Good day. If anyone doesn’t know, Stefania Volna advises and advises you. I am telling you about my experience and knowledge in jurisprudence, which in total is more than 15 years, this makes it possible to give the correct answers to what may be necessary in various situations and now we will consider - Dismissal by agreement of the parties: compensation, application. If in your particular case you need an instant answer in your city or online, then, of course, it is better to get help on the website. Or it’s even easier to ask regular readers who have previously encountered the same question in the comments.

Attention please, the data may not be relevant at the time of reading, laws are updated and supplemented very quickly, so we look forward to your subscription to us on social media. networks so that you are aware of all updates.

When thinking about how to calculate the amount that a resigning employee will receive, it is necessary to take into account personal income tax and insurance premiums. According to the Tax Code of the Russian Federation, the employer pays a tax at a rate of 13 percent to the state treasury on wages not previously transferred and compensation payments for unused vacation. They are also subject to insurance premiums. Severance pay is exempt from deduction of income tax if its amount does not exceed the average three salaries, and for the regions of the Far North and equivalent - 6 average salaries. Insurance contributions are not deducted from severance pay if it does not exceed this limit. The amount of compensation above this threshold is subject to taxation, and an insurance fee is also paid from it.

The Labor Code of the Russian Federation does not provide for mandatory payment of severance pay for this type of dismissal. But Article 178 notes that the parties to the main agreement consolidating the employment relationship may provide for the transfer of compensation to the employee in other cases, including upon termination of mutual obligations by agreement. If the local regulations of the enterprise do not contain rules on the calculation of such payments, the parties independently determine the calculation of the amount and the calculation procedure. The following options exist:

Severance pay upon dismissal by agreement

According to the law, settlements with an employee upon dismissal by agreement of the parties must be made immediately on the day of resignation in full. This procedure is formalized by a certificate in form T-61. If on the day of dismissal the employee’s severance payment is made to him no later than the next day after his request for this. Otherwise, the company will be subject to administrative sanctions. The calculation note is filled out by an employee of the HR department and an accountant (you can download the form here). It should indicate:

IMPORTANT. Do not forget to give the employee a pay slip (the employer must develop and approve the form of this document himself). If payments are made in several stages, then in each case a new payslip is issued.

Based on the agreement, a dismissal order is issued (you can use the unified form No. T-8, approved by Resolution of the State Statistics Committee dated 01/05/04 No. 1). In this case, in the line (column) “Grounds for termination (termination) of the employment contract (dismissal)” you must indicate: “Agreement of the parties, paragraph 1 of part one of Article 77 of the Labor Code of the Russian Federation.” And in the line (column) “Base (document, number, date)” you should write: “Agreement dated_ No. on termination of the employment contract dated_ No_”, or “Additional agreement dated_ No_ to the employment contract dated_ No_”, depending on how the agreement was concluded.

We recommend reading: Federal Law 217 Article on Re-election of the Chairman

How to dismiss by agreement of the parties: entry in the work book

The dismissal agreement may stipulate the employer’s obligation to pay the dismissed employee severance pay. For commercial organizations, the amount of such benefits is not limited by law (Article 349.3 of the Labor Code of the Russian Federation). In other words, the employer and employee can agree on absolutely any amount of compensation (severance pay).

If severance pay is established by a local act, an employment contract or a dismissal agreement, then these documents usually stipulate not only the fact of accrual and the amount of compensation, but also the timing of the payment of funds to the employee. For example, a time period after dismissal may be agreed upon during which the amount will be issued.

Compensation under additional agreement upon dismissal

In addition, the employment contract or collective agreement may provide for other cases of payment of severance pay, as well as establish increased amounts of severance pay. According to Art. 57 of the Labor Code of the Russian Federation, if, when concluding an employment contract, no conditions were included in it, these conditions can be determined by a separate annex to the employment contract, or by a separate agreement of the parties, concluded in writing, which are an integral part of the employment contract. Thus, expenses in the form of payment of severance pay provided for in the additional agreement to the employment contract can be taken into account as part of expenses that reduce the tax base for corporate income tax. Labor legislation defines a list of situations in which the employer is obliged to pay severance pay upon termination of an employment contract. For example, severance pay in case of liquidation of a company, reduction in the number or staff of employees, etc. At the same time, the Labor Code allows for other cases of payment of severance pay to be provided for in an employment or collective agreement 1 . Sometimes a company agrees to pay an employee an additional one-time compensation upon dismissal and establishes such payment in the agreement on termination of the employment contract. However, this compensation is not provided for either in the list of mandatory payments under labor legislation, or in the labor or collective agreement. According to the courts, the agreement to terminate the employment contract is not part of it. It does not regulate relations related to the employee’s performance of a labor function. In this case, the income tax base cannot be reduced by the costs of paying compensation (compensation) to an employee upon dismissal 2 . However, the company may enter into an additional agreement with the employee to the employment contract, which will provide for the payment of severance pay upon its termination by agreement of the parties. The Russian Ministry of Finance and tax authorities in their recent letters explained that costs in the form of severance payments can be taken into account as part of expenses that reduce the income tax base. To do this, it is necessary 3 that such payment be provided for in an employment contract, an additional agreement (which is an integral part of it) or a collective agreement. Moreover, the text of the additional agreement must indicate that it is an integral part of the employment contract. Otherwise, the accounting of expenses for payment of compensation may be challenged by tax authorities. Below we provide a sample additional agreement to an employment contract. In earlier letters, the Russian Ministry of Finance opposed reflecting, when calculating the income tax base, the costs of compensation payments under an additional agreement to resigning employees 4 . Officials believed that these compensations are not directly provided for in Russian legislation, they do not meet the criteria of tax legislation and cannot be reflected as part of labor costs 5 .

Payment terms

Whether an employee will receive this type of compensation payment upon dismissal or not depends on many factors. Some organizations have a collective agreement that stipulates additional cases of assigning severance pay.

Useful video

The recorded earnings should include those payments to the employee that are assigned in the billing period and that are related to the employee’s work function. That is, salaries and bonuses should be taken into account; sick leave and maternity benefits, payment for business trips and vacations, and financial assistance should not be taken into account.

A reduction in production volumes, sales of products, goods and services inevitably leads to the need to reduce the number of personnel. Which categories of citizens are preferable and painless to dismiss? When a pensioner is laid off, is a benefit paid, and in what amounts is it tax deductible? – questions that arise for employers.

Severance pay is recognized as compensation in cases documented. Payment cannot be provided for dismissal at the initiative of the employer in accordance with the definition of the Supreme Court of the Russian Federation No. 5-KG 13-125 dated December 6, 2021. On this basis, a veiled severance pay to pensioners in case of staff reduction, formalized on paper as a payment by agreement of the parties, is considered illegal. This applies not only to preferential taxation, but can be interpreted as a violation of constitutional rights, since a pensioner has equal rights along with other categories of citizens.

Procedure for calculation and taxation

Termination of a fixed-term or open-ended contract under this article is mutually beneficial for both participants. Personnel changes include the veiled dismissal of retirees due to staff reductions, and compensation in the amount of several salaries significantly improves the financial situation compared to the payment of 2 salaries due directly upon reduction. Judicial practice in relation to the payment of compensation in the amount of the 3rd salary in the absence of employment is ambiguous, since receiving a pension, according to the courts, is nothing more than a benefit that protects against unemployment.

It is necessary to follow a certain algorithm of actions: first, you must put the agreement reached that the employee is leaving by mutual agreement in writing. When drawing up the document, the participation of the employee himself is allowed; he has the opportunity to offer more favorable conditions, including payment of compensation and its exact amount. It is advisable to indicate the following details in the agreement:

And yet: how to resign by agreement of the parties without problems for all participants in the process, if there are some specifics? The procedure for such termination of labor obligations is reminiscent of the procedure for terminating an employment contract at the citizen’s own request, but there are differences. Specifics of the process of terminating a contract on this basis:

Benefits and risks for the employer

In Russia, legislation provides the parties to an employment contract with the opportunity to separate by mutual consent. This method of terminating the relationship between an employee and an employer differs from dismissal at the employee’s own request. Article 78 of the Labor Code provides for such grounds for termination of a contract as dismissal by agreement of the parties. This option for ending cooperation is optimal if the relationship does not work out and is beneficial for each party.

We recommend reading: Who is entitled to Chernobyl Benefits

The amount of compensation upon dismissal, upon mutual agreement of the parties, must be fixed in the relevant written agreement. The law does not establish a strict amount of severance pay. Based on this, the employer has the right, when establishing it, to be guided by local documents or to specify the amount in the agreement on termination of the employment contract.

Compensation upon dismissal by agreement of the parties

Include the costs of paying employees severance pay, average earnings for the period of employment and compensation upon dismissal as part of labor costs. Moreover, expenses can include both benefits paid in accordance with labor legislation and additional compensation provided for in an employment or collective agreement. This follows from paragraph 1 and paragraph 9 of Article 255 of the Tax Code of the Russian Federation and is confirmed in the letter of the Ministry of Finance of Russia dated January 30, 2015 No. 03-03-06/1/3654. We are a municipal unitary enterprise, a common taxation system. Profit only at the end of the year. During the year, we fired people under the “Agreement of the Parties” (that’s what the order said and there is a signed agreement with each employee). We made the payment from account 91.2 “Other expenses”. The payment was made in a lump sum, in the amount of 2 or 3 times the average salary of the employee. Can we take these expenses into account in tax accounting and attribute them to profit in account 91.2 (NU)?

Please note => Instructions for replacing a driver’s license through government services

simplified tax system

If an organization applies a simplified taxation system with the object of taxation “income minus expenses”, include the amount of compensation upon dismissal and average earnings for the period of employment in expenses that reduce the single tax. Moreover, you can take into account in expenses both benefits paid according to the norms of labor legislation, and additional compensation provided for by an employment or collective agreement (subclause 6, clause 1, clause 2, article 346.16, clause 9, article 255 of the Tax Code of the Russian Federation). These amounts reduce the single tax at the time of payment to the employee (clause 2 of Article 346.17 of the Tax Code of the Russian Federation).

An example of reflection in accounting and taxation of severance pay to an employee dismissed due to staff reduction. The organization operates on a simplified basis, pays a single tax on the difference between income and expenses

Alpha LLC uses a simplified approach to the “income minus expenses” object.

Yu.I. Kolesov works as a driver at Alfa. On May 5, he was fired due to staff reduction, of which he was notified in a timely manner.

Kolesov’s average daily earnings were 500 rubles/day. Upon dismissal, he was paid severance pay in the amount of average monthly earnings for the first month after dismissal (from May 5 to June 4). In this period, according to Kolesov’s work schedule (five-day work week), there are 22 working days. The severance pay was: 500 rubles/day. × 22 days = 11,000 rub.

In accounting, the accountant reflected the transaction with the following entries:

Debit 26 Credit 70 – 11,000 rub. – severance pay accrued;

Debit 70 Credit 50 – 11,000 rub. - severance pay was issued.

The accountant reduced the single tax base by expenses in the amount of 11,000 rubles. Since the severance pay does not exceed three average monthly earnings, this payment is not subject to personal income tax and insurance contributions.

If an organization applies a simplification with the object of taxation being income, then the amount of severance pay (average earnings for the period of employment, compensation upon dismissal) does not affect the calculation of the single tax (clause 1 of Article 346.18 of the Tax Code of the Russian Federation).

Severance pay upon dismissal by agreement of the parties

A frequent condition for dismissal by agreement of the parties is the payment of compensation to the employee, while the amount of such payment is not regulated - neither minimum nor maximum, payment is made in the amount agreed upon by the parties. To formalize the payment, there is no need to indicate the amount in the dismissal order, but the amount of payment must be indicated either in the local act, or in the employment contract, or in the termination agreement. In addition to dismissal at the initiative of the employee or employer, the employment contract may be terminated by agreement of the parties in accordance with Art. 78 of the Labor Code of the Russian Federation at any time and on the terms agreed upon by the parties. Often the parties agree on the payment of severance pay upon dismissal by agreement of the parties.

Amount of severance pay

An accountant usually has a question about how to calculate severance pay upon dismissal. The agreement or labor (collective) agreement may indicate a fixed amount or number of salaries/average earnings. Depending on this, the calculation of severance pay upon dismissal differs .

For example, it is necessary to determine the amount of average earnings taking into account the points and Regulations on the average salary, approved by Decree of the Government of the Russian Federation of December 24, 2007 No. 922 “On the specifics of the procedure for calculating the average salary.”

Do not forget that the regional coefficient is not calculated on severance pay, since it is already taken into account when calculating the employee’s average earnings.

On accounting for expenses of payments made upon dismissal of an employee by agreement of the parties

In connection with the business reorganization, agreements were concluded with employees of the CJSC on the termination of employment contracts (including those that are an integral part of the relevant employment contracts), which stipulated the date of dismissal and the amount of payment associated with dismissal. The workers were dismissed on the basis of paragraph 1 of Article 77 of the Labor Code of the Russian Federation (dismissal by agreement of the parties). This legal position was developed in the Resolutions of the Federal Arbitration Court of the Moscow District dated August 22, 2013 in case No. A40-147336/12-115-1029 and No. F05-14514/2013 dated November 20, 2013, which directly applied it to the payment of compensation upon dismissal of employees due to agreement of the parties.

Reduction

In any case of reduction, the employee is entitled to all payments provided for by law. This includes the usual calculation, as well as compensation for the period of new employment.

Important! All financial accruals in the organization are entered into the 1c program. This should include both taxable payments and amounts without deductions.

A reduction of any type ends with a full settlement with the employee. It is worth considering that in case of early termination of the employment relationship, the employee is entitled to additional compensation, which depends on the number of unworked days before the initial date of departure and on the average daily earnings.

The reduction process itself looks like this:

- employee notification;

- working out the required period (2 or 3 months);

- on the last working day, receipt of a full payment, as well as all documents.

Important! When making payments, the employee is also required to be given a pay slip, which will indicate all accrued amounts. This sheet is printed by the accountant after completely filling out the 1C program and the payroll.

After registering with the employment center, the employee can also receive a third payment, but subject to all conditions that are mandatory. It is important to remember that for some categories of workers the third payment is considered mandatory. This third payment must also be included in the organization's program and financial statements. Upon payment, a payslip is also printed and given to the former employee.

Payment of severance pay upon dismissal by agreement of the parties

The payment of severance pay to an employee upon dismissal by agreement of the parties is not directly mentioned in this article, however, taking into account Part 4 of this article, the employment contract may provide for other cases of payment of severance pay and other compensation payments, as well as establish increased amounts of severance pay. In a similar way, taxation is carried out on severance pay paid upon dismissal to employees of an organization on the basis of an agreement to terminate the employment contract, which is an integral part of the employment contract (letter of the Ministry of Finance of Russia dated June 19, 2014 No. 03-03-06 /2/29308).

How are payments to employees upon dismissal due to redundancy reflected in accounting?

Answer:

The amounts of recognized estimated liabilities for the payment of severance pay to the employee and for the payment of monetary compensation to the employee for all unused vacations form expenses for ordinary activities and are reflected in the reserve account for future expenses.

Upon actual fulfillment of the obligation to accrue severance pay to the employee, compensation for all unused vacations, the incurred costs are included in repayment of previously recognized estimated liabilities.

Salary for the current period of work before dismissal, additional compensation paid to the employee in the event of termination of the employment contract with him before the expiration of the notice period for dismissal, as well as the average earnings retained by the employee for the period of employment (minus severance pay) are taken into account as part of the expenses for ordinary activities on the date of their accrual, regardless of the time of actual payment of funds.

Rationale:

One of the grounds for termination of an employment contract at the initiative of the employer is a reduction in the number or staff of employees (clause 2, part 1, article 81 of the Labor Code of the Russian Federation). All laid-off employees must be notified of the upcoming dismissal at least two months before termination of the contract (Part 2 of Article 180 of the Labor Code of the Russian Federation).

Payments to employees upon dismissal due to reduction

Upon dismissal due to reduction, the employer is obliged to pay the employee the following amounts (part 1 of article 127, part 7 of article 136, part 1 of article 140, part 1, 4 of article 178, part 3 of article 180, part 1 Article 318 of the Labor Code of the Russian Federation):

- salary for the current period of work before dismissal;

— monetary compensation for all unused vacations;

— severance pay in the amount of average monthly earnings (unless the labor or collective agreement provides for an increased amount of benefits);

- additional compensation in the amount of average earnings in proportion to the time before the expiration of the notice period, if the employer dismisses the employee with his consent before the expiration of the two-month notice period;

— average earnings for the period of employment (if there are grounds).

On the day the employee is dismissed, the organization must make a settlement with the employee. If the employee did not work on the day of dismissal, then the corresponding amounts must be paid no later than the next day after the dismissed employee submits a request for payment (part 4 of article 84.1, part 1 of article 140 of the Labor Code of the Russian Federation).

Accounting for redundancy payments

To account for settlements with a dismissed employee for payments due to him, account 70 “Settlements with personnel for wages” is used; settlements with an employee after dismissal can be reflected in account 76 “Settlements with various debtors and creditors” (Instructions for using the Chart of Accounts for Financial Accounting economic activities of organizations, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n).

Sub-accounts can be opened to balance sheet account 96 “Reserves for future expenses”:

— subaccount 96.OO “Estimated obligation to pay for vacations”;

— subaccount 96.ВС “Estimated liability for redundancy payments.”

The accounting entries will be as follows in accordance with the Instructions for the application of the Chart of Accounts for accounting of financial and economic activities of organizations:

1) on the date of notification of the employee about dismissal:

— Debit 20, 23, 26, 29, 44 “Sales expenses” Credit 96, subaccount 96.ВС - reflects the estimated obligation to pay severance pay based on the employee’s notification of the upcoming dismissal and an accounting certificate;

2) on the dates of accrual and dismissal of the employee:

— Debit 96 Credit 70 — severance pay was accrued to the employee at the expense of a previously created estimated liability based on the calculation note;

— Debit 70 Credit 51 “Current accounts” — severance pay was paid based on the bank statement on the current account;

— Debit 20, 23, 26, 29, 44 Credit 70 — the employee’s salary was accrued for the current period of work before dismissal on the basis of a dismissal order and a calculation note;

— Debit 70 Credit 51 “Current accounts” — wages were paid for the current period of work before dismissal based on the bank statement of the current account;

3) on the dates of accrual and payment of additional compensation to the employee upon his early dismissal before the expiration of the notice period for dismissal:

— Debit 20, 23, 26, 29, 44 Credit 70 — additional compensation was accrued to the employee upon early dismissal due to layoffs based on a dismissal order, a written statement from the employee, or a written offer from the employer to resign before the end of the notice period and the settlement note;

— Debit 70 Credit 51 — additional compensation was paid in case of early dismissal based on the bank statement of the current account;

4) on the dates of accrual and payment to the employee of average earnings maintained for the period of employment:

- Debit 20, 23, 26, 29, 44 Credit 76 - accrued average earnings retained by the former employee for the period of employment based on the application of the former employee, a copy of the pages of his work book, where there are no notes on employment after layoffs, and an accounting certificate;

— Debit 76 Credit 51 — the amount of average earnings saved for the period of employment was paid to the former employee based on a bank statement;

5) on the date of accrual and the date of payment of compensation for all unused vacations:

- Debit 96.ОО, 96.ВС Credit 70 - compensation was accrued to the employee for all unused vacations, if the amounts of previously recognized estimated liabilities are sufficient to cover the costs incurred, based on the dismissal order and the calculation note;

— Debit 96.ОО, 96.ВС Credit 69 — insurance premiums have been calculated for the amount of compensation for all unused vacations;

— Debit 70 Credit 51 — monetary compensation was paid to the employee for all unused vacations.

Information provided by the reference and legal system "ConsultantPlus".

Accounting for severance pay upon dismissal of an employee by agreement of the parties

In labor costs, the employer can include any accruals to employees in cash or in kind, incentive accruals and allowances, compensation payments related to work hours or working conditions, bonuses and one-time incentive accruals. A different situation arises with the imposition of insurance contributions on severance pay when an employee is dismissed by agreement of the parties. In accordance with subparagraph “e” of paragraph 2 of part 1 of Article 9 of the Federal Law of July 24, 2009 No. 212-FZ, all types of compensation payments established by law (within the limits of norms) associated with the dismissal of employees are not subject to insurance premiums, with the exception of compensation for unused vacation.

Please note => Allowance for class rank in the state civil service

The procedure for dismissal due to staff reduction for temporary and seasonal workers: step-by-step instructions

This procedure applies:

- to temporary workers;

- seasonal workers.

The characteristics of such labor relations are given in Art. 59 Labor Code of the Russian Federation.

For these employees, the procedure for dismissal on this basis has been shortened and simplified:

- We notify employees:

- temporary - 3 days before the order (Article 292 of the Labor Code of the Russian Federation);

- seasonal - 7 days in advance (Article 296 of the Labor Code of the Russian Federation).

- We fill out the order and fill out the work book. We hand the book to the employee and get his signature on the order.

- We pay wages for time worked.

- We pay compensation for unused vacation. According to the norms of Art. 291, 295 of the Labor Code of the Russian Federation, such employees are entitled to 2 days of vacation for each month of work.

- We determine the severance pay taking into account the fact that:

- it is not paid to a temporary worker (Article 292 of the Labor Code of the Russian Federation);

- a seasonal worker is entitled to a payment in the amount of average earnings for 2 weeks (Article 296 of the Labor Code of the Russian Federation), so we count it and pay it.

Other benefits for temporary and seasonal workers are not regulated by the Labor Code of the Russian Federation.

Severance pay upon dismissal due to staff reduction depends on the payroll calculation procedure established for the employee.

ConsultantPlus experts gave examples of calculating payments when laying off an employee. Get free demo access to K+ and go to the Ready Solution to find out all the details of this procedure.

Dismissal by agreement of the parties to personal income tax

It should be clarified that the severance pay (three salaries) will not be calculated from a specific amount (for example, received last month), but on the basis of average earnings calculated for the year (that is, the average annual salary multiplied by three). In general, upon dismissal, an employee may qualify for the following payments: It is legislated that in the event of dismissal, the employee will be paid 3 months' salary, plus compensation payments. However, this causes a lot of controversy and doubt, therefore, regarding the taxation of severance pay, it is limited to the fact that personal income tax is levied on that part of the funds that exceeds the amount of three times earnings. If a particular payment is higher than your average salary multiplied by three, then paying tax cannot be avoided.

Payment for early dismissal

Next, we will talk about another payment, which is often called a voluntary dismissal benefit. This is additional compensation to the employee for resigning on his own before the company is liquidated or staff is reduced.

The fact is that in the event of liquidation or layoff, the employer is obliged to warn the employee no later than 2 months before the date of dismissal. However, the employee may agree to leave earlier than the appointed date.

Many believe that in this case loses But that's not true. In addition to severance pay and compensation for unused vacation, as well as compensation for the period of employment, the employee has the right to receive additional compensation. Its size is also tied to average earnings and is, in fact, the salary for the time that the employee does not work until the appointed date of dismissal.

is often not profitable to pay this benefit, because the employee will receive it not for work, but for agreeing to leave earlier. But sometimes this is the best option, because the employer during the liquidation process cannot provide all employees with jobs and safe working conditions.

Compensation for dismissal by agreement of the parties

However, in most cases, employers prefer to issue a document signed by the employee. The agreement then carries an additional informational and legal burden, and in addition to the main provisions, it fixes the procedure for transferring cases, determines the amount of compensation, etc. However, in practice there are many lawsuits, as a result of which employees were denied payment of severance pay, even when they were determined employment contract. For example, if a company goes bankrupt, judges recognize such terms of an employment contract as invalid. You should not provide an excessively high amount of compensation upon dismissal. This type of compensation does not create additional motivation for work; therefore, the court may refuse to pay an employee if there are negative financial consequences for the enterprise proven by the employer.

Golden parachutes

The norms of Art. 181, paragraph 2 of Art. 278, art. 279 of the Labor Code of the Russian Federation provides for special payments to top management. They are imposed upon a change of owner or without explanation at all (this, first of all, applies to general directors who are the owners).

Upon dismissal due to the specified circumstances (or other situations provided for in the employment contract with the “top”), the manager or chief accountant must be paid at least 3 months’ salary . In this case, they are no longer entitled to compensation for the period of employment and severance pay .

Dismissal by agreement of the parties: we part amicably

All that is required to carry out dismissal by agreement is the will of the employee and the employer, documented. Moreover, the entire procedure can take only one day - if the day the agreement is drawn up is the day of dismissal. Neither the employer nor the employee is required to notify each other in advance of their intention to terminate the employment contract. In addition, the employer does not need to notify the employment service and the trade union. Thus, it is obvious that it is much easier for an employer to “part” with an employee by agreement than, for example, by reducing numbers or staff. Such an agreement between the employee and the employer is the basis for dismissal, so it must be documented. However, the form of the dismissal agreement is not regulated, that is, the parties have the right to draw it up in any form. The main thing is that this document must contain:

Drawing up a note-calculation in form T-61

A settlement note in the unified form No. T-61 is not a document that must be drawn up and given to an employee upon dismissal by agreement of the parties. However, if a corresponding written statement has been received from the dismissed person, the employer must prepare a note-calculation and give it to the employee. Also, this document will have to be issued to the employee if this is provided for in the dismissal agreement itself.

Let us remind you that form No. T-61 contains information about vacations used and unused during work, as well as the calculation of payments upon dismissal.

Payments and compensation upon dismissal by agreement of the parties

The employer, in accordance with the agreement, regulates the amount of compensation payments when there is mutual agreement to terminate the employment contract. He has the right not to determine any benefits. By law, an employee receives only those payments that are stipulated in labor legislation. Such an agreement cannot be terminated unilaterally. But when a new contract is drawn up, the old one becomes invalid. When a specialist quits in this way, he is not required to work for two weeks in his old place. Termination takes place very quickly, within 24 hours, but only when this is stipulated in the concluded contract. In any case, the final decision on working time is made by the employer.

Employer risks in case of non-payment of compensation and other miscalculations

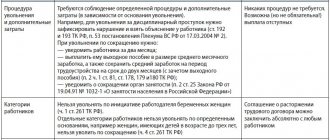

For an employer who intentionally or unintentionally makes mistakes in terms of paying compensation when dismissing an employee, negative consequences may occur:

| What will the employer be punished for? | Type of responsibility | Base |

| For delay in payment of “severance” compensation or evasion of its payment | Administrative or criminal liability | Part 6, 7 Art. 5.27 Code of Administrative Offenses of the Russian Federation Art. 145.1 of the Criminal Code of the Russian Federation |

| For late payment upon dismissal | Financial liability (payment of interest) | Art. 236 Labor Code of the Russian Federation |

| For errors made when preparing dismissal documents (orders, employee’s personal card, work book) | Administrative responsibility | Part 1, Art. 2 5.27 Code of Administrative Offenses of the Russian Federation |

The issue of the legality of punishing an employer for non-payment of compensation in connection with dismissal by agreement of the parties is not always resolved unambiguously. Thus, if the condition for the payment of such compensation is contained only in the employment contract or dismissal agreement, and the remuneration system does not provide for such payment, judges often recognize the employer’s refusal to pay compensation/severance pay as lawful (Appeal ruling of the St. Petersburg City Court dated March 27. 2018 No. 33-6196/2018 in case No. 2-1581/2017). But there are also opposing court decisions (Decision of the Moscow City Court dated November 6, 2019 in case No. 33-49600/2019, Determination of the Supreme Court of the Russian Federation dated May 17, 2013 No. 14-KG13-2).

Dismissal by agreement of the parties: procedure, compensation

- Agreement with the signature of each party;

- Details of an open-ended or fixed-term employment contract that must be terminated;

- The date of the employee’s last working day and, accordingly, the end date of the employment relationship;

- The amount of compensation due to the employee in accordance with labor legislation and the organization’s charter;

- Date and place of signing the agreement. Without these details, the document is not recognized as valid;

- Employee details: full name and position;

- Full name of the employing company;

- Indication of the organizational and legal form of the employing organization;

- Details of the person authorized to sign securities (director, head of the human resources department, authorized representative, etc.): full name and position;

- employer's tax identification number;

- Signatures of the parties to the agreement and their transcripts.

An important feature of this process is voluntariness. That is, neither party has the right to force the other to make an appropriate decision. An attempt at such coercion is criminally punishable if the coerced party applies to the appropriate authorities.

21 Dec 2021 marketur 137

Share this post

- Related Posts

- Employment contract nature of work traveling nature of work

- Can labor safety representatives be elected from among specialists not working at a given enterprise?

- Maximum period of detention on recognizance not to leave the place

- Regional coefficient of the Saratov region

The program and its use

The 1c program is used to reflect all financial transactions. When laying off, the dismissal tab is filled in. All transactions and settlements with the employee are also reflected there. In accordance with the law, all payments must be made in full. This is required for tax transparency during inspections by regulatory authorities. It is also worth considering that any error in the calculations can lead to incomplete payment to the employee who is being laid off. In this case, he will be able to file a claim in court for full compensation.

Important! 1c has many options depending on the update. The most commonly used version is 8.3, which is considered the newest. You need to remember that different versions of the program have their own characteristics. For example, in the first versions, you have to create tabs with various data, including dismissal information, yourself. Newer ones already have such a tab initially.

According to labor law, the employer must pay the funds to the employee after the accountant has calculated all payments. Most errors occur as a result of the employer or accountant not knowing where to enter certain data. For example, severance pay can be paid immediately, or it can be issued in accordance with the expiration of a month after dismissal at the request of a former employee, but the dismissal tab will already be closed, since the main payments have been transferred upon full payment.

Read on the topic: Purpose of payment in a payment order when dismissing an employee

Read on the topic: 6 personal income taxes upon dismissal. How to reflect?