Powers of attorney will become notarized

The government of the Russian Federation came up with such an initiative. Officials are going to amend the Tax Code of the Russian Federation, according to which the authorized representative of the taxpayer will have to certify the power of attorney with a notary. Nowadays, to certify this document, the seal of the organization and the signature of its head are sufficient.

The status of an authorized representative, enshrined in Article 29 of the Tax Code of the Russian Federation, will be clarified. Now they have the right to act as an individual or legal entity that the taxpayer has authorized to represent his interests in relations with tax and customs authorities. The new version of the article will indicate that the representative exercises powers only on the basis of a notarized power of attorney or its electronic version certified by an enhanced qualified electronic signature of the principal. It is noteworthy that organizations do not require a notarized power of attorney for representation in court. After the adoption of the amendments, tax authorities’ requirements for representatives will become much stricter. Officials claim that this will protect organizations and individual entrepreneurs from fraudsters, since it is more difficult to forge a notarized power of attorney.

The Chamber of Commerce and Industry of the Russian Federation (CCI) reacted negatively to the government’s idea. Its head, Sergei Katyrin, sent a letter to the Cabinet of Ministers with a request to preserve ordinary paper powers of attorney with the signature of the head for filing tax reports. As the head of the Chamber of Commerce and Industry clarified, the innovation will worsen the situation of taxpayers:

This may entail additional costs for the business to pay for notary services, as well as time spent visiting notary offices.

In his opinion, the threat of fraudulent actions in relation to reports to the Federal Tax Service is not so great as to complicate the life of business. However, until now, obtaining representative status for these purposes has been as simple as possible.

Rules for drawing up a power of attorney

Such a document is drawn up in accordance with certain requirements for design and content. This is an official document, which, if executed incorrectly, may cause Tax Service employees to refuse to issue or accept the principal’s documents.

If a document requires notarization, this can be easily avoided, since the power of attorney is drawn up on a form provided by a notary. But even if you use a sample from the Internet for a tax power of attorney or even write it by hand, the notary will still check the correctness of the entered data during certification and indicate any mistakes made.

The power of attorney must contain the following points:

- name and date of preparation (mandatory point, without which the document will be considered invalid);

- place of compilation;

- passport details of the principal or details of the legal entity from which the document is being drawn up (including checkpoint and tax identification number, legal address, name, position and full name of the manager);

- Full name and passport details of the authorized representative;

- powers and rights that the person in whose name the power of attorney is drawn up will have;

- validity period of the document (the maximum validity period of the power of attorney is three years from the date of preparation; without specifying the period, the document is valid for one year).

Duty to report

All taxpayers are required to submit reports to the Federal Tax Service. Moreover, officials have provided several forms of provision:

- Upon personal visit to the inspection and provision of a paper report.

- Sending papers by mail.

- Submission of electronic reports via special secure communication channels.

But not every employee has the right to send tax reports to the Federal Tax Service. Such powers are assigned to the manager (director or individual entrepreneur). Nevertheless, the company's management has the right to delegate the authority to submit reports to a third party. For example, a third-party company, a private individual, or your employee. In this case, a power of attorney is issued for the tax authorities to submit reports.

Why do you need a power of attorney for the tax authorities to represent interests in 2021?

Individual entrepreneurs and legal entities have to visit the tax office quite often. As you know, the head of a company can represent its interests in any organization without a power of attorney. But there is no need for the director to personally deal with current affairs by visiting the tax authority. Typically this responsibility is assigned to an employee. It is precisely in such situations that the need to draw up a power of attorney arises. Among the powers that this power of attorney confers on the representative are:

- Receiving any documents;

- Filing declarations and tax reports;

- Take part in supervisory activities;

- Submit applications;

- Challenge decisions of tax inspectors;

- Receive statements;

- Get acquainted with the materials of cases concerning the principal.

In most cases, the power of attorney is taken by tax officials. This is due to the fact that usually such a document is issued to fulfill a specific assignment. Even if you have to visit the tax office several times, the attorney often turns to the same specialist. Although, if a representative needs to visit various tax authority specialists, it is possible that each of them will have to give a power of attorney. The head of the organization must take this feature into account. It is recommended to immediately issue a power of attorney in several copies.

( Video : “How to issue a power of attorney”)

Who can be a confidant

If the principal is an ordinary person, he has the right to appoint anyone as his representative. This can be either an individual or an entire company. Although this happens extremely rarely. In most cases, a power of attorney of this kind is used by various companies. Typically, the director of a company assigns such responsibilities to a company employee, for example, a lawyer or chief accountant. In addition, other employees can act as a representative.

Many people mistakenly believe that a trusted person can only be an employee of an organization. However, it is not. The law does not prohibit a manager from appointing a representative of absolutely any person. It is possible that the director will entrust the tax office visit to a third-party specialist who is ideally versed in a specific issue.

It can be assumed that here the principal has no restrictions at all. However, this opinion is erroneous. The law prohibits the appointment of attorneys for minors, incapacitated citizens, and representatives with disabilities. You can guess that if an attorney appears at the tax office in any way intoxicated, the responsible employees may refuse to serve him. Naturally, the attorney must be adequate and accountable for his actions.

How to compose

Representatives of the Federal Tax Service did not approve a unified form for transferring powers to a third party. Consequently, organizations and individual entrepreneurs have the right to issue a power of attorney in any form. The document must contain the following mandatory details:

- Date and place of creation of the document.

- Information about the business entity that acts as the principal. That is, a company whose interests will be represented by an authorized person. It is enough to indicate the full name, TIN and address, both actual and legal.

- Information about the authorized representative. Indicate the name of the organization (or full name of an individual), its Taxpayer Identification Number (TIN), and location (residence) address. For an individual, you will need to register your passport details.

- A list of operations, interests, responsibilities and powers that are assigned to the authorized representative.

- List of rights vested in the representative.

- Validity. Please note that a document can be of a fixed-term (limited) or unlimited (unlimited) nature.

The finished paper must be certified by the director of the organization or individual entrepreneur or by a person authorized by law and constituent documents.

Power of attorney for the tax authorities from a legal entity - sample

When developing a sample power of attorney for the tax office in 2021, the same rules apply that were relevant in 2021. The following details must be included in the document:

- Name of the form.

- Place, date and number of compilation.

- Details of the legal entity or individual entrepreneur – name, INN, KPP, OGRN/OGRNIP, legal address.

- Information about the manager - position, full name, on the basis of which document he acts.

- Information about the authorized person – full name, passport details.

- List of powers - indicates what actions an authorized person has the right to perform at the tax authority.

- Validity period of the power of attorney – if the period is not specified, the power of attorney will be valid for 1 year from the date of its preparation.

- Personal signatures of the principal and authorized person.

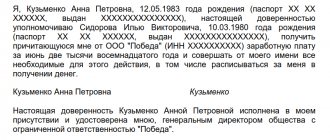

Power of attorney for an accountant at the tax office - sample

Moscow 02/10/2020

— Submit tax and accounting reports and other documentation if necessary;

— Receive and sign acts of joint reconciliation of payments for taxes, fees, penalties, and penalties.

The power of attorney was issued for a period of 5 (five) years without the right of substitution.

General Director of Titul LLC Petrov /M.L.Petrov/

Trusted person accountant Sheveleva /O.I.Sheveleva/

Features of submitting declarations by proxy

If tax reports are submitted to the Federal Tax Service by an authorized representative, then the following nuances must be taken into account. When preparing the declaration, an appropriate mark is made on the title page of the reporting form with the details of the power of attorney. You will also have to attach a copy of the power of attorney form for submitting reports to the tax office to the report. This feature is spelled out in paragraph 5 of Art. 80 Tax Code of the Russian Federation.

Similar rules apply for submitting information via secure communication channels. When sending an electronic form of the report, information about a valid power of attorney is sent along with it. At the same time, in order for such a document to be considered valid, a copy of it must be sent to the Federal Tax Service (clause 1.11 of the Methodological Recommendations, approved by Order of the Federal Tax Service of Russia dated July 31, 2014 No. ММВ-7-6/ [email protected] ).

Power of attorney for the Pension Fund

Like the Federal Tax Service, reporting to the Pension Fund can be submitted by the head of the company or a representative. The authorized representative must have the appropriate power of attorney to represent the interests of the organization.

Expert opinion

Gusev Vladislav Semenovich

Lawyer with 10 years of experience. Specializes in criminal law. Member of the Bar Association.

Special attention should be paid to individual entrepreneurs. They are also required to submit reports to the Pension Fund if they make payments to their employees.

In this case, reporting can also be submitted by a representative of the organization. In this case, a power of attorney must be issued to him.

For individual entrepreneurs, the following requirement applies: the power of attorney must be notarized.

According to the norms of tax legislation, authorized representatives have the right to represent the interests of the taxpayer in the tax authorities. Often such responsibilities are assigned to the chief accountants of companies or their deputies. In this case, the manager issues a power of attorney to represent interests at the tax office - you will find a sample document below.

Duration of the power of attorney

As with any trust document, there must be a period for which it is valid.

Although this cannot be called a mandatory point. If there is no deadline, then by law the validity of such a document will last exactly one year, starting from the date of execution. If the principal does not indicate it, the power of attorney will generally be considered invalid. As for the deadlines themselves, the principal’s hands are completely untied. If previously the law limited the maximum period of validity of a power of attorney, today this rule has been abolished. Moreover, there are no restrictions on either the maximum or minimum period. Typically, this largely depends on the duties that the representative must perform. Perhaps the attorney will only need to appear at the tax office once, or, conversely, carry out a large number of instructions under one power of attorney. Thus, the document can be one-time or special, allowing you to perform various actions. Often, an organization issues a general power of attorney for its employee. This document gives a lot of powers. These also include the right to shift one’s responsibilities to other people, i.e., to write out a delegation of power.

Cancellation of power of attorney

Do not forget that the company, represented by the director, can revoke the trust document at any time. Moreover, it does not matter how much time is left before its expiration date. For example, the services of a representative are no longer necessary, and he has done all the work before. In this case, the director draws up a revocation of the power of attorney, presenting it not only to the authorized person. The tax inspectorate must also be notified of the cancellation of the document. In this case, the representative must return the power of attorney itself to the manager.

In addition, the law provides for situations in which early termination of a document occurs without issuing a corresponding revocation. Thus, a power of attorney becomes invalid in the following cases:

- The company on whose behalf the representative was acting underwent reorganization;

- The company's details have changed;

- The director who signed the power of attorney has resigned or been transferred to another position;

- The attorney, if this is an employee of the company, has changed his position, or has been completely removed from business;

- Death of the principal or representative;

- The employee independently refuses to fulfill the obligations assigned to him.

In all of the above cases, the information specified in the document will not correspond to reality. For example, when receiving other details, the information specified in the power of attorney is considered unreliable. In such situations, the power of attorney is terminated. If this becomes necessary, the principal must draw up a new document.