No one is immune from tax debt. Is it possible to write off the resulting debt, if so, how to do it? Let’s look at these and other related issues.

ATTENTION: watch the video about appealing a tax decision and the participation of a lawyer in a tax audit. Subscribe to the YouTube channel to receive free advice on taxes and other issues through comments on videos:

Is it possible to write off tax debt?

On the issue of the possibility of writing off tax debt, Art. 59 of the Tax Code of the Russian Federation speaks about the possibility of recognizing arrears and debts on penalties and fines as hopeless for collection and writing them off in the following cases:

- in case of liquidation of a legal entity, exclusion of a legal entity from the Unified State Register of Legal Entities by decision of the tax authorities

- in the event that an individual entrepreneur is declared bankrupt in terms of arrears, debts on penalties and fines that have not been repaid due to the insufficiency of the debtor’s property

- if a citizen is declared bankrupt

- if a citizen has died or been declared dead, the write-off is carried out in the part that exceeds the amount of the inheritance

- if the court has adopted an act according to which the tax office has missed the statute of limitations for debt collection

- in other cases

Results

The amount of uncollectible receivables with an expired statute of limitations is written off from previously created reserves for doubtful debts. If the amount of the reserve is not enough, then the amount of receivables that exceeds it is shown as part of other expenses. The amount of a bad creditor is taken into account as part of other income. Expired debts are written off separately for each obligation.

Sources:

- Tax Code of the Russian Federation

- Regulations on accounting and financial reporting in the Russian Federation, approved. by order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n

- Civil Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How to write off debts to a pension fund?

The pension fund may recognize financial sanctions as hopeless for collection and write them off.

Resolution of the Board of the Pension Fund of the Russian Federation dated August 28, 2017 No. 600p approved the procedure for writing off financial sanctions, according to which the write-off is carried out on the basis of a decision made to recognize them as hopeless for collection.

According to Art. 11 Federal Law No. 436 dated December 28, 2017, arrears on insurance contributions to extra-budgetary funds of the Russian Federation for periods that expired before January 1, 2017, attributed to individual entrepreneurs and other persons engaged in private practice are recognized as uncollectible and subject to write-off. The decision is made by the tax office.

What is the procedure for writing off bad debts under the Tax Code of the Russian Federation?

According to Art. 59 of the Tax Code of the Russian Federation, debts on taxes and fees (including those paid when moving goods across the border), insurance premiums, interest, penalties and fines are subject to write-off. Tax debts are considered uncollectible in the following situations:

- liquidation of a legal entity when its property is insufficient to repay the debt and the debt for some reason cannot be repaid by the founder (participant);

- bankruptcy of an individual entrepreneur or individual when the debtor’s property is insufficient to pay off debts;

- death of an individual or declaration of his death, and in relation to property taxes - in the amount exceeding the value of his inheritance;

- the court has made a decision on the impossibility of collecting the debt due to the expiration of the period allotted for this procedure, or on the refusal to restore such a period;

- the bailiff issuing a resolution to complete enforcement proceedings after a 5-year period from the date of formation of the debt, if its size is insufficient to initiate bankruptcy proceedings or bankruptcy proceedings are terminated due to the debtor’s insufficient funds to pay legal costs;

- deregistration at the initiative of the tax authority of a foreign legal entity that has provided false information about itself or does not pay taxes or does not submit the necessary documents;

- debiting funds from the payer's account to pay taxes by a bank that did not transfer them to the budget and was subsequently liquidated (clause 4 of article 59 of the Tax Code of the Russian Federation);

- other established by law (including those situations established by the latest legislative act on this issue - the Law “On Amendments...” dated December 28, 2017 No. 436-FZ).

Grounds for recognizing tax debts as bad can also be introduced at the level of constituent entities of the Russian Federation and municipalities in relation to payments to the corresponding budget.

What is the procedure for writing off bad tax debts? It is established by orders of bodies that are granted the right to recognize debt as bad:

- Federal Tax Service of Russia dated August 19, 2010 No. YAK-7-8/ [email protected] ;

- Federal Customs Service of the Russian Federation dated May 27, 2011 No. 1071.

For information about the criteria that legal entities follow when recognizing debts as subject to write-off, read the article “Regulations on the write-off of accounts payable and receivable.”

How to write off taxes under the tax amnesty?

The tax authorities write off taxes under the tax amnesty independently.

In some cases, due to a technical error or other reasons, the tax office may not write off the tax, and therefore the individual or individual entrepreneur will be in debt. In such a situation, the taxpayer should submit an application to the tax office, indicating a request to write off the debt.

At the same time, the procedure does not provide for the initiation of a procedure for recognizing a debt as uncollectible at the request of the taxpayer, since the tax office itself decides to write off taxes or not.

Income tax penalties

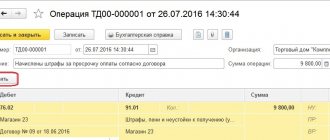

The organization (OSNO) untimely paid income tax to the federal budget for the 1st quarter. Having discovered an error, I independently calculated penalties for the profit tax for the 1st quarter of 2021 and reflected their accrual in accounting. The amount of penalties according to the calculation is 21,000 rubles.

The accrual of penalties is documented in the Transaction in the Transactions – Accounting – Transactions entered manually section.

The tabular part is filled in with the following entries:

- Debit – 99.01.1 “Profits and losses from activities with the main tax system”; Subconto 1 – components of the financial result Tax penalties due .

Analytics Income tax and similar payments are used when calculating (additionally accruing) income tax or other taxes that are accrued in Dt 99. For example, a trade fee or tax under the simplified tax system. In our example, penalties are charged on income tax, and not the tax itself. Therefore, such analytics are not applicable.

- Credit — 68.04.1 “Calculations with the budget”; Subconto 1 – type of payment to the budget Penalties: additionally accrued / paid (independently);

- Subconto 2 – budget levels Federal budget .

Statement of claim for write-off of tax debt

Taxpayers may file an administrative claim in court to declare tax debts uncollectible. The following information must be indicated in the claim:

- name of the court that will hear the claim

- information about the plaintiff (full name, address, telephone number)

- information about the tax defendant (name, address, TIN)

- title of the document – administrative statement of claim

- the text of the claim must set out the circumstances of the case, why the debt should be considered uncollectible with legal justification

- the pleading part sets out specific requirements that the plaintiff asks the court to satisfy

- the list of attachments indicates the documents attached to the claim

- at the end of the claim there must be a signature of the plaintiff

USEFUL : watch a video with tips on filing a claim, and also order a ready-made version from our lawyer

Why is debt written off?

The company's assets and liabilities are reflected in accounting and reporting if they provide useful, timely and truthful information about the financial condition of the business entity. Recognition of debts as impossible to collect obliges the organization to exclude information about them from the accounting data. It is no longer possible to collect debts from debtors, therefore, funds will never reach the company’s account. After the expiration of the statute of limitations for writing off accounts payable, creditors have no right to make claims, and the company is not obliged to satisfy them.

How to calculate the statute of limitations for taxes?

To calculate the limitation period, the amount of debt and the deadline for fulfilling the claim are important.

The tax office issues a demand to an individual to pay a tax, fine, or penalty and sets a deadline for fulfilling such a demand. After the expiration of the deadline for fulfilling the requirement, the tax authority goes to court within 6 months if the debt exceeds 3 thousand rubles. If the amount of the debt is equal to or less than 3 thousand rubles, then the debt is collected after 3 years, when the deadline for fulfilling the requirement expires. The period for filing a claim is 6 months.

The limitation periods for debt collection from legal entities are considered the same as for collection from individuals.

How to write off bad debts to the tax authorities

What is bad debt

A debt is considered bad if it cannot be collected from the debtor. For a debt to be considered bad, it must fall into one of these categories (Letter of the Ministry of Finance of the Russian Federation dated November 16, 2010 No. 03-03-06/1/725):

- the statute of limitations has expired;

- the obligation under it is terminated:

a) due to the impossibility of its execution

b) on the basis of an act of a state body

c) as a result of liquidation of the organization

- the impossibility of collection is confirmed by the decision of the bailiff on the completion of enforcement proceedings;

- The debtor citizen is declared bankrupt and, therefore, his debts are considered repaid (clause 2 of Article 266 of the Tax Code of the Russian Federation, a new basis that is valid from January 1, 2021).

Below we will analyze each category in detail.

Why and how to write off a bad debt to the tax authorities

When taking inventory of receivables, you can identify old debts that can no longer be collected and take into account losses from their write-off, reducing the taxable base for income tax by the amount of receivables (clause 2, clause 2, article 265 of the Tax Code of the Russian Federation).

To write off a bad debt, you need to submit documents that confirm the existence of a debt under a supply agreement, payment for services or work: a delivery note or a delivery and acceptance certificate and an inventory report of receivables, indicating that the counterparty’s debt has not been repaid.

It is best to conduct an inventory of expenses at the end of each reporting or tax period in order to timely attribute overdue debts to expenses. Accounts receivable must be included as expenses during the period when the statute of limitations has passed.

The manager must issue an order to write off bad debts on the basis of an accounting certificate, which indicates that the statute of limitations on the debt has passed, and refer to the primary supporting documents - agreements and payment documents, which must indicate the period of occurrence of the debt, the deadline for payment under the agreement , conditions for deferred payment and the beginning of delay in payment, invoices and work acceptance certificates.

Documents for writing off accounts receivable

To document the procedures and results of the accounts receivable inventory, the following documents are needed:

- order (decree, order) to conduct an inventory (Unified Form No. INV-22);

- act of inventory of settlements with buyers, suppliers and other debtors and creditors (Unified Form No. INV-17);

- certificate to the act of inventory of settlements with buyers, suppliers and other debtors and creditors (appendix to form No. INV-17);

- order from the head of the organization to write off accounts receivable;

- accounting information.

To write off accounts receivable you need:

- documents confirming the occurrence of debt (contracts, invoices, certificates of work performed, services rendered, etc.);

- documents confirming the interruption of the limitation period (debt reconciliation acts, letters, agreements, acceptances, etc.), if the period was interrupted;

- acts of inventory of obligations.

These documents must be stored for at least five years from the date of write-off for accounting purposes, and for at least four years for tax accounting.

During a tax audit, the taxpayer must document the occurrence of receivables, otherwise he will face non-recognition of written off receivables as a loss, additional taxes, penalties and fines.

What debts are considered bad

- time-barred debt

If the debt has not been confirmed for more than three years, it goes into the category of bad debt (Article 196 of the Civil Code of the Russian Federation and paragraph 2 of Article 200 of the Civil Code of the Russian Federation). The limitation period begins after the date of debt formation and is renewed (Article 203 of the Civil Code of the Russian Federation) after each new confirmation of the debt by both parties - when signing a reconciliation report, receiving from the counterparty a letter of guarantee with an expected term or schedule for payment of the debt, or a letter requesting a deferred payment, partial payment of the debt or payment of a penalty for late payment.

If the tax inspectorate has not attempted to collect the debt for three years, after this period it cannot demand payment from the creditor and will receive a denial of the claim if it tries to collect the debt through the court.

If the taxpayer himself overpaid the tax office and forgot about it, and more than three years have passed since the overpayment, it will also be impossible to return or recalculate the payment, since in this case the statute of limitations is also three years.

Comment by Pavel Timokhin, head of UBC

By independently maintaining tax records, the taxpayer often incorrectly reflects his income and expenses in the declaration and incorrectly calculates the amount of tax. If for 2014 he was supposed to charge VAT on 500,000 rubles, but mistakenly charged and declared only 200,000 rubles, and the tax office only checked the documents in 2021, its demand for payment of the balance will not be satisfied, since the taxpayer can easily prove court that the statute of limitations has expired.

Exceptions are cases when the situation is related to a criminal offense and the statute of limitations is 15 years (Clause 1 of Article 78 of the Criminal Code of the Russian Federation).

If an entrepreneur indicated 300,000 rubles in the declaration, but did not pay them, and the tax inspectorate assessed and wrote off a penalty of 30,000 rubles from the current account, later the taxpayer recalculated the amount of tax and reduced it to 100,000 rubles, and the tax will also decrease along with it. penalty amount up to 8,000 rubles. The same 22,000 rubles that have already been withdrawn can be considered an overpayment. Here you need to remember about this amount and not try to collect it after the statute of limitations has expired.

- debt, the obligation for which has been terminated due to the impossibility of its fulfillment (clause 1 of Article 416 of the Civil Code of the Russian Federation)

An obligation cannot be fulfilled if neither party is responsible for it due to objective circumstances, for example, a fire or flood that destroyed all the debtor’s property.

To confirm the impossibility of collecting the debt in this case, you need to submit a certificate from the Ministry of Internal Affairs and the fire inspectorate with a list of lost property and data on the absence of other property from the debtor. Also, the obligation may terminate due to the death of the debtor (Article 418 of the Civil Code of the Russian Federation).

- a debt that cannot be collected on the basis of an act of a state body (clause 1 of Article 417 of the Civil Code of the Russian Federation)

If, as a result of laws, decrees, regulations, orders and regulations, the fulfillment of an obligation becomes impossible. This could be, for example, acts on limited use of airspace, cessation of loading of cargo and luggage, prohibition of entry into the port, import and export of goods when suppliers cannot deliver goods to buyers.

- debt that cannot be collected due to the liquidation of the debtor organization (Article 419 of the Civil Code of the Russian Federation)

a) by decision of its founders (participants), including in connection with the expiration of the period for which the legal entity was created, with the achievement of the purpose for which it was created (clause 2 of Article 61 of the Civil Code of the Russian Federation);

b) by court decision in cases provided for in paragraph 3 of Art. 61 Civil Code of the Russian Federation;

c) as a result of declaring a legal entity bankrupt (clause 6 of Article 61 of the Civil Code of the Russian Federation).

An organization has the right to recognize a debt as bad and include its amount in expenses when calculating the income tax base after making an entry in the Unified State Register of Legal Entities on the exclusion of a legal entity-debtor from the register (Letter of the Ministry of Finance of the Russian Federation dated March 25, 2016 No. 03-03-06/1/16721 ).

An extract from the Unified State Register of Legal Entities can serve as documentary evidence of the liquidation of the debtor organization (Article 6 of Federal Law No. 129-FZ dated 08.08.2001 (Letter of the Ministry of Finance of the Russian Federation dated 03.25.2016 No. 03-03-06/1/16721)).

However, information about the liquidation of a counterparty posted on the official website of the Federal Tax Service cannot be used as the only documentary evidence of expenses in the form of the amount of bad debt written off (Letter of the Ministry of Finance of the Russian Federation dated February 15, 2007 No. 03-03-06/1/98).

Tax authorities have the right to exclude an inactive legal entity from the Unified State Register of Legal Entities in the so-called simplified procedure.

A legal entity that has not submitted reports on taxes and fees for 12 months and has not carried out transactions on at least one bank account is considered to have actually ceased its activities (Article 64.2 of the Civil Code of the Russian Federation).

An organization can write off as tax expenses the debts of a legal entity that has actually ceased its activities, starting from the date of exclusion of this person from the Unified State Register of Legal Entities (Letters of the Ministry of Finance of the Russian Federation dated March 25, 2016 No. 03-03-06/1/16721, dated January 23, 2015 No. 03 01 10 /1982).

However, an extract from the Unified State Register of Individual Entrepreneurs on the termination of the activities of an individual entrepreneur is not a sufficient basis for recognizing the debt as bad (Letter of the Ministry of Finance of the Russian Federation dated September 16, 2015 No. 03-03-06/53157).

After exclusion from the Unified State Register of Individual Entrepreneurs, an individual entrepreneur loses the right to engage in entrepreneurial activities, but continues to bear property liability to creditors as a citizen. Despite the fact that an individual has lost his individual entrepreneur status, the creditor organization will not be able to take his debt into account in expenses when calculating the income tax base.

- if the debtor is declared bankrupt

The insolvency of a company can be recognized as a result of bankruptcy. If at the time of bankruptcy proceedings the company has nothing to collect, its debt is considered uncollectible. This can be confirmed by an act of bailiffs or a bankruptcy commission.

If an organization has a debt to it from an individual, and this person is declared bankrupt and released from obligations, including to it, the organization has the right to take this debt into account when calculating the taxable base.

- the impossibility of debt collection was confirmed by the bailiff’s decision on the completion of enforcement proceedings

If it is impossible to establish the location of the debtor and his property or obtain information about the availability of funds and other valuables belonging to him, located in accounts, deposits or in storage in banks or other credit organizations, or the debtor does not have property that can be recovered, and legal The bailiffs were unable to find him.

What debts are not recognized as bad and cannot be taken into account in reducing the income tax base (clause 2 of Article 266 of the Tax Code of the Russian Federation)

- if the country of the foreign counterparty-debtor has introduced restrictions on the fulfillment of obligations in relation to Russian organizations (Letter of the Ministry of Finance of the Russian Federation dated 06/07/2017 No. 03-03-06/1/35488);

- the court made a decision to refuse to collect the debt (Letters of the Ministry of Finance of the Russian Federation dated July 22, 2016 No. 03-03-06/1/42962, dated September 18, 2009 No. 03-03-06/1/591 and dated February 2, 2006 No. 03-03 -04/1/72);

- the debtor ceased operations due to a merger with another legal entity. In this case, the rights and obligations of the debtor are transferred to a new legal entity (Letter of the Ministry of Finance of the Russian Federation dated September 6, 2016 No. 03-03-06/1/52041 and Article 58 of the Civil Code of the Russian Federation).

Appeal against refusal to write off debt under tax amnesty

If the tax office refuses to write off debt, then there is a possibility that it refuses justifiably. However, the tax office may be wrong and its refusal will be illegal.

The taxpayer may apply to the court to declare the debt uncollectible.

There is judicial practice on claims from taxpayers when they ask to recognize as illegal the inaction of the tax service in not writing off the debt, the obligation of the tax service to write off.

To appeal the write-off refusal, the taxpayer should determine the requirements and file an administrative claim with the district court. Based on the results of the consideration of the claim, the court will make a decision.

ATTENTION : our lawyer on credit matters in Yekaterinburg and issues of writing off debts to microfinance organizations will help you: professionally, on favorable terms and on time. Call today!

Rules for writing off bad debt

After the statute of limitations expires, if the debt is not repaid, it becomes uncollectible. Such debt can be written off as expenses regardless of whether measures were taken to collect it or not. The Ministry of Finance of Russia has repeatedly pointed this out (see letters dated January 13, 2009 No. 03-03-06/1/3, dated February 21, 2008 No. 03-03-06/1/124).

Bad debt can be written off before the statute of limitations expires. For example, if the debtor is excluded from the Unified State Register of Legal Entities due to liquidation.

According to judicial practice, the fact that:

- the taxpayer did not claim the existing debt from the debtor (resolutions of the Federal Antimonopoly Service of the Central District dated October 17, 2013 No. A48-4654/2012, FAS Volga District dated January 20, 2011 No. A72-2931/2010, FAS Moscow District dated April 22, 2010 No. KA-A40/3571 -10);

- the taxpayer did not apply to the arbitration court with a claim for debt collection (resolution of the FAS Moscow District dated December 15, 2010 No. KA-A40/15446-10, FAS North Caucasus District dated May 13, 2008 No. F08-2526/2008, FAS Northwestern District dated February 19, 2007 No. A56-35936/2005).

It should be borne in mind that filing a claim with an arbitration court and making a decision on the case means that you will no longer be able to recognize this debt as bad on this basis (see letter of the Ministry of Finance dated May 29, 2013 No. 03-03-06/1/19566, resolution FAS Volga District dated February 21, 2012 No. A72-2866/2011). This can be done only on the basis of a resolution of the bailiff on the completion of enforcement proceedings or in the event of liquidation of the organization (clause 2 of Article 266 of the Tax Code of the Russian Federation).

If you have access to ConsultantPlus, check whether you are writing off accounts receivable correctly. If you don't have access, get a free trial of online legal access.