issues of unjustified tax benefits that took place in Support, a desire was born to prepare brief conclusions on the issue of the consequences of transactions with counterparties, which, when audited, turn out to be companies that are not in good working order in the tax sphere, because so-called “fly-by-night” tax risks and accents, which first of all need to be paid attention to. We have tried to present the main arguments, reducing their totality to an algorithm that, in our opinion, should be useful.

Part 1. Brief description of a typical dispute.

Very often, the basis for additional assessment of VAT, corresponding amounts of penalties and prosecution is the conclusion that the taxpayer has unjustifiably applied tax deductions for transactions related to the purchase of goods from companies that are not correct in the tax sphere and do not declare the relevant transactions or when fulfilling this declaration obligation reduce the amount of tax calculated on them for tax deductions for which there is no right, reducing the amount of tax payable to zero.

In a number of cases, the risks of a counterparty’s malfunction in the tax sphere are transferred to the taxpayer due to the presence of suspicious signs that may indicate the actual “control” of a shell company by the taxpayer. However, it should be recognized that this justification is not predominant.

As a rule, the basis for refusal of a tax deduction is the judgment that the counterparty is a person involved formally, since he, not carrying out entrepreneurial activities, did not have the opportunity to execute the transaction, and the real supplier was another entity, which the taxpayer should have known about , if he had exercised due diligence in his selection.

Very often, abuses occur where and when the actual manufacturer or supplier is not a VAT payer, and an intermediary, who applies the general tax regime and does not have the right to exempt the transactions he carries out from VAT, is built in to create the right to deduction.

Abuses also occur in the case of an increase in the cost of the purchased goods and transfer of part of the profit into the gray zone by cashing it through an intermediary. How to figure out - where are the abuses of which the taxpayer is guilty, due to which he must bear the corresponding negative consequences, and where are the situations of unjustified shifting of the consequences of a tax malfunction of one person to another.

Very often we see a very common position according to which a sufficient basis for denying the right to deduct VAT is the establishment of the fact that disputed transactions for the supply, performance of work, or provision of services were executed by another entity , and not by the person on whose behalf the relevant agreements were signed. This defect is regarded as evidence of the unreliability of documents , the absence of real business transactions with the specified counterparties and is a sufficient basis for denial of the right to deduct VAT.

Is it possible to defend against this statement by citing the exercise of due diligence when choosing a counterparty? Has this opportunity been lost under the new Article 54-1 of the Tax Code, thanks to which a general anti-evasion rule has appeared in tax legislation?

Very often we hear the statement that when it is determined that a company that was a party to a transaction is unable to perform, due diligence in selection is irrelevant.

Referring to the exercise of due diligence is possible only if the execution of the transaction is confirmed by the counterparty, and the controversial situation comes down solely to the tax malfunction of the counterparty and the solution to the question of whether the taxpayer should be responsible for it. In this sense, according to supporters of the stated point of view, due diligence should be manifested in tax diligence and in providing the taxpayer with the opportunity to prove that he should not have known about violations committed by the counterparty in the tax sphere. But this issue - about exercising due diligence - is discussed only when performance has been received from the counterparty. In the absence of such, according to supporters of this point of view, there are no grounds for applying the due diligence test. In this case, the basis for loss of the right to deduction is seen in the of documentary evidence of the disputed transactions , which is expressed in the absence of appropriate documents - contracts, invoices, invoices issued with the persons who carried out the actual execution.

Is it correct? We'll look into it further.

Part 2. Judicial doctrines. Algorithm based on the findings of the higher courts. The reality of performance.

The approach set out in Part 1 about the applicability of the due diligence test only if a party to the transaction provides execution is formal and does not provide protection. The position that in order to deny the right to deduct VAT it is enough to establish that the execution of the transaction was carried out by another entity, and not by the person specified in the agreement, seems controversial.

The main approaches of the Supreme Arbitration Court of the Russian Federation on the issue under consideration were set out in paragraph 10 of the Plenum Resolution No. 53 dated October 12, 2016 “On the assessment by arbitration courts of the validity of taxpayers receiving tax benefits,” as well as in the Presidium Resolutions dated April 20, 2010 No. 18162/09 in the JSC case "Murom Switch Plant", dated 05/25/2010 No. 15658/09 in the case of JSC "Koksokhimmontazh-Tagil", dated 06/08/2010 No. 17684/09 in the case of IP Kotov, dated 07/03/2012 No. 2341/12 in the case of JSC "Kama Plant" Concrete goods."

The approaches of the Supreme Arbitration Court of the Russian Federation were adopted by the Supreme Court of the Russian Federation in the ruling of the Judicial Collegium for Economic Disputes dated November 29, 2016 No. 305-KG16-10399 in the case of Tsentrregionugol JSC. Based on this definition, the Presidium of the Supreme Court of the Russian Federation formed an approach that was reflected in paragraph 31 of the review of judicial practice for the 1st quarter of 2021.

Based on these positions, the following algorithm for assessing transactions performed with counterparties that do not fulfill their tax obligations can be formulated.

Firstly, given the reality of fulfillment, the taxpayer has the right to claim a VAT deduction for a transaction with a counterparty who does not fulfill tax obligations, as well as take into account expenses in the relevant part (in the part exceeding the market value of the purchased goods, works, services), if it is proven , that the taxpayer should have known (could not but have known) about the tax malfunction of the counterparty due to the legal or actual control of the latter. In other words, the taxpayer bears the negative consequences of a counterparty’s failure to fulfill tax obligations if it is proven that the taxpayer himself controlled this counterparty (used him as an intermediary, built a chain of transactions, including the intermediary in the relationship between himself and the person with whom there was a valid agreement on the supply of goods , performance of work, provision of services).

Secondly, to exclude facts of tax fraud and record transactions that were not actually performed (goods were not supplied, work was not performed, services were not provided), an assessment of the reality of execution is necessary. At the same time, it is important to understand that the reality of execution is understood as the fact that the transaction was actually performed, and not its execution by the person specified in the contract as the counterparty. It is in this aspect that a mistake is often made, and a different content is put into the concept of reality - it is understood as a category indicating the receipt of performance specifically from the person named in the contract, which does not correspond to the practice of the highest courts.

Thirdly, the Supreme Arbitration Court of the Russian Federation, distinguishing between the categories of “reality of performance” and “provision of performance by a person who is not a counterparty to the transaction,” pointed out the inadmissibility of a formal approach, which will occur if the unreliability of documents is considered as a self-sufficient basis for refusal.

According to the highest courts, the execution of an agreement and documents confirming its execution, invoices on behalf of the counterparty by an unidentified person or signed by a person who denies their signing and the presence of his authority as a manager (with reference to the unreliability of registration of information about him as a manager in the Unified State Register of Legal Entities ), in itself is not a sufficient basis for denying a taxpayer the right to deduct VAT and account for expenses.

Fourthly, given the reality of execution (goods delivered, work performed, services provided), an assessment of due diligence in choosing a counterparty is necessary.

When applying this test, due diligence should be understood as commercial diligence, which involves the application of standards for verifying the business reputation, serviceability, ability to perform, and solvency of the counterparty. These are the same assessment standards accepted in business practice that are used when checking any counterparty when concluding a significant, significant transaction, and in case of violation of which the director or manager will be liable to society for losses caused to him resulting from the counterparty’s failure to fulfill the transaction.

To understand this standard of verification, you can refer to the approaches set out in the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 No. 62 “On compensation for losses by persons included in the bodies of a legal entity.”

Giving explanations about what actions can be qualified as dishonest or unreasonable, the highest court indicated that such actions should include, in particular: 1) knowledge by the director of a significant disadvantage of the terms of the transaction or a known malfunction of the counterparty, or the establishment that the director should have known about the specified conditions, 2) failure to take steps to obtain the necessary information before the transaction, which are usual for business practice, 3) completion of the transaction in violation of internal approval procedures or contrary to the business strategy (high-risk, non-core transaction).

In revealing the standard of commercial due diligence in relation to tax disputes, the Supreme Arbitration Court of the Russian Federation and the Supreme Court of the Russian Federation proceeded from the following.

The tax authority must prove and provide a set of suspicious signs indicating that the taxpayer, based on the conditions and circumstances of the execution and execution of the transaction, should have known that the counterparty under the agreement is a person who does not carry out actual business activities, and that the actual execution will be carried out by another person, and not the counterparty to the transaction (due to which the documents executed on behalf of such a “counterparty” are forged).

Contesting the arguments of the tax authority, which may indicate this knowledge, the taxpayer has the right to give arguments to justify the choice (business reputation, solvency of the counterparty, risk of non-fulfillment of obligations and the provision of security for their fulfillment, availability of the counterparty with the necessary resources and relevant experience) and facts indicating knowledge about how (at the expense of what resources, with the involvement of which co-executors, etc.) the execution should be carried out. Evaluation of the choice according to the specified criteria should lead to the conviction that the taxpayer could not know that the person acting as a counterparty is used by other persons carrying out the actual execution to formalize controversial transactions and conceal by these persons income from taxation by withdrawing them completely or in a significant part to an organization that does not declare tax liabilities.

It should be noted that the highest courts have never required the taxpayer to check the tax efficiency of the counterparty, understanding that the information on the basis of which such an assessment could be made is not available to the taxpayer.

But even this reason was not the main one.

The main thing is that the taxpayer should not suffer adverse consequences associated with the tax failure of the counterparty, and, accordingly, in principle, no obligation can be assigned to him to check whether the counterparty properly takes into account transactions when calculating the tax base and whether it pays taxes. After all, as soon as the duty to verify begins to be assigned, consequences for failure to fulfill this duty must also arise. The Supreme Arbitration Court of the Russian Federation proceeded from the fact that tax administration is exclusively the responsibility of the state, and the burden of fulfilling this responsibility cannot be shifted to taxpayers.

Fifthly, even if due diligence is not shown, then if the execution is real, the costs incurred are subject to accounting for tax purposes. This conclusion is based on the provisions of Article 31 of the Code, since in the absence of documents, the calculation method provided for in this article for determining the tax liability must be applied.

For VAT, when establishing a failure to exercise due diligence, a different solution was developed - the right to deduction is not granted, since deductions, unlike expenses, are not determined by calculation.

It should be recognized that from the specified general rule on the non-application of a deduction in full, it seems that an exception could be made when it was established that the counterparty that was faulty in the tax sphere performed only an intermediary function and, accordingly, the source for the non-application of the deduction from the taxpayer was not formed in budget only in the part attributable to the increase in the cost of execution by the intermediary in comparison with the cost at which the product (result of work, service) was sold by the direct supplier. If the supplier calculated VAT for a corresponding transaction made in favor of an intermediary that was faulty in the tax sphere, then a source for reimbursement in the budget was created in this amount, and a deduction in the corresponding part should be provided to the taxpayer.

The indicated position on an exception to the general rule on the non-application of deductions in full was not formed at the level of the highest courts, since it was faced with the need to clearly establish the chain of movement of goods, which presented a significant difficulty in the absence of an electronic accounting system similar to the ASK VAT. With the advent of this system and the elimination of technical difficulties, there are no obstacles to the application of the stated position.

Part 3. Due diligence as commercial prudence.

When entering into legal relations and making transactions, participants in the turnover are convinced, first of all, that they are truly an economic entity engaged in economic activity and capable of fulfilling the obligations assumed within the framework of this activity.

The conduct of activities is objectively reflected in the company’s business history and its fame in the relevant market segment, in public positioning and advertising promotion, in business reputation, experience, in the presence of executed contracts and in the ability to provide recommendations from counterparties, in the presence of a place of business (office, industrial site, etc.), own assets or the possibility of attracting co-executors within the framework of established contractual relations, in accordance with the nature of the obligations assumed, their size, scale, cost of execution and the period of existence of the company (bearing in mind that in each area business there is an idea of the dynamics of its development and the scale achievable at each stage).

This understanding of the existence of a business entity, and not a shell of a legal entity without assets and guarantees, is formed, which is important, not for tax purposes, but for confidence that performance will be obtained, and in case of grounds for applying liability measures, recovery of losses from the counterparty there will be a subject capable of answering for debts.

This is the commercial choice, justifying which, in the event of losses to the company due to improper execution of the transaction by its counterparty, the manager of the company, its director, will be able to give arguments, answering to the company and its shareholders, participants, why of the possible, potential entities operating in the market in the relevant area, the exact counterparty was chosen with whom the controversial transaction was made, which resulted in losses due to the failure of the counterparty.

The standards for assessing the validity of a commercial choice are the same for both a tax dispute and a dispute over the recovery from a director of losses caused as a result of non-execution or improper execution of a transaction, the decision to enter into which is assessed as unreasonable (prior to making the decision, no actions were taken to obtain the necessary information, which are usual for business practice, the transaction was completed in violation of internal approval procedures, the transaction was completed contrary to the business strategy (overly risky, non-core).

It should not be forgotten that tax disputes related to the assessment of due diligence arise when the validity of the commercial choice is questionable from the position of a reasonable average entrepreneur, and the degree of trust provided based on the nature of the obligations and risks assumed borders on the immaturity of a minor.

As a rule, organizations embedded in the chain between entities carrying out actual execution and created for an illegal purpose - to withdraw profits into the gray zone and cash them out - cannot demonstrate a business history of doing business, and their credibility and excess risks cannot be explained due to the absence of property from which a reasonable creditor expects to receive satisfaction in the event of losses due to improper performance, business experience, credit of trust provided by participants or third parties by providing security for the execution of the transaction. Such companies, in justifying their experience and the effectiveness of commercial practice, cannot refer to a significant period of activity, as well as to the experience of their founders, since they are founded mainly by individuals who do not have such experience.

Justifying the artificiality of embedding an intermediary is a matter of proving suspicious signs that indicate the unwiseness of the commercial choice. This is evidence, carried out, inter alia, taking into account the assessment of the circumstances of the transaction (circumstances that may indicate that the agreement to complete the transaction was reached between the relevant persons without the participation of a nominal intermediary who is not conducting business, and the execution of the transaction by these persons by signing papers with the participation of the specified intermediary did not correspond to the actual agreements), as well as its execution (circumstances indicating interaction in the provision and acceptance of execution exclusively by the employees of the specified persons in the absence of the participation of representatives of the intermediary).

Part 4. Analysis of Article 54-1 of the Code and the possibility of its application to past relationships to assess transactions and transactions completed before the entry into force of this norm.

On August 19 of this year, general anti-evasion rules came into force, reflected in Article 54-1 of the Code on the limits of taxpayers’ exercise of rights when calculating the tax base or the amount of tax (fees, insurance contributions).

The essence of these rules boils down, firstly, to the establishment of a prohibition on distorting information about the facts of economic life , about objects of taxation and, secondly, to the need to perform two tests in relation to transactions (operations): the business purpose and the execution of the transaction by its party .

While the prohibition on misrepresentation of transactions and the business purpose test are not in doubt, the proper party test cannot reach the same conclusion.

In our opinion, the legislator, by including the proper party test in the law, tried to consolidate a formal approach, which, as stated above, was not supported by the higher courts.

This assumption is based on the absence of a “due diligence” test in the analyzed norm. The application of the criterion of “execution of a transaction by a party to the agreement” is not made dependent on the assessment of the extent to which the taxpayer, when making a transaction and making a commercial choice, could have known that the organization on whose behalf the agreement was signed was not a business entity and was used by unscrupulous persons as “paper” company for concealing income and processing transactions, the execution of which was provided by another person.

The substantive test of due diligence, based on commercial choice criteria accepted in business practice, which assumed the possibility of protection and exclusion of negative consequences in the event of a tax failure of the counterparty, has been replaced by a formal test that does not allow such protection.

This understanding is expressed in the letter of the Federal Tax Service of Russia dated August 16, 2017 No. SA-4-7-/ [email protected] “On the application of the norms of the Federal Law dated July 18, 2017 No. 163-FZ “On Amendments to Part One of the Tax Code of the Russian Federation.”

According to the tax department:

“When applying Article 54-1 of the Code, it should be borne in mind that for tax purposes, transactions (operations) can be taken into account subject to the obligatory observance of the condition that the transaction (operation) itself was carried out by the counterparty. Failure to comply with this requirement entails refusal to account for such transactions (operations) for tax purposes. In this regard, during tax control activities, special attention must be paid to the study of circumstances confirming or refuting the execution of a transaction (operations) by the counterparty.

If at least one of the two criteria defined in paragraph 2 of Article 54.1 of the Code is not met (one of these is the test of execution of the transaction by its party), the taxpayer must be denied the right to account for expenses incurred, as well as statements for them for deduction (offset) of amounts VAT in full."

From the above understanding, it follows that the legislator has tightened its approaches to the issue under consideration, which consists in the fact that if the proper party test is not met, there should be a denial not only of VAT deductions, but also of income tax expenses. The consequence of this refusal will be the collection into the budget of 38% (18% - VAT and 20% - income tax) of the cost of execution provided under the disputed transaction.

An approach similar to that stated regarding the denial of the right to account for expenses, as well as the deduction of VAT in full, is also duplicated in the letter of the Federal Tax Service of Russia dated October 31, 2017 No. ED-4-9 / [email protected] “On recommendations for the application of Article 54.1 of the Tax Code of the Russian Federation " Nevertheless, we believe that there is room for discussion, discussion and defense of a point of view based on established judicial practice.

Article 54-1 of the Code itself does not regulate the consequences of failure to comply with the requirements specified therein in relation to certain types of taxes and does not exclude the need to use the calculation method when there is no documentary evidence of transactions in a situation where there are no doubts about the actual execution.

Accordingly, contained in Article 54-1 of the Code, the prohibition of reducing the tax base, the amount of VAT should be understood as a prohibition of reducing in accordance with the information contained in the primary documents due to their unreliability (for example, due to the fact that the legal basis of the transaction was distorted and it is necessary to re-qualify this basis for tax purposes based on the economic essence of the transaction, or due to the unreliability of the document due to its preparation on behalf of the person who did not provide the performance, etc.).

But a caveat needs to be made.

The indicated unreliability of information about a business transaction is not fatal; it can be cured by the calculation method. The conclusion about the need to use this method was made by the Supreme Arbitration Court of the Russian Federation in the Resolution of the Presidium dated 07/03/2012 No. 2341/12 in the case of JSC “Kama Precast Concrete Plant” and was further enshrined in paragraph 8 of the Plenum Resolution dated 07/30/2013 No. 57 “On some issues arising when arbitration courts apply part one of the Tax Code of the Russian Federation” for cases of lack of documents or recognition of them as inadequate.

In this regard, we believe that even in the conditions of application of Article 54.1 of the Code, there are still grounds for accounting for expenses for a transaction performed by an entity other than the person specified in the contract, in the commercial choice of which due diligence was not exercised. As for VAT and the development of judicial practice in the direction of developing an exception to the general rule, namely the approach to the admissibility of deducting tax calculated on a transaction by the person who carried out the actual performance in favor of the taxpayer (which is revealed due to the elimination of “fictitious” intermediaries from the chain of transactions), then On this issue our forecast is pessimistic. The possibility of developing this position is not excluded, but it is unlikely.

It should be noted that the new assessment standards (more stringent standards, if we are guided by the understanding of the Federal Tax Service of Russia) were introduced with retroactive force , since they are subject to application to past periods, the verification of which began after the entry into force of Article 54-1 of the Code. Such an extension, of course, raises questions from the point of view of the constitutionality of the norm, but until it is recognized as unconstitutional, the courts will apply it to past relations, each time defining the limits of such application in their own way.

In this regard, in the context of the application of formal tests, it is necessary to develop a standard for concluding contracts and checking counterparties that excludes or minimizes the likelihood of executing a transaction with an entity that could subsequently be recognized as a person who did not carry out the execution.

Despite the stated position of the Federal Tax Service of Russia, we believe it is possible to assert that the application of the due diligence test will be preserved due to the conservatism of judicial practice and the inadmissibility of a formal approach without assessing the actual circumstances of the dispute, in which the right to judicial protection is recognized as violated, as has been repeatedly stated by the Constitutional Court of the Russian Federation .

The basis for this judgment is also the approaches of the Federal Tax Service of Russia, which, whether willingly or not, is forced, when determining the conditions for applying the proper party test and proving formal document flow, to reproduce the evaluation criteria that make up the content of the commercial diligence test.

For example, the Federal Tax Service of Russia in a letter dated October 31, 2017 No. ED-4-9/ [email protected] “On recommendations for the application of Article 54.1 of the Tax Code of the Russian Federation” indicates “the need to assess the extent to which the document flow was atypical, to what extent the behavior of the parties to the transaction ( transactions), officials of the taxpayer when concluding, supporting, and documenting the results of transactions (operations) complied with business customs.”

Along with the prohibition of distortion of information about completed transactions and the consolidation of tests of the business purpose and the proper party, paragraph 3 of Article 54.1 of the Code reflects the provisions according to which the signing of primary accounting documents by an unidentified or unauthorized person, violation of tax legislation by the taxpayer’s counterparty cannot be considered as an independent basis for recognition of the reduction of tax liability as unlawful .

These provisions, of course, can be applied to past relationships, including for the assessment of transactions, operations analyzed during inspections initiated before August 19 of this year, they can also be referred to when considering current cases in the courts. And it’s not even a matter of paragraph 3 of Article 5 of the Code on the application of tax legislation that establishes additional guarantees for the protection of taxpayers’ rights, with retroactive effect. The fact is that the provisions under consideration do not constitute new regulation; they essentially consolidate the approach existing in the practice of the Supreme Arbitration Court of the Russian Federation, according to which due diligence in the choice cannot be understood as a requirement to assess the tax serviceability of the counterparty, and, as a consequence, the circumstance The extent to which the counterparty complied with tax laws has no legal significance with this approach.

Part 5. Constitutionality of judicial doctrines. The possibility of challenging Articles 169, 252 of the Tax Code of the Russian Federation, in the interpretation given to them in law enforcement practice, as not corresponding to the Constitution of the Russian Federation.

The very legal position of the Supreme Arbitration Court of the Russian Federation and the Supreme Court of the Russian Federation on the admissibility of denial of the right to a tax deduction for VAT when making a transaction with a counterparty that is faulty in the tax sphere, if it is “under the control” of the taxpayer and the application in this case, due to the controllability of the presumption of existence collusion, coordination of actions and , as a consequence, the receipt by the taxpayer of an illegal effect , expressed in the appropriation of the amount of VAT not paid by the counterparty, is beyond doubt.

It also appears that there are no grounds for recognizing the interpretation of the analyzed norms as inconsistent with the Constitution of the Russian Federation, expressed in the admissibility of denial of the right to a tax deduction for VAT in the event of a taxpayer’s failure to exercise prudence in choosing a counterparty , when such prudence is understood as a due choice of a counterparty made taking into account the assessment of the risks of non-fulfillment, improper fulfillment of the obligation, as well as guarantees of actual satisfaction of claims in the event of the occurrence of grounds for liability of the counterparty.

The choice must be explainable precisely from the point of view of business practice and protection of the interests of the taxpayer as a creditor, as a participant in civil transactions.

If the choice is inexplicable, there are grounds for presuming knowledge by the taxpayer that the organization with which the contract is being drawn up is not an entity conducting business, is being built artificially, and the documents formalizing the transaction and execution on it are forged and cannot be considered as a basis for VAT deduction. As a result, the question may be raised that the transaction was not executed (services were not provided, work was not performed, goods were not supplied, and payment was made in the absence of a legal basis for this) or about the imaginary intermediary function and the groundlessness of the payment in that part, in which it exceeds the performance received by the person who actually provided the performance.

The presence of a sufficient set of suspicious signs is the basis for placing the burden of proving the reasonableness of the commercial choice, and, as a result, refuting the presumption that the taxpayer received an illegal effect, expressed in the misappropriation of the amount of VAT, on the taxpayer.

These approaches, from the point of view of the need to fulfill the requirement for documentary exposure of expenses and the right to deduct VAT, enshrined in Articles 169 and 252 of the Tax Code of the Russian Federation, do not raise any doubts. At the same time, the right to judicial protection cannot be considered violated, since the application of the stated approaches presupposes an essential assessment - to what extent the taxpayer, based on the conditions and circumstances of the execution and execution of the relevant transaction, should have known about the counterparty providing false information or about the forgery of documents, or about the that the counterparty to the contract is a person who does not carry out actual business activities.

Formal approach , due to which the loss of the right to deduct VAT and to account for expenses would occur automatically if the documents are unreliable (due to their execution on behalf of the entity that did not carry out the execution of the transaction, or when a false signature or signature is made on the documents on behalf of a person , denying his participation in the activities of the counterparty and the existence of the powers of a director due to the unreliability of information about him as a director in the Unified State Register of Legal Entities), regardless of the assessment of how much the taxpayer could know about these circumstances, was considered unacceptable.

Thus, the stated legal positions themselves cannot be recognized as an interpretation of Articles 169, 252 of the Tax Code of the Russian Federation, which does not comply with the Constitution of the Russian Federation.

The question of how correctly these approaches are applied in specific cases, whether judicial errors are made, as related to the assessment of the factual circumstances of the case, cannot be the subject of constitutional proceedings.

Cases on assessing the validity of applying the right to deduct VAT for transactions in which the taxpayer actually received the corresponding performance are cases based on an assessment of the totality of indirect suspicious signs that give reason to believe that the taxpayer has received an illegal effect, expressed in the misappropriation of the amount of VAT unpaid by the counterparty, in view of:

1) establishing circumstances indicating the “ control ” of the counterparty to the taxpayer, or

2) the choice of a counterparty, inexplicable from the point of view of commercial turnover, and the presumption , as a consequence, of the taxpayer’s knowledge that the organization with which the contract is being drawn up is not an entity conducting business , is built artificially, and the documents formalizing the transaction and execution thereunder are forged .

Given the stated grounds, the fictitiousness of the intermediary function and the groundlessness of the payment are seen to the extent that it exceeds the performance due and received by the person who actually provided the performance.

Part 6. Constitutionality of Article 54-1 of the Tax Code of the Russian Federation.

We leave the answer to this question to our readers and for subsequent discussions at the seminars held by the “Support” project.

We are waiting for everyone! All the best to everyone and professional success!

The next discussion of pressing issues on the problems of defense against charges of abuse of rights in the tax sphere will take place in Moscow, December 20-22 https://podderzhka.org/nnv/.

How to exercise due diligence when choosing a counterparty in 2020-2021

A taxpayer entering into a relationship with another counterparty should check it:

- for legitimacy (presence in the Unified State Register of Legal Entities (USRIP), absence of a mass registration address and a disqualified manager, availability of permits necessary to conduct the relevant activities);

- the reality of the activity being carried out (actual location at the place of registration, the presence of a manager with the necessary powers, physically existing offices and warehouses at the specified addresses, necessary equipment and transport, personnel, a valid current account, the presence of information in the media and the Internet);

- reliability (absence of non-filers, tax evaders, bankrupts, persons involved in legal proceedings in connection with their non-payments or work with one-day companies, availability of recommendations from business partners, duration of activity and maintaining relationships with the same partners ).

When checking, use the services from the Federal Tax Service.

However, you should not be limited to the above, since any additional information (including, for example, correspondence preceding the conclusion of the contract or conducted during its execution, or minutes of a meeting of managers) will serve as confirmation of the reality of the existence of the counterparty and the actual conduct of those activities, the results which the taxpayer will take into account.

It is preferable to have all data received about the counterparty in the form of documents (originals, copies, printouts from websites, screenshots of Internet pages, photographs, emails, advertising materials, audio and video recordings) and store them formed into a file (dossier).

You will find more practical advice on due diligence and verification of counterparties in the Ready-made solution from ConsultantPlus. Get trial access to the system for free and proceed to the material.

How to act

Now about how to exercise due diligence when choosing a counterparty. It can be carried out in the following directions.

Official registration

All legal entities (IPs) officially conducting financial and economic activities must be mentioned in the Unified State Register of Legal Entities - Unified State Register of Legal Entities (USRIP). You can compare the TIN provided by the counterparty with the TIN indicated on the official website of the Federal Tax Service.

Also on the portal of the Tax Service of the Russian Federation you can verify:

- whether the director (representative) of the counterparty company is a disqualified person;

- whether the counterparty is one of the persons who are subject to exclusion from the Unified State Register of Legal Entities (USRIP).

In addition, you definitely need to request copies of state registration certificates and tax registration.

Also see “Checking the counterparty, how to do this only using the TIN?”.

Information in the media and the Internet

If the counterparty is an active legal entity (IP), then information about it can be easily found on the World Wide Web.

In addition, there are specialized services, including on the Federal Tax Service website, that provide information on state registration of organizations and merchants:

- OGRN;

- actual location;

- information about management (full name);

- average number of personnel;

- occupation;

- types of services provided;

- revenue, etc.

Internet pages (screenshots) must be immediately printed and saved. This will serve as evidence of due diligence. In addition, we recommend saving advertising brochures, emails, photographs of the counterparty’s advertising signs, etc.

Verification of counterparty representatives

In addition to checking the counterparty itself, it is necessary to find out the powers of the person who acts before you on behalf of this organization. For this purpose, you should request from the counterparty copies of documents on senior management and the appointment of the chief accountant.

If the contract can be signed simply by an authorized representative, then you need to check his power of attorney for this. Afterwards, check the information with his passport details, if he provides them. Please note: you do not have the right to demand that a person provide personal data.

Contractor's documents

When conducting activities that require licensing, you should request documents confirming that the counterparty has the appropriate permit. It would be better if you keep a copy of the license.

Also, based on business practice, it is necessary to check the following:

- current accounts;

- recommendations and information confirming reputation;

- availability of qualified personnel;

- ownership rights to office and other premises;

- annual volumes of completed contracts.

In addition, you can check whether the counterparty has appeared in litigation related to shell companies.

The best option is to divide all counterparties into risk groups and, in accordance with this, collect sets of documents for them.

Read also

29.05.2017

Justification for choosing a counterparty to the Federal Tax Service: sample

The presence of such a dossier will help you easily justify the choice of a specific counterparty to the Federal Tax Service. The documents present in it will not only make it possible to correctly formulate all the grounds necessary for the argument, but will also serve as an appendix (in copies) to the text of such an explanation.

The justification for choosing a counterparty does not have a specific form. It will need to be drawn up in the form of a regular letter addressed to the Federal Tax Service, on the form used by the taxpayer for such documents. The main text part of it will be devoted to the argument itself. For example, it might look like this:

“Variant LLC showed due diligence when choosing Soyuz LLC as a counterparty, taking actions to obtain:

- copies of the counterparty's constituent documents, its accounting records for the year preceding the year of conclusion of the agreement, tax returns for profit, VAT, property tax for the last 4 reporting periods;

- originals of certificates issued by Soyuz LLC from the Federal Tax Service on the absence of tax arrears and from the bank on the flow of funds on accounts for the last six months;

- copies of documents confirming the authority of the manager and chief accountant;

- extracts from the Unified State Register of Legal Entities, information from the Federal Tax Service website about the absence of disqualified persons in the management of the counterparty and the non-classification of the registration address as a mass one;

- screenshots of Soyuz LLC website pages with a description of the types of work it performs, the technologies used and the personnel involved in them;

- reviews from representatives of Mir LLC and Grad LLC about the quality of work performed for their Soyuz LLC and the fulfillment of warranty obligations;

- protocols of negotiations between the heads of Variant LLC and Soyuz LLC that preceded the conclusion of the agreement;

- photographs of the counterparty’s office, production and warehouse premises taken at the place of its registration.”

Enclosures to such a letter will be copies of the documents listed in it.

Stages of verification of counterparties

Practice shows that it is advisable to carry out such a check in several stages:

Stage 1. Request from the company certified copies of constituent documents

As a rule, this is a standard package that includes:

- OGRN and TIN certificates;

- current version of the charter;

- documents confirming the authority of the manager: a decision or protocol on appointment, an order for the general director to take office, an order for the extension of his powers;

- extract from the Unified State Register of Legal Entities;

- licenses, SRO approvals, if the company conducts regulated activities;

- power of attorney for the representative if he signs the agreement.

It is worth noting that any company can independently obtain information from the Unified State Register of Legal Entities for its counterparty through the website of the Federal Tax Service of Russia.

In addition to the specified list of documents, an organization can request from its potential partner:

- accounting and financial statements for the last year,

- a copy of a bank card with sample signatures and a seal imprint.

These documents, in the event of a dispute with the tax authority, will strengthen the company’s position and its arguments about exercising due diligence.

Stage 2. Check the company through special services

Most of these services are provided by the Federal Tax Service of Russia. These are, for example, registers of addresses of mass registration, disqualified persons, information about persons in respect of whom the court has established the fact of impossibility of participation in the organization.

You can check the counterparty through the State Registration Bulletin. It contains information about the upcoming exclusion of inactive legal entities from the state register.

You can use the websites of the courts, the Federal Bailiff Service, the Fedresurs, which display legally significant information about the facts of the activities of companies and individual entrepreneurs, information about bankruptcies, as well as a register of unscrupulous suppliers.

Court practice confirms that checking a counterparty through the official website of the Federal Tax Service of Russia proves the taxpayer’s due diligence (for example, Resolution of the Administrative Court of the North Caucasus District dated August 23, 2021 No. F 08-5352/2017).

It should be noted that the “Transparent Business” service of the Federal Tax Service of Russia is scheduled to begin operation on August 1, 2021. This service will become another tool for checking counterparties. With the help of this service, organizations will find out the amount of arrears and debts of their counterparties in terms of penalties and fines, receive data on tax offenses, and the average number of their employees.

Stage 3. Analyze information about the company posted on the Internet, check its business reputation.

When deciding whether to start cooperation with a new organization, it is advisable to look at its official website, advertisements, and receive reviews and letters of recommendation from its partners. In particular, it is useful to study information about the experience of performing similar contracts, check the business reputation and solvency of the counterparty (Resolution 9 of the AAS dated May 21, 2021 No. 09 AP-18025/2018, AS of the West Siberian District dated March 15, 2021 No. F 04-281 /2018).

It is better to document all actions. For example, take screenshots of the official website’s Internet pages, indicating the dates when the monitoring was carried out.

Stage 4. Take advantage of special programs

The advantages of such a check are the efficiency and clarity of information about the counterparty, which is presented in the form of a single report. Special programs additionally show the connections of companies and their leaders, which is also a definite plus.

The legality of checking future business partners in exactly this way is confirmed by the courts: resolutions 16 AAS dated April 25, 2018 No. 16 AP-989/2018, 15 AAS dated July 6, 2021 No. 15 AP-2456/2017.

Stage 5. Get additional information about the counterparty company

Tax authorities and courts, having discovered signs of a shell company in an organization, check whether it has labor and material resources confirming that the company really exists and can fulfill its obligations under the transaction on its own.

If you want to confirm that you exercised due diligence when choosing a counterparty, then it is advisable to ask your potential partner:

- certificates of the number of employees to confirm labor resources;

- copies of lease agreements;

- certificates of ownership;

- an extract from the Unified State Register of Real Estate to confirm material resources.

If it was not possible to obtain such documents from the counterparty, and later it turned out that it does not have the necessary resources, a conscientious taxpayer can give the following effective argument in its favor: the absence of the enterprise’s own production and human resources does not in itself indicate the fictitious nature of the transactions. In this case, the organization remains able to attract the necessary capacity from third-party companies.

In the absence of other evidence, the court does not confirm the unjustified tax benefit (Resolution 9 of the AAS dated March 21, 2021 No. 09 AP-7457/2018).

Practice shows that inspectors, when identifying technical companies, conduct a survey of legal addresses to confirm that the company does not have an office at its registered address.

Therefore, when visiting a counterparty’s office, it is advisable to take photographs of its interior premises and signs, where the name of the organization and other identifying features would be visible, as well as a photo of the business center in which the office is located.

In case of a dispute, the main argument of the taxpayer is the fact that the company is located at the specified address during the period of validity of the contract. The weight of this argument is confirmed in Resolution 12 of the AAS dated August 17, 2021 No. 12 AP-8472/2017.

Stage 6. Analyze the product market and commercial offers on it

In a letter dated March 23, 2021 No. ED-5-9/ [email protected] , the Federal Tax Service of Russia emphasized that due diligence when choosing a counterparty will be proven by documents confirming the results of the taxpayer’s monitoring of the relevant product market, assessment of potential partners, and justification for choosing a specific organization.

Therefore, when deciding on cooperation, it is advisable to study the product market and price offers on it. And the results of such analysis should be recorded in writing. This will confirm the economic feasibility of the decision to cooperate with a specific company.

As a rule, tax authorities analyze the procedure for selecting counterparties that the taxpayer used and assess the commercial attractiveness of concluded transactions.

Stage 7. Generate a final report on the verification of the counterparty

The main rule when confirming your due diligence is to document all actions taken to verify a potential counterparty.

There are no regulatory requirements for recording the results of audits of companies. What documents the counterparty has the right to require when concluding an agreement is described above.

How to submit an inspection report?

In the eyes of tax authorities, the advantage of your organization will be the presence of:

- local act regulating the verification of counterparties,

- approved form of documenting the results of the inspection.

For example, this could be a counterparty audit report. The results of the audit can be reflected in a legal opinion with a conclusion about the feasibility and safety of further cooperation with a certain organization and an assessment of possible risks.

The attachment to the inspection report or legal opinion includes all documents compiled and received during the inspection, screenshots, photographs, business correspondence of the parties, confirmation of personal contacts with employees of the counterparty company.

Answer for the bank about the reasons for choosing a counterparty

The response to a bank requesting information within the framework of the requirements of Law No. 115-FZ will also be similar in content. In addition to justifying the choice of a specific counterparty, it may also be necessary to justify the conditions for concluding a specific transaction.

Since banks face quite serious liability for failure to take measures to combat money laundering, they can rely on any (not just those listed as mandatory) signs that make a transaction suspicious (Methodological recommendations attached to the letter of the Bank of Russia dated July 13, 2005 No. 99-T). For this reason, a request from the bank may be received in relation to any transaction with any of the counterparties and require the most complete documentary justification.

You should not ignore a credit institution’s request for documents. This may become a reason for the bank not to carry out the transaction that has raised doubts (Clause 11, Article 7 of Law No. 115-FZ).

Your own deal

The criteria for exercising diligence, as indicated by the Supreme Court in Ruling No. 307-ES19-27597 dated May 14, 2021, will be different for the purchase of, for example, ordinary inventories and an expensive asset.

In relation to contracts for the provision of services, it is necessary to request data on the average number of employees of the counterparty, staffing, information about the professional experience and education of employees, recommendations from other customers for similar services, and contracts with contractors for similar services.

In relation to contracts for logistics, transportation, storage, customs services, it is necessary to have confirmation that the counterparty has its own or hired transport; it is advisable to request documents on the warehouse (ownership, lease), collect business correspondence on ordering the volume of services, ordering passes, powers of attorney for drivers.

When concluding a supply agreement, logistics (transportation of goods to the buyer) is also important. Even if there is a condition for the delivery of goods by the supplier, it is recommended to save the customs declaration for the import of goods into Russia and invoices (waybills) to prove the reality of the delivery of products (letter of the Federal Tax Service of Russia dated July 2, 2021 No. SD-4-3 / [email protected ] ).

Dubious Argument

The opinions of courts and tax inspectors agree on the subject of proof of due diligence. In particular, arbitrators pay attention to the business reputation, solvency of the counterparty, and the availability of resources and experience. Below are examples of negligence from judicial practice.

Few resources

The counterparty lacks the necessary resources to execute the transaction - these may include production capacity, the availability of technological equipment, and qualified personnel (Resolution of the Moscow District Court of November 20, 2021 in case No. A414123/2019).

Registration period

The counterparty was registered shortly before the transaction or registered at the mass registration address (Resolution of the Arbitration Court of the Northwestern District of January 25, 2021 in case No. A6615990/2017).

Insufficient data

Documents have not been submitted indicating that due diligence was observed when choosing a counterparty by obtaining directly from the business partner information and documents about the activities of the disputed company, information about types of activities, staff, material and technical resources, other concluded and (or) executed contracts (Resolution of the Moscow District Court of February 12, 2021 in case No. A40137957/2017).

"Empty" address

The counterparty is not listed at the address indicated in the Unified State Register of Legal Entities, there are no lease agreements, the manager denies his involvement in the financial and economic activities of the specified organization, the signing of documents (Resolution of the AS of the Far Eastern District of December 5, 2021 No. F035483/2019).

Reputation audit

Evidence of checking the reputation of the partners was not provided: the presence of personal contacts between the management of the supplier company and the management of the buyer’s organization when discussing the terms of delivery, the presence of documentary evidence of the authority of the head of the counterparty company, copies of his identity document (Resolution of the Moscow District Court of December 27, 2021 in case No. A40229622/2018 ).

Questionable reporting

Tax returns were submitted with zero figures; small staff; reporting on insurance premiums with “zero indicators”, the organization does not own movable (immovable) property (Resolution of the AS of the Far Eastern District of August 13, 2021 No. F033194/2019).

Results

Exercising due diligence is becoming increasingly important for the taxpayer when choosing a counterparty.

He will need to explain his actions, supporting them with documentary justification, not only to the Federal Tax Service, which detects the receipt of an unjustified tax benefit, but also to the bank, which controls the process of legalizing illegally obtained income. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Risk assessment

For 2021, first of all, the correct choice of a business partner affects the payer’s right to make a deduction for VAT - value added tax. Therefore, exercising due diligence when choosing a counterparty is an extremely important step to reduce the risks associated with business activities.

It is known that the Federal Tax Service (FTS of Russia) uses an expensive automated VAT control system (ASK, version 3). The general scheme of its operation is as follows: the system compares tax deductions claimed by the taxpayer for their purchases with information from the corresponding invoices from the counterparty-seller. And if the counterparty has not filed a declaration/has not reflected the transactions in the sales book, or there are other significant shortcomings, and the payer has applied for a deduction for relations with this counterparty, the tax authorities will file claims against the final buyer. Because, when choosing a counterparty, he acted at his own risk.

It must be said that when conducting audits, tax authorities immediately take into account the totality of identified factors and circumstances that can serve as evidence that the taxpayer has received an unjustified benefit. At the same time, they understand that firms and merchants conduct their activities independently. That is, all possible threats and risks are taken upon themselves. Including:

- when choosing a business partner;

- for the consequences associated with this, which may turn out unfavorably for the taxpayer.

By the way, the official Internet resource of the tax department - www.nalog.ru - provides information on ways of conducting financial and economic activities with increased tax risk. You can also find on this site:

- mass business registration addresses;

- officials who are prohibited from running a business for a certain period of time, as well as the names of the companies involved.

Also see “Electronic services for accountants on the Federal Tax Service website: use wisely.”