When goods are transferred from one owner to another, appropriate documentation must be drawn up. Accompanying papers are used everywhere. They are used for purchase and transportation, and also confirm the fact of transfer of cargo from the seller to the buyer. Therefore, everyone who carries out business activities needs to know what a consignment note looks like, what it is and the rules for registering TORG-12 according to the law.

What is

A representative of the buying party is required to sign the TN when the delivery service (courier or from the selling company) delivers new items. Under any circumstances, be it a parcel to a private person from another city or a batch of frozen dumplings delivered to a grocery store. So, if an entrepreneur orders a certain quantity, the corresponding document is sent to him along with it. At the time of signing, the buyer confirms by his action that he has received the declared cargo and has no claims against the supplier.

In addition, accompanying documentation of this type is necessary to confirm expenses with the tax office if the retail outlet operates under the basic or simplified taxation system.

By law, the activities of any organization related to production, storage and resale must be documented, carried out through primary accounting documents, which are formed and approved by the company’s management.

When trying to find out how to draw up an invoice for goods and the rules for registering TORG-12 on the part of the seller, it is worth remembering that back in the late 90s, Rosstat published resolution number 132. It contains a complete catalog of accounting papers, including the form we are considering, otherwise called as OKUD 0330212. The scope of this TN is limited to the transfer of inventory from the selling party to the buying party. Such documentation may be compiled and stored not only in printed form, but also in a similar electronic format.

With the help of this document, wholesale deliveries to customers are documented. To create it, it is necessary to use a standard form or develop an alternative version that fully complies with the requirements. You should fill out your independently created TN in compliance with all the rules provided for by law.

How to sign an invoice

The completed TORG-12 must be signed by all authorized persons on the part of the supplier and the customer.

There are situations when the buyer’s representative independently picks up the cargo by proxy. In such cases, in the “Cargo accepted” column, information about the person who picks up the products and the details of the basis - the power of attorney - are entered. The column “Cargo received” is signed by the employee responsible for placing the products in the warehouse.

If the delivery note is drawn up and sent to the customer electronically, then both parties must sign it with a digital signature. Electronic TORG-12 is generated in one copy, but the document contains two files. One is created from the buyer's side, the other from the supplier's side.

The electronic invoice can be sent to the territorial Federal Tax Service in XML format via telecommunication channels. This document is signed by the manager, chief accountant and other responsible persons.

Five signatures are placed under the invoice, which is drawn up in paper form:

- In the column “Cargo received” the authorized person of the customer puts his signature. The right to sign is enshrined in the organization’s charter or is formalized by a special order or power of attorney.

- The section “Cargo accepted” is signed by the financially responsible person of the customer. This line can also be signed by the employee who directly accepts the goods. If the party is accepted by the director, then the power of attorney is not issued. Any other employee can act only on the basis of a power of attorney.

- Three signatures are placed on the supplier’s side: the manager, the accountant and the employee responsible for the shipment of inventory items. You can issue an order that will secure the right of a specific employee to sign from the supplier in all three sections.

Stamps are affixed by both parties only if they are used in institutions.

A seal is not a mandatory requisite in the documentation, but it is better to put it in TORG-12, since the form itself provides space for a seal imprint. When checking, the Federal Tax Service may find fault with the procedure for filling out the document if it is missing.

If the customer’s representative received the products under the manager’s power of attorney, which was certified by a seal, you can attach the power of attorney form to the delivery note as accompanying documentation and store these registers together. This will be enough for the inspection inspector.

What does the invoice for goods TORG-12 look like: procedure for registration, decoding of the abbreviation

Looking at the self-explanatory name, it is easy to understand that the capital letters are an abbreviated version of the word “trade”. The catalog of various types of primary accounting papers for control of trading operations displays all available forms intended for generating documentary evidence. Today, other samples from TORG-1 to TORG-31 are considered optional. However, many accounting departments still use them.

Document type

The TN we are considering acts as confirmation of the transfer/sale of products by a third-party company. Therefore, it belongs to the category of external documentation.

When collecting information on how to issue a TORG-12 consignment note and find out the required details to fill out, it is important to remember a number of nuances. Although this form is a universal option that meets the requirements of legislation in this area in all respects, it is still not uniform. Entrepreneurs have the right to use other versions. Thus, according to the law, it is allowed to develop and compose technical specifications independently.

When drawing up a document, it is necessary to take into account all the mandatory points that must be displayed on paper. Many people have difficulty with this. As a result, misunderstandings often arise when interacting with representatives of inspection authorities. That is why the vast majority of companies still prefer the twelfth form.

Application

An invoice is issued when transferring ownership of commodity items and other goods and materials through sale or release from the selling party to the buying party. The company has the right to use not only the sample established in accordance with the law, but also to create its own version.

Upon receipt of goods

In this case, the technical specification is formed by the organization performing the shipment. As a result, registration is required from the supplier company. This can be done in one of the most preferred options: written or electronic. Often the format of the documentation is determined by mutual agreement between the buyer and seller.

Anyone who buys products has the right to refuse to accept them without appropriate documentary support. Moreover, if during the transfer procedure inconsistencies in the transferred items in terms of quality indicators are discovered, and a representative of the receiving party wants to make a return, he will need to draw up a document for the returned values.

When figuring out what this form TORG-12 is in accounting and what are the requirements for the consignment note, you should remember that along with it, an act of discrepancy in quality and quantity of products is drawn up in the form of TORG-2. At the same time, it is necessary to discuss the nuances of the return transfer of goods and be sure to record the oral agreement in writing. Otherwise, low-quality products simply cannot be returned.

For implementation

Sale (providing ownership rights to cargo from one person to another on a reimbursable basis) is also accompanied by relevant papers. The TN we are considering presupposes the availability of information about the movement of inventory items from the warehouse and settlements with the purchasing party.

Such documents are generated by the selling company. They indicate the details of the organization. The buyer accepts the delivered products and pays at the time of shipment.

In the “Payer” and “Consignee” paragraphs, the following data should be entered equally:

- Company name;

- its location (address data);

- Bank details.

For shipment

Often, commodity items and other material assets are transferred to one point, and the procedure is paid for from another. In this situation, the TN must indicate information not only about the recipient of the cargo, but also about the payer (separately). In the established form there are special columns for this.

The organization making the payment is the buyer. The goods can be accepted by a third party (for example, a subsidiary) enterprise, representative office or branch. This type of operation in TORG-12 implies a mandatory indication in the sales agreement to whom exactly the products will be sent and who will act as the consignee.

To supply

When goods and materials are supplied through the involvement of a third company, the selling party must, in addition to the twelfth invoice, also issue a goods and transport invoice. The TTN is drawn up according to the standards of the unified sample 1-T.

This paper is always prepared in 3 copies, intended for the supplier, the carrier company and the buyer. It should be noted that the formation of this documentation is required for each batch of goods that is transported using one vehicle (not for the entire volume of delivery, transported in several trips).

Packing list

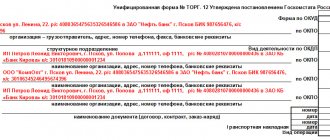

These include shortcomings that do not prevent tax authorities from identifying the seller, buyer, name of goods, work or services and their cost during the audit (Letter dated 02/04/2015 N 03-03-10/4547). The Federal Tax Service of Russia supported this approach (Letter dated 02/12/2015 N ГД-4-3/ [email protected] ). This means that the most dangerous errors are in the following details of the consignment note (the names of the details are given in accordance with the unified form N TORG-12, approved by Resolution of the State Statistics Committee of Russia dated December 25, 1998 N 132): - supplier, his address, telephone, fax, bank details; — payer, his address, telephone, fax, bank details; — name, characteristics, grade, article number of the product (column 2 of the tabular part); — amount including VAT (column 15 of the tabular section). The absence of bank details of the supplier or buyer in the invoice does not refute the fact of purchase of the goods. The capital's tax authorities confirmed that this deficiency does not affect the recognition of expenses and the deduction of VAT (Letter of the Federal Tax Service of Russia for Moscow dated April 26, 2010 N 16-15/43834). If an organization uses an independently developed form of a consignment note, it is important that it contains all the details required for the “primary” (Clause 2, Article 9 of the Federal Law of December 6, 2011 N 402-FZ “On Accounting”, hereinafter referred to as the Law on accounting): - name and date of preparation of the document; — name of the organization or full name. the entrepreneur on whose behalf the document was drawn up; - content of the fact of economic life; - unit of measurement; — job title, surname, initials and signatures of the persons responsible for processing the transaction (read more in the box below).

Note! It is risky to endorse an invoice with a facsimile signature. Tax officials say that primary documents cannot be signed using a facsimile. After all, they must bear the personal signature of the responsible person (Letters of the Federal Tax Service of Russia dated September 23, 2008 N 3-1-11 / [email protected] and the Federal Tax Service of Russia for Moscow dated January 25, 2008 N 20-12/05968). But the legislation has changed. The requirement to affix a personal signature was specified in the Federal Law of November 21, 1996 N 129-FZ “On Accounting”. This document has lost force since January 1, 2013. Now the list of mandatory details of the “primary registration” simply mentions a signature (clause 7, clause 2, article 9 of the Accounting Law). Despite this, judicial practice remains ambiguous. Many courts are still against signing the “primary document” with facsimile signatures. In their opinion, documents certified by facsimile are invalid. That is, with the help of such papers it is impossible to confirm any facts of economic activity. Including the fact of purchase of goods (Resolutions of the Far Eastern Federal Antimonopoly Service dated April 2, 2014 N F03-1016/2014, Volga District dated April 1, 2014 N A57-4665/2013 and Central District dated March 28, 2013 N A68-2818/12). Of course, the organization has the right to refer to changes in accounting legislation. But this does not guarantee her victory in the argument. Therefore, it is safer not to endorse invoices and other “primary documents” with facsimile signatures. Even if this option for signing documents is provided for in the agreement with the counterparty (clause 2 of Article 160 of the Civil Code of the Russian Federation).

Failure to complete or absence of other details in the invoice is not so important. For example, the company itself decides whether or not to fill out the line “Shipping organization, address, telephone, fax, bank details.” Tax officials consider this detail of the delivery note to be optional (Letter of the Federal Tax Service of Russia dated November 25, 2014 N ED-4-15/ [email protected] ). This means that errors in it should not lead to refusal to account for expenses and deduct “input” VAT.

Note. The absence of secondary details in the invoice does not refute the fact of purchase of the goods.

If there is other evidence that the transaction is fictitious, errors in the invoice will only confirm suspicions

The courts believe that the presence of errors in the delivery note does not refute the delivery of goods and their acceptance for accounting. Defects only indicate a violation of accounting rules. This means that the tax authorities’ reference only to these defects cannot be the basis for excluding the buyer’s expenses and refusing to deduct VAT (Resolutions of the Moscow Federal Antimonopoly Service dated February 26, 2014 N F05-576/2014, West Siberian Federal Antimonopoly Service dated March 1, 2012 N A75-1969/2011 , Ural dated June 30, 2011 N F09-3562/11, East Siberian dated December 20, 2007 N A19-7415/07-33-F02-9351/07 and dated December 14, 2007 N A19-8418/07-57-F02- 9192/07 districts). But if there is other evidence of the unreality of the transaction, the court can support the inspectors (Resolutions of the Federal Antimonopoly Service of the North Caucasus dated September 20, 2013 N A53-24630/2012, the Ural Federal Antimonopoly Service dated February 17, 2012 N F09-99/12 and the West Siberian Federal Antimonopoly Service dated November 6, 2009 N A27- 1367/2009 districts).

What claims regarding the registration of delivery notes do organizations successfully challenge in the courts?

The date of shipment or acceptance of the goods is not indicated

According to tax authorities, the absence of this information in the invoice is evidence that the buyer did not receive the goods. This means that he does not have the right to include the cost of goods in tax expenses and deduct “input” VAT (paragraph 2, paragraph 1, article 172 and paragraph 4, paragraph 1, article 252 of the Tax Code of the Russian Federation). But the date of shipment of the goods by the supplier and the date of its receipt by the buyer are not mandatory details. These include only the date of preparation of the invoice itself (clause 2, clause 2, article 9 of the Accounting Law). Therefore, the courts believe that the absence of delivery and acceptance dates of goods in invoices does not prevent the accounting of expenses and the deduction of VAT (Determination of the Supreme Arbitration Court of the Russian Federation dated December 17, 2009 N VAS-16581/09, Resolution of the Arbitration Court of the North-Western District dated May 22, 2015 N F07-2297 /2015, FAS Moscow District dated 08/12/2011 N KA-A40/8591-11 and dated 03/12/2010 N KA-A41/1727-10).

There are no details of the power of attorney of the person who signed the invoice

This defect also does not refute the fact of delivery and receipt of goods. Especially if the other details of the delivery note are filled out flawlessly. The main thing is that the person who signed the invoice has the authority to do so. Therefore, a copy of the power of attorney must be attached to the invoice. This will help deny claims. Moreover, the parties to the transaction have the right to make corrections to the invoice (Clause 7, Article 9 of the Accounting Law). That is, enter the details of the power of attorney into it. Since the invoice is prepared by the seller, he must make changes to it. Corrections must be certified by the signatures of those persons who prepared the invoice, and their surnames and initials must be indicated. You also need to put a date for making changes. Most courts allow the buyer to take into account expenses and accept VAT for deduction, even if the invoice does not contain a reference to the details of the power of attorney (Resolution of the Arbitration Court of the West Siberian dated 09.18.2014 N A03-24469/2013, FAS West Siberian dated 01.03.2012 N A75- 1969/2011, Moscow dated 02/29/2012 N A40-127306/10-90-714 and Volga region dated 05/22/2007 N A12-16921/06 districts). The arbitrators consider this defect to be minor. But only in the absence of other signs that the transaction is fictitious.

The position or signature of the person who signed the invoice

Both of these details of the consignment note are mandatory (clauses 6 and 7, clause 2, article 9 of the Accounting Law). This is what tax authorities usually refer to when deducting expenses and refusing to deduct VAT. But the courts reason differently. In their opinion, the absence of a position name and a transcript of the signature in the invoice is a minor drawback. It indicates, first of all, a violation of accounting rules. Moreover, this violation was committed by the seller. The buyer should not be responsible for the mistakes of counterparties (Definition of the Constitutional Court of the Russian Federation of October 16, 2003 N 329-O). If the facts of shipment and acceptance of goods are confirmed, the buyer has the right to take into account their value in tax accounting and accept “input” VAT for deduction even in the absence of a decryption of the signature (Resolutions of the Federal Antimonopoly Service of Povolzhsky dated May 22, 2012 N A55-5626/2010 and dated May 22, 2007 N A12 -16921/06, East Siberian from 09/22/2011 N A58-6676/2010 and Moscow from 09/14/2011 N A40-123143/10-116-503 districts). In addition to invoices, the fact of receipt of goods can be confirmed by contracts, waybills, reconciliation reports with suppliers, warehouse accounting documents, printouts of accounting account cards indicating the posting of goods and materials (for example, accounts 10 or 41). Another argument is that the absence of a transcript of the signature of the person who signed the delivery note does not prevent the identification of the supplier, buyer, name of the product, its quantity and date of release. This means that this deficiency does not lead to negative tax consequences. This is noted by some courts (Resolutions of the Federal Antimonopoly Service of the Central District dated 05/31/2011 N A35-9286/2010 and the Northwestern District dated 05/04/2011 N A13-7011/2010).

Note. Courts consider many shortcomings in the preparation of invoices to be insignificant.

The Russian Ministry of Finance agrees that shortcomings in the “primary”, which do not create obstacles to identifying the essential aspects of the transaction, do not entail a refusal to account for expenses (Letter dated 02/04/2015 N 03-03-10/4547). It is advisable to refer to this when disagreements arise.

There is no link to the waybill

If goods are delivered to the buyer by a third-party carrier, the supplier indicates the details of the bill of lading - its number and date - in the delivery note. Tax authorities consider the absence of this information to be a serious violation. In their opinion, this casts doubt on the reality of transporting goods. Therefore, inspectors refuse to allow the buyer to account for expenses and deduct “input” VAT. The courts note that a reference to the waybill is not a mandatory detail of the invoice. Even without this link, you can reliably establish who received what product, when and what. Lack of information about the waybill does not prevent the goods from being posted. After all, the organization accepts goods for accounting on the basis of the consignment note. There is enough data in it for this. Therefore, the courts do not see any obstacles to recognizing expenses and deducting VAT on goods, the shipment of which was registered with such a minor defect (Resolutions of the Federal Antimonopoly Service of the North-West of September 26, 2013 N A13-9242/2012 and of November 8, 2011 N A13-12880/2010, Central dated December 22, 2010 N A68-11668/09, East Siberian district dated June 24, 2008 NN A19-15326/07-57-F02-2709/08 and A19-15325/07-24-F02-2707/08 districts).

The gross weight of the cargo is not indicated

In the delivery note, in addition to the quantity of goods, there is a column to indicate the gross weight. That is, the weight of the goods together with containers and packaging (column 9 of the tabular part). Failure to fill out this detail, together with other shortcomings, is recognized by tax authorities as a violation, which entails a refusal to deduct VAT and account for expenses. Many organizations simply do not need information about gross weight. Especially if they accept goods for accounting individually. The courts take this circumstance into account and reject the claims of the inspectors (Resolutions of the FAS North Caucasus dated October 26, 2009 N A53-27009/2008-C5-34, Moscow dated August 21, 2008 N KA-A40/7847-08, East Siberian dated March 18, 2008 N A33-6296/07-F02-967/08 and dated 03/06/2008 N A19-11334/07-51-F02-737/08 districts). Even if the goods are by weight, the absence of data on the gross weight in the invoice does not refute the fact of purchase of the goods. This information is not required to be filled out. Therefore, the courts allow buyers to recognize the costs of purchasing weighted goods and accept the “input” VAT on them for deduction (Resolutions of the FAS Povolzhsky dated 05.05.2011 N A49-5601/2010, Uralsky dated 04.28.2011 N F09-1468/11-C2, Moscow dated 02/16/2009 N KA-A40/374-09 and West Siberian district dated 09/11/2007 N F04-6170/2007(37886-A03-29) districts).

If you do not find the information you need on this page, try using the site search:

What kind of document is this - unified form TORG 12: design requirements

When trading, it is not at all necessary to adhere to the established type of composition. Entrepreneurs and commercial organizations have the right to update approved forms while complying with mandatory requirements. Thus, you can create a technical specification that fully corresponds to your own preferences and business characteristics. This can be done in one of two available ways:

- by making additions to the unified sample (enter additional details necessary to more fully reflect the economic activities of the enterprise);

- create a completely new, previously unused option.

The main thing is that after introducing modifications to the structure, it contains all the main components recognized as mandatory for reflection in documentary form. So, the invoice must indicate:

- the name of the documentation itself;

- day of compilation;

- name of the supplier company or personal data of the entrepreneur;

- list of goods being moved;

- number of cargo positions (in monetary and physical terms);

- job descriptions of persons responsible for the acceptance and delivery of inventory items;

- personal signatures of participants.

All of the above points must be present. This should be remembered when dealing with the topic: “what kind of document is a consignment note: definition, design requirements, example of filling out.”

Compliance with the mandatory conditions for the formation of technical specifications allows us to confirm the fact of shipment on a legal basis. And also record the corresponding meters (quantity, weight, cost). Thanks to the TORG-12 form, it is possible to reflect the write-off of products from the selling party and the capitalization of them to the buying party. To have a clear idea of the wiring, you should consider the attached table:

| Debit | Credit | Operation | ||

| Code | Name | Code | Name | |

| Selling side | ||||

| 62 | Carrying out settlements with customers | 90-1 | Sale Revenue | Sales of goods and materials |

| Buying party | ||||

| 10 | Materials | 60 | Payment for the work of supplier companies | Reception of goods transferred by the supplier company |

| 41 | Products | Capitalization of purchased items | ||

| Transport organization | ||||

| 002 | Stored inventory items | Receipt | ||

| 002 | Goods received for storage | Broadcast | ||

Filling Features

The formation of technical specifications is carried out by employees of the accounting department, warehouse or other company employees vested with such powers. There is no single standard according to which such documentation would be required. You can stick to the existing general template or create your own version. The number of rows and tables is not regulated; if necessary, it will be easy to reduce or, conversely, increase.

While observing the correct execution of documents according to the TORG-12 consignment note, it is worth remembering that it must contain the following information:

- name of the selling company;

- information about the buyer;

- description of the product indicating weight, number and cost.

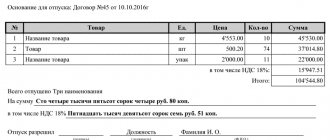

The TN can be drawn up on one sheet or on several at once (depending on the list of components of the transferred cargo). In the second case, the title indicates exactly how many pages are available.

The paper must be drawn up in 2 copies. One of them is taken directly by the seller, the other is sent to the buyer. If necessary, it is allowed to attach additions, information about which is also recorded in the form itself.

An example should be examined in detail in the attached image:

Is it necessary to register?

The answer to this question can be unequivocally “Yes”. A consignment note is a mandatory accounting document .

Registration of a delivery note is necessary when selling or accepting any goods.

Moreover, the invoice must be drawn up in two copies, this applies to both vertical and horizontal formats of invoices.

Why is it needed?

According to the law of the Russian Federation “On Bukh. accounting" No. 402-FZ, in order for the receipt and sale of goods to be considered legal, an appropriate invoice must be drawn up.

One copy of the invoice must be given to the supplier of the goods to document the write-off. The second copy is kept by the counterparty, which is the enterprise to which the goods are supplied, or an individual entrepreneur who also receives the goods.

The consignee's responsible person certifies the fact of receipt of the goods . The absence of this document and the accompanying acts when trading between individual entrepreneurs or organizations makes the operation illegal.

You will find more information about why a technical document is needed and whether it can replace a sales receipt in our material, and here we talked about the difference between a delivery note and an invoice.

Rules for issuing the TORG-12 consignment note upon receipt of goods: instructions for filling out

The employee authorized to draw up the relevant documentation first of all begins to indicate the parties entering into the transaction. In the column for the sender of the goods, the name of the sending company is indicated, followed by the necessary details. The recipient line is intended for entering similar information about the buyer. The “Supplier” position implies duplication of data from the “Consignor”. Information about the consignee is copied into the “Payer” column.

Next, I date the document and assign it a number in accordance with the general document flow of the enterprise. Only after this do they begin to compile a table in which they enter:

- an accurate list of products being moved;

- indicate units of measurement (pieces, kg, l, etc.);

- quantitative indicators;

- prices;

- total delivery cost.

Under the table display it is written how many pages the TN has. In a certain column, enter the cost value in capital form. Finally, the paper goes for signature:

- to the employee who is engaged in the release of cargo;

- chief accountant;

- responsible for acceptance.

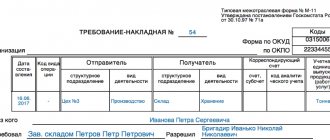

Rules for filling out the bill of lading 2021

In 2021, the bill of lading form is filled out in accordance with the updated Rules for the carriage of goods:

- The shipper must fill out paragraphs 1-6 and 16 in the document (“Consignor”, “Consignee”, “Name of the cargo”, “Accompanying documents for the cargo”, “Instructions of the shipper”, “Acceptance of the cargo”, “Date of compilation, signatures of the parties”) .

- The carrier must determine (in agreement with the sender) the conditions of transportation. He fills out (in his part) paragraphs 8-11, 13, 15, 16 of the TN (“Conditions of transportation”, “Information on acceptance of the order for execution”, “Carrier”, “Vehicle”, “Other conditions”, “Cost of services” carrier and the procedure for calculating freight charges”, “Date of preparation, signatures of the parties”).

- The driver signs the waybill in paragraphs 6 and 7 (“Acceptance of cargo”, “Deliverance of cargo”), fills out paragraph 15 (“Cost of carrier services and the procedure for calculating the freight charge” - the amount of the freight charge is indicated here), if necessary - paragraph 12 (“ Reservations and comments of the carrier" - here are comments about the actual condition of the cargo, containers, packaging, marking, sealing - when delivering the cargo, changes in transportation conditions - when unloading). On the way, the driver, as necessary, has the right to make notes about changes in transportation conditions (clause 12) and redirection (clause 14 “Readdressing”).

- The consignee fills out clause 7 (“Deliverance of cargo”) in the waybill.

- Paragraph 5 (“Consignor’s instructions”) provides the value of the cargo declared by the consignor. It should not be more than its actual value.

- The absence of an entry in the cargo transportation invoice form is confirmed by a dash. There should be no empty fields in the document.

- If there are no entries in paragraph 8, the general conditions under the Rules for the Transportation of Goods and the Federal Law “Charter of Motor Transport and Urban Ground Electric Transport” apply.

- The consignment note is drawn up in three copies: for the shipper, the consignee and the carrier. All copies are originals.

- The consignment note is signed by the shipper and the carrier or their authorized representatives. Corrections are certified by the same signatures.

- The form of the consignment note for the transportation of goods includes information about all consignments of cargo transported in one transport.

- If several cars are involved, the number of copies of the waybill must correspond to their number: for each car - three TN.

When transporting dangerous goods or when using large or heavy vehicles, in paragraph 13, if necessary, information about the route, as well as the number, date and validity period of the special permit is indicated.

What is this form for?

It is used by all parties involved in the trading process. The invoice allows you to verify the transferred goods with the data specified in it. If the buyer is not satisfied with the quality of the delivered products, based on documentary evidence, he has the right to return it to the supplier or exchange it for products that have the appropriate quality characteristics.

In addition, TNs involve forwarders in their work. It helps them avoid problems by confirming exactly what quantity is being transported. No one will accuse the driver of theft if the transported cargo is accompanied by documentary evidence.

What information does it contain?

The generated document consists of the following items

- information about participants who sell, send, receive and pay for cargo;

- details of the agreement on the basis of which the transfer is carried out;

- date and assigned number;

- list of goods plus units of measurement;

- list of attached papers;

- signatures of everyone involved in the process.

Affixing the seals of organizations and entrepreneurs is not a mandatory element. Therefore, some businessmen and companies do without them.

Results

The consignment note is the primary document, which is quite rightly considered the most common and easiest to use.

It helps control the movement of goods and other inventory items, guaranteeing financial security to the participants in the transaction. And to make document management easier, contact Cleverence. With the help of our software, you can easily conduct all routine operations, as well as accounting for goods and products in the warehouse. For example, you can use the “Warehouse 15” software, which will ensure the automation of all commodity accounting operations. Number of impressions: 2220

How to make corrections

It is not recommended to correct the invoice, like any other primary accounting document. But if errors are found in the register, corrections are made to both copies - both in the supplier’s documentation and in the form transferred to the customer.

Erroneous information is crossed out, corrections are certified by the signatures of authorized persons of both parties. Below is the date the corrections were made.

If an error is detected in the electronic register, the organization corrects the violation and sends a new invoice to the customer. There are no strict rules for making corrections in the electronic form.