Home / Consumers

Back

Published: 03/11/2020

Reading time: 10 min

0

32

- 1 Certificate of write-off of spare parts: document structure

- 2 Certificate of write-off of auto parts sample 2.1 Defective statement

- 2.2 Advisor

- 3.1 Defective statement

Why do you need a spare parts write-off act?

Enterprises that use cars regularly record transactions that reflect the turnover of spare parts for them. In this case, it is assumed that the following basic operations with these materials are recorded:

- Posting.

- Moving from one division of the company to another.

- Write-off for repair.

Each case uses its own supporting documents. If we talk about the 3rd operation, then as a corresponding document, many companies use an independently developed form of an act of writing off spare parts for a car, the main feature of which is the justification for the need to replace the corresponding spare part.

This act can be used as an alternative to such unified forms as an invoice (drawn up according to the M-15 form) or a demand invoice (drawn up according to the M-11 form), which do not always meet the specifics of the movement of spare parts accepted in the organization when writing off for repairs.

M-11 and M-15 are unified forms reflecting the release of goods and materials from the warehouse (clause 100 of the Methodological Instructions, approved by Order of the Ministry of Finance of the Russian Federation dated December 28, 2001 No. 119n). At the same time, the act of writing off for repairs can formalize the transfer of inventory items not only from the warehouse, but also between divisions of the company.

Read about forms M-11 and M-15 in the articles:

Accountant's Directory

Attention

The following entries are made in the company's accounting:

- The supply of spare parts is reflected: Dt 10/5 Kt 60 in the amount of 21,779.66 rubles;

- The VAT presented by the supplier is taken into account: Dt 19 Kt 60 in the amount of 3,920.34 rubles;

- Payment to the supplier is taken into account: Dt 60 Kt 51 in the amount of 25,700 rubles.

A special need for maintaining cards arises when an organization uses an exchange fund of spare parts that are repaired and subsequently installed on the operating system. Enterprises independently determine the list of accounting documents for inventory items.

A number of organizations with small warehouse receipts and issues keep a log of the movement of spare parts. If there is automated accounting, the journal is not used.

Some material assets, such as spare parts, are at some point used in the organization's activities, and for this they must be installed on equipment, vehicles, etc.

At the same moment, there is a need to document (take into account) this fact. In such a situation, the organization can draw up an act of installation of material assets, a sample of which will be given in this article.

Procedure for installing a spare part If there is a need to install a spare part, the organization can carry out this procedure on its own (if specialists are available) or involve a third-party specialized organization by concluding an appropriate agreement with it.

Accounting for spare parts requires careful documentation to confirm economically justifiable expenses.

Features of replacing spare parts of a fixed asset Installation of new parts, assemblies, spare parts on a fixed asset (OS) is carried out to replace failed worn out elements.

In order for the act to be as objective as possible, it is necessary to include in the commission a person who will subsequently directly use the vehicle on which the spare part is installed, as well as an engineer or auto mechanic who understands this equipment. act The act must be drawn up in writing.

Depending on the subjects of these relations and the subject of the agreement, this document may differ in content.

N 283/97-BP, hereinafter referred to as the Law on Profit), If the company has not carried out routine repairs on its own since the date of purchase of the car, then in accounting as of the date of liquidation of worn-out spare parts, their cost continues to be depreciated in the cost of the car according to P(S)BU 7 “Fixed assets”, and in tax - as part of group 2 fixed assets (clause 8.1.2 clause 8.1 art.

8 of the Profit Law). As a result of the liquidation of spare parts that are not suitable for use, the accounting records reflect their entry into the storeroom for the purpose of further delivery (sale) as scrap metal to a special organization. The cost of spare parts is included in the enterprise’s income under subaccount 716 “Reimbursement of previously written off assets” and is taken into account in subaccount 209 “Other materials” as part of inventories intended for sale.

The commission inspects the vehicle’s spare parts within the specified period and records in the report the reason for their write-off. In order for the act to have legal force and evidence, it must contain the mandatory details of the primary document. Their list, approved by the Law of Ukraine “On Accounting and Financial Reporting in Ukraine” dated July 16, 1999.

N 996-XIV, includes: - title of the document - date and place of preparation - name of the enterprise on behalf of which the document was drawn up - content and volume of the business transaction, unit of measurement of the business transaction - positions of persons responsible for the implementation of the business transaction and the correctness of its execution - personal signature or other data that makes it possible to identify the person who took part in the business transaction.

Act on write-off of spare parts: document structure

The act, based on the requirements of Art. 9 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ, must include:

- information about the enterprise (name, address);

- title of the document, date of its preparation, number;

- information about the structural unit of the company that writes off spare parts;

- information about the structural unit of the company that receives spare parts (for example, a repair shop);

- information about the types of spare parts being written off and their item numbers;

- data on the quantity and cost of written off spare parts;

- information about the accounts used to record the write-off of spare parts in accordance with clause 93 of Methodological Instructions No. 119n.

The document can be signed:

- a representative of the department from which spare parts are written off;

- repair shop employee.

Also, the chief accountant of the organization can put his signature on the document, confirming the correctness of the act.

The form of the act on the write-off of spare parts is entered into the document flow by order of the head of the company.

To learn about what a document for writing off materials for production may look like, read the material “Writ-off certificate - sample for 2017.”

General information

In order to keep records and control the production capacity of an organization, it is necessary to write off equipment in a timely manner, documenting it. From this moment it is written off from the balance sheet of the enterprise.

Drawed up in triplicate, certified by the signatures of the commission members and seal. Every year, the leading person of the organization is obliged to issue an order appointing a commission that will write off the main resources.

It includes a deputy director, accountant, economist and workers. The following material assets are subject to write-off:

- which cannot be used in the future because they are unsuitable;

- do not exist based on inventory results;

- morally outdated;

- completely worn out;

- have damage.

The act must include the following information:

- its name;

- date of preparation and approval;

- name of the enterprise;

- name and number of the item to be written off;

- list of defects;

- defect parameters;

- data and positions of commission members;

- their signatures.

When drawing up a document, there are nuances that should be adhered to. The main thing is to indicate the date (the one when the act was drawn up).

If an inventory was taken before drawing up the document, this is worth mentioning. The title must be specified in the prepositional or genitive case.

The text of the document should begin with an indication of the reason for drawing up the act. Basically, this is an order from the director. When decommissioning equipment, you must follow a certain procedure.

When the cost price is indicated, the following nuances should be indicated - the price during the purchase period, transportation costs, consultation fees, customs costs and the cost of intermediary services.

When drawing up a document, you must be guided by the following documents:

| Report of materially responsible persons | By used reserves |

| Planned costing | Which contains a list of all types of costs |

| Product quantity report | Which was produced for a specific period (reporting) |

The document must be kept in the organization for 15 years. The following write-off rules must be observed:

- the technical condition of each object is determined individually;

- the required documentation is drawn up, which indicates the specific resources that have failed;

- an act is drawn up;

- permission is obtained from the director of the organization to write off these funds;

- dismantling or disposal is carried out;

- funds are debited from the account.

What it is

The act of writing off fixed resources is a document that serves as the basis for deregistration of an object. Certificate of technical condition of equipment – a document attached to the write-off report.

The document must contain the results of the examination and the necessary measurements. It is also necessary to describe in detail the current state of the equipment, what shortcomings were discovered, and how they can be eliminated.

The act should include the following information:

- where and when the inspection was carried out;

- information about experts;

- information about everyone who attended the inspection;

- name of the equipment being tested - brand, type, number, etc.;

- where the equipment is located;

- information about his work;

- under what conditions the inspection was carried out - time, devices;

- the opinion of each participant;

- results of the work;

- troubleshooting instructions;

- list of documentation used;

- signatures of participants.

What is the role of the document

Write-off is necessary in two cases - for further use of equipment or for disposal.

A write-off act is required in the following cases:

| Get cost data | Produced goods for the purpose of further formation of value |

| Justify and support with documents | Taxation costs |

| Confirm asset performance | Which is transferred for use by other enterprises |

| Assess the state of inventory in the warehouse | — |

The process of writing off material assets is necessary for those assets that have become unusable - have lost their quality or have been damaged.

For a sample act for writing off gasoline for a lawn mower, see the article: sample act for writing off fuel and lubricants.

How to fill out the write-off form.

The document confirms the withdrawal of products from circulation for various reasons. The act gives formality to the write-off process. It also serves as the main document for checking equipment for unsuitability.

Legal regulation

By its Resolution No. 7 of January 21, 2003, the State Committee developed a typical form for writing off main resources.

According to Federal Law No. 402 “On Accounting”, adopted on December 6, 2001, organizations have the right to independently develop a form for a write-off act.

Features of the act for writing off car spare parts in Russia

During operation, the property gradually wears out. Cars that periodically require repairs are no exception. How are car parts written off in Russia, what are the features of drawing up the corresponding act?

The main business transactions relating to vehicles include the receipt, movement and disposal of spare parts.

Each of these facts must be documented. This is especially important when writing off parts. What are the features of the act for writing off automobile parts in Russia?

Automotive parts that are unusable should be scrapped. But the essence of the procedure is not so clear.

First of all, there must be confirmation of the validity of the write-off. In addition, there may be situations where spare parts are deregistered but not retired.

For example, if an organization has the necessary parts, they can be used for repairs, which requires them to be written off as a separate object.

If a faulty spare part that is not suitable for restoration is written off, a defective statement is issued. The document is drawn up by a specially created commission with the participation of a mechanic.

Based on the statement, an application for the purchase of a new spare part is submitted. The application must be approved by the chief accountant and the head of the organization.

Next, the necessary spare parts are purchased and taken into account. The purchased spare part, in accordance with the mechanic’s memo, is transferred to replace the faulty part.

After this, the old spare part can be written off. The write-off is documented by a defective statement and an inventory write-off act.

When car repairs are carried out by a third party, spare parts can be written off on the basis of an invoice for the release of materials to the third party in the M-15 form.

In this case, an acceptance certificate is additionally drawn up in a unified form.

When repairing on your own, the transfer of the part is carried out on the basis of a demand invoice, and the act can be drawn up in any form.

What it is

The act is the primary document confirming the fact of the transaction. Thus, the act of writing off car spare parts certifies the fact of writing off certain values from the organization’s accounting records.

Based on the provisions of Federal Law No. 402. the obligation to use unified forms of primary documentation is excluded.

Since 2013, organizations have the right to develop their own forms of documents, guided by standard templates. In this case, the document must contain mandatory details that allow it to be recognized as primary.

The structure of the act for writing off car spare parts is as follows:

Owner information

Name of organization, details, legal address

Write-off of purchased spare parts

Without prior posting of such

As for the act of writing off spare parts for a car itself, the validity of the document is recognized only if the basic requirements are met. Such as the availability of mandatory details and accuracy of data.

That is, all write-off parts must be identified in as much detail as possible in order to eliminate the possibility of erroneous write-off of other objects. The same applies to the cost of write-off spare parts.

The amount spent on purchasing the required part is written off, and not the residual value of the worn-out part. Disposal of spare parts requires compliance with certain preliminary procedures.

Thus, an act for writing off spare parts can be drawn up only after the process of identifying defects and establishing the scope of work is completed. And initially a proper order from the leader is necessary.

Formation of an order for a vehicle

To generate an order for a vehicle, a technical report is initially required on the failure of the vehicle due to physical wear and tear of parts.

The conclusion states that it is necessary to restore a certain unit through partial replacement of parts, or it is necessary to replace it due to the impossibility of repair.

Based on the technical report, the head of the organization issues an order to carry out repairs in accordance with the technical report.

At the same time, an order is issued to create a special commission that will determine the need to repair vehicles. If the need for repair work is confirmed, a defective statement is drawn up.

It indicates which parts need replacement. Based on the defective list, the necessary spare parts are purchased, which are then transferred upon request-invoice.

Upon completion of the repair, a materials write-off act is drawn up. In the event that there are spare parts suitable for use, they are received on the basis of a commission report. When spare parts are not subject to further use, a disposal report is drawn up.

Filling out form OS-4a

A separate write-off procedure is provided in cases where car repairs are deemed inappropriate. For example, the physical wear and tear of the asset is too great, and the depreciation value has already been written off.

In this situation, the vehicle is written off completely. For write-off, a standard form is used, approved by the State Statistics Committee of the Russian Federation in Resolution No. 71a of October 30, 1997.

An act is drawn up in form OS-4a in two copies. The first is sent to the accounting department along with a document confirming the deregistration of the car with the traffic police.

Another copy is retained by the responsible person and becomes the basis for depositing the valuables and materials remaining as a result of write-off.

When filling out form OS-4a:

Write-off costs and value of valuables

Those remaining after dismantling the car are displayed in the section “Certificate of costs associated with the write-off of vehicles and the receipt of material assets from their write-off”

The eighth column displays

The amount of accrued depreciation on a car at the time of its disposal

In the section “The following main parts and assemblies are subject to capitalization”

Displays the quantity, item numbers and cost of material assets remaining after write-off

From the first to the fourth columns

The amount of all expenses for writing off the car is displayed

In columns five to nine

Data is recorded on expenses associated with the write-off and values received after the write-off

Act OS-4a is signed by all members of the commission and the chief accountant. After this, the document is approved by the head of the organization.

Sample act for writing off tires

At this time, there are no approved standards regarding the write-off of spare parts and consumables, including tires used during the operation of vehicles.

The standard tire mileage is determined by the manufacturer. Guided by this information, the head of the enterprise can independently approve the mileage standards for car tires.

It is also permissible to base the approval on existing operating experience. In any case, operating mileage standards must be justified, economically justified and documented.

Find out what reasons there may be for writing off furniture in a write-off act from the article: write-off act.

Read how to draw up a sample defect report for equipment here.

About the form of a defective act in the construction of the Russian Federation, see here.

Tires are written off according to the standard scheme. But at the same time, you need to take into account the nuance that scrapped tires must be handed over for recycling.

A sample act for writing off tires looks like this:

- The title is “Act for writing off tires.”

- Document number, approving organization.

- Composition of the commission indicating the order of appointment.

- The fact that the tires were declared unfit for use.

- The name of the organization or department that operated the vehicle.

- Car data.

- Data on tires indicating the actual mileage and standard tire mileage.

- List of tire defects.

- The commission's conclusion regarding further use (completely unsuitable, handing over for disposal).

- Signatures of all commission members.

Is a vehicle inspection report required?

A car inspection report is required at the very initial stage, when a technical report on the condition of the car is being prepared. The act justifies the need for vehicle repairs and subsequent write-off of spare parts.

An inspection report is also drawn up upon completion of the repair to detect possible remaining faults.

The structure of the vehicle inspection report includes:

- mandatory details;

- composition of the commission;

- vehicle identification information;

- owner's name;

- technical condition parameters;

- signatures of responsible persons.

Defective statement

The defect sheet refers to the primary documentation and records defects, breakdowns, and all kinds of defects in equipment, devices, and materials used in the activities of the enterprise. In order to carry out their repair and restoration according to all the rules, you need to follow a certain procedure, part of which is the preparation of a defective statement. It should be noted that the defect report, also drawn up when deficiencies are detected in inventory items, is not an exact copy of the statement and serves only as an appendix to this document.

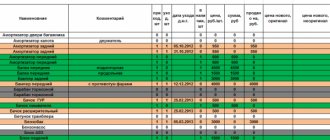

Certificate of write-off of auto parts

Name I APPROVED the organization _____________________ _________________________________ (position) ___________ _____________________ (signature) (signature transcript) “___” _____________ 20__

ACT N __________

for write-off of auto parts

from "___" ______________ 20___

A commission consisting of: chairman _________________________________________________ (position, full name) members of the commission _________________________________________________ (position, full name) ________________________________________________, (position, full name) appointed by order (instruction) No. ______ dated _____________ , confirms the write-off of the following spare parts spent on the repair of vehicles during the period from ________ to _______: —————————————————————————————- ¦ N ¦Name¦ Unit¦Quantity-¦Price¦Amount¦ Number ¦ For repair of which unit ¦Number and date¦ ¦p/p¦auto parts¦meas.¦ in ¦rub.¦ rub.¦vehicle¦vehicle ¦ defective ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦spare parts wasted¦ statements ¦ +—+————+—-+—-+—-+——+———-+————————+ ————+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+————+—-+—-+—-+——+———-+————————+— ———+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+————+—-+—-+—-+——+———-+————————+—— ——+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+————+—-+—-+—-+——+———-+————————+——— —+ ¦ ¦ Total¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ —-+————+—-+—-+—-+——+———-+————————+——— —- Total number ________________________ units, total write-off amount (in words) _________________________________________ rub. (in words) After replacing spare parts, scrap metal was registered at the price of procurement organizations: —————————————————————————— ¦ N ¦ Name ¦Unit. unit ¦ Quantity ¦ Price ¦ Cost ¦ ¦p/p¦ auto parts ¦ ¦ ¦ rub. ¦ rub. ¦ +—+———————+———+———-+———+——————-+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—+——————— +———+———-+———+——————-+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ —-+———————+———+———-+— ——+——————— Scrap (scrap) was delivered to the warehouse for repair (destruction) according to invoice N ___ (cross out what is unnecessary) dated “___” ___________ 20__. The organization drew up an act of acceptance and delivery of the car from repair in one copy. The act was signed by members of the commission and the organization’s mechanic. A note about the repair was made in the vehicle's inventory card. Chairman _______________ ________________ _____________________ (position) (signature) (signature transcript) Members of the commission: _______________ ________________ _____________________ (position) (signature) (signature transcript) _______________ ________________ _____________________ (position) (signature) (signature transcript)

Sample of drawing up a defective statement

- At the top left or right (it doesn’t matter) several lines are allocated for approval by the head of the enterprise. This includes:

- his position (director, general director),

- Full Name,

- full company name.

- Then in the middle of the line the name of the document and its number according to the internal document flow are written, below is the locality in which the company is registered and the date the statement was compiled.

- Next comes the main part. It is formed in the form of a table,

- in the first column of which the serial number is entered,

- in the second - defects and damage discovered during the inspection,

- third - the required measures to eliminate them,

- in the fourth - the time frame within which the damage must be corrected.

- At the end, the document is signed by the members of the commission who participated in the inspection of the equipment, device or inventory, indicating their positions and decoding autographs.

Particulars.

The further fate of spare parts obtained as a result of dismantling may develop differently. They can be sold in the form of separate blocks or sold as scrap metal to a specialized organization. Sometimes dismantled spare parts are planned to be used in the future to repair cars of a similar brand.

As already discussed above, the release of materials into production and their other disposal are carried out in a manner fixed in the accounting policy of the organization. At the same time, regardless of the chosen method, inventories that cannot replace each other in the usual way can be valued at the cost of each unit (clause 17 of PBU 5/01). This, according to the author, can exactly be attributed to our situation.

Example 5. LLC Transport Company, after an accident involving a GAZ 33-07 car it owned and the subsequent dismantling of a vehicle that could not be restored, handed it over to a specialized scrap metal collection point. After the assessment, the scrap metal was capitalized in accounting at market value - 8,000 rubles.

Since in this article we are considering only accounting issues, calculations with the VAT budget for the sale of spare parts, including the delivery of scrap metal, are not given.