The movement of material assets in the territories of KFU is carried out according to the invoice for the internal movement of fixed assets f. OS-2, which is used when transferring fixed assets from one materially responsible person to another within an institution or with centralized accounting - from one institution to another, in accordance with the established procedure in accordance with Instruction of the Ministry of Finance of the Russian Federation No. 2 107N dated December 30, 1999.

To export (remove)/import (bring in) material assets you must:

- Fill out the memo (sample).

- Sign the memo in the department of accounting of material assets of the Department of Accounting and Reporting of KFU.

- Submit the memo to the reception of the director of the Department for Internal Regime, Civil Defense and Labor Safety of KFU.

- On the appointed day, receive a memo endorsed by the Director of the Department.

- When removing (exporting) / bringing in (importing) material assets, present a memo to the security officer.

Employees of the maintenance and repair units of the chief engineer's service who carry out maintenance and repair of utility networks have the right to remove (bring in) tools, instruments, and consumables without special permission.

For employees providing support for the information and telecommunications infrastructure of KFU, on the basis of a memo from the head of the relevant structural unit, agreed with the director of the Department, the Service issues passes for the export (removal)/import (input) of material assets for a period of 30 days to 1 calendar year. The pass indicates: structural unit, name of imported (brought in)/exported (taken out) items, (type) brand, serial/inventory numbers, validity period ().

Export (carrying out)/import (bringing in) material assets according to oral orders is not allowed!

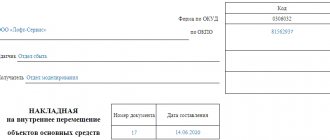

Form OS-2. Invoice for internal movement of fixed assets

The invoice for the internal movement of fixed assets, form OS-2, is intended to document the actual movement of any fixed assets of the organization. This can be interaction between workshops, sections, departments. The main thing is that both sides of the process (receiving and receiving units) belong to the same company.

FILES

The fixed assets of an organization may include buildings, various equipment, machines, instruments, computer equipment, inventory, various tools, livestock, etc. All this may well be transferred from one workshop or site to another.

If the useful life of different parts of one building is different, then it is worth dividing it into two independent objects and describing it separately.

Paperwork

The transfer of property between OPs is not a sale, since the transfer of ownership does not occur during such a transaction.

You can develop and approve your own document on the transfer of fixed assets or use a unified form.

https://www.youtube.com/watch{q}v=ytpolicyandsafetyru

If the OP is not allocated to a separate balance sheet, then form No. OS-2 “Invoice for the internal movement of fixed assets”, which is issued on the basis of an order from the head of the organization, is suitable. After all, the main thing is to record the transfer of the operating system from one financially responsible person to another.

But if the OP is allocated to a separate balance sheet, then the information in form No. OS-2 will not be enough, since not only the initial cost of the OS is “transferred”, but also the “accumulated” depreciation (in order to continue further depreciation). In this case, it is better to develop and approve your own form.

LLC "Karavan" name of the organization

| name of the structural unit |

| name of the structural unit |

Invoice for internal movement of fixed assets No. VP-15 dated July 1, 2014

Note (brief description of the technical condition of a fixed asset item)

| Objects are in working (good) condition |

Fixed assets

Passed

| Head of temporary storage warehouse job title | signature | HELL. Sopov full name |

Accepted

| Head of technical support department job title | signature | V.A. Mukhin full name |

In the inventory card (book) of accounting for the fixed asset object, the movement is noted

| Chief accountant (accountant) job title | signature | V.S. Konakova full name |

All copies are signed by the financially responsible persons of the transmitting and receiving OP.

After that:

- if accounting is maintained by a centralized accounting department, one copy is transferred to the accounting department. If accounting in the OP is maintained independently, one copy is transferred to the accounting department of the transmitting and receiving OP;

- one copy remains with the financially responsible person of the transferring party;

- one copy is transferred to the financially responsible person of the receiving party.

We invite you to read: Advantages of an employment contract for an indefinite period

Data on the movement of fixed assets must be recorded in section 4 of the OS-6 inventory card of the transferred fixed assets (if you use unified forms). Let's format it like this.

Section 4 “Information on acceptance, internal movements, disposal (write-off) of fixed assets”

If the OP is allocated to a separate balance, then together with the invoice, the receiving OP must be transferred:

- act of acceptance and transfer of an asset (form No. OS-1), which was issued upon receipt of the asset;

- inventory card;

- all technical documentation.

Filling algorithm

The invoice is filled out on both sides. It consists of a header on the title side, a table of seven columns that continues on the reverse side, as well as a place for a brief description of the transferred object and signatures of the responsible persons.

In the upper right corner of the title part of the document there is a link to the Decree of the State Statistics Committee of 2003, which approved this form as mandatory. After 10 years, it became a recommendation, but its use continues.

At the top of the invoice, the OKUD and OKPO forms and the name of the company within which the movement takes place are indicated. The unit from which the object is being withdrawn is indicated first (it is called the “delivery”). The recipient department is indicated below.

Attention! The invoice must be filled out by the delivery department.

After the names of the departments, the name of the document, the date of preparation of the paper and the assigned number are written.

Below is a table with:

- number;

- a description that includes the date of manufacture (or construction), full name, inventory number;

- number of transferred objects in pieces;

- cost;

- results.

After the table, space is left to describe the object, its technical and other characteristics. When filling out, these lines cannot be left blank.

You can mention the condition (good, excellent, satisfactory), existing defects (scuffs, chips, etc.), and describe the packaging. If warranty cards or instructions are included, these are also included.

At the end there should be signatures (deciphered) of the persons who made the delivery and acceptance. The fact that information about the movement was entered into the accounting book is confirmed by the chief accountant (or simply the accountant who carried out the data transfer).

Important! When putting signatures, mentioning the positions of persons is mandatory.

Nuances of filling

Rows in the table should not be left empty. If a document is generated electronically, then unfilled sections of the document are simply deleted. If the paper is already printed, they are crossed out. Corrections to the invoice are not recommended. But if a mistake was made, it is corrected by a longitudinal strikethrough and the inscription “Believe the corrected one.” Moreover, next to this inscription there must be signatures of all persons who are also signed at the end of the document: the chief accountant, the handing over and receiving persons.

Is it possible to change graphs?

All this data is necessary for maintaining full-fledged accounting and warehouse records in the organization. Since 2013, this form has ceased to be mandatory. It became only advisory, in accordance with the law “On Accounting” dated 06.12.2011 No. 402-FZ.

At its own discretion, the organization has the right to refuse some columns of the primary document or add new ones. However, all these changes must be documented and have good reasons.

In short, the form is widely used today because it is convenient, illustrates the maximum amount of information and does not confuse regulatory authorities when conducting inspections and audits.

How many copies will be required?

The invoice must be filled out in at least 3 identical copies. This is done so that one invoice remains with the accountant (or the employee performing his duties) for the generation of further reporting. The second paper must be kept by the employee responsible for it for a specific facility. And the third option must be provided to the receiving party as confirmation of the verified fact. Ideally, all 3 invoices have 3 signatures of employees who are financially responsible.

Control

If during the inspection it is discovered that the object is under the jurisdiction of one division, but is registered with another, then the organization will face administrative liability in the form of a fine.

If a violation is detected for the first time and it does not lead to an understatement of taxes, then the company can get off with a fine of 5 thousand rubles.

If during the audit it is discovered that there is no invoice for the movement of fixed assets, form OS-2, and this fact will underestimate the taxes due from the organization, then less than 15 thousand rubles. There is no penalty for such a violation. Moreover, an amount of 10% of the total tax not paid for this reason may be assigned (but this amount will still not be less than 15 thousand rubles).

OS: Relocation, restoration, inventory, disposal, write-off, transfer, revaluation

Purpose of the lecture:

master the accounting of such operations with fixed assets as movement, restoration, inventory, disposal, write-off, revaluation, transfer.

3.1. Moving OS

OS objects during operation can move between organizational units. This process may be accompanied by a change of financially responsible persons.

Consider the following example:

On March 2, 2011, it was decided to move the air conditioner (inventory number 000000002) from the Administration division of the organization to the Production Shop division and appoint a new materially responsible person for it - Ivan Ivanovich Ivanov.

In order to perform this operation, create a document Moving OS (OS > Moving OS)

. In Fig. 3.1 you can see the completed document form.

Rice.

3.1. Document Moving OS

Let's consider filling out the fields of the document.

Event

— this field is filled in from the directory

Events with fixed assets

; when selected from this document, the

Internal movement

with the event type

Internal movement

, fig. 3.2.

Rice.

3.2. Events with fixed assets

Delivery Groups

and

Recipient

, their details

Location of the OS

and

MOL

are filled in in accordance with the initial and final location of the OS (divisions) and financially responsible persons between whom the OS is moved. Various options for filling out these fields are possible, allowing you to implement, for example, movement between materially responsible persons within one department, movements between different departments while maintaining the materially responsible person.

Parameter group Depreciation

allows you to set a new method for reflecting depreciation expenses (or, without specifying, keep the old one), enable or disable the calculation of depreciation.

In addition, the method of reflecting depreciation expenses can be changed using a specialized document - Changing the method of reflecting depreciation expenses of fixed assets (OS > Depreciation Parameters > Changing the method of reflecting depreciation expenses of fixed assets)

.

We must not forget that, if necessary, actions performed by the document Transfer of fixed assets

and others can be performed using the document

Operation (accounting and tax accounting)

.

Tabular part Fixed assets

contains a list of moving OS objects.

Let's review the document and see what movements it generated in accounting, Fig. 3.3.

Rice.

3.3. Result of document Transfer of OS

Namely, the document performed movements in the registers Location of OS (accounting)

,

Events of fixed assets of organizations

,

Methods of reflecting expenses for depreciation of fixed assets (accounting)

,

Calculation of depreciation of fixed assets (accounting)

,

Calculation of depreciation of fixed assets (tax accounting)

. These movements recorded new parameters of the fixed asset object - its new location, a new financially responsible person, parameters for calculating depreciation. The document can also form, if necessary, accounting movements. In our case, the fact of moving fixed assets between departments does not affect the reflection of information on fixed assets in accounting.

The movement of the fixed assets object in this case led to one very noticeable main consequence - namely, when calculating depreciation, it will be written off to account 20, and not to account 26, as was previously the case. Pay attention to the state of the register Methods of reflecting expenses for depreciation of fixed assets (accounting)

, rice.

3.4. The register contains a new entry dated 03/02/2011 about the new method of depreciation of the Air Conditioner

, however, the old entry is also retained. As a result, starting from March 2011, depreciation will be reflected in a new way.

Rice. 3.4. Register of information Methods of recording depreciation of fixed assets (accounting)

What is the OS-2 form intended for?

An invoice in the OS-2 form is issued at the site from which the internal movement of fixed assets is carried out. The information contained in this invoice is subsequently used to fill out the inventory book (forms OS-6, OS-6a and OS-6b) or a card issued for this transported object.

Read about the design of these forms in the articles:

- “Unified form No. OS-6 - form and sample”;

- “Unified form No. OS-6a - form and sample”;

- “Unified form No. OS-6b - form and sample.”

The procedure for completing the OS-2 form

The invoice in form OS-2 is issued in 3 copies, one of which is intended for the accounting service, the second remains with the person responsible for the safety of the moved object, and the third is issued for the recipient of the property.

Each copy of the invoice for the movement of assets (OS) within the company must be signed by the deliverer and the recipient, who are financially responsible for the property.

In accordance with the Law “On Accounting” dated 06.122011 No. 402-FZ, since 2013, unified forms, including the OS-2 invoice, are no longer mandatory for use - they are only recommended for use. This means that each company can develop its own form based on the OS-2 form.

Internal movement of fixed assets - document flow

In total, Resolution No. 7 approved 14 forms of primary documents, including the Invoice for the internal movement of fixed assets (Form No. OS-2). According to the Instructions for the use and completion of primary accounting documentation forms for accounting for fixed assets, form N OS-2 is used to register and record the movement of fixed assets within an organization from one structural unit (workshop, department, site, etc.) to another . The invoice is issued by the structural unit that transfers the fixed asset, that is, it is the deliverer. Three copies of the invoice are drawn up: the first copy is transferred to the accounting department of the organization, the second copy remains with the person responsible for the safety of the fixed assets of the delivery unit, and the third copy is intended for the unit receiving the fixed asset. Each of the three copies must be signed by the responsible persons of the delivering unit and the receiving unit. The accounting unit for fixed assets, as you know, is an inventory item . In accordance with clause 11 of Methodological Instructions N 91n, each inventory item is assigned a corresponding inventory number . During the period that the fixed asset is in the organization, the inventory number assigned to the object is retained. When fixed assets are received by the organization, an inventory card (book) is opened for each inventory item. The basis for filling out the card are, in particular, acts of acceptance and transfer of fixed assets (forms NN OS-1, OS-1a, OS-1b). The movement of fixed assets within the organization is also reflected in the inventory card (book) for accounting for fixed assets (forms NN OS-6, OS-6a, OS-6b). In the inventory card for recording a fixed asset object (Form N OS-6), internal movement is reflected in section. 4 “Information on acceptance, internal movements, disposal (write-off) of fixed assets.” In the tabular part of Sect. 4 indicates the date and number of the document on the basis of which the entry is made, the type of transaction, the name of the structural unit, the residual value of the object, as well as the surname and initials of the person responsible for storage. So, let's look at the order in which the Invoice for the internal movement of fixed assets should be filled out (Form N OS-2). The invoice indicates the OKUD form code. According to the All-Russian Classifier of Management Documentation OK 011-93, approved by Decree of the State Standard of the Russian Federation of December 30, 1993 N 299, form N OS-2 corresponds to code 0306032. Then the name of the organization, its OKPO code assigned by the territorial body of state statistics, and also the name of the structural unit-deliver and recipient. Please note that the Procedure for the use of unified forms of primary accounting documentation, approved by Resolution of the State Statistics Committee of Russia dated March 24, 1999 N 20, determines that all details of the unified forms must remain unchanged (including codes). Removing individual details from unified forms is not allowed. Next, you should indicate the document number and the date of its preparation. Documents must be numbered in chronological order and numbers must not be repeated during the reporting year. If an organization keeps records using computer technology, then a number is assigned to the document when it is compiled, which avoids repetition. If an organization has a large number of divisions, it is possible to provide for the numbering of documents separately for each such division. In this case, all departments should be assigned a digital or letter code, which will be indicated in the document. According to paragraph 4 of Art. 9 of the Law “On Accounting”, the primary accounting document must be drawn up at the time of the transaction. If this is not possible, then the document is drawn up immediately after its completion. Persons drawing up and signing primary documents must ensure timely and high-quality execution of documents, the reliability of the data contained in the documents, as well as their transfer within the established time frame to the accounting department to reflect transactions in accounting. After filling out the details already mentioned, you can begin filling out the tabular form of the invoice. It indicates the name of the transferred fixed asset object, the date of its acquisition (year of manufacture, construction), as well as the inventory number assigned to the object. The number of objects being transferred, the unit cost and the total cost are also indicated. In the case of simultaneous transfer of several names of fixed asset objects, information about each object is entered in a separate line indicating its number. In the unfilled terms of the invoice, dashes should be added. On the reverse side of Form N OS-2, in the “Note” section, a brief description of the technical condition of the fixed asset object is indicated, as well as the positions and personnel numbers of the persons handing over and accepting the valuables. It also contains transcripts of the signatures of these persons indicating the date of signing the document. The chief accountant makes a note that the movement of the fixed asset item is noted in the inventory card (book). So, the invoice must be properly executed, that is, all the necessary details must be filled out in the document and the document must have the appropriate signatures, as established by clause 7 of Methodological Instructions No. 91n.

Note! According to clause 82 of Methodological Instructions No. 91n, the movement of a fixed asset item between structural divisions of an organization is not recognized as a disposal of a fixed asset item. The organization's costs associated with moving an object within the organization, that is, transportation and other costs, according to clause 74 of Methodological Instructions N 91n are included in production costs (selling costs).

It is necessary to recall that assets in respect of which the conditions provided for in clause 4 of PBU 6/01 are met, and with a value within the limit established by the organization’s accounting policy, but not more than 20,000 rubles. per unit, can be reflected in accounting and reporting as part of inventories. To ensure the safety of these objects, the organization should organize control over the movement of such objects. In Letter of the Ministry of Finance of Russia dated May 30, 2006 N 03-03-04/4/98 it is noted that if an organization decides to account for such objects as part of inventories, it must maintain appropriate accounting cards for them - a receipt order in the form N M-4, demand invoice in form N M-11, materials accounting card in form N M-17 and other primary documents . These forms of primary accounting documents were approved by Resolution of the State Statistics Committee of Russia dated October 30, 1997 N 71a “On approval of unified forms of primary accounting documentation for accounting of labor and its payment, fixed assets and intangible assets, materials, low-value and wear-and-tear items, work in capital construction” . A few words should be said about how the transfer of property from one division to another is reflected in the accounting records of an organization. In addition to the fact that an organization can have various workshops, departments, sites, production and other divisions in its structure, it can also have representative offices and branches. Representation according to Art. 55 of the Civil Code of the Russian Federation (hereinafter referred to as the Civil Code of the Russian Federation) is a separate division of a legal entity located outside its location, which represents the interests of the legal entity and protects them. A branch is a separate division of a legal entity located outside its location and performing all or part of its functions, including the functions of a representative office. Clause 3 of Art. 55 of the Civil Code of the Russian Federation establishes that representative offices and branches are not legal entities and are vested with property by the legal entity that created them. Accounting in an organization that transfers fixed assets to its branches will depend on whether or not the branch is allocated to a separate balance sheet. If the branch is not allocated to a separate balance sheet, then the operations carried out by the branch, as well as its property and liabilities, are accounted for by the main organization in the corresponding sub-accounts opened to the accounting accounts. According to the Chart of Accounts for accounting financial and economic activities of organizations and the Instructions for its application, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n (hereinafter referred to as the Chart of Accounts), an account is intended to summarize information on the availability and movement of fixed assets in an organization 01 "Fixed assets". On account 01 “Fixed assets”, analytical accounting should be kept for individual inventory items, while the construction of analytical accounting should provide the ability to obtain data on the availability and movement of fixed assets necessary for the preparation of financial statements (by type, location, and so on). For account 01 “Fixed assets” you can open, for example, the following subaccounts: 01-1 “Fixed assets in operation of the parent organization”; 01-2 “Fixed assets in the operation of the branch.” Then the transfer of a fixed asset item to the branch will be reflected in the accounting record as a debit entry in account 01-2 “Fixed assets in operation of the branch” in correspondence with the credit of account 01-1 “Fixed assets in operation of the parent organization.” The corresponding sub-accounts must be opened for the depreciation account for fixed assets (account 02 “Depreciation of fixed assets”), as well as for other accounts. If a branch of an organization is allocated to a separate balance sheet, accounting in the main organization will be slightly different. The chart of accounts for summarizing information on all types of settlements with branches, representative offices, divisions and other separate divisions of the organization, allocated to separate balance sheets, is account 79 “Intra-business settlements”. It is recommended to open a subaccount 79-1 “Settlements for allocated property” for account 79 “On-farm settlements”. This sub-account takes into account the status of settlements with branches, representative offices, departments and other separate divisions of the organization, allocated to separate balance sheets, for non-current and current assets transferred to them. The property allocated to the divisions is written off by the organization from account 01 “Fixed assets” to the debit of account 79 “Intra-business settlements”. Accordingly, the registration of property by a separate division is reflected in the credit of account 79 “Intra-business settlements” in correspondence with the debit of account 01 “Fixed assets”.

www.mosbuhuslugi.ru

Where is OS-2

The invoice form for internal movements of funds was approved by State Statistics Committee Resolution No. 7 dated January 21, 2003. You can download its form on our website.

You can also download a completed sample of this document from us.

Reasons for transferring an object within an organization

The decision on the need for internal movement of fixed assets within one owner can only be made by the management of the enterprise.

Important! Funds can move between structural divisions, workshops, areas, etc.

In turn, the management of the department into which the funds fall has the right to distribute them within the association.

The following circumstances can be considered the main reasons for the internal movement of operating systems:

- the need for repairs, reconstruction or modernization;

- the need to transfer fixed assets to a subsidiary (branch), for which a separate balance sheet is allocated;

- the need to transfer OS objects to another department.

Lesson 9.7

Lesson 9

Moving the OS.

OS objects during operation can move between organizational units. This process may be accompanied by a change of financially responsible persons.

Consider the following example:

On January 27, 2009, it was decided to move the air conditioner (inventory number 000000002) from the Administration division of the organization to the Production Shop division and appoint a new materially responsible person for it - Ivan Ivanovich Ivanov.

In order to perform this operation, create a document Moving OS ( OS > Moving OS ). In the picture below you can see the completed document form.

Let's look at the features of filling out its fields.

In the Organization , enter the organization whose fixed asset you want to move.

In the Event , enter the name of the event that occurs with the fixed asset. This event must be selected from the Fixed Asset Events . If, when you open the reference book from the document window, you find it empty, you need to create a new event, and, in this case, you need this event to have the form Internal movement . The name of the event is not particularly important.

In the group of parameters Data for accounting, we must indicate the division ( Production workshop or Administration ) and the new financially responsible person ( Ivanov Ivan Ivanovich ).

In the tabular section of Fixed Assets , you need to indicate those OS objects that are to be moved. It is filled out based on the Fixed Assets .

After posting the document, it does not generate accounting and tax records, but makes changes to some registers:

In the register, information about the location of the OS (accounting) was made that the Air Conditioner was moved to the Production Shop under the financial responsibility of Ivan Ivanovich Ivanov .

OS Events information register, a record is made of the fact of internal movement of an OS object.

I think here you might have noticed that the fixed asset was moved from a division for which depreciation on fixed assets is charged to account 26, to a division for which expenses are recorded on account 20. This means that our work on moving the fixed asset is not yet completed - you need to tell the system how to allocate depreciation in a new way. To do this, you need to use the document Changing the method of reflecting expenses for depreciation of fixed assets ( OS > Depreciation parameters > Changing the method of reflecting expenses for depreciation of fixed assets ).

In the Event , you must indicate the basis for the change in depreciation. It is filled out from the directory Events with fixed assets (event type - Other ).

The Method field should be filled in indicating the depreciation method that should now be applied to the asset.

Fixed Assets table field , we enter a list of fixed assets for which we want to change the way in which depreciation expenses are reflected.

After execution, the document generates records in the following registers:

In the information register Methods for reflecting expenses for depreciation of fixed assets (accounting), an entry is made about the new method used for the fixed assets object.

In the information register Methods of reflecting expenses for depreciation of fixed assets (tax accounting), an entry is also made about the new method of reflecting expenses.

organization's OS Events information register, a record is made of the event that led to a change in the method of reflecting depreciation expenses.

Pay attention to what the information register looks like. Method of reflecting expenses for depreciation of fixed assets (accounting).

Please note that there are two entries in the register for the Air Conditioner . The first was done when accepting an object for accounting when entering initial balances for fixed assets. The second was done using the document discussed above. When calculating depreciation at the end of May 2009, depreciation will go to account 26. But starting from January 2009, it will go to account 20.

How to transfer to another financially responsible person within the same owner?

A financially responsible person is considered to be a working citizen whose professional activity involves interaction with company property.

The employee is responsible for its safety, damage and condition, and in case of problems, he compensates the employer for the damage caused.

In order to transfer property under the responsibility of another financially responsible person, it is necessary to carry out several actions.

First of all, you need to take an inventory. The results of the procedure are properly documented.

During the event, the exact quantity of fixed assets and their main characteristics, including condition, are determined.

Both material persons—current and future—as well as members of a specially created commission take part in the inventory.

Next comes the execution of contracts. In this case, there are several of them - about the change of the financially responsible person and about the responsibility assigned to him.

Order to change MOL.

Compiled upon completion of the inventory. The document contains information about employees, as well as fixed assets.

A note is also made on the exact date from which responsibility for the property is transferred to another employee.

Order to transfer OS to another MOL.

Please note that documentation of this nature is quite important. However, there is no standardized form for filling it out.

When issuing an order, the management of the enterprise must comply with certain rules regarding the content of the paper.

If you have a form developed by your company for creating such documents, you can use its sample.

The following information is required to be reflected:

- date of registration;

- serial number;

- full company name;

- the reason why there was a need for internal movement of fixed assets;

- information about the inventory carried out;

- information about financially responsible persons;

- appointment of commission members.

At the end of the order there must be a signature of the chief manager of the enterprise or his deputy.

In addition, when transferring fixed assets to another financially responsible person, the latter draws up a special receipt.

It acts as agreement with the information obtained during the inventory. It also indicates that the new MOL has no claims against the commission members.

There is a corresponding section in the inventory list for registering a note.

A change in the financially responsible person may be due to several factors. Among these, the following should be highlighted:

- dismissal;

- registration of long-term sick leave by the current MOL;

- going on a business trip;

- damage to property, its damage, etc.;

- other unfavorable circumstances.

What documents need to be completed for internal OS movements?

It was previously stated that the movement of OS within an organization must be accompanied by the preparation of special documentation, which must be drawn up properly.

If the established rules are violated, the employer may have problems with inspection authorities.

In this case, several documents must be drawn up - an invoice and an order.

Previously, instead of the first paper, an OS acceptance certificate was used.

At the moment, it is necessary to issue an invoice for internal movement. For this purpose, the unified form of the OS-2 form should be used.

The order can be drawn up in free form, taking into account the generally accepted rules of the company.

Also, marks about the movement of OS within the same owner are placed in the inventory books. Changes are made to section 4 of cards.

Sample order for the transfer of property from one MOL to another

To issue an internal movement order, you do not need to use a unified form. It is enough to adhere to the document management rules used in the company.

The order must contain the following information:

- full name of the paper;

- place and date of issue of the order;

- document's name;

- information about fixed assets transferred within the organization - quantity, cost and other characteristics;

- the name of the divisions in which the fixed assets were previously located and where they are located;

- a note about the persons responsible for the movement;

- a note about the person responsible for executing the order;

- signatures of persons who have read the order.

The chief manager of the enterprise is in charge of processing the order. Without his signature, the document is considered invalid.

order on the internal movement of fixed assets between financially responsible persons - word.

How to issue an invoice to move an asset between financially responsible persons?

An equally important document that must be drawn up when moving fixed assets within the company is the invoice. When filling it out, you should adhere to the unified form of the form - No. OS-2.

The documentation is prepared in 3 copies. The first is intended for the person responsible for the movement, the second for the party receiving fixed assets, and the third for the company’s accounting department.

At the top of the invoice information about the enterprise is displayed:

- name of company;

- information about the OS sender and receiver;

- OKUD form;

- OKPO code.

Next is the paper number and the date of its preparation. The next part of the invoice looks like a table. It consists of 7 columns.

The name of each column should reflect the following meaning:

- serial number of the fixed asset;

- OS name;

- date of acquisition of property;

- inventory serial number;

- number of units;

- the cost of each object;

- the total cost.

If necessary, marks about the state of the OS are placed after the table. There are special lines for this - Notes.

At the end, information about the employee who passed the OS and the employee who accepted them is indicated. A note is made to make changes to the books of fixed assets. The chief accountant also leaves his signature.

invoice for the internal movement of fixed assets from one MOL to another – word.

What is an act

The reason for transporting equipment for which it is necessary to draw up appropriate documents may be the following:

- simple repair;

- for rental;

- delivery to the customer and installation;

- for testing.

The equipment acceptance certificate is necessary to prove the transfer of equipment to the buyer by the supplier.

The form can have three varieties:

- OS-14 (repair);

- OS-15 (installation);

- OS-16 (testing).

Each form is used in a specific situation. Let's look at an example of the OS-14 form, which is necessary for accounting for equipment arriving at the warehouse. After this, the resulting equipment can be used as main equipment.

A contract for sending for repairs must be drawn up only in the presence of all representatives of the special commission responsible for receiving the equipment. The agreement is concluded in several copies, each sample requires the signature of the head or authorized representative.

INTERNAL MOVEMENTS IN BUDGET ACCOUNTING

I.V. Artemova, chief accountant, consultant

Internal movements of fixed assets, intangible assets, and inventories are reflected in a number of cases. This may be a transfer for use, transfer of property to another group, or repurchase of leased property. Changes have recently been made to the accounting treatment of such transactions in budget accounting. In addition, when reflecting internal movements from January 1, 2021, it is necessary to take into account the federal accounting standards that have entered into force.

Types of movements

In some cases, the movement of non-financial assets does not lead to their writing off from the account in which they were recorded, but requires the reflection of internal movement. These types of movements include movements:

| — | between employees and departments; |

| — | temporary issuance outside the institution without removal from the balance sheet; |

| — | between property groups; |

| — | when purchasing leased property. |

Fixed assets

In accordance with paragraph 7 of the Instructions for budget accounting, approved by order of the Ministry of Finance of Russia dated December 6, 2010 No. 162n (hereinafter referred to as Instruction No. 162n), the internal movement of fixed assets between financially responsible persons in the institution is reflected as follows: Debit of account 0 101хх 310 “Fixed assets » Account credit 0 101хх 310 “Fixed assets”. In the current edition at the time of submission of the journal Instructions for the Application of the Unified Chart of Accounts, approved by Order of the Ministry of Finance of Russia dated December 1, 2010 No. 157n (hereinafter referred to as Instruction No. 157n), transactions for the transfer and return of a tangible object of non-financial assets for free or paid use are reflected in the corresponding accounting accounts non-financial assets through the internal movement of an object while simultaneously reflecting on an off-balance sheet account the transferred or received object at its book value. The movement is reflected on the basis of the primary accounting document (act) (clause 33 of Instruction No. 157n). Let us recall that last year, changes were made to Instruction No. 162n by Order of the Ministry of Finance of Russia dated October 31, 2017 No. 172n (hereinafter referred to as Order No. 172n<*>). Order No. 172n brought Instruction No. 162n into line with the current edition of the more “general” Instruction No. 157n.

<*> Order No. 172n was registered with the Ministry of Justice of Russia on November 24, 2017 under No. 48998. A similar accounting entry (on the debit and credit of account 0 101хх 310), according to the new edition of paragraph 7 of Instruction No. 162n, reflects the transfer of property for rent, gratuitous use, trust management, storage. At the same time, information about fixed assets that are leased, gratuitously used, in trust management or in storage is reflected in the structure of the corresponding groups (types) of non-financial assets in the corresponding off-balance sheet accounts of the Working Chart of Accounts of the accounting entity. According to paragraphs 381, 383 of Instruction No. 157n, in order to control the movement and safety of transferred property, it is reflected on the balance sheet on account 25 “Property transferred for paid use (rent)” or account 26 “Property transferred for free use.” Let us also recall that by order of the Ministry of Finance of Russia dated December 31, 2016 No. 258n, the federal accounting standard for public sector organizations “Rent” (hereinafter referred to as Standard No. 258n) was approved, which came into force on January 1, 2021. The Ministry of Finance of Russia sent Guidelines on the transitional provisions of Standard No. 258n for the first application (letter dated December 13, 2017 No. 02-07-07/83463) and Guidelines on the application of Standard No. 258n for public sector organizations (letter dated December 13, 2017 No. 02- 07-07/83464).

We reflect the movement in accounting

It all depends on whether the divisions are allocated to a separate balance sheet or not.

The movement of fixed assets between departments is reflected using account 79 “On-farm settlements”, subaccount “Settlements for allocated property”.

| Contents of operation | Dt | CT |

| In accounting OP-1 | ||

| The initial cost of the fixed assets moved from OP-1 to OP-2 was written off | 79 “On-farm expenses”, sub-account “Calculations for allocated property” | 01 "Fixed assets" |

| The amount of accumulated depreciation written off | 02 “Depreciation of fixed assets” | 79, subaccount “Settlements for allocated property” |

| In accounting OP-2 | ||

| The initial cost of the OS obtained from OP-1 is reflected | 01 "Fixed assets" | 79, subaccount “Settlements for allocated property” |

| The amount of accumulated depreciation is reflected | 79, subaccount “Settlements for allocated property” | 02 “Depreciation of fixed assets” |

When moving, neither the initial cost of the OS nor its useful life changes. Therefore, depreciation on the received fixed assets from the receiving separate division continues to be accrued in the order that was established by the transferring party.

If your accounting program allows you to maintain analytical accounting on account 01 “Fixed Assets” for each OP, then the following entries are made in the accounting.

We invite you to familiarize yourself with: Collection of alimony in the amount of the subsistence minimum sample

| Contents of operation | Dt | CT |

| Reflects the movement of OS from OP-1 to OP-2 | 01 “Fixed assets”, subaccount “OP-2” | 01, subaccount “OP-1” |

| The amount of accumulated depreciation transferred | 02 “Depreciation of fixed assets”, subaccount “OP-1” | 02, subaccount “OP-2” |

If such analytics are not carried out, then no entries need to be made in accounting.

https://www.youtube.com/watch{q}v=ytadvertiseru

Costs arising from the dismantling of fixed assets, their transportation, installation and commissioning in a new location do not entail a change in the initial cost of the fixed assets either in accounting or tax accounting. After all, the initial cost of the fixed assets is subject to change in cases of completion, reconstruction, modernization, partial liquidation and for other similar reasons. 14 PBU 6/01; clause 2 art. 257 Tax Code of the Russian Federation.

In accounting, expenses arising when moving fixed assets are included in production costs (selling expenses), etc. 74 Guidelines, approved. By Order of the Ministry of Finance dated October 13, 2003 No. 91n; clause 7 PBU 10/99; Resolution 9 of the AAS dated July 22, 2009 No. 09-AP-12225/2009-AK; FAS UO dated November 10, 2010 No. F09-7088/10-S2 of the OP that carries them.

| Contents of operation | Dt | CT |

| Expenses for moving fixed assets from OP-1 to OP-2 | 20 “Main production”, 25 “General production expenses”, 26 “General business expenses”, 44 “Sales expenses” |

|

Input VAT on work performed by third parties is accepted for deduction on the date of completion of work on the basis of the invoice no. 1 item 2 art. 171, paragraph 1, art. 172 of the Tax Code of the Russian Federation.

For the purposes of calculating income tax paid to the budgets of the constituent entities of the Russian Federation, it is important to ensure that the movement of fixed assets among separate divisions is correctly reflected in tax accounting. After all, the calculation of the share of profit attributable to the operating enterprise is made on the basis of the residual value of the fixed asset according to tax accounting data.

We suggest you read: How to formulate an order to transfer an employee from a temporary position to a permanent one {q}