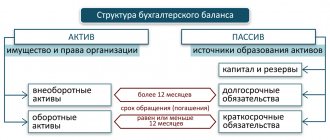

The balance sheet is a reporting form that systematizes and presents all information about the financial condition of the company as of a certain date. The balance is divided into two parts of equal value. On its left side - “Asset” - grouped data on the availability of property in the enterprise (real estate, financial investments, production assets and inventories, accounts receivable, cash, etc.) at the end of the reporting period, and on the right side - “Liabilities” are combined information about the sources of financing with which existing assets were acquired: capital (own and borrowed), as well as obligations to creditors. Both parts of the balance sheet must be equal, since the value of the property cannot exceed the available capabilities of the company, i.e., the size of its sources. Today, the balance sheet form approved by order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n is in force (as amended on April 19, 2019).

Balance sheet structure

Each part of the balance sheet groups assets and liabilities into sections. So, on the left side there are two sections - non-current and current assets, and the right side consists of three sections, separately combining capital and reserves, long-term as well as short-term liabilities.

In turn, the positions in each section are encoded with special four-digit codes established by Appendix No. 4 to Order No. 66n. Encryption of lines is necessary in reporting submitted to regulatory authorities - the legislator approved this procedure in order to systematize statistical data when generating information in general for an industry, region or country. A balance sheet compiled to review results within an enterprise may not contain codes - there is no need for them, but it is more convenient to generate a report and post accounting data, correlating them with the code number. Let's figure out how the current balance line codes are deciphered, what information is grouped in each of them, and how the indicators are formed.

Old and new balance: similarities and differences

In general, the new balance sheet is similar to the old one. In both cases, the document has 5 sections, each of which deciphers information about the assets and liabilities of the company. At the same time, the new balance sheet is more compact, since, unlike the old form, it does not require decoding:

- stocks;

- debts to debtors;

- reserve capital amounts.

In the new balance sheet, these indicators are reflected in the total amount without indicating breakdowns by subgroups and types of assets/liabilities.

If an organization needs to convert the old balance sheet to a new one, then it can use the table of correspondence between the lines of the new and old statements given in the order of the Ministry of Finance. The table will help you transfer data from the old balance sheet to the new format.

Explanation of balance sheet lines 2021 in section 1

In the current balance sheet form, the assets are allocated lines from 1100 to 1600. Let's start with deciphering the balance sheet lines of the 1st section “Non-current assets”, where it is accumulated, incl. information about the presence of assets with low liquidity in the company - fixed assets (fixed assets) and intangible assets (intangible assets). The lines of this section record their residual value, i.e. the difference between the original price and accrued depreciation.

| Balance sheet line | Decoding | How is the balance formed and from what accounts is it taken? | |

| Name | code | ||

| Intangible assets (IMA) | 1110 | The residual value of intangible assets (patents, licenses, software) is the difference between the debit balance of the account. 04 and the balance on the loan account. 05 | D/t 04 (not taking into account R&D) – K/t 05, or D/t 04, if the account is not applied. 05, and depreciation is taken into account on the account. 04 |

| Research and development results | 1120 | The company's expenses on completed and positive results, but not related to intangible assets, scientific developments (R&D) are taken into account in separate sub-accounts to the account. 04 | D/t 04 for R&D expenses |

| Intangible search assets (IPA) | 1130 | Costs for searching and evaluating mineral deposits - the right to conduct exploration, collecting information about the subsoil, the results of exploration drilling, the cost of assessing the feasibility of development. Accounted for as part of capital investments, indicated in the balance sheet minus accrued depreciation | D/t 08 – K/t 05 for related to search intangible assets |

| Material prospecting assets (MPAs) | 1140 | Material component of search and exploration costs | D/t 08- K/t 02 in terms of MPA |

| Fixed Assets (Fixed Assets) | 1150 | The residual value of fixed assets (buildings, equipment, tools, machines) is the debit balance of the account. 01, reduced by the amount of accrued depreciation on the fixed assets, i.e. on the credit balance of the account. 02. On line 1150 of the balance sheet, the explanation (example) could be as follows: if for an OS object with an initial cost of 100 thousand rubles. depreciation in the amount of 20 thousand rubles is accrued, then in the balance sheet its value will be 80 thousand rubles. (100 – 20) | D/t 01 – K/t 02 (except for wear and tear on fixed assets taken into account on account 03) |

| Profitable investments in material assets | 1160 | The residual value of assets, for example, equipment, listed on the account. 03 and intended for rental/rental | D/t 03 – K/t 02 in terms of depreciation accrued on the property recorded on the account. 03 |

| Financial investments | 1170 | Information about the company's investments to make a profit. Debit balance on long-term investment accounts: — loans to personnel (account 73/1), - for deposit accounts (account 55/3) and financial investment account 58. If a reserve was created for the depreciation of investments (account 59), then the balance in account. 58 is reduced by the credit balance on the account. 59 | D/t 55/3 + D/t 58 – K/t 59 (when creating a reserve) + D/t 73/1 for long-term interest-bearing loans |

| Deferred tax assets (DTA) | 1180 | Formed if tax accounting does not coincide with accounting, it reduces the amount of income tax. | D/t 09 |

| Other noncurrent assets | 1190 | Line 1190 of the balance sheet (decoding): indicates property the value of which is recognized as insignificant, for example, uninstalled equipment, capital investments or expenses that the company will incur outside the reporting period - account. 07, 08, 97 (regarding a one-time payment for the right to use an intellectual resource) | D/t 07 + D/t 08 (except for those related to exploration assets) + D/t 97 (for expenses with a write-off period of more than a year) |

| Total for Section I | 1100 | Total line by section | Sum of filled section lines |

Results

To reflect fixed assets in the balance sheet, a specific line (1150) is allocated in the section devoted to non-current assets. This property includes objects of a certain value (above 40,000 rubles) and service life (over 1 year). On the balance sheet, this cost is shown reduced by the amount of depreciation. Situations of changes in value associated with additional equipment (reconstruction, partial write-off) and revaluation are disclosed in the appendices to the balance sheet.

- Purpose of the article: Displaying information about available land plots, residual value of machinery and equipment, buildings, etc.

- Line number in the balance sheet: 1150.

- Account number according to the chart of accounts: Debit balance - credit balance.

Note from the author!

Line 1150 can display information about the debit balance of the account for subaccounts 01-04 (in terms of fixed assets) and the debit balance of the account. The company makes the decision to include data independently (if the data is unimportant, the balances can be displayed on line 1190).

Fixed assets are understood as assets of an organization intended for long-term use for the purposes of the company.

According to the accounting rules, in order to accept acquired assets on the balance sheet as fixed assets, certain conditions must be simultaneously met:

- Asset purpose:

production of company products, performance of work, services;use for management needs;

leasing - transfer of an asset for temporary use and possession to third parties or temporary use.

- The useful life of the object is more than 12 months or during the operating cycle (when the cycle is more than a year).

- When purchasing an asset, the company does not have the goal of further resale of the object.

- The use of an asset affects the company's income: the asset's ability generates economic benefits for the firm with continued use.

Fixed assets are expensive objects used by the company for a long time:

- buildings, structures;

- production equipment (for example, machines);

- control devices and computer technology;

- transport;

- expensive household equipment;

- livestock;

- perennial plantings;

- natural resources: land, water, etc.

Line 1150 - balance sheet asset: this displays the residual value of non-current assets - fixed assets (original cost minus accrued depreciation) as of December 31 of the financial year. For non-depreciable property, the original cost of the item is displayed.

The final figure in accounting should be reflected as the final debit balance of account 01 minus the credit balance of account 02.

The reporting displays information as of the current period, December 31 of the previous year, and December 31 of the year preceding the previous one.

Explanation of the balance sheet according to the lines of section 2

In the 2nd section of the balance sheet there are lines reflecting the value of the most liquid assets available in the company at the reporting date - working capital:

| Balance sheet line | Decoding | How is the balance formed and from what accounts is it taken? | |

| Name | code | ||

| Reserves | 1210 | Explanation of line 1210 “Inventories” in the balance sheet includes:

| D/t 10 + D/t 15 + D/t 16 (or – K/t 16) + D/t 20 + D/t 21 + D/t 23 + D/t 28 + D/t 29 + D/ t 41+ D/t 43 – K/t 42– K/t 14 + D/t 44 + D/t 45 |

| VAT on purchased assets | 1220 | Debit balance of the account. 19 “VAT on purchased MC” | D/t 19 |

| Accounts receivable | 1230 | Combine debit balances on settlement accounts with suppliers, customers, employees - 60, 62, 70, 71, 73 (excluding long-term interest-bearing loans on account 73/1), 75, 68, 69.76 (VAT on advances reflected on these are not taken into account). The credit balance of the account is subtracted from the resulting value. 63 “Reserves for doubtful debts”, if a reserve was created | D/t 60 + D/t 62 – D/t 63 + D/t 68 + D/t 69 + D/t 70 + D/t 71 + D/t 73 (except for loans on account 73-1) + D/t 75 + D/t 76 (minus VAT on advances issued and received) |

| Financial investments (except cash equivalents) | 1240 | Investments in short-term periods (less than a year) to make a profit. Sum up the debit balances on accounts 55/3 and 58 (minus the credit balance of the reserve for impairment of short-term investments on account 59), 73 | D/t 58 – K/t 59 + D/t 55/3 + D/t 73-1 (for short-term transactions) |

| Cash and cash equivalents | 1250 | They generate information about the balances of funds in bank accounts and the cash desk of the company, for which they sum up the debit balances on accounts 50 (except for the subaccount for monetary documents 50/3), 51, 52, 55, 57, 58 (in terms of cash equivalents - securities , shares, etc.) | D/t 50 (except 50/3) + D/t 51 + D/t 52 + D/t 55 (except 55/3) + D/t 57 + D/t 58 (for investments in securities) |

| Other current assets | 1260 | The value of assets not included in the listed lines, for example, the debit balance of an account. 50/3 (when taking into account monetary documents), the amount of shortages and losses in the account. 94 | D/t 50/3 + D/t 94 |

| Total for Section II | 1200 | Total line by section | Sum of filled section lines |

| BALANCE | 1600 | Total for balance sheet assets | Sum of lines 1100 and 1200 |

Section IV. long term duties

Borrowed funds.

Line 1410 is reserved for the debt of the organization itself on long-term (with a repayment period of more than 12 months as of December 31, 2015) loans and credits.

Deferred tax liabilities.

Line 1420 is filled in by income tax payers. “Simplers” are not included in their number, so they put a dash in this line.

Estimated liabilities.

The specified line 1430 is filled in if the organization recognizes estimated liabilities in accounting in accordance with the Accounting Regulations “Estimated Liabilities, Contingent Liabilities and Contingent Assets” (PBU 8/2010), approved by Order of the Ministry of Finance of Russia dated December 13, 2010 N 167n. Let us remind you that small businesses, which are the majority of “simplified” ones, may not apply this PBU.

Other obligations.

Here (line 1450) others are shown that are not reflected in other lines of section. IV balance. Please note that Order No. 66n does not provide an indicator for line 1440.

Balance lines 2021: decoding of the 3rd section

The third section of the liabilities side of the balance sheet contains information about the presence of equity capital and reserves in the company. The balance breakdown will be as follows:

| Balance sheet line | Decoding | How is the balance formed and from what accounts is it taken? | |

| Name | code | ||

| UK | 1310 | Amount of authorized capital | K/t 80 |

| Own shares purchased from shareholders | 1320 | This is a negative indicator on the balance sheet (indicated in parentheses), indicating the balance of the company's shares, which it bought back from participants for intended resale or cancellation | D/t 81 |

| Revaluation of non-current assets | 1340 | The amount of additional valuation of fixed assets and intangible assets resulting from revaluation (revision of the initial value of property), recorded in the account. 83 | K/t 83 (in terms of additional valuation of fixed assets and intangible assets) |

| Additional capital (without revaluation) | 1350 | The amount of additional capital without taking into account the revaluation carried out, for example, upon receipt of property - the credit balance on the account. 83 | K/t 83 (except for revaluation amounts) |

| Reserve capital | 1360 | The amount of the formed reserve fund or other funds formed by distribution from the company’s profits is the credit balance of the account. 82 | K/t 82 |

| Retained earnings/uncovered loss | 1370 | Balance sheet line 1370 - decoding reflects the result of the enterprise's activities: the amount of profit remaining in the company after taxes or the amount of loss. A credit balance means the presence of retained earnings, a debit balance means a loss. | One way:

|

| Total for Section III | 1300 | Total line by section | Sum of section row indicators |

Cost of fixed assets

The initial cost of assets is the total cost of all costs incurred to acquire an object or bring it into operation. The cost of objects depends on the methods of obtaining:

- purchasing finished equipment from a supplier using company funds;

- contribution to the authorized capital of the company;

- free of charge (the initial cost is based on market prices);

- creation of the facility by the enterprise itself (in addition, the consumption of materials and wages of employees will be taken into account).

A change in the initial value is possible in cases of revaluation of assets, additional equipment, reconstruction, measures to modernize assets and partial liquidation.

According to PBU, companies have the right to revalue fixed assets at the end of the reporting period (price indexation or calculation of replacement price based on market prices).

Explanation of the balance sheet according to the lines of section 4

This section of the balance sheet reflects the status of settlements on short-term loans, the amount of deferred tax liabilities, estimated and other liabilities:

| Balance sheet line | Decoding | How is the balance formed and from what accounts is it taken? | |

| Name | code | ||

| Borrowed funds | 1410 | Balance of outstanding long-term loan taken out for a period of more than 12 months | K/t 67 |

| Deferred tax liabilities (DTL) | 1420 | Formed if tax accounting in a company differs from accounting - the differences are formed according to the account. 77, the balance of outstanding obligations is the credit balance on the account. 77 | K/t 77 |

| Estimated liabilities | 1430 | The amount of reserves for upcoming expenses planned in the long term, for example, for reconstruction - the credit balance on the account. 96 | K/t 96 in terms of reserves formed for events that will occur no earlier than in a year |

| Other obligations | 1450 | Reflect borrowed (not own!) funds that are not indicated in line 1410. This may be long-term debt to a counterparty or the budget, incl. on bills of exchange, target receipts with a long-term perspective of coverage | K/t 60 + K/t 62 + K/t 68 + K/t 69 + K/t 76 + K/t 86 (for long-term debt) |

| Total for Section IV | 1400 | Total line | Sum of partition rows |

Lines 1510 (610), 1520 (620), 1530, 1540, 1550 and 1500 with decryption

In the previous edition of the form, line 1510

of the balance sheet with a breakdown

was

line 610 of the balance sheet.

It contains information about short-term borrowed funds (accounts 66 and 67).

Line 1520

of the balance sheet with a breakdown

until 2015 was line 620. It reflects short-term debt to partners, staff, etc. Line 1530 contains account balance 98.

Line 1540 is liabilities reflected on the credit of account 96, the maturity of which is less than 12 months.

Line 1550 is all other obligations that are not reflected in the previous lines.

Line 1500 contains the final result for section 4.

Requirements for filling out a simplified balance sheet

The annual balance sheet must contain data on the assets and liabilities that the organization has at the end of the reporting year, that is, as of December 31. Additionally, information on previous years is entered into the balance sheet, that is, as of December 31 of last year and as of December 31 of the year before. For example, the balance sheet prepared by an enterprise for 2021 must contain data as of December 31, 2017, December 31, 2021 and December 31, 2015.

All last year's information is taken from last year's reports. And for indicators for the current year, information is taken from sources such as:

- The balance sheet for the organization as a whole for the reporting year;

- Indicators of accrued interest on credits (loans) for the reporting year.

If there is no data to fill out any balance line, it is not filled in and a dash is placed.

What data does line 1150 contain?

In the special approved form used to fill out reporting, the line under the specified number is designated as “Fixed assets”. Judging by the name, it can be determined that this column will directly display the size of fixed assets that the organization has at the time of reporting. However, there are some nuances that also need to be taken into account when filling out this column and drawing up documentation.

This column does not indicate all existing fixed assets at the disposal of the organization, but only those that are reflected in the corresponding account. If the funds, by their intended purpose, belong to the category provided for temporary possession in order to increase income, then this will be the account “Income-generating investments in material assets,” which belongs to a different line.

In addition, it is necessary to take into account that the funds in this line are necessarily reflected in the net assessment. If we are talking about fixed assets when filling out documentation, then they are indicated in the residual value.

To complete the reporting, from the debit balance relating to the fixed assets account, subtract the credit balance from the depreciation account of fixed assets falling on the same date in the reporting period under review. Only depreciation that relates to fixed assets in the relevant account is deducted. It is necessary to exclude depreciation, which is accrued from profitable investments in material assets, since it does not relate to fixed assets, but goes to the same account.

When preparing reports, you must comply with the requirements for the established form and use it to complete the documentation.

This will avoid errors and provide the correct report. Each digital code has a decoding that can be clarified to avoid inaccuracies when filling out. Also, when preparing reports, you can use samples that are freely available. As for accounting accounts, to fill out line 1150 you need to subtract from the debit balance of account 01 the credit balance of account 02 “Depreciation of fixed assets” for the same reporting date. Naturally, depreciation needs to be deducted only that which relates to fixed assets accounted for in account 01. After all, for profitable investments in material assets accounted for in account 03, depreciation is also accrued for account 02. And since the debit balance of account 03 is not included in line 1150 , then the depreciation related to them should also be excluded from the balance of account 02.

general information

Let's start with terminology. Tangible non-current assets are the property of an enterprise that is used repeatedly and during this process transfers its property to products in parts. In practice, this includes everything that has been used for more than one year and its value exceeds fifteen non-taxable minimum income of the enterprise.

More specifically, tangible non-current assets are:

- equipment and machinery;

- fixed assets;

- unfinished capital investments (investments);

- other tangible non-current assets.

This is not a complete list due to the large number of possible physical manifestations. In operating activities, tangible non-current assets have a number of advantages and disadvantages. Let's look at them in more detail.

Profitable and financial investments (part 1)

Property that is rented or leased is also reflected in the balance sheet at its residual value on line 1160. Financial investments mean deposits in capital assets purchased by the Central Bank of other organizations. Line 1170 reflects the initial cost of long-term investments (circulation period more than 12 months). Information is entered from the debit balance of the account. 58, count. 55, count. 73. If an organization creates reserves for a decrease in the value of such assets, then they should also be accounted for on line 1170.

Financial investments also include issued interest-free loans. Their amount is reflected not in line 1170, but as part of accounts receivable (1190). The cost of shares purchased from the founders should also be reflected not in investments, but in liabilities (p. 1320).