Is it necessary to put the organization's stamp on the expense report?

The employee is obliged, within the deadlines established by the internal documents of the organization, to draw up a brief report on the work performed during the business trip, which is agreed upon by the manager, and submit it to the accounting department along with a travel certificate (Form N T-10) and an advance report (Form AO-1).

Supporting documents, expenses confirming the production nature of the business trip must be attached to the advance report.

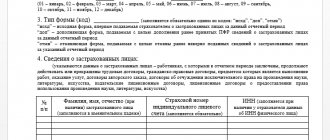

Such documents may be: - travel tickets; — travel bills; — residence certificate in form N T-10, except for long-distance business trips abroad; — a copy of the international passport for a business trip outside the CIS; — report on the completion of the service form (task No. T-10a);

Local act on business trips sample

An employee purchases goods and materials abroad on his own behalf and at his own expense, and subsequently sells such goods and materials by concluding a sales and purchase agreement directly to the enterprise. Формы, образцы, шабРоны RїРѕ РѕСЃРЅРѕРІРЅРѕР№ деятеРьности. Р' настоящее время действует форма бРанка Ристка РЅРµС ‚рудоспособности, установенная РџСЂРёРєР° Р·РѕРј Монздравсоцразвития R Р¤ РѕС‚. Что измениРось РІ РїРѕСЂСЏРґРєРµ оформРRµРЅРЅСЏ сРужебных РєРѕјР°Р ЅРґРёСЂРѕРІРѕРє РІ РіРѕРґСѓ. R SѓРєРѕРІРѕРґСЃС‚РІР°, R˜РЅСЃС‚рукции, R'Р R°РЅРєРё R'Р R°РЅРєРёРћР±СЂР°Р·С†С‹ RѕР±СЂР°Р·Рµ С† сРужебна СЏ записка Рѕ командировании SЃРѕС‚СЂСѓРґРЅРёРєР°. First, let's look at Rostrud's comments and responses to employee complaints regarding the procedure for changing job descriptions. An agreement to change the terms of an employment contract determined by the parties is concluded in writing.

In the event of a period of temporary disability on a business trip, the employee is obliged to immediately notify the official of the company who made the decision on his business trip about such circumstances. Reimbursement for expenses for business telephone conversations is made in the amounts agreed upon with the person who made the decision to send the employee. Now it is necessary to make appropriate changes to this document or approve its new edition. And most often, such a rule is established. The posted worker, within 3 working days after returning, is obliged to provide documents confirming the intended use of the funds issued for the trip. In such cases, the duration of the trip is determined according to the official letter that the traveler must write after his return to the office. The staffing table is a normative act of local significance, revealing information about the staffing structure of the enterprise, the composition and number of employees. If you were looking for “a sample of a local regulatory act on the amount of travel allowances,” there is a pneumatic button for downloading below on the page. But the requirements for state entities and brothers with terrible or harmful labor contracts are somewhat stricter. It covers not only the names of possible positions, but also their code values. The number of real units for each position is indicated in column 4 and is determined based on the financial needs of the organization.

More to read: Refund for kindergarten 2021 for the second child

Do I need to put a stamp on the expense report?

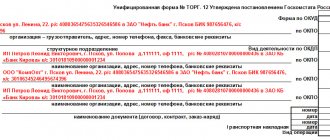

Until January 1, 2021, a unified form was provided for the preparation of an advance report - form No. AO-1, approved by Resolution of the State Statistics Committee dated 01.08.2021 No. 55. In the instructions for the use and completion of the unified form “Advance report” there is no mention of printing, also on the form (AO-1) did not have a specially designated place for the organization’s seal.

From January 1, 2021, unified forms of primary documents are no longer mandatory for use. Organizations (entrepreneurs) can document all their business transactions with independently developed forms of documents, which are approved by an order on accounting policies.

Is it necessary to put a stamp on the expense report? (AND

1. Responses of government bodies to specific questions from citizens and organizations in various sectors of activity. 2. Your practical source for applying the law. 3. The official position of government bodies in specific legal situations requiring decisions.

The database contains cases:

- — civil proceedings

- - administrative proceedings

- — criminal cases of open court proceedings

Simple and convenient search for documents:

- - by territory

- - by court

- - by date

- - type

- - by case number

- - on both sides

- - according to the judge

We have developed a special type of search - SEARCH BY CONTEXT

, which is used to search the text of court documents using specified words. All documents are grouped into

individual cases

, which saves time when studying a specific court case. Each case is attached with

an information card

that contains brief information on the case - number, date, court, judge, type of case, parties, history of the process, indicating the date and action taken.

Systematization of accounting

InfoV assistance to employees when filling out the report, the employer can develop instructions for its preparation. On the front of the form, the accountant indicates the following information:

Travel certificate (form T-10)** Mandatory: a mark is placed at each destination* Sections 1 and 2 of the instructions approved by Decree of the State Statistics Committee of Russia dated January 5, 2021 No. 1, Methodological guidelines approved by order of the Ministry of Finance of Russia dated December 15, 2021 . No. 173n Other documents (orders, instructions, staffing table (form T-3), personal card of the employee (form T-2), official assignment for sending on a business trip and a report on its implementation (form T-10a)*, record sheet working time (in commercial organizations - form T-13, in state (municipal) institutions - either form T-13 or form 0504421), payroll (in commercial organizations - form T-49, in state (municipal) institutions – form 0504401), personal accounts (forms T-54, T-54a), etc.

We recommend reading: Pension benefits for Chernobyl victims in 2021 in the Moscow region

Printing on the expense report

"UNP" No. 3, 2021 I ask for advice. Do I need to keep mobile call logs? The material was prepared by Irina Bushueva, UNP expert. This time Olga Protova, chief accountant from Moscow, asked for advice: “Our company plans to provide employees with mobile communications. We will have supporting documents: an agreement with a telecom operator, monthly bills, a list of positions of employees who use the organization's SIM cards, as well as job descriptions. I read that tax authorities also require keeping a log of all calls indicating the full names and positions of the people our employees call. Or indicate the subscriber on the bill details against each conversation. But this is almost impossible to do! Colleagues, tell us how you are doing.” Opinion 1: set a limit for each employee Natalya Ermolaeva, chief accountant of Partner LLC from Blagoveshchensk, solved this problem as follows: “In the order of the manager, a limit of funds for mobile communications is established for each employee (SIM cards are issued to the company). If an employee goes beyond the established amount, then such excess is not taken into account for income tax. Limits are set within reasonable limits and are reviewed periodically.

The small value of the limit indicates that even with the most thorough inspection, the inspector is unlikely to identify significant distortions. The inspectors themselves understand this, so we have not yet encountered any complaints. We also do not order account details from the operator.” Opinion 2: limit plus account detailing Ilya Antonenko, financial director of a leasing group from St. Petersburg, also uses limits: “If an employee has exceeded the established limit, then a detailed report is requested at this number. Based on it, a decision is made: to take into account the excess as an expense or to withhold this amount from the employee. The Ministry of Finance does not object to such accounting (letter dated October 13, 2006 No. 03-03-04/2/217). Our company does not keep a call log, but the inspectors did not make any claims, despite the significant amounts of expenses under this item.” Opinion 3: sample according to detail Another option is suggested by Igor Bely, chief accountant of Kontur-Flok LLC from Lipetsk: “We do not study each number in detail, but select subscribers according to the following scheme. First, we note negotiations that are clearly production (for example, telephone numbers of counterparties, their employees, negotiations were conducted during working hours, etc.). Taking into account negotiations, the productive nature of which can only be proven indirectly, risks are assessed and a decision is made. And calls that are not included in the sample are automatically considered personal, the cost of which is reimbursed by the employee.” Opinion 4: the log can indicate the general direction of calls “I think the main thing is to have detailed accounts,” notes Maxim Domukhovsky, chief accountant of SmolCarton LLC from Smolensk. — The need to keep a call log follows from the letter of the Federal Tax Service for Moscow dated 02/09/05 No. 20-12/8153. However, this is just a private explanation from local tax authorities, which is not binding. We still keep a similar log, but we do not indicate a complete list of negotiations, but only group calls, for example, “negotiations with suppliers.” During the inspections, no complaints were made against us.” We make a decision Reader's choice. Olga Protova decided to make a selection based on detail until statistics on mobile communications costs were compiled. And then, perhaps, he will switch to using limits. Editor's Choice. We agree with Olga, but it should be noted that it is better for any company to have detailed accounts, regardless of the chosen option.

We recommend reading: Are Amendments to Article 1114 Expected in 2021

Do I need to stamp the expense report?

Is it necessary to put a stamp on an expense report - a set of accounting indicators reflected in the form of certain tables and characterizing the movement of property, liabilities and the financial position of the company for the reporting period. Financial statements are a system of data on the financial position of a company, the financial results of its activities and changes in its financial position and are compiled on the basis of accounting data.

Is it necessary to put a stamp on the expense report - designed to display information from the database. Reports are similar to documents, but these objects perform different functions. Documents enter information into a database, reports output results.

Enter the site

Look, i.e. The accountant must sign: 1. in the box: The report has been verified - signature 2. in the following. square: accountant - signature 3. I approve the report in the amount signature - signature 4. Under the table with DT CT: Accountant - signature

At the beginning of the organization’s activities, the founder (not an employee of the organization) purchased the organization’s seal in cash, there is an invoice for the amount of 96,228 with VAT (VAT is allocated) and a cash receipt for the amount of 96,230. According to the cash receipt, an advance report was made to the founder (entries Dt-60.2.1 Kt-71.1), and the invoice - capitalization of the stamp on 10.6-60.1.1 - cost, 18.3.1.-60.1.1 - VAT. Account 60 freezes, not closed. How to close it. And how to do it right. .

How to do it in 1s 8

Question No. 186. The company operates according to the simplified tax system, income minus expenses. (The data that should be displayed in the book is all entered). It is necessary to display a ledger of income and expenses for the year. The book is not completely formed, the first column: income is all recorded, but the second column of expenses is not recorded. What settings need to be made for this, maybe this is the problem? How to check?

Question No. 111. Configuration “1C: Accounting 8” edition 1.6. We fired an employee at the beginning of the year and when we provide him with a 2-NDFL certificate, we see that in section 4.1, instead of the standard deductions due to him of 800 rubles (400 rubles each for January and February), the program puts 4800 rubles, although the taxes themselves are calculated correctly. How can I correct the report so that the amount is 800 rubles.

22 Jul 2021 stopurist 424

Share this post

- Related Posts

- When Retired Naofier Reserve Officer Changes

- Is it possible to sell the right to lease a land plot?

- Sberbank current account for individual entrepreneurs cost of service

- Encumbrance on a Garden Plot From the Bailiff Service

Advance reports are stamped

There are also cases when sales receipts indicate “medicines” or “services” in the “Name of Goods” column. Attention In such a situation, the accountable person must write down on the back of the check exactly what he purchased and at what cost. However, it should be warned that the presence of such checks for auditors is a reason to fray their nerves and attempts to prove that the institution accepted them for accounting unlawfully. Sometimes the cause of a dispute when checking expense reports are checks punched on weekends, holidays, and outside working hours.

After the expenses have been incurred, the employee who received the money is obliged to return the balance to the enterprise’s cash desk or, if there was an overspending, to receive the excess money spent from the cash register. It is at this stage that a document called “Advance report” .

Form AO-1

You can’t just return the remaining money to the company’s cash desk. It is necessary to submit papers to the accounting department specialists confirming that the accountable funds were spent exactly for the purposes for which they were provided. Such evidence primarily includes cash and sales receipts, receipts, train tickets, strict reporting forms, etc. All of the above documents must have clearly legible details, dates and amounts.

- information about the organization that issued the money,

- the employee who received them,

- exact amount of funds

- the purposes for which they were intended.

- The expenses incurred are also reflected here, along with all supporting documents. In addition, the report contains the signatures of the accounting employees who issued the money and accepted the balance, as well as the employee for whom the accountable funds were registered.

Interesting read: Can an employer calculate alimony arrears?

Types of documents for expense reports

Cash receipts are quite problematic documents. Due to poor print quality, some details may be difficult to read. And during storage, they fade and can become blank sheets of paper. To protect yourself, you need to make a copy of the check immediately after receiving it and have it certified either by the seller or your manager. These copies should be kept next to the receipts.

- Receive a production and economic task from the management of the enterprise (for example, to purchase / pay for goods, work or services);

- Receive a cash advance for expenses related to the task received;

- Go to another enterprise(s) at the place of work or outside it (business trip);

- Have with you properly executed documents for receipt and payment of inventory items (power of attorney, checkbook, corporate card);

- Draw up a report on the use of money and submit it to the accounting department within the prescribed period;

- Transfer valuables for storage and documents to the accounting department;

- Settle monetary relations (return the balance of unused money or receive additional funds to compensate for overspending).

We recommend reading: Description 228 Articles

How to properly prepare an advance report? Sample and rules

The Central Bank of Russia shared the same opinion in 2021 in its letter No. 36-3/2408. At the same time, his letter, but dated December 24, 2021 No. 14-27/513, contains information about whether the question: whether it is possible to use a bank card to calculate the accountable amount is not within the competence of the Central Bank. Then the network enterprise must independently deal with its problems in this case. And so that the regulatory agency does not have unnecessary questions, it is recommended to use the cash register.

To generate information about cash issuance, you need to start by creating a new cash receipt order. After filling out, the document should be printed and given to the accountable person so that the latter fills out the line about receipt of funds and signs. Only after this can you save and post the document.

How have reporting documents changed since July 1, 2021?

From July 1, 2021, the rules for accepting documents from accountable persons have changed significantly. If innovations in work are not taken into account, then the company’s expenses cannot be taken into account for tax purposes. Let's figure out how to work with accountable documents according to the new rules.

Old BSOs are not valid

Not all businessmen are required to switch to online cash register systems from 07/01/2021. Consequently, some have the right to work under the old rules. Remind your colleagues what types of services, goods and works can be purchased without new generation fiscal documentation:

If you have already posted a document and want to draw up a new one, not a corrective one, the document with the error must be cancelled. To do this, cross out the entire text of the incorrect document. Write “Cancelled” in any empty space. Place the date and signature next to it with a transcript.

We recommend reading: Number of Prisoners in 2021

Printing on the expense report

2) the boss pays sums of money for telephone expenses to employees by order, they noted that monthly on the day of salary payment these amounts are also paid, but not everyone provides supporting documents (not all terminals have paper for printing a check) does this threaten me with something and is it necessary pay personal income tax on these amounts?

The procedure for drawing up and submitting an advance report is established by Directive of the Bank of Russia dated March 11, 2021 N 3210-U “On the procedure for conducting cash transactions by legal entities and the simplified procedure for conducting cash transactions by individual entrepreneurs and small businesses” (hereinafter referred to as Directive N 3210-U).

Accounting and - cash expenses

OPTION 3. Do not take into account input VAT when taxing. That is, do not take it as a deduction and do not include it in expenses when calculating income tax. This is the safest and at the same time the most unprofitable option for the organization.

Responsibility for the actual issuance of money to non-workers has not been established. However, a fine for violating the procedure for conducting cash transactions is still possible if an individual on your behalf buys any goods from third-party organizations (entrepreneurs) (pays for work/services) and the payment amount exceeds 100,000 rubles. under one contract. Indeed, in this case, you will exceed the limit of cash payments and Part 1 of Art. 15.1 Code of Administrative Offenses of the Russian Federation; Directive of the Central Bank dated June 20, 2007 No. 1843-U.

22 Jul 2021 stopurist 553

Share this post

- Related Posts

- Is it possible to build a house on a summer cottage?

- Amendments to the Criminal Code of the Russian Federation in 2021 under Article 10

- Which bank can I get a loan from with a bad credit history?

- How to get car insurance online

Under the advance report

For organizations and individual entrepreneurs, the obligation to issue cash register checks to customers when making cash payments is established by Federal Law dated May 22, 2021 N 54-FZ “On the use of cash register equipment when making cash payments and (or) settlements using payment cards” (hereinafter - Law No. 54-FZ). In accordance with this law (clause 1 of article 4 of Law N 54-FZ), the Government of the Russian Federation, by resolution of July 23, 2021 N 470, approved the Regulations on the registration and use of cash register equipment used by organizations and individual entrepreneurs (hereinafter referred to as the Regulations on CCP) .

Some cash receipts indicate the names of purchased goods and their cost. However, even in this case, the check does not yet become the primary document. But some checks have a special field for the signature of the person issuing it.

A sales receipt without a cash receipt is valid in 2021

The sale of goods for cash is usually confirmed by issuing a cash receipt to the buyer. When using online cash registers, the required details of the cash register receipt contain all the necessary information about the seller and the goods sold (name, price, value). Therefore, drawing up a sales receipt at the same time as the cash register receipt is not required. What if the cash receipt is not issued or is lost? Is a sales receipt valid without a cash receipt?

This is interesting: Last Day to Submit Personal Income Tax Reimbursement D 2020

Regardless of whether the cash register receipt was lost or the seller did not issue it because he was exempt from the use of cash registers, a sales receipt can confirm the costs of purchasing goods if such a receipt contains all the required details.