Formation of indicators for analyzing the organization’s balance sheet

The balance sheet is the main reporting document of any organization.

The composition of its indicators may vary from company to company, but the analysis is based on general principles and methods. ATTENTION! From 2021, financial statements will be submitted exclusively in electronic form. Paper forms will no longer be accepted. Read more about changes to the rules for presenting financial statements here. We also remind you that in 2021 the reporting forms have been updated.

Analysis of the balance sheet is of practical importance if it is based on reliable information. To avoid its distortions (accidental or intentional), the enterprise must have an internal control system (Article 19 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ). And to externally confirm the reliability of the balance sheet, an audit is used (clause 3 of the Law “On Auditing” dated December 30, 2008 No. 307-FZ). In some cases this is mandatory (Article 5 of Law No. 307-FZ). The list of companies subject to mandatory reporting audit can be found on the website of the Russian Ministry of Finance.

All mandatory accounting reports must meet the requirements for them: comparability, consistency, etc.

Look at a sample balance sheet prepared by ConsultantPlus experts. Get trial access to the system and proceed to the material. It's free.

For more information about what requirements the balance sheet must meet, see the material “What requirements must accounting records satisfy? ”

Let's consider the main stages of the analysis of the balance sheet.

The number of hours spent does not equal success.

Co-founder and director of Strategic Nudge Christine Baker believes that spending time is not the same as achieving a goal:

“You work until you reach your goal—whether it's your first product launch, your first sale, your first year of $100,000 in sales, or anything like that. If it takes 20 or 70 hours a week, so be it. Of course, you will still have to factor in all your other responsibilities in the day - business, family, and perhaps part-time work in order to maintain income during the most difficult first months or years of your business, time for hobbies."

Maggie Patterson, founder of Small Business Boss, has experienced both 20-hour and 80-hour work weeks in her life:

“The essence of entrepreneurship is that you can control how many hours you need to work to grow your business.”

Analysis of the balance sheet using an example: preliminary stage

Let's consider an example of analyzing the balance sheet of an enterprise. The balance sheet of Sekunda LLC as of December 31, 2020 is as follows:

| Indicator name | Code | As of 12/31/2020 | As of 12/31/2019 | As of 12/31/2018 |

| ASSETS | ||||

| Fixed assets | 1150 | 320 | 250 | 200 |

| Reserves | 1210 | 205 | 160 | 115 |

| Accounts receivable | 1230 | 170 | 190 | 160 |

| Financial investments (excluding cash equivalents) | 1240 | 50 | 50 | — |

| Cash and cash equivalents | 1250 | 120 | 210 | 25 |

| BALANCE | 1600 | 865 | 860 | 500 |

| PASSIVE | ||||

| Authorized capital | 1310 | 10 | 10 | 10 |

| retained earnings | 1370 | 385 | 210 | 85 |

| Accounts payable | 1520 | 470 | 640 | 405 |

| BALANCE | 1700 | 865 | 860 | 500 |

The first reading of this report can be called introductory: the balance sheet figures assess the general structure of property and liabilities, the availability of raised funds, etc.

In this case, we are dealing with a developing company: an annual increase in the balance sheet currency, the appearance of financial investments in the asset structure, an increase in the cost of fixed assets (which may indicate the company’s intentions to invest in the development of its production potential), a steady decrease in debts - and all this without attracting long-term borrowed funds.

Preliminary conclusions have been made and we can proceed to a more detailed analysis. To do this, we will conduct a horizontal and vertical analysis of the balance sheet.

Application in the analysis process

Very often, when conducting financial analysis and calculating ratios, important initial information is the state of the company’s current assets and their individual elements. During the research process, attention is paid specifically to the study of current assets: their dynamics and structure.

There are two options for conducting analytics: horizontal and vertical methods. When analyzing the financial condition of an enterprise, both of these methods are used equally often.

Horizontal analysis of the balance sheet

Using horizontal analysis, we compare the balance sheet indicators by reporting dates (to simplify the example, we use data at the beginning and end of the reporting period):

| Balance sheet item | As of 12/31/2020 | As of 12/31/2019 | Deviation (+/–) | |

| sum | % | |||

| Property dynamics | ||||

| Including: non-current (OS) | 320 | 250 | +70 | +28,00 |

| negotiable | 545 | 610 | –65 | –10,65 |

| Reserves | 205 | 160 | +45 | +28,13 |

| Accounts receivable | 170 | 190 | -20 | –10,53 |

| Financial investments (excluding cash equivalents) | 50 | 50 | – | – |

| Cash and cash equivalents | 120 | 210 | -90 | –42,86 |

| Capital dynamics | ||||

| Including: equity | 395 | 220 | +175 | +79,55 |

| Authorized capital | 10 | 10 | – | – |

| retained earnings | 385 | 210 | +175 | 83,33 |

| borrowed capital | 470 | 640 | –170 | –26,56 |

| Sources of funds in calculations (accounts payable) | 470 | 640 | –170 | –26,56 |

A horizontal analysis of the balance sheet showed the following: during the reporting period, non-current assets increased by 28%, which may indicate the expansion of activities and growth of the company’s economic potential. At the same time, working capital decreased (by 10.65%) - mainly due to a decrease in cash balances (by 42.86%). There was an increase in working capital in inventories by 28.13%, which indicates a decrease in liquidity and may affect the solvency of the company. The presence of short-term financial investments in the current assets indicates a desire to invest funds in order to obtain additional profit. The growth of the balance sheet currency must also be compared with the rate of inflation and revenue growth.

If you have access to ConsultantPlus, find out how to assess the solvency of a counterparty based on the balance sheet. If you don't have access, get a free trial of online legal access.

The essence of balance sheet indicators

Financial indicators of the balance sheet are determined by analyzing the financial statements.

Analysis of financial statements consists of analysis of all its forms, including explanatory notes and the final part of the auditor’s report. When carrying out a preliminary analysis of financial statements, the dynamics of two types of sick reporting items are identified and assessed:

- which indicate the extremely unsatisfactory position of the enterprise in the reporting period. This is reflected in a poor financial position, represented by uncovered losses, overdue loans and borrowings and accounts payable.

- which indicate certain regularly recurring shortcomings in the company’s work, recorded in the financial statements for several adjacent periods. They include overdue accounts receivable, debt that is written off to financial results, collected fines, penalties and interest.

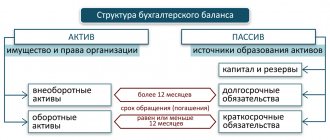

The balance sheet analysis is carried out in accordance with the balance sheet or aggregated analytical balance sheet. When analyzing, it is advisable to determine the growth rate of the most significant items or group of items by comparing the results obtained with the growth rate of sales revenue.

Too lazy to read?

Ask a question to the experts and get an answer within 15 minutes!

Ask a Question

Note 1

The most important area is the vertical analysis of the balance sheet, during which the share and structural dynamics of individual groups and items of assets and liabilities of the balance sheet are assessed.

Determination of the structure of articles (vertical analysis) and the share of indicators

Using this type of balance sheet analysis, we examine the structure of indicators over time:

| Balance sheet item | As of 12/31/2020 | As of 12/31/2019 | Shifts in structure, % | ||

| sum | % to total | sum | % to total | ||

| Property structure | |||||

| Including: non-current assets (OC) | 320 | 36,99 | 250 | 29,07 | +7,92 |

| current assets | 545 | 63,01 | 610 | 70,93 | –7,92 |

| Reserves | 205 | 37,61 | 160 | 26,23 | +11,38 |

| Accounts receivable | 170 | 31,20 | 190 | 31,15 | +0,05 |

| Financial investments (excluding cash equivalents) | 50 | 9,17 | 50 | 9,17 | – |

| Cash and cash equivalents | 120 | 22,02 | 210 | 34,43 | -12,41 |

| Capital structure | |||||

| Including: equity | 395 | 45,66 | 220 | 25,58 | +2,02 |

| borrowed capital | 470 | 54,36 | 640 | 74,42 | – |

A vertical analysis of the balance sheet showed that during the reporting period there were no significant changes in the overall structure of property and capital.

The growth of non-current assets amounted to 7.92%. In the structure of current assets, small structural changes are observed in the lines “Cash and cash equivalents” (12.41%) and inventories (11.38%). An increase in working capital in inventories reduces their turnover, which may negatively affect current liquidity. The share of equity in the balance sheet currency amounted to 45.66% at the end of the period, mainly due to the share of retained earnings in equity (97.47%). There are no uncovered losses on the balance sheet.

The company does without long-term loans and borrowings, that is, the volume and structure of equity capital allows it to organize the production process and develop without external borrowings.

Example of a balance sheet and its analysis

Let's consider the comparative analytical balance using the example of conditional trading. For clarity, we present it in the table below.

Example of reporting of Orion LLC for 2015-2017. All indicators are presented in rubles.

| Assets/Balance Sheet | 2015 | 2016 | 2017 | Dynamics of indicators | Indicator growth rate (%) |

| 1. Non-current assets | 140376 | 131383 | 204096 | 63720 | 145,4 |

| 2. Current assets | 505047 | 991666 | 1221270 | 716223 | 241,8 |

| 2.1. Reserves | 42801 | 50339 | 52420 | 9619 | 122,5 |

| 2.2. Accounts receivable | 61984 | 743478 | 769202 | 707218 | 1241,0 |

| 2.3. Cash and financial investments | 400093 | 197673 | 399422 | -671 | 99,8 |

| 2.4. Others | 169 | 176 | 226 | 57 | 133,7 |

| TOTAL balance | 645423 | 1123049 | 1425366 | 779943 | 220,8 |

| LIABILITIES | |||||

| 3. Own capital | 551026 | 718786 | 519694 | -31332 | 94,3 |

| 4. Long-term liabilities | 9028 | 308210 | 506842 | 497814 | 5614,1 |

| 5. Current liabilities | 85369 | 96053 | 398830 | 313461 | 467,2 |

| 5.1. Loan obligations | — | — | — | — | — |

| 5.2. Accounts payable | 85369 | 96053 | 398830 | 313461 | 467,2 |

| TOTAL balance | 645423 | 1123049 | 1425366 | 779943 | 220,8 |

Data from a horizontal analysis of the balance sheet allow us to conclude that in 2021 there was an increase in the total amount of the company’s assets by 779,943 thousand rubles, mainly due to an increase in the value of non-current assets by 63,720 thousand rubles, as well as growth of current assets by 716,223 thousand rubles. The increase in the amount of working capital was ensured by an increase in the value of long-term liabilities by 497,814 thousand rubles, as well as short-term liabilities by 313,461 thousand rubles.

At the next stage, we will consider the application of the methodology for vertical analysis of the company’s analytical balance sheet in the table below.

Vertical methodology as applied to Orion LLC for 2015-2017. (%)

| Balance sheet item | 2015 | 2016 | 2017 | Dynamics of indicators over a period of time |

| ASSETS | ||||

| 1. Non-current assets | 21,7 | 11,7 | 14,3 | -7,4 |

| 2. Current assets | 78,3 | 88,3 | 85,7 | 7,4 |

| 2.1. Reserves | 6,6 | 4,5 | 3,7 | -3,0 |

| 2.2. Accounts receivable | 9,6 | 66,2 | 54,0 | 44,4 |

| 2.3. Cash and financial investments | 62,0 | 17,6 | 28,0 | -34,0 |

| 2.4. Others | — | — | — | — |

| TOTAL balance | 100,0 | 100,0 | 100,0 | 0,0 |

| LIABILITIES | ||||

| 3. Own capital | 85,4 | 64,0 | 36,5 | -48,9 |

| 4. Long-term liabilities | 1,4 | 27,4 | 35,6 | 34,2 |

| 5. Current liabilities | 13,2 | 8,6 | 28,0 | 14,8 |

| 5.1. Loan obligations | — | — | — | — |

| 5.2. Accounts payable | 13,2 | 8,6 | 28,0 | 14,8 |

| TOTAL balance | 100,0 | 100,0 | 100,0 | — |

As can be seen from the table, in the structure of the analytical balance sheet the share of current assets is maximum. In addition, there is a noticeable upward trend in this share by 7.4% by 2021. Accordingly, the share of non-current assets by 2021 is reduced by 7.4%. The liability structure of the balance sheet contains the maximum share of equity capital. By 2021, it is sharply reduced by 48.9%, which negatively affects the structure of the balance sheet. The share of long-term liabilities by 2021 is growing by 34.2%, and short-term liabilities by 14.8%.

The positive results of the assessment of the consolidated analytical balance are the following trends:

- Growth in the value of the balance sheet currency in 2021.

- The growth rate of current assets (241.8%) exceeds the growth rate of non-current assets (145.4%).

- The organization’s own capital is more than 50%, but only in 2015 and 2016.

However, the presented form of analytical balance also has negative characteristics:

- The organization's equity in 2021 is below 50%.

- The growth rate of long-term liabilities (5614%) and short-term liabilities (467%) exceeds the growth rate of equity capital (94%).

- The growth rates of accounts receivable (1241%) and accounts payable (467.2%) differ significantly.

However, the presented analytical balance sheet and its example do not provide complete information for the investor about the effectiveness when studying the financial situation. They only allow you to assess the current state and dynamics of the company's assets and liabilities.

Analyzing the Balance Sheet Using Financial Ratios

By calculating special coefficients, further analysis of the balance sheet is carried out:

Solvency analysis

| Coefficient | Calculation | Recommended Range | |

| Formula | Sum | ||

| Financial dependency ratio. Read more about the coefficient in the article “Financial dependence coefficient (balance sheet formula)” | Balance sheet currency / equity | 865 / 395 = 2,2 | ≤2,0 |

| Financial independence ratio. Read more about the coefficient in the article “Financial independence coefficient (formula)” | Own capital / balance sheet currency | 395 / 865 = 0,46 | ≥0,5 |

| Total Solvency Ratio | Balance sheet currency / borrowed capital | 865 / 470 = 1,84 | ≥1,0 |

| Debt ratio | Debt capital/equity | 470 / 395 = 1,19 | ≤1,0 |

Liquidity analysis

| Coefficient | Calculation | Recommended Range | |

| Formula | Sum | ||

| Instant liquidity ratio | (DS and DE)*/ KO*** | 120 / 470 = 0,26 | >0,8 |

| Absolute liquidity ratio | (DS and DE + KFV**) / KO | (120+50) / 470 = 0,36 | >0,2 |

| Quick ratio | (DS and DE + KFV + DZ) / KO | (120 + 50 + 170) / 470 = 0,72 | ≥1,0 |

| Average liquidity ratio | (DS and DE + KFV + DZ + Reserves) / KO | (120 + 50 + 170 + 205) / 470 = 1,16 | >2,0 |

| Intermediate liquidity ratio | (DS and DE + KFV + DZ + Inventories + VAT) / KO | (120 + 50 + 170 + 205) / 470 = 1,16 | ≥1,0 |

| Current ratio | Current assets / KO | 545 / 470 = 1,16 | 1,5–2,0 |

* (DS and DE) - cash and cash equivalents.

** KFV - short-term financial. attachments.

*** KO - short-term liabilities.

For more information about liquidity ratios, read the article “Calculation of the liquidity ratio (balance sheet formula)” .

An analysis of the balance sheet using financial ratios showed that solvency indicators are close to the recommended ones. However, the instant, quick and current liquidity ratios show the insufficiency of working capital to repay short-term liabilities at the reporting date.

In addition, it is necessary to calculate financial stability coefficients (autonomy, agility, etc.).

Our articles will help you do this:

- “What does the autonomy coefficient show - the balance formula?”;

- “Agility coefficient (balance sheet formula)” and other materials in the “Analysis of Economic Activity (ABA)” .

Trend, factor and comparative analysis

In addition to the above stages of balance sheet analysis, trend, factor and comparative types of analysis can be carried out. They will complement and expand the volume of analytical data for making the necessary economic decisions.

Thanks to trend analysis, you can form an opinion about the main trend of changes in certain indicators (predictive analysis).

For example, a joint study of the dynamics of short-term debt and cash:

| Balance indicator | As of 12/31/2018 | As of 12/31/2019 | As of 12/31/2020 |

| Accounts payable | 405 | 640 | 470 |

| Cash and cash equivalents | 25 | 210 | 120 |

From the above figures it follows that, as of reporting dates, the nature of changes in the amount of short-term debts corresponds to changes in the volume of cash, but the company’s free cash is not enough to repay these debts.

Using factor analysis, the nature of the influence of the main factors on the change in the value of the indicator under study is determined. It is carried out according to a certain method of analyzing the balance sheet.

To carry out a comparative analysis, additional information is needed - the balance sheet data of one company is not enough. This is due to the fact that when carrying out this type of analysis, the balance sheet indicators of different companies are compared in order to determine their rating.

Specifics of analyzing the balance sheet of individual companies using the example of a bank balance sheet (Form 1)

Banks, although they are commercial companies and are created to make a profit, have specific features. They are subject to special legislation, maintain a special chart of accounts and build a different methodology for accounting processes.

At the same time, the main approaches to analyzing a bank’s balance sheet are in many ways similar to analyzing the balance sheet of an ordinary commercial company. For the bank balance sheet, the main stages of analysis also remain relevant:

- preliminary (reading the balance sheet, structuring its items, etc.),

- analytical (description of calculated indicators of structure, dynamics, relationship between balance sheet indicators);

- final (evaluation of analysis results).

In the process of analyzing the bank’s balance sheet, special coefficients are also calculated, but their types differ from those discussed earlier:

- bank reliability coefficient (capital adequacy ratio),

- return on assets ratio (shows the efficiency of using assets and quality based on their profitability),

- leverage ratio (interbank loans), etc.

To learn how banks analyze the creditworthiness of their clients, read the material “Methods for assessing the creditworthiness of commercial bank clients.”

What are the consequences of lack of rest?

An employee of the Microsoft venture fund, Makand Mohan, believes that a businessman should not have a balance between work and personal life:

“Almost every entrepreneur will tell you that they work a lot. This is par for the course. Those who are older (after 35 years, usually) will insist on their ability to manage time between work and personal life. In fact, this is impossible in a startup. If you have such a balance, then you are not taking your business seriously enough.”

Perhaps the fact is that successful entrepreneurs are people who love their business and really enjoy devoting all their time to it. However, lack of proper rest and too long working hours have a negative impact on concentration, attention and work performance, as well as on mood and family relationships.

Research shows that excessive workaholism can negatively impact productivity and health. While famous entrepreneurs motivate us to work 60 to 100 hours a week, science doesn't agree. There is no right answer to how many hours you should work. It is important to monitor your physical and mental state, and not try to copy other people's behavior patterns.

Lack of breaks and overwork threaten to reduce concentration. Even targeted short breaks from work, such as a 15-minute coffee break every two hours, can seriously help attention and concentration. Another way to work more concentratedly is the Pomodoro Method.

Online program to facilitate the analysis process

Modern information processing tools can significantly simplify the process of comprehensive analysis of the balance sheet. Calculations are carried out both using standard computer programs (for example, using Excel, where you can carry out calculations, create tables and charts), and using specialized programs that allow you to conduct financial analysis online - via the Internet.

The use of specialized software not only saves time, but also significantly expands the types of analysis. They allow you to analyze market stability, business activity, score assessment of financial stability, etc. In addition, developers of specialized programs provide the possibility of adapting and changing the program depending on the goals and objectives of the analysis, taking into account the specifics of a particular enterprise.

Results

Analysis of balance sheet indicators is a voluminous and multi-stage process. Its results make it possible to identify potential risks, develop the financial policy of the enterprise and contribute to effective management decisions. The analysis process can be facilitated by using specialized programs.

Sources:

- Federal Law of December 6, 2011 No. 402-FZ

- Federal Law of December 30, 2008 No. 307-FZ

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.