Is there a stamp on the balance sheet in 2019?

The customer does not want to put a stamp on the “Certificate of Acceptance of Completed Work” (Form N KS-2).

What are the consequences of recognizing for profit tax purposes expenses confirmed by an unstamped act?

The absence of a seal imprint in the act of acceptance of work performed cannot be a basis for non-acceptance of this document for tax and accounting purposes. According to paragraph 1 of Art. 252 of the Tax Code of the Russian Federation, for the purpose of taxing the profits of organizations, the taxpayer reduces the income received by the amount of expenses incurred (except for the expenses specified in Art.

270 of the Tax Code of the Russian Federation). In this case, expenses are recognized as justified and documented expenses incurred by the taxpayer.

Inspectors calculate the amount of the fine based on the complete list of documents that a specific organization must submit.

For example, for 2015 you need to submit the following forms: Balance Sheet, Statement of Financial Results, Statement of Changes in Equity, Statement of Cash Flows, explanations in tabular and text form. If you do not submit your reports on time, the fine will be 1000 rubles. (200 × 5).

And the chief accountant faces an administrative fine in the amount of 300 to 500 rubles. What documents need to be submitted as part of the financial statements, read the recommendations.

There is no need to print on financial statements

BB codes On

Smilies On Code On

What documents need to be submitted as part of the financial statements, read the recommendations.

Balance

How to reflect issued interest-free loans on the balance sheet?

Interest-free loans are reflected in the balance sheet on line 1230 “Accounts receivable”. Such loans are not financial investments because they do not generate income for the organization. Also, the information on line 1230 can be detailed, for example, depending on who the debtor is - an organization or a citizen.

See the table for line-by-line filling of the balance.

Do I need to submit an updated balance sheet if accounting errors are found?

If the submitted financial statements have already been approved by the founders, then there is no need to submit updated ones.

Printing on financial statements.

Attention

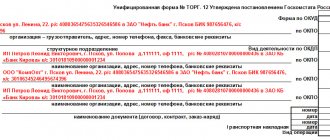

At the same time, it is safer for the seller if the buyer puts his own stamp. This will be an additional argument if the buyer refuses to pay, citing the fact that the document on his part contains the signature of an unauthorized person. Part 2 of Article 9 of the Law of December 6, 2011 No. 402-FZ, paragraph 7 of the Instructions for the Unified Chart of Accounts No. 157n Documents for accounting of trade transactions Mandatory: only in the consignment note (form TORG-12) and the commodity journal of a small retail trade employee (form TORG-23) - space for printing is provided in the document forms. However, the instructions for filling out these documents do not say anything about printing* Instructions approved by the Decree of the State Statistics Committee of Russia dated December 25, 1998.

No. 132 Optional: in all other cases.

Is it necessary to put a stamp on the balance sheet and form 2

Documents for recording the work of construction machines and mechanisms Mandatory: in the report on the work of the tower crane (form ESM-1) and the work order report on the work of the construction machine (mechanism) (form ESM-4), as well as in the certificate for payments for work performed ( services) (form ESM-7) stamp is placed by the customer* Section 1 of the instructions approved by the Decree of the State Statistics Committee of Russia dated November 28, 1997.

Stamping on tax reports: to put it on or not

Legislative framework when compiling reports It is recommended to study the following laws: Legislative act Contents Law No. 82-FZ dated 04/06/2015 “On amendments to certain legislative acts of the Russian Federation regarding the abolition of the mandatory seal of business companies” Letter of the Ministry of Finance No. 03-01-10/45390 dated 08/06/2015 “On affixing a seal when preparing primary accounting documents, as well as on tax returns, if the LLC does not have a seal” Letter of the Ministry of Finance No. BS-4-17/dated 08/05/2015 “On the presence of LLC and JSC seals in documents” Answers to common questions Question No. 1. Do I need a stamp on the power of attorney for the tax office? Firstly, it depends on whether a seal is provided for by the Charter of your organization. Even if available, you don’t have to install it.

News

Unlike tax reporting, accounting reports for 2015 can be submitted both electronically and in paper form.

The form of the primary document “Certificate of Acceptance of Completed Work” (Form N KS-2) is contained in the album of unified forms of primary accounting documentation approved by Resolution of the State Statistics Committee of Russia N 100 and indeed includes the field “Place for printing (MP)”, which, in in principle, implies the presence of such details as a seal. However, it should be noted that among the mandatory details that the form of the primary document used by the organization must contain in accordance with clause 2 of Art. 9 of Law No. 129-FZ, sealing is not indicated.

Legislative framework for reporting

It is recommended to study the following laws:

| Legislative act | Content |

| Law No. 82-FZ of 04/06/2015 | “On amendments to certain legislative acts of the Russian Federation regarding the abolition of the mandatory seal of business companies” |

| Letter of the Ministry of Finance No. 03-01-10/45390 dated 08/06/2015 | “On affixing a seal when preparing primary accounting documents, as well as on tax returns, if the LLC does not have a seal” |

| Letter of the Ministry of Finance No. BS-4-17/ [email protected] dated 08/05/2015 | “On the presence of LLC and JSC seals in documents” |

The balance sheet must be stamped

1 tbsp.

252 of the Tax Code of the Russian Federation, for the purpose of taxing the profits of organizations, the taxpayer reduces the income received by the amount of expenses incurred (except for the expenses specified in Art.

270 of the Tax Code of the Russian Federation). In this case, expenses are recognized as justified and documented expenses incurred by the taxpayer.

Important To be precise, there is no such mandatory requirement for printing on accounting records.

True, there is a GOST recommendation: A seal impression certifies the authenticity of an official’s signature on documents certifying the rights of persons, recording facts related to financial assets, as well as on other documents that provide for the certification of an authentic signature.

Attention: Documents are certified with the seal of the organization.

(State standard of the Russian Federation GOST R 6.30-2003, paragraph 3.25.

The balance sheet must be stamped

5 tbsp. 13 of Federal Law No. 129-FZ). The Balance Sheet and Profit and Loss Statement are part of the financial statements, as well as instructions on the procedure for preparation and presentation were approved by order of the Ministry of Finance of Russia dated July 22, 2003.

Stamping on tax reports: to put it on or not

Legislative framework when compiling reports It is recommended to study the following laws: Legislative act Contents Law No. 82-FZ dated 04/06/2015 “On amendments to certain legislative acts of the Russian Federation regarding the abolition of the mandatory seal of business companies” Letter of the Ministry of Finance No. 03-01-10/45390 dated 08/06/2015 “On affixing a seal when preparing primary accounting documents, as well as on tax returns, if the LLC does not have a seal” Letter of the Ministry of Finance No. BS-4-17/dated 08/05/2015 “On the presence of LLC and JSC seals in documents” Answers to common questions Question No. 1.

Enter the site

RSS Print

Category : Reporting Replies : 12

You can add a topic to your favorites list and subscribe to email notifications.

« First ← Prev.1 Next → Last (2) »

| Julie |

| Is the organization's seal placed on the account? balance sheet, its annexes and explanatory note? I don’t know, because I'm handing over my balance for the first time... |

| I want to draw the moderator's attention to this message because: Notification is being sent... |

| VALYUSHA [email hidden] Belarus Europe, Minsk Wrote 12250 messages Write a private message Reputation: 1344 | #2[106038] March 25, 2010, 1:47 pm |

Notification is being sent...

| Victorovna [email hidden] Belarus, Minsk Wrote 225 messages Write a private message Reputation: | #3[106040] March 25, 2010, 1:47 pm |

Notification is being sent...

| AZA [email hidden] Belarus, Minsk Wrote 17500 messages Write a private message Reputation: 1513 | #4[106043] March 25, 2010, 13:49 |

Notification is being sent...

Life is not a test. If you made a mistake, live with the mistake.| Yermak [email protected] Belarus, Minsk Wrote 2627 messages Write a private message Reputation: 134 Group: Moderators | #5[106046] March 25, 2010, 1:52 pm |

Notification is being sent...

| Julie [email hidden] Belarus Wrote 636 messages Write a private message Reputation: | #6[106047] March 25, 2010, 1:52 pm |

Notification is being sent...

| VikoKoshechka [email protected]ler.ru Belarus, Minsk Wrote 1233 messages Write a private message Reputation: | #7[106048] March 25, 2010, 13:52 |

Notification is being sent...

| D.V. [email hidden] Belarus, Vitebsk Wrote 30471 messages Write a private message Reputation: 2037 Group: Moderators | #8[106053] March 25, 2010, 1:57 pm |

Notification is being sent...

Uninvited <B.K.worse than a Tatar

| VikoKoshechka [email protected] Belarus, Minsk Wrote 1233 messages Write a private message Reputation: | #9[106059] March 25, 2010, 2:04 pm |

Notification is being sent...

| Yan [email protected] Belarus, Grodno Wrote 16 messages Write a private message Reputation: | #10[106062] March 25, 2010, 2:09 pm |

Notification is being sent...

« First ← Prev.1 Next → Last (2) »

In order to reply to this topic, you must log in or register.

Is it necessary to put a stamp on the balance sheet?

Documents for recording the work of construction machines and mechanisms Mandatory: in the report on the work of the tower crane (form ESM-1) and the work order report on the work of the construction machine (mechanism) (form ESM-4), as well as in the certificate for payments for work performed ( services) (form ESM-7) stamp is placed by the customer* Section 1 of the instructions approved by the Decree of the State Statistics Committee of Russia dated November 28, 1997.

- home

- Question answer

- 09/16/2010 Question Do the tax authorities have the right to require stamping on the balance sheet and the Profit and Loss Statement? A. Makeeva, accountant, Kashira Answer Organizations are required to prepare financial statements based on synthetic and analytical accounting data and submit them to the tax authority at their location (subclause 5, clause 1, article 23 of the Tax Code of the Russian Federation).

An exception is organizations that have the right to use simplified forms of accounting and reporting. For example, these are small businesses that are not subject to mandatory audit, as well as most non-profit organizations. But in some situations, even small organizations must draw up Explanations.

How to show advertising expenses in the Financial Results Report?

The answer to this question depends on the order in which you account for business expenses (which includes advertising expenses). If such costs are attributed entirely to the current period, then advertising costs should be reflected in line 2210 “Commercial expenses” of the Report. And if you distribute between the cost of individual types of products, then reflect them on line 2120 “Cost of sales”. The procedure for accounting for business expenses must be specified in the accounting policy.

Law of December 6, 2011 No. 402-FZ). The instructions for submitting reports (both accounting and budget) also do not contain a requirement for a seal on the reporting forms - the signatures of the responsible persons are sufficient (clause 5 of the Instructions, approved by order of the Ministry of Finance of Russia dated March 25, 2011 No. 33n, clause 6 of the Instructions , approved by order of the Ministry of Finance of Russia dated December 28, 2010. Therefore, it is not necessary to put a stamp, in particular, in the list of goods accepted for commission (form KOMIS-1) and a certificate of sale of goods accepted for commission (form KOMIS-4) Documents for accounting of transactions in public catering Optional: space for printing is not provided in these documents.

Will there be a stamp on the balance sheet in 2021?

In addition, the accounting reporting forms do not provide for affixing a stamp on the accounting (financial) reporting Forms of the accounting (budget) reporting of state and municipal institutions Optional: no space is provided for printing on the accounting (budget) reporting forms Accounting (financial) reporting is considered prepared after signing its copy on paper by the head of the economic entity (Part 8 of Article 13 of the Law of December 6, 2011 No. 402-FZ). The instructions for submitting reports (both accounting and budget) also do not contain a requirement for a seal on the reporting forms - the signatures of the responsible persons are sufficient (clause 5 of the Instructions, approved by order of the Ministry of Finance of Russia dated March 25, 2011 No. 33n, clause 6 of the Instructions , approved by order of the Ministry of Finance of Russia dated December 28, 2010. Therefore, it is not necessary to put a stamp, in particular, in the list of goods accepted for commission (form KOMIS-1) and a certificate of sale of goods accepted for commission (form KOMIS-4) Documents for accounting of operations in public catering Optional: there is no space for printing in these documents. Therefore, it is not necessary to put a stamp, in particular, in the menu plan (form OP-2), invoice for goods release (form OP-4), purchasing act (form OP-5), order-invoice (form OP-20) Instructions approved by Decree of the State Statistics Committee of Russia dated December 25, 1998 No. 132 Documents for accounting for work in capital construction and repair and construction work Mandatory: On document forms that provide place for printing. Accounting document Availability of a seal Declarations for tax and accounting reporting Not provided for Other documents submitted to the tax office Not provided for Reports and other documents submitted to the Social Insurance Fund A seal is provided for when used by a company Negative impact on the environment A seal is provided for when used by a company Sales book, book of expenses and income A seal is required when used by the company Documents submitted for verification by non-tax authorities A seal is provided when used by the company Customs documents Almost all of them require a seal Also, a seal can not be placed on employment contracts, orders manager, as well as civil contracts, unless the contract specifies that the contract itself and all amendments to it are signed and sealed. The form of the primary document “Certificate of Acceptance of Completed Work” (Form N KS-2) is contained in the album of unified forms of primary accounting documentation approved by Resolution of the State Statistics Committee of Russia N 100 and indeed includes the field “Place for printing (MP)”, which, in in principle, implies the presence of such details as a seal. However, it should be noted that among the mandatory details that the form of the primary document used by the organization must contain in accordance with clause 2 of Art. 9 of Law No. 129-FZ, sealing is not indicated. From this we can conclude that the seal impression is an optional requisite of the act of acceptance of completed work. Optional: on documents on internal movement and accounting of goods and materials (forms M-8, M-11, M-15, M-17) and the act of acceptance of materials (form M-7), which is drawn up if there is a discrepancy between the actual data and the data specified in the accompanying documents Section 3 of the instructions approved by Resolution of the State Statistics Committee of Russia dated October 30, 1997 No. 71a Documents for accounting of fixed assets and intangible assets Mandatory: on all acceptance certificates (delivery) of fixed assets (forms OS-1, OS-1a, OS-1b, OS-3), act on acceptance and transfer of equipment for installation (form OS-15) and act on identified equipment defects (form OS-16)* Instructions approved by the resolution of the State Statistics Committee of Russia dated January 21, 2003.

Stamping is not required on financial statements

According to paragraph 1 of Art. 252 of the Tax Code of the Russian Federation, for the purpose of taxing the profits of organizations, the taxpayer reduces the income received by the amount of expenses incurred (except for the expenses specified in Article 270 of the Tax Code of the Russian Federation). In this case, expenses are recognized as justified and documented expenses incurred by the taxpayer. However, tax legislation does not establish any requirements for the form of documentary evidence of expenses.

The Civil Code of the Russian Federation, which indicates that a power of attorney on behalf of a legal entity is issued signed by its head or another person authorized to do so by its constituent documents, with the seal of this organization attached.

Topic: Stamp on balance sheet?

Quick link Documentation and reporting Up

- Navigation

- Cabinet

- Private messages

- Subscriptions

- Who's on the site

- Search the forum

- Forum home page

- Forum

- Accounting

- General Accounting Accounting and Taxation

- Payroll and personnel records

- Documentation and reporting

- Accounting for securities and foreign exchange transactions

- Foreign economic activity

- Foreign economic activity. Customs Union

- Alcohol: licensing and declaration

- Online cash register, BSO, acquiring and cash transactions

- Industries and special regimes

- Individual entrepreneurs. Special modes (UTII, simplified tax system, PSN, unified agricultural tax)

- Accounting in non-profit organizations and housing sector

- Accounting in construction

- Accounting in tourism

- Budgetary, autonomous and government institutions

- Budget accounting

- Programs for budget accounting

- Banks

- IFRS, GAAP, management accounting

- Legal department

- Legal assistance

- Registration

- Inspection experience

- Enterprise management

- Administration and management at the enterprise

- Outsourcing

- Enterprise automation

- Programs for accounting and tax accounting Info-Accountant

- Other programs

- 1C

- Electronic document management and electronic reporting

- Other tools for automating the work of accountants

- Clerks Guild

- Relationships at work

- Accounting business

- Education

- Labor exchange Looking for a job

- I offer a job

- Club Clerk.Ru

- Friday

- Private investment

- Policy

- Sport. Tourism

- Meetings and congratulations

- Author forums Interviews

- Simple as a moo

- Author's forum Goblin_Gaga Accountant can...

- Gaga's opusnik

- Internet conferences

- To whom do I owe - goodbye to everyone: all about bankruptcy of individuals

- Archive of Internet conferences Internet conferences Exchange of electronic documents and surprises from the Federal Tax Service

- Violation of citizens' rights during employment and dismissal

- New procedure for submitting VAT reports in electronic format

- Preparation of annual financial/accounting statements for 2014

- Everything you wanted to ask the electronic document exchange operator

- How to turn a financial crisis into a window of opportunity?

- VAT: changes in regulatory regulation and their implementation in the 1C: Accounting 8 program

- Ensuring the reliability of the results of inventory activities

- Protection of personal information. Application of ZPK "1C:Enterprise 8.2z"

- Formation of a company's accounting policy: opportunities for convergence with IFRS

- Electronic document management in the service of an accountant

- Time tracking for various remuneration systems in the program “1C: Salary and Personnel Management 8”

- Semi-annual income tax report: we will reveal all the secrets

- Interpersonal relationships in the workplace

- Cloud accounting 1C. Is it worth going to the cloud?

- Bank deposits: how not to lose and win

- Sick leave and other benefits at the expense of the Social Insurance Fund. Procedure for calculation and accrual

- Clerk.Ru: ask any question to the site management

- Rules for calculating VAT when carrying out export-import transactions

- How to submit reports to the Pension Fund for the 3rd quarter of 2012

- Reporting to the Social Insurance Fund for 9 months of 2012

- Preparation of reports to the Pension Fund for the 2nd quarter. Difficult questions

- Launch of electronic invoices in Russia

- How to reduce costs for IT equipment, software and IT personnel using cloud power

- Reporting to the Pension Fund for the 1st quarter of 2012. Main changes

- Income tax: nuances of filling out the declaration for 2011

- Annual reporting to the Pension Fund. Current issues

- New in financial statements for 2011

- Reporting to the Social Insurance Fund in questions and answers

- Semi-annual reporting to the Pension Fund in questions and answers

- Calculation of temporary disability benefits in 2011

- Electronic invoices and electronic primary documents

- Preparation of financial statements for 2010

- Calculation of sick leave in 2011. Maternity and transition benefits

- New in the legislation on taxes and insurance premiums in 2011

- Changes in financial statements in 2011

- DDoS attacks in Russia as a method of unfair competition.

- Banking products for individuals: lending, deposits, special offers

- A document in electronic form is an effective solution to current problems

- How to find a job using Clerk.Ru

- Providing information per person. accounting for the first half of 2010

- Tax liability: who is responsible for what?

- Inspections, collection, refund/offset of taxes and other issues of Part 1 of the Tax Code of the Russian Federation

- Calculation of sick sheets and insurance premiums in the light of quarterly reporting

- Replacement of unified social tax with insurance premiums and other innovations of 2010

- Liquidation of commercial and non-profit organizations

- Accounting and tax accounting of inventory items

- Mandatory re-registration of companies in accordance with Law No. 312-FZ

- PR and marketing in the field of professional services in-house

- Clerk.Ru: design change

- Building a personal financial plan: dreams and reality

- Preparation of accounting reporting. Changes in Russia accounting standards in 2009

- Kickbacks in sales: pros and cons

- Losing a job during a crisis. What to do?

- Everything you wanted to know about Clerk.Ru, but were embarrassed to ask

- Credit in a crisis: conditions and opportunities

- Preserving capital during a crisis: strategies for private investors

- VAT: deductions on advances. Questions with and without answers

- Press conference of Santa Claus

- Changes to the Tax Code coming into force in 2009

- Income tax taking into account the latest changes and clarifications from the Ministry of Finance

- Russian crisis: threats and opportunities

- Network business: quality goods or a scam?

- CASCO: insurance without secrets

- Payments to individuals

- Raiding. How to protect your own business?

- Current issues of VAT calculation and reimbursement

- Special modes: UTII and simplified tax system. Features and difficult questions

- Income tax. Calculation, features of calculus, controversial issues

- Accounting policies for accounting purposes

- Tax audits. Practice of application of new rules

- VAT: calculation procedure

- Outsourcing Q&A

- How can an accountant comply with the requirements of the Law “On Personal Data”

- The ideal archive of accounting documents

- Service forums

- Archive FAQ (Frequently Asked Questions) FAQ: Frequently Asked Questions on Accounting and Taxes

- Games and trainings

- Self-confidence training

- Foreign trade activities in harsh reality

- Book of complaints and suggestions

- Diaries