Typically, an invoice and delivery note serve different purposes, but contain almost identical data. To reduce document flow, a document was created that combines a delivery note and an invoice - a universal transfer document (UTD). In what cases can such a document be used? Is there for it ? Let's talk about the features of using a delivery note and an invoice in one document - UPD.

Also see:

- How to fill out the UPD correctly

- What is the difference between an invoice and an UTD?

Functions of the invoice

A consignment note in the TORG-12 form is used when selling inventory items. However, since 2013, the requirement to use only unified forms of documents has been abolished . Organizations are allowed to create their own document forms (with rare exceptions). The main condition is the presence of mandatory details in such a document and its consolidation in the company’s accounting policy.

The consignment note is classified as a primary accounting document, on the basis of which records are made about the facts of economic activity in the accounting accounts.

The list of mandatory details for primary accounting is enshrined in Art. 9 of the Federal Law of December 6, 2011 No. 402-FZ.

Here is a list of attributes that a document must contain in order to be considered a full-fledged primary document (in our case, an invoice):

As a rule, when implementing inventory materials in practice, they still use TORG-12, since this form is familiar and understandable.

The form of the unified form TORG-12 can be downloaded for free from our website using the link:

FORM TORG-12

How does a deed differ from an invoice?

Very often, entrepreneurs and novice economists do not understand how the act differs from the invoice. It displays all types of completed work, start and end dates. It is necessary if it is necessary to confirm the fact of performing certain functions. In this case, it acts as a report from the contractor to customers.

Such a document regarding acceptance and transfer without a previously drawn up contract or agreement may be considered void by the tax authorities. Because of this, it will be impossible to take into account expenses in order to reduce the tax base.

When answering how the act differs from the invoice, it is necessary to note cases when it is impossible to do without it:

- transfer of the building to the buyer;

- transfer of the enterprise to a second party;

- acceptance of work under the contract;

- transfer of real estate for rent.

On the one hand, the form is not mandatory, but is often requested from the accounting department. According to the Federal Tax Service, only such a form can reliably confirm the fact that certain expenses have been incurred.

Many people are interested in what is the difference between a deed and a delivery note. The latter is needed when transferring certain goods, for example, those that were purchased for resale. It is also relevant in relation to products of the buyer’s own production. It indicates the type of product, its price, quantity, cost and VAT amount. Must contain details of the sending and receiving parties.

Analyzing what is the difference between an act and a delivery note, it can be noted that the first, if the second is available, may not be required to be filled out. If you need to confirm compliance with the rules for accepting goods, you cannot do without it.

Invoice Functions

An invoice has a function that is different from the TORG-12 function.

An invoice is issued by each organization that applies a common taxation system for each of its shipments. This shows that VAT is included in the sale price. The buyer who receives the invoice claims a VAT deduction based on it. Without a properly executed invoice, it is impossible . Therefore, keeping track of the presence of all required details in the invoice is vital.

The rules for filling out an invoice govern 2 documents:

From these documents we can conclude what attributes must be present in the invoice so that a deduction can be obtained from it:

As can be seen from the diagrams, many items in the delivery note and in the invoice are the same.

Provision of documents

Can an invoice be issued before an invoice? The buyer must confirm receipt of the goods with the signature of an authorized person, which means that the invoice is presented together with the goods, in contrast to the invoice, which may not be accompanied by the invoice. In practice, for a more simplified operation, the invoice is issued on the same day as the invoice, thereby forming one package of documents.

For the seller, this allows you to avoid violating the established deadlines of 5 calendar days. When approving the UPD, today there is no need to issue two different documents (invoice and invoice).

UPD functions

Obviously, in the delivery note and invoice, many items are the same. But it is impossible to draw up just one transaction document, since they perform completely different functions.

In order to reduce document flow, a universal transfer document – UPD – was introduced. He combined the invoice and delivery note into one document. That is, one document can be used to ship/receive goods and other materials. values, and also deduct VAT.

Similar rules apply for UPD: the recommended form can be modified in accordance with the needs of the enterprise, but it is necessary to ensure the presence of mandatory details .

Mandatory attributes of the UPD are a set of mandatory details of the invoice and invoice. But there are also unique details that are unique to UPD.

The UPD form is developed on the basis of the invoice form. In fact, the invoice form is part of the UTD form.

UPD and you can get acquainted with samples of filling it out in our article “What correct samples of filling out UPD look like: examples.”

Can they replace each other?

Does a TTN replace an invoice?

If the goods are delivered to the buyer by the supplier or using hired vehicles, then a TTN is issued. If the buyer picks up the goods independently, then the TTN is not issued. Based on this, TTN cannot replace an invoice. Because filling out and registering the TTN is questionable in the case of self-pickup (the peculiarities of registering the TTN when the buyer picks up goods at own expense are discussed in our material).

Tax authorities may request a TTN when checking the validity of VAT deductions. But the tax service takes the invoice as the main document for its work. If the VAT rate differs in the tax form and invoice, the data on the invoice is still taken into account. For the tax service, this accounting document is a priority.

Also, the TTN does not always indicate all the information about the product. If the list is large, then the product part is drawn up in an abbreviated form with a note that the document is not valid without a delivery note (TORG-12). Therefore, TTN cannot be a reliable and complete source of information about cargo.

Is TN necessary if there is a TTN?

A waybill is a shipping document. The functions of TTN are much broader.

But these accounting documents also have something in common:

- information about cargo weight (net, gross);

- data on transportation conditions, time and conditions, properties of the vehicle;

- information about the actual condition of the cargo, containers, packaging, marking and sealing upon acceptance and delivery of the cargo;

- data on changes in transportation conditions during movement and unloading, etc.

The appearance of the consignment note and the consignment note created confusion in accounting circles and raised questions about the need for both accounting forms.

The Ministry of Finance of Russia issued several Letters at once stating that the TTN (form N 1-T), which was approved by Resolution of the State Statistics Committee of Russia dated N 78), has not been canceled and it must be filled out simultaneously with the TN approved by the Government of the Russian Federation (approved by Decree of the Government of the Russian Federation dated N 272 ). That is, they do not replace each other.

So, three types of accounting documentation and the importance of their correct execution for the organization are considered. Each of them accompanies certain processes and has different tasks.

Despite the fact that information is often duplicated, documents cannot replace each other.

- Registration of TTN in EGAIS.

- What is a TTN number and is it a mandatory requirement?

Who can use UPD

The use of UPD is voluntary . To complete transactions, a company can use any acceptable forms: a set of invoice + invoice or only UPD. Moreover, some clients can be issued an invoice and invoice, while others can receive an UTD. It is better to specify what set of documents the transaction will be closed in the agreement with the counterparty.

As already mentioned, the invoice is issued by VAT payer organizations. That is, those who use OSNO.

Can a company issue a UPD in a special regime? Yes maybe . But in this case, the UPD will only play the role of a primary accounting system. To indicate the status of the UTD - only primary or invoice - invoice - there is a special requisite in the UTD form.

Special regime officers should not be afraid to prescribe UPD. If the “status” detail is set correctly, the UTD is not equivalent to an invoice and does not entail consequences in the form of mandatory payment of VAT to the budget.

For a sample of a single document “invoice and delivery note” for simplifiers, as well as filling out specific UPD details, see the article “What does status mean in UPD.”

Instructions for filling

In order to fill out the account correctly you need:

- In the “Recipient” line, indicate the name of the seller or contractor.

- In the line “Recipient's bank” enter the bank details of the organization that sells goods and materials or provides services.

- The empty line indicates the invoice number and the date of its preparation.

- In the line “Goods (works, services)” the name of these types is entered.

- The lines “Quantity”, “Unit of Measurement”, “Price” and “Amount” indicate the quantity of goods or services, their price and total cost.

- Under the total cost, VAT is indicated, if any, as well as the total cost.

- At the end of the document, information about the manager and chief accountant is placed.

- invoices for payment

- invoices with VAT

- invoices from individual entrepreneurs without VAT

To fill out an invoice you need:

- In the first line, indicate the date the document was compiled and its serial number.

- In lines 2,3,4 and 6, indicate the details of the seller, buyer, consignee or consignor.

- Line 5 contains the number of the payment document according to which the advance was received.

- Line 7 indicates the name of the payment currency.

The tabular part of this document is filled out as follows:

- The first column indicates the name of the goods.

- In gr. 2,3,4 indicate the unit of measurement, quantity and price.

- In gr. 6 information about excise duty is entered. 4. In gr. 7 and 8 indicate the tax rate and the tax itself in rubles and kopecks without rounding.

- In gr. 5 and 9 – total cost with and without VAT.

- In gr. 10 and 11 enter information about imported goods.

- The invoice is signed by the director and chief accountant, or other officials authorized to draw up this document. The document is completed either by hand or using a computer. But you can partially fill it out in a computer program, and partially add it by hand.

Important!

In addition, all invoices issued or received are recorded in special accounting journals. If transactions are subject to VAT, the documents are displayed in the sales and purchases books.

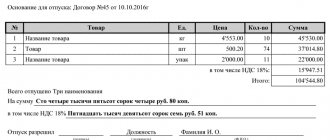

To fill out a delivery note you must:

- In the line “Consignor” you must indicate the name, location, as well as bank details of the organization itself, which is engaged in shipping the goods to the customers themselves.

- In the lines “OKPO” or “Type of activity according to OKDP” information about the seller of goods and materials is recorded.

- In the “Consignee” line, you must indicate all the buyer’s details, including his name, location, and bank information.

- In the lines of the TN form “Supplier” or “Buyer” information similar to that indicated in the lines “Consignor” or “Consignee” is recorded.

- In the “Bases” line, enter the number of the signed agreement and the date of its preparation.

- If the supplier does not deliver his own goods himself, but engages a third-party organization, then the line “Billing note” is filled in.

- The “Product” line provides a detailed description of the product.

- The line “Unit of measurement” must indicate the name of the unit of measurement itself.

- In the “Quantity” line, enter the quantity of the product being sold.

- In the lines “Price”, “Amount without VAT”, “VAT”, “Amount with VAT” the required amounts are indicated accordingly.

- At the end, the data of those officials who issued the goods, as well as those who, according to the power of attorney, accepted the goods and materials, are indicated.

- All entries at the end are sealed with the signatures and seals of the seller and buyer of the goods and materials.

- delivery note

- delivery note