The concept of an authorized representative of a taxpayer

The tax payment procedure is quite lengthy and consists of several stages. First of all, you need to collect reports, fill out a declaration and visit the tax office.

Managers of large companies cannot always afford to spend time visiting tax authorities. Today, an authorized representative of the taxpayer can pay fees for any legal entity.

An authorized representative of a taxpayer is a person (individual or legal entity) who can represent the interests of the taxpayer in transactions with tax authorities, as well as with other participants in relations regarding taxes and fees.

The authorized person carries out his actions on the basis of a power of attorney, which is issued in accordance with the procedure established by the Civil Code of the Russian Federation.

Application of the term “legal representative of a legal entity”

Legal provisions that contain the term “legal representative” are reflected in the table.

| Art. 25.4 Code of Administrative Offenses of the Russian Federation | Art. 27 Tax Code of the Russian Federation |

| The protection of the interests of a legal entity can be carried out by legal representatives - the head, other persons recognized by the law and constituent documents of the legal entity. The legal representative confirms his authority with documents certifying his official position | Legal representatives - persons authorized to represent the specified organization on the basis of the law or its constituent documents |

As we can see, the legislator uses a variety of formulations and concepts (for example, the Tax Code of the Russian Federation does not require that the legal representative be a body of a legal entity). In the scientific literature there are the following objections to the use of the expression “legal representative”:

- The exercise of powers by a manager or other person acting without a power of attorney is not representation, but the direct exercise of the legal capacity of a legal entity, and therefore the use of the term “legal representative” is legally incorrect.

- There is a generally accepted terminology for designating the bodies of a legal entity, which is enshrined in industry (civil and labor) legislation: sole executive body, director (Article 273 of the Labor Code). And there is no need to duplicate it. In Art. 53 of the Civil Code of the Russian Federation provides the designation “a person acting without a power of attorney on behalf of a legal entity”, the list of such persons is fixed in the Unified State Register of Legal Entities, and there is no need to rename them as legal representatives.

Who cannot be an authorized representative of a taxpayer

The legislation prohibits the following categories from being authorized representatives:

- employees of tax and customs authorities;

- specialists of internal affairs law enforcement agencies;

- judges, investigators and prosecutors;

- specialists of state extra-budgetary funds.

This rule is enshrined in Article 29 of the Tax Code of the Russian Federation. This legislative norm was established for the reason that these persons represent the interests of the state and cannot simultaneously be representatives of the taxpayer and the party exercising control over the payment of taxes and fees.

The concept of a tax commissioner

The legal and authorized person from the organization does not have to be the same person; they can be completely different citizens who are vested with different powers. Moreover, the procedure for legitimizing the powers of these representatives is different.

Thus, within the framework of Article 29 of the Tax Code, an authorized representative is appointed by the head of the organization by drawing up an appropriate power of attorney in accordance with civil law. That is, through a notary.

An authorized representative has the right to act on behalf of the organization in matters of tax legal relations and interactions with tax authorities. There is often a practice when a private person (should be understood as an individual) has an authorized and legal representative - this is the same organization or individual.

In this case, only the representative whose powers are notarized is considered authorized.

Within the framework of civil law, there are powers of attorney that are equivalent to notarial ones. On their basis, a representative of an individual is also considered authorized.

Such powers of attorney include:

- powers of attorney from persons serving sentences in prison;

- powers of attorney from military personnel who are undergoing military or contract service;

- powers of attorney from military personnel who are in hospitals, clinics, and sanatoriums.

All documents are certified by the head of the organization in whose care the citizen is. In places of deprivation of liberty, this is the head of the colony or prison organization; for military personnel, this is the unit commander, who is the immediate superior of the employee.

Responsibility of the taxpayer's authorized representative

Authorized representatives of the taxpayer are responsible to the participants in tax legal relations. They are responsible for representing interests in the following cases:

- related to company registration with tax authorities;

- related to filing a declaration;

- related to the collection of tax arrears from taxpayers;

- related to holding a company accountable for violations in the field of payment of taxes and fees, as well as in other cases if the action or inaction of the tax authorities affects the rights of the organization.

The authorized person is responsible for meeting deadlines, filing tax reports, correctly filling out the tax return, as well as for the correct calculation of the final amounts.

For this reason, the taxpayer's authorized representative must have a very good understanding of modern tax laws.

Legal representative of the taxpayer: who is it?

Taxpayer representatives may be:

- legal (Article of the Tax Code of the Russian Federation);

- authorized (Art. Tax Code of the Russian Federation).

In relation to legal representatives, you need to consider who they represent - a legal entity or an individual:

- The legal representatives of a taxpayer organization can be persons representing its interests on the basis of the law or constituent documents. As a rule, the legal representative of the company is its director. Such a representative does not require a power of attorney. The action (or inaction) of such a legal representative related to the participation of the legal entity he represents in tax legal relations is regarded as an action (inaction) of the organization itself that he represents (Article of the Tax Code of the Russian Federation), therefore it will bear responsibility. For example, if a manager fails to submit a declaration on time, a fine under Art. 119 of the Tax Code of the Russian Federation will be imposed on the organization.

- According to the law, only persons determined by civil law can be representatives of an individual. So, in accordance with Art. , Civil Code of the Russian Federation, they can be parents, adoptive parents or trustees of minor individuals, as well as guardians and trustees of incapacitated and partially capable citizens.

As for the second category of representatives - authorized persons, their role is the same in interaction with both individuals and legal entities: such representatives act on the basis of a power of attorney issued to them.

An authorized representative of a legal entity or individual entrepreneur can be:

- full-time employee;

- freelance entity (lawyer, jurist, legal organization, etc.).

The interests of an individual who is not an individual entrepreneur can be represented by another person (for example, the same lawyer) or organization.

Employees of the Federal Tax Service, Department of Internal Affairs, customs authorities, prosecutors, judges, investigators have no right to be authorized representatives of taxpayers (Clause 2 of Article 29 of the Tax Code of the Russian Federation).

Thus, strictly speaking, only the person who is specified in the provisions of regulations and in the constituent documents is recognized as the legal representative of the taxpayer. At the same time, in everyday life, “legal representative” is often understood as just an authorized representative. In this case, it is considered “legal” not by virtue of the provisions of the Tax Code of the Russian Federation or the Civil Code of the Russian Federation, but by virtue of a “legal” power of attorney.

Let us agree that the legal representatives of the taxpayer are essentially the trustees. Let's get acquainted with the features of drawing up the document on the basis of which they act - a power of attorney.

Power of attorney for an authorized representative of the taxpayer

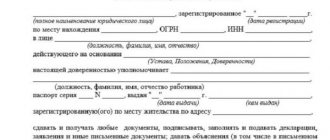

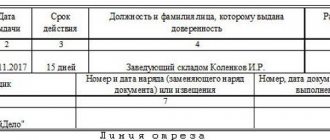

An authorized representative of a taxpayer carries out his activities on the basis of a power of attorney. A power of attorney is a written agreement between a taxpayer and a third party regarding the transfer and division of rights. According to Article 185.1 of the Civil Code of the Russian Federation, the validity period of a power of attorney is no more than 3 years.

If the agreement does not contain information about the terms, then the power of attorney is considered to be valid for exactly one year. Moreover, if the date of opening of the power of attorney is not indicated, then it is considered invalid.

The authorized representative has the right to perform all actions specified in the power of attorney personally.

He can delegate his powers to third parties, but only if this is really necessary.

In this case, the authorized person is obliged to notify his principal and issue a power of attorney to a third party. Such a power of attorney must be notarized.

Page 3 of 3

Legal status of tax representatives

Taxpayers, fee payers and tax agents can participate in tax legal relations personally or through their tax representatives.

Russian tax law provides for two categories of representatives :

- legal - representatives vested with appropriate powers by law or constituent documents of the organization;

- authorized - representatives vested with appropriate powers by powers of attorney, executed in accordance with the rules of Art. 185 of the Civil Code of the Russian Federation.

Representatives in tax relations can be individuals and organizations, regardless of their legal form. There are organizations specializing in representation in tax matters.

The composition of the legal representatives of a taxpayer - an individual is similar to the list of representatives in accordance with the civil legislation of the Russian Federation:

- for minor children - their parents,

- in relation to wards or wards - guardians or trustees.

The legal representatives of an organization are its bodies, since a legal entity acquires rights and assumes responsibilities through its bodies acting on the basis of the law, other regulations or constituent documents. The legal representative of the organization can also be another legal entity, the relationship of which is formalized by a contract or a surety agreement. In this situation, the legal representative who actually participates in tax legal relations for his client will be only the head of the representative organization. Employees of the representative organization can act only on the basis of a power of attorney executed by way of delegation.

The Tax Code of the Russian Federation establishes that actions or inactions of legal representatives of an organization committed in connection with the participation of this organization in tax relations are regarded as actions or inactions of the represented organization itself. Thus, in Russian tax law, the actions of a legal representative are similar to the actions of the represented one, which entails the same legal consequences: whether the act will be recognized as lawful or not, guilty or innocent, whether there are grounds for the use of mitigating or aggravating circumstances, etc.

The participation of a representative in tax relations does not exclude the possibility of the taxpayer (payer of fees) or tax agent independently exercising their powers. In a number of tax relations, representation is inevitable, even if the represented person wishes to exercise fiscal rights and bear responsibilities himself. For example, minors or incompetent persons are required by law to act through a representative. Tax representation is also inevitable when the head of an enterprise or chief accountant signs orders for the transfer of taxes, tax returns, etc.

An authorized representative of a taxpayer may be an individual or legal entity endowed by the taxpayer with the right to represent his interests in relations with tax authorities and other subjects of tax law. Since authorized representation is possible only at the will of the taxpayer, such relations are formalized by a power of attorney. In this case, the authorized representative of the organization exercises his powers on the basis of a power of attorney issued in accordance with the rules of civil law. An authorized representative of an individual exercises his powers on the basis of a notarized power of attorney.

Thus, the relationship between the taxpayer and another entity regarding the authorized tax representation is of a civil law nature. The Tax Code of the Russian Federation “establishes” the institution of an authorized representative office, giving the taxpayer the right to decide for himself whether it is necessary to participate in tax relations through another person. Detailed regulation of the relationship between the principal and the representative is carried out within the framework of civil law. However, further actions of the authorized tax representative, his relationships with tax authorities and other entities regarding tax issues are regulated exclusively by the norms of tax legislation.

The Tax Code of the Russian Federation establishes a rule according to which officials of tax authorities, customs authorities, internal affairs bodies, judges, investigators and prosecutors cannot be authorized representatives of the taxpayer (Article 29 of the Tax Code of the Russian Federation). Unlike the status of a legal representative, actions or inactions of an authorized representative are not recognized without confirmation by the actions (inactions) of the taxpayer himself. There are two conditions, if one of which is present, the actions of the authorized representative will be regarded as actions (inaction) of the taxpayer himself:

- the actions were performed on the basis and within the limits of the power of attorney issued by the taxpayer;

- in the event that an authorized representative commits any acts in favor of the taxpayer without a power of attorney or in excess of the powers specified in the power of attorney, but with subsequent approval of these

- actions (inaction) by the taxpayer himself.

Consequently, the adverse acts of the authorized representative can subsequently be neutralized by the represented entity. At the same time, an instruction to participate in tax relations on one’s own behalf to another person does not relieve the taxpayer of tax obligations, as well as personal liability for illegal acts.

0

- Back

1.5

The procedure for issuing a power of attorney for an authorized representative of a taxpayer

A power of attorney has a certain procedure for issuance, which is established by Article 185.1 of the Civil Code of the Russian Federation. At the same time, on the basis of this document, the authorized person has the right to perform all legal actions to the same extent as the principal.

According to the law, the contract must have a unified form. The powers of the trustee are confirmed by a notary.

The power of attorney must be issued with the signature of the head or the person replacing him. The organization's seal is not required. This rule is enshrined in paragraph 4 of Article 185.1 of the Civil Code of the Russian Federation. Also, if the commissioner files tax returns, he may provide written notarization.

Article 29 of the Tax Code of the Russian Federation. Authorized representative of the taxpayer (current version)

The commented article defines persons who can act as authorized representatives.

An authorized representative of a taxpayer must have a power of attorney.

The procedure for issuing a power of attorney is determined by Article 185 of the Civil Code of the Russian Federation.

The procedure for notarization of powers of attorney is established by Article 59 of the Fundamentals of the Legislation of the Russian Federation on Notaries, approved by the Supreme Council of the Russian Federation on February 11, 1993, N 4462-1.

A power of attorney gives the right to perform legal actions to the person to whom the power of attorney was issued in relation to the person who issued the power of attorney.

The law requires compliance with the form of the power of attorney in the form of its notarization, if such a form is required by law.

The powers of representatives of individuals must be confirmed by a notarized power of attorney or a power of attorney equivalent to a notarized one in accordance with the civil legislation of the Russian Federation.

For example, the performance of actions by a representative (in particular, payment of training expenses) on behalf of the represented person on the basis of a written power of attorney, concluded in a simple, not notarized form, should be understood as the exercise of the civil rights of the represented person.

In this regard, the refusal in such a situation to an individual to provide a social tax deduction in the absence of a notarized power of attorney issued by him to his representative to pay for education is not based on the norms of the current legislation.

In paragraph 4 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 N 57 “On some issues arising when arbitration courts apply part one of the Tax Code of the Russian Federation” it is explained that by virtue of the paragraph of the first paragraph 3 of Article 29 of the Tax Code of the Russian Federation, the authorized representative of the taxpayer-organization exercises his powers on the basis of a power of attorney issued in the manner established by the civil legislation of the Russian Federation, unless otherwise provided by the Tax Code of the Russian Federation.

In particular, an exception to the above general rule is provided for in paragraph 4 of Article 29 of the Tax Code of the Russian Federation, according to which the responsible participant in a consolidated group of taxpayers is an authorized representative of all participants in the consolidated group of taxpayers on the basis of the law.

At the same time, a trust management agreement is not a sufficient legal basis for the trustee to represent the interests of the management founder in the field of taxation. The corresponding powers of the manager must be formalized taking into account the requirements of paragraph 3 of Article 29 of the Tax Code of the Russian Federation.

However, courts must keep in mind that the trustee does not need a power of attorney to perform the duties directly assigned to him by the provisions of part two of the Tax Code of the Russian Federation (for example, Articles 174.1, 214.1, 214.4, 275, etc.).

An authorized representative of a taxpayer - an individual exercises his powers on the basis of a notarized power of attorney or a power of attorney equivalent to a notarized one in accordance with the civil legislation of the Russian Federation (paragraph two of paragraph 3 of Article 29 of the Tax Code of the Russian Federation). These provisions also apply to individuals who are individual entrepreneurs.

Clause 2 of Article 185.1 of the Civil Code of the Russian Federation lists the types of powers of attorney that are equivalent to notarized ones.

Thus, a representative of an individual entrepreneur has the right to act either on the basis of a notarized power of attorney, or on the basis of a power of attorney issued in accordance with Article 185.1 of the Civil Code of the Russian Federation.

Such clarifications are given in the letter of the Federal Tax Service of Russia dated August 22, 2014 N SA-4-7/16692.

The powers of representatives of legal entities must be confirmed by a written power of attorney concluded in a simple form.

A power of attorney on behalf of a legal entity is issued signed by its head or another person authorized to do so by its constituent documents, and it is not necessary to put the organization’s seal on the power of attorney (clause 4 of Article 185.1 of the Civil Code of the Russian Federation).

The legislation of the Russian Federation does not provide for a notarized form of power of attorney when submitting tax reports and other information by legal entities to the tax authorities.

For example, the head of a separate division may be an authorized representative of a taxpayer organization (see letter of the Ministry of Finance of Russia dated 08/05/2011 N 03-02-07/1-278).

According to paragraph 15 of the Review of judicial practice of the FAS East Siberian District related to the application of Chapter 14 of the Tax Code of the Russian Federation (tax control) (recommended by Resolution of the Presidium of the FAS East Siberian District dated 06/09/2011 N 4), a power of attorney issued to an authorized representative of the taxpayer may indicate general authority to represent interests in relations with government agencies. Neither the legislation on taxes and fees, nor civil legislation prescribe the need for a special indication in the power of attorney of the authority to participate in the consideration of tax audit materials.

Comment source:

“ARTICLE-BY-ARTICLE COMMENTARY TO PART ONE OF THE TAX CODE OF THE RUSSIAN FEDERATION” (UPDATE)

Yu.M. Lermontov, 2016

Grounds for termination of the power of attorney

Article 187 of the Civil Code of the Russian Federation contains grounds for termination of a power of attorney:

- if the power of attorney has expired;

- if the power of attorney is canceled by the principal;

- if the trustee himself renounced his authority;

- if the legal entity has ceased its activities as a result of liquidation or reorganization;

- if the principal and the trustee are declared incompetent or missing;

- upon the death of the principal or trustee;

- if a bankruptcy procedure has been introduced in relation to the organization, in which the principal loses the right to issue powers of attorney.

There are no deadlines for revocation of a power of attorney for either the principal or the authorized person. If the principal changes or cancels the power of attorney, he is obliged to notify the authorized person and the tax authorities about this.

The taxpayer's legal successors retain their rights and obligations that arose as a result of their actions after it became known about the termination of the power of attorney. However, the rule is not valid if the tax authorities were aware of the termination of the document.

After the power of attorney has expired, the authorized person or legal successor is obliged to return the document to the taxpayer immediately.

This obligation is two-sided.

If this does not happen, and the organization is unable to return the document form, then it must submit an announcement within the established time frame that the power of attorney is considered invalid. This is necessary to prevent fraudulent activities, namely to ensure that no one else can use the company’s power of attorney.

After publication of the announcement, all actions under the power of attorney carried out within the period following publication are considered invalid.

When can an authorized representative be admitted under the Code of Administrative Offences?

Supreme Arbitration Court of the Russian Federation in paragraphs. 24, 24.1 of Resolution No. 10 gave an interpretation of the rules on proceedings under the Code of Administrative Offenses of the Russian Federation, from which the following conclusions can be drawn:

- in a case of an administrative offense, the determining factor for the observance of the rights of a legal entity is the notification of the initiation of the case, as well as an explanation of rights and obligations; it should be ensured that the legal representative is informed (Article 25.15, paragraph 3 of Article 28.2 of the Code of Administrative Offenses of the Russian Federation);

- further exercise of rights depends on the management of the legal entity, which can send a representative or defender to participate at all stages of the procedure (in accordance with Article 25.5 of the Code of Administrative Offenses of the Russian Federation).

At the same time, the power of attorney issued to the representative must list specific powers in the case of an administrative offense; a general power of attorney in this case may be rejected (see the resolution of the Supreme Court of the Russian Federation dated September 1, 2017 in case No. 18-AD17-22). This also applies to an abstract judicial power of attorney, which is not accepted during judicial appeals of decisions in cases of administrative offenses (see decision of the Supreme Court of the Russian Federation dated 06/07/2018 No. 47-AAD18-9).

In accordance with the conclusions of the Armed Forces of the Russian Federation, set out in the above judicial acts, if the power of attorney indicates the powers of representation in this particular case, such a document confirms that the legal representative has been properly notified and has expressed his will for the representative to participate in this case by power of attorney.

Powers of attorney equivalent to notarized ones

A power of attorney for the authorized person must be notarized, but there are certain circumstances when notarization is not possible. Article 185.1 of the Civil Code of the Russian Federation establishes a list of powers of attorney that are equivalent to notarized ones:

- documents issued to military personnel undergoing treatment in hospitals. Must be certified by the head of the medical institution or senior physician;

- documents issued to military personnel located in places of military headquarters where there are no notary offices;

- powers of attorney of convicts in places of deprivation of liberty, which are certified by the management of the correctional institution;

- powers of attorney of adults located in social protection organizations, certified by the management of such organizations.

How to register a representative of an individual (not an individual entrepreneur)

A typical legal representative of an individual taxpayer is an organization or individual entrepreneur that helps him file an income tax return, draw up and receive a tax deduction, etc. Note that in general, such companies do not require any powers of attorney from the taxpayer, since they use a “cunning” way of interacting with the Federal Tax Service, sending documents there on behalf of the individual customer by regular mail. If necessary, the necessary accompanying documentation is drawn up, or ordinary civil powers of attorney (not dictated by the provisions of the Tax Code of the Russian Federation) are issued to send letters by mail.

But in particularly difficult cases (for example, if it is necessary to coordinate a large volume of documentation with the tax authorities), a power of attorney is drawn up that meets the requirements of the Tax Code of the Russian Federation. Its main feature is that it must be notarized (Clause 3, Article 29 of the Tax Code of the Russian Federation). Looking ahead, let's say that the same requirement is established for powers of attorney on behalf of individual entrepreneurs, since they are considered individuals (clause 4 of the resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 No. 57).

In certain cases, it is possible to use a document equivalent to a notarized power of attorney. The list of such documents is given in paragraph 2 of Art. 185.1 of the Civil Code of the Russian Federation (powers of attorney for military personnel, certified by the commanders of military units, persons in prison, certified by the heads of such places, etc.).

The contents of the power of attorney, especially regarding the powers delegated to the authorized person, are negotiated by the parties individually.