How to take into account rolling holidays and recalculate them?

No less pressing will be the question of how to reflect vacation pay that transfers to another period in form 6-NDFL. The sequence of actions will be as follows:

- The income received in the form of vacation pay, as well as the tax accrued on their amount without taking into account the period to which they relate, are fully included in section 1 of the form in the period of their actual accrual.

- The transfer of vacation pay will be reflected in section 2 depending on its date and the deadline for paying income tax.

In other words, when solving the problem of how to reflect carryover vacation pay in 6-NDFL, you need to focus not on the period for which they are paid, but on the date of actual transfer and payment of personal income tax.

You will have to recalculate vacation pay in 6-NDFL in the following cases:

- The amount of accruals for vacation was determined incorrectly - in this case, it is necessary to recalculate vacation pay and submit an updated report with the correct data.

- If circumstances arise that require an adjustment of the amounts by force of law (for example, illness during the period of annual leave, recall of an employee from vacation), the corresponding correct data must be entered into the reporting during the recalculation period. This position is defended by the Federal Tax Service in its letter dated May 24, 2016 No. BS-4-11/9248.

Extension of vacation will not affect 6-NDFL

In accordance with Art. 124 of the Labor Code of the Russian Federation, annual leave is subject to extension for the period of such circumstances as:

- illness confirmed by sick leave;

- performance of government duties, for the period of which a release from work is provided;

- other cases provided for by industry legislation or internal regulations.

In such cases, there will be no consequences for personal income tax accounting, since payment for all vacation days has already been made, and no recalculation is made. As for disability benefits, the amounts of income and personal income tax on sick pay are reflected in 6-NDFL in the period in which they were paid.

Learn more about how disability benefits are reflected in the calculation of the amount of disability benefits from the material “How to correctly reflect sick leave in 6-NDFL - an example.”

Upon agreement with the employee and in order to ensure the normal operation of the enterprise, vacation days unused due to illness or other reasons can be postponed to another date, and then the recalculation of vacation pay in 6-NDFL will be necessary.

What to write in 6-NDFL if vacation and vacation pay are in different periods

When vacation pay was transferred to an employee in one month, and the vacation began in another, include the entire amount in the calculation in the payment period. Complete sections 1 and 2 in the general order. In the case of rolling vacation, also write down vacation pay in 6-NDFL in the payment periods. There is no need to distribute the amount of payment and tax in proportion to the days of rest.

Example. How to fill out 6-NDFL with carryover vacation pay

The employee took leave from September 24 to October 2. Vacation pay was paid on September 19. The amount of vacation pay is 25,000 rubles, personal income tax is 3,250 rubles. (RUB 25,000 x 13%). The employee is not entitled to deductions. The accountant will show vacation pay in form 6-NDFL for 9 months like this.

In section 1 on line 020 he will write down 25,000 rubles, on lines 040 and 070 he will put 3,250 rubles. In line 060 he will enter 1, since the calculation is filled out one employee at a time. The accountant will enter 0 in the remaining lines.

In section 2 on lines 100 and 110 he will write 09.19.2019, , in line 120 - 09.30.2019, in line 130 - 25,000 rubles, in line 140 - 3250 rubles.

Filling out 6-NDFL regarding adjustment of overpayment

Taking into account the explanations of the financial department, set out in our letter from the Ministry of Finance of Russia dated October 30, 2015 No. 03-04-07/62635, the tax amounts withheld and transferred to the budget from erroneously paid vacation pay are overpaid by the tax agent. Accordingly, the amount of the employee’s tax liability for personal income tax for the tax period must be adjusted. At the same time, the tax agent – the employer – will overpay personal income tax. The specified overpayment can be returned to the tax agent under Art. 78 of the Tax Code of the Russian Federation, which determines the procedure for offset or refund of amounts of overpaid tax, on the basis of clause 14 of Art. 78 Tax Code of the Russian Federation.

However, in this letter we were talking about a resigning employee; in this case, the employee will continue to work and the organization expects to recalculate him in subsequent months, when calculating wages after leaving leave. Then, in our opinion, the overpayment of personal income tax to the budget can be settled during the subsequent calculation of wages. That is, personal income tax calculated from subsequent payments will be transferred to the budget in a smaller amount.

Taking into account the above, information related to the overpayment of personal income tax that took place in the first half of the year, in our opinion, can be reflected in the 6-personal income tax indicators as follows:

6-NDFL for half a year

Section 1:

- line 020 – the amount of accrued income in the form of erroneously paid vacation pay is not reflected;

- line 040 – the amount of calculated tax in relation to erroneously paid vacation pay is not reflected;

- line 070 – the amount of tax withheld from the amount of erroneously paid vacation pay is not reflected.

Section 2:

- line 100 – date of actual receipt of income in the form of vacation pay, for example, the employee was paid the amount of vacation pay 06/24/2016 – 06/24/2016;

- line 110 – date of personal income tax withholding – 06/24/2016;

- line 120 – date of personal income tax transfer – 06/30/2016;

- line 130 – the amount of income actually received in the form of vacation pay, including erroneously paid;

- line 140 – the amount of tax withheld from actually paid vacation pay, including erroneously paid ones.

***

We looked at the issue of filling out 6-NDFL for vacation pay along with salary and gave an example that we hope will help our readers.

Every accountant is interested in how to reflect vacation pay in 6-NDFL. Let's take a closer look at filling out 6-NDFL using the following types of payments as an example:

- vacation pay;

- carryover vacation pay;

- vacation compensation upon dismissal;

- vacation pay for the month of July paid in the month of June.

Vacation pay is cash income that an employee receives from a previously worked period. All employees working under an employment contract receive vacation pay. The employer is required to pay the amount of vacation pay 3 calendar days before the start of the vacation (calendar days are taken into account, not working days).

If an employee resigns of his own free will, the employer, in accordance with Article 127 of the Labor Code of the Russian Federation, is obliged to pay him compensation for unused vacation. According to Article 140 of the Labor Code of the Russian Federation, the employer is obliged to make all payments on the last day of work of the dismissing employee. Accordingly, the employee receives the amount of compensation for unused vacation on the last working day.

Vacation pay can be divided into two situations:

- when vacation pay is paid separately from salary;

- when vacation pay is paid along with salary.

In the first situation, in 6-NDFL, vacation pay is shown as a separate line, since it is accrued individually to the employee and, accordingly, has a separate tax payment deadline.

In the second situation, vacation pay in section 2 is reflected separately, since the deadline for paying tax on vacation pay has a deadline.

Therefore, when filling out 6-NDFL for vacation pay, you can note the following:

- in section 1, the amount of vacation pay is included in income on line 020;

- the calculated amount of personal income tax on vacation pay is included in the calculated amount of tax on line 040;

- The accrued personal income tax is included in the total amount of tax paid in line 070 if it is listed in the current reporting period.

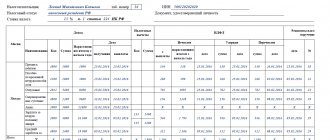

Example 1. Vacation pay accrued and paid in one quarter

- line 020 - 925,000 rub. (900,000 + 25,000);

- line 030 - 63,000 rubles;

- line 040 - 112,060 rub. (108,810 + 3,250);

- line 070 - 103,250 rub. (100,000 + 3,250);

- line 100 - 01/31/2017; line 130 - 300,000 rubles;

- line 110 - 02/06/2017; line 140 - RUB 36,270;

- line 120 - 02/07/2017;

- line 100 - 02/28/2017; line 130 - 300,000 rubles;

- line 110 - 03/06/2017; line 140 - 36,270 rubles;

- line 120 - 03/07/2017;

- line 100 - 03/15/2017; line 130 - 25,000 rubles;

- line 110 - 03/16/2017; line 140 - 3,250 rubles;

- line 120 - 03/17/2017;

- line 100 - 03/31/2017; line 130 - 300,000 rubles;

- line 110 - 04/06/2017; line 140 - RUB 36,270;

- line 120 - 04/07/2017

Accrued vacation pay is not reflected in the 6-NDFL calculation for the six months. The amount of vacation pay will be reflected in the calculation of 6-NDFL for 9 months.

Let's perform the calculation and fill out the form as follows:

- line 020 - 50,000 rub.;

- line 040 - 6,500 rubles;

- line 070 - 6,500 rubles;

- line 100 - 07/05/2017; line 130 - 50,000 rubles;

- line 110 - 07/05/2017; line 140 - 6,500 rubles;

- line 120 - 07/31/2017:

Example 3. Compensation for unused vacation upon dismissal in 6-NDFL

Let's perform the calculation and fill out the form as follows:

- line 020 - 25,000 rubles;

- line 040 - 3,250 rubles;

- line 070 - 3,250 rub.

- line 100 - 06/24/2017; line 130 - 25,000 rubles;

- line 110 - 06/24/2017; line 140 - 3,250 rubles;

- line 120 - 06/30/2017:

General filling procedure

Regardless of the payments, different sections have their own nuances of filling out. The first is recorded as a cumulative total of the total tax deductions during the year. In the second - only the amount transferred for a specific quarter.

Section 1

When recording payments to tax authorities from vacation pay, the accounting employee is interested in only 3 lines in the first section:

- the amount of all vacation pay paid during this reporting period together with personal income tax;

- 040 and 070 - finances to the treasury from these numbers.

Section 2

Here you need to reflect all the data for the last quarter. Only amounts issued on certain lines should be recorded:

- 100 and 110 - the day they were paid;

- 120 - write the last day of the period when funds for the vacation were paid. If it falls on a weekend or holiday - the first working day of another month;

- 130 - payment amount, including personal income tax;

- 140 - numbers of tax that is withheld.

This is an example of filling in the general rules. There are nuances that should be taken into account when maintaining the record in question.

Main options

The employer can pay money for vacation and reflect vacation pay in 6 personal income tax, both together with the salary and separately from it. The following legal details need to be remembered:

- The date of specific receipt of finance for labor is considered to be the last day of the month. This means that for April the paperwork is settled with the employee on April 30.

- Personal income tax is withheld on the same day.

- The deadline for tax transfer to the budget is the next day after receipt of income.

The deduction of relevant finances is regulated by other rules:

- the day of actual receipt is the date of payment;

- tax withholding date - when the money is paid;

- transfer - the last day of the month when vacation income was paid.

Attention! It follows from this that the day of payment of taxes for vacation pay and salary will always be different, even if they were issued at the same time.

According to Art. 136 of the Labor Code of the Russian Federation, vacation pay must be paid to the employee 3 days before the start of the corresponding period. If the employer delays these accruals, then nothing changes in the accounting department and in the personal income tax report: the date of receipt of income is the actual day of payment. But on the same day the company is obliged to pay the employee for the delay. This amount is not taxed, and therefore does not need to be documented.

Example of filling out 6-NDFL vacation pay

Before considering an example of reflecting vacation pay in 6-NDFL, it is necessary to dwell on the following important points:

- Vacation pay is also an employee’s income, therefore, they must be reflected in full along with the accrued tax in section 1 of form 6-NDFL.

- For section 2, the date of payment is important, and therefore the inclusion of vacation pay here will depend on it. The day of issuance or transfer of the corresponding amounts to the employee in this case will also be the actual day of receipt of income.

- The last day allowed for personal income tax payment is very important; it must be taken into account when filling out 6-personal income tax for vacation and sick leave with a tax agent. This element determines the specifics of reflecting these payments in the 6-NDFL report.

Example

The figures below are used as initial data. December wages were issued at the end of 2016.

It must be remembered that all transfers made before the end of the month are considered as advance payments, and tax on them is paid only upon completion of the final salary payment. Therefore, an example - how to reflect vacation pay in 6-NDFL - will look like this:

In section 1:

- field 020: RUB 503,700;

- field 030: 18,000 rub.;

- field 040: RUB 63,141;

- field 060: 6;

- field 070: RUB 43,511 – the amount of personal income tax from the salary for March will not be included.

In section 2:

- field 100: 01/31/2017;

- field 110: 02/10/2017;

- field 120: 02/11/2017;

- field 130: RUB 157,000;

- field 140: RUB 19,630;

- field 100: 02/28/2017;

- field 110: 03/10/2017;

- field 120: 03/13/2017;

- field 130: RUB 157,000;

- field 140: RUB 19,630;

- field 100: 03/28/2017;

- field 110: 03/28/2017;

- field 120: 03/31/2017;

- field 130: RUB 32,700;

- field 140: 4251 rub.

In the 2nd section, wages for March will not be reflected, since in fact they will be paid only on April 10.

Dates of receipt of income and withholding of personal income tax

Unlike salary, the day of actual receipt of income for which is considered the last day of the month, the day of receipt of income for vacation pay (including compensation for unused vacation upon dismissal) and sick leave is considered the date on which they were transferred to the employee’s bank account, or paid in cash (clause 1, clause 1, article 223 of the Tax Code of the Russian Federation).

The employer must pay vacation pay to the employee 3 working days before the vacation. As for sick leave benefits, the employer accrues them on the basis of sick leave within a 10-day period, paying them on the next “payday” day.

“Vacation pay” and “sick leave” personal income tax, as well as tax on other income, must be withheld on the day of their payment, and transferred to the budget no later than the last date of the month of payment to the employee, taking into account the transfer to the next working day if it coincides with weekends and holidays (p 6 Article 226 of the Tax Code of the Russian Federation). Let us remind you that for tax withheld from salary and compensation for vacation, the transfer deadline is the next day after payment of income.

These features of reflecting dates, common for sick leave and vacation pay, must be taken into account when filling out section 2 of the 6-NDFL calculation.

Reflection in 6-NDFL of vacation pay that was paid additionally to the employee

Do not submit an update on 6-NDFL if vacation pay was recalculated and paid extra after the report was submitted. The explanation is simple. Income in the form of vacation pay is considered received on the day of payment.

Reflect the additional payment of vacation pay in 6-NDFL for the period in which the money was paid to the employee. Include this amount in both the first and second sections of the report. In section 1, show the total tax amount taking into account the surcharge. In section 2, reflect the initially accrued vacation pay and additional payment as separate payments.

When an employee was initially overpaid for vacation pay, but was withheld after submitting the 6-NDFL, an amendment will need to be submitted. In section 1 of the updated calculation, show the total amount taking into account deductions.

In what cases may it be necessary to recalculate vacation pay?

The calculation of an employee's rest payment is based on the amount of average daily earnings and the number of vacation days. It is logical that their change will inevitably affect not only the amount due to the employee, but also income tax.

Here are the main situations in which recalculation of vacation pay is inevitable:

- Error when calculating vacation pay or average earnings.

- Additional accruals of wages that occurred after the start of the vacation (for example, a bonus was paid for the previous year).

- Making a decision to increase staff salaries after the employee starts resting.

- Employee illness while on vacation.

- Recall from vacation due to production needs