The loss of materials is written off as a transaction loss

The following articles talk about the nuances of inventory:

- “Inventory of inventories: order and nuances”;

- “Procedure for conducting an inventory of fixed assets”;

- “The procedure for carrying out a BSO inventory (nuances).”

To understand the postings for writing off shortages during inventory, we will use the conditions of the example.

After conducting an inventory at warehouse No. 3 (the financially responsible person is storekeeper Zavyalov N.

InfoS credit account 94 they can be written off:

- for production or sales costs;

- against the culprit with compensation from his earnings or by paying him the amount of the loss to the company’s cash desk;

- in other expenses.

Write-off of shortage within normal limits

Shortages within the limits of natural loss are written off as production or sales costs. Write-offs are carried out from accounts intended for recording material assets into expenses by type of production, using account 94:

- Dt 94 Kt 10 (41, 43..);

- Dt 20 (23, 44..) Kt 94.

By analogy with shortages, the write-off of losses from defects is reflected in the accounting entry in the debit of accounts 20, 23, 29, etc.

and account credit 28, depending on in which production they are identified: main, auxiliary, servicing.

Objects under repair are also reflected separately; an inventory report of unfinished repairs in the INV-10 form is filled out for these fixed assets.

Objects that are listed in the organization, but do not belong to it, for example, those that are in custody, are entered into separate matching statements.

All inventory documents are certified by the signatures of financially responsible persons and members of the commission headed by the chairman.

The final results of the inventory of fixed assets are entered into the statement of results, form INV-26.

OS inventory accounting

The results of the inventory are subject to immediate reflection in the accounting records of the enterprise.

Write-off of materials in 1C

In manufacturing organizations, materials are used to produce products.

Writing off materials is a process that includes certain specifics and follows established rules.

Before writing off the material, let’s briefly consider how to configure it correctly:

- accounting policy of the organization,

- accounting accounts for the item group and the item itself,

- How to make the receipt of materials to the warehouse.

Let's start with the most important “Accounting policy” (“Main” - “Settings” - “Accounting policy”)

In this form we indicate “Method of operation of MPZ” - “According to average”.

It is important to note: that an enterprise that is on the general taxation system (OSNO) can choose any valuation method. When we need a method of valuation based on the cost of a unit of material, we choose the FIFO method.

However, if the organization is on a simplified taxation system (USN 15%), then materials will be written off only using the FIFO method. This is due to some features of this taxation system.

Let's move on to setting up accounting accounts for the item group and the item itself.

In order to set up accounts correctly, let’s go to “Directories” - Nomenclature”

Create a product group “Materials” by clicking on the “Create group” button. Enter the Group Name and “Type of Item”

After creating the group, follow the hyperlink “Item Accounting Accounts”

In the window that opens we see a general list

We create a new record or we can copy an existing one. In this case, copy the “Materials” entry. Afterwards, a new form will open in which all accounting accounts will already be registered; all that remains is to fill out the “Nomenclature” details.

After this setting, all materials that will fall into this product group will be understood by the program that this item is “Material”.

After all the settings, we create receipts of materials. To do this, we will use the document “Receipts (acts, invoices)” (“Purchases” - “Receipts (acts, invoices)”)

Create a new document with the type of operation “Goods (invoice)”

We fill out the header of the document, after which we proceed to filling out the tabular part of the document. Adding nomenclature. Please note that accounting accounts and VAT invoices are entered automatically

We carry out the document

Write-off of materials for general business needs

Let’s use the document “Requirement - Invoice” (“Warehouse” - “Requirement - Invoice”)

Let's create a new document and fill out the header of the document, indicating “Organization”, “Warehouse”, “Purpose of expenditure” (the purpose of using material assets is indicated).

Let's move on to filling out the document. On the “Materials” tab, add the required nomenclature

Go to the “Cost Account” tab and indicate:

- Cost account - an account in which costs are accumulated. According to the accounting system, these accounts are taken into account, since the costs are spent on general business needs.

- Department - from which the material is issued

- Cost item - the item on which costs will accumulate

We record and post the document. Then you can see the transactions that this document created.

Dt 26 Kt 10.01 - the cost of materials was written off as general business expenses, using the operation method - By average.

Write-off of materials for production

When you need to write off material for the manufacture of some product, you can use two methods:

- The document “Demand invoice” is used if the material is written off in total quantity.

- The document “Production report for a shift” is used if you need to write off a certain amount of material for a certain finished product.

Using the document “Demand invoice” on the “Materials” tab, select the item we need.

Then go to the “Cost Accounts” tab:

- We enter the cost account on January 20 - this account relates to the production of products and direct costs will be taken into account on it.

- Nomenclature group - indicates the type of product.

- Items tomorrow - indicate the cost item “material costs”

- Products - indicates the finished products for which materials will be written off.

Movements of the document that were formed after the

Dt 20.01 Kt 10.01 - shows what cost of materials was written off for production.

Let’s consider the option when materials are written off using the document “Production Report for a Shift” (“Enterprises” - “Product Output” - “Processing”).

We create a new document in which we fill in the necessary details.

On the “Products” tab, select the item that will be manufactured and in this nomenclature the “Specification” column is filled in, then on the “Materials” tab the data will appear by first clicking the “Fill” button.

Posting a document

Dt 43 Kt 20.01 - production release.

Dt 20.01 Kt 10.01 - write-off of materials for the manufacture of the required products.

Write-off of IBP.

MBP are low-value and wearable items. This category includes assets that have a service life of no more than 1 year and the cost of these assets is at least 40,000 rubles. These assets are included in account 10.09 “Inventory and household supplies”.

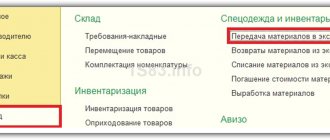

The transfer of IBP occurs using the document “Transfer of materials into operation” (“Warehouse” - “Workwear and equipment” - “Transfer of materials into operation”)

We create a document, indicate the organization and warehouse and go to the “Inventory and household supplies” tab.

Using the “Add” or “Selection” button, select the required inventory and transfer it to the document.

Postings of this document

Dt 44.01 Kt 10.09 - writing off the cost of inventory as expenses;

MC.04 - the cost of inventory in operation is reflected off the balance sheet.

MBP is written off using the document “Write-off of materials from service” ((“Warehouse” - “Workwear and equipment” - “Write-off of materials from service”)

Create a document and go to the “Inventory and Household Supplies” tab. Select the desired item and fill in all the required fields.

We post the document and look at the postings it created

Kt MTs.04 - write-off from off-balance sheet accounting of the cost of inventory transferred for operation.

It is important to pay attention to errors that may occur when writing off materials.

Let's briefly look at some of the most common errors.

- When there are not enough materials in the warehouse.

This error may occur if the required amount of materials was not accepted for accounting.

By default, when posting a write-off document, the program will display the error “The column “Quantity” is filled in incorrectly.”

However, this warning can be bypassed by turning it off, so to speak.

By going to the “Administration” – “Posting Documents” section, we can set the setting “Allow inventory write-off if there are no balances according to accounting data.”

If this setting is enabled and documents are posted, the debit will occur without the amount.

- Difference in receipt and debit

It happens that when a material is received, it is indicated as “Goods” (accounting account 44.01), but is written off as “Material” (accounting account 10.01). Initially, this is no longer correct, since upon receipt the material must be reflected in the program as “Material”, and not as “Product”.

To correct this error in the program, you just need to go to the required document and enter the required accounting account opposite that material.

It so happens that the program keeps records of several warehouses, so when creating a document it is worth paying attention to which warehouse receives this or that material.

Since when writing off material and selecting the wrong warehouse, the program will display a message that the warehouse does not have enough of the required quantity.

But if this mistake has already been made, then you should use the “Movement of Goods” document, which is located in the “Warehouse” menu item.

Features of accounting for shortages and losses

When reflecting shortages and damage, a number of rules must be taken into account.

Reflecting shortages

Shortages can only be recorded when they are discovered:

- when carrying out inventory;

- upon receipt of objects in volumes limited by the supply agreement.

On the DT account, the shortage is recorded in the following amounts:

- Real cost if the values cannot be restored or do not exist at all.

- Residual value, if the question concerns fixed assets that are out of order or missing.

- Real losses if partial damage occurs.

That is, the accounting amount is determined depending on the specific circumstances.

Write-off

The write-off is carried out on CT account 94. In the process, they are included in the cost structure.

The accounting entry was written off as a loss of materials.

Usually, employees with whom agreements on full financial responsibility have been concluded are responsible for shortfalls in the response. Let's say a warehouse worker.

Employees whose fault caused shortages are required to compensate for material damage to the company.

Attention: This is directly stated in paragraph 1 of Article 243 of the Labor Code of the Russian Federation.

The employee responsible for the shortage can cover the damage by depositing money into the company's cash register. Another option is that the company and the employee agreed that the accounting department will withhold funds from upcoming salaries.

In this case, do not forget about the restriction: the amount of withheld funds should not exceed 20 percent of the salary. If the damage is greater, you will have to provide the employee with an installment plan.

In any case, take a statement from the employee in which he writes that he agrees to compensate for the damage and within what time frame.

If the employee refuses to compensate for the damage, the company has the right to go to court. Important: Then in the transactions, instead of account 73, account 76 “Settlements with various debtors and creditors” is used.

Tax accounting for shortfalls is somewhat simpler - in it the amount of the shortfall is considered a non-operating expense, and the compensated damage is fully attributed to non-operating income (letter of the Ministry of Finance of Russia dated October 14, 2010 No. 03-03-06/1/648).

But in the case where the manager decides not to recover damages from the guilty person, the amount of the shortfall cannot be written off as expenses. For these purposes you will have to spend your net profit.

When compensation for damage is made at the expense of the employee, the manager issues an appropriate order.

Manager of Romashka LLC Lopatkin O.G.

Knocked a can of paint over a box of printer paper, rendering it unusable. Lopatkin admits his guilt and is ready to reimburse the book value of the paint in the amount of 300 rubles. and paper in the amount of 200 rubles.

They can be written off as other expenses. In this case, this wiring is performed: DT91/2 KT94. The entry is relevant when the amount of losses exceeds the norms of natural profit. If the person responsible for causing the damage is found, recovery occurs. In this case, the following wiring is relevant: DT73/2 KT94. If a shortage is detected within the EU boundaries, it is written off at the expense of cost. Record used: DT20, 44 KT94.

If a shortage is discovered upon acceptance of goods and materials, it makes sense to act on the basis of the provisions of the agreement. The agreement, as a rule, stipulates the maximum amount of shortages. If losses are made within these values, they are reflected in account 94.

Company assets can be lost as a result of force majeure (flood, drought, earthquake) or stolen by thieves who cleverly cover their tracks.

First, the property owner must understand the true reasons for the shortage and take measures to find the perpetrators, as well as evidence of their involvement in the loss of valuables. To do this, the company can conduct an internal investigation itself or file a complaint with the police.

Let's look at an example to see what kind of postings are used when writing off a shortage if the culprit is not identified.

Construction materials worth RUB 2,654,399 disappeared from the construction site.

38 kopecks

Registration and approval of results Accounting reference Bringing accounting data into compliance with actual availability. Write-off of shortages or capitalization of surpluses

Reasons for conducting an inventory, in addition to the annual obligation, may be:

- Change of financially responsible person;

- Fact of theft or damage;

- Disaster;

- Organizational reasons (change of manager, reorganization, etc.):

Get 267 video lessons on 1C for free:

- Free video tutorial on 1C Accounting 8.3 and 8.2;

- Tutorial on the new version of 1C ZUP 3.0;

- Good course on 1C Trade Management 11.

The results of the inventory can be:

To carry out an inventory at the enterprise, a commission consisting of at least three people is formed.

And those that are not associated with emergency events.

Due to emergency events

Deficiencies arising as a result of force majeure events are included in accounting as other expenses.

In this case, make the following entries:

DEBIT 94 CREDIT 41 – reflects the cost of missing goods;

DEBIT 91 subaccount “Other expenses” CREDIT 94 – the cost of missing valuables is written off as other expenses.

Losses resulting from extraordinary events should be written off as material expenses in tax accounting. But first, be sure to obtain written confirmation from the authorities that force majeure actually occurred. For example, a certificate from the Ministry of Emergency Situations.

Due to the employee's fault

But usually, excess shortages are not associated with extraordinary events. Accounting for shortages depends on whether there are those responsible for them.

Let's consider typical accounting entries for writing off shortages of materials identified during the inventory.

How to take into account the write-off of illiquid inventory items in tax accounting

Material costs include losses from shortages or damage to goods and materials during their storage and transportation within the limits of natural loss norms established by law (clause 2, clause 7, article 254 of the Tax Code of the Russian Federation).

However, expenses associated with shortages or damage to inventory items for other reasons can also be included in income tax expenses if they meet the requirements of paragraph 1 of Art. 252 of the Tax Code of the Russian Federation on economic feasibility and documentary evidence.

Such costs can be written off by inclusion in one of the following categories: non-operating expenses (clause 20, clause 1, article 265 of the Tax Code of the Russian Federation), other expenses associated with production and sales (clause 49, clause 1, article 264 of the Tax Code of the Russian Federation) ). The lists are open. It should be noted that including the cost of damaged valuables in expenses may entail claims from the tax authorities (Letter of the Ministry of Finance of Russia dated 06/07/2011 N 03-03-06/1/332).

However, with proper documentation, a positive outcome of the dispute with the tax authorities is very likely for the organization.

The Resolution of the Federal Antimonopoly Service of the North-Western District dated September 11, 2008 in case No. A56-3652/2007 considered a situation where a company wrote off physically worn-out and obsolete materials as illiquid property and included their cost in expenses. The court found that the materials were recognized as illiquid due to their long-term storage (the materials were purchased in 1980 - 1995 for production purposes), lack of movement (income - expenditure), loss of marketability, and unsuitability for use. The court came to the conclusion that the company was not able to use the decommissioned materials for their intended purpose due to the loss of their original properties, and indicated that the decommissioned materials were purchased by the company directly for production activities, their use was supposed to generate income, which is justified, in accordance with Art. 252 of the Tax Code of the Russian Federation.

The cost of physically worn out and obsolete materials at the time of their write-off as illiquid property can be attributed to the reduction of taxable profit.

Regarding the restoration of the VAT amount.

According to the position of the Supreme Arbitration Court of the Russian Federation, set out in Decisions dated May 19, 2011 N 3943/11, dated October 23, 2006 N 10652/06, the obligation to pay to the budget VAT amounts previously legally accepted for deduction must be directly provided for by law, and the Tax Code of the Russian Federation does not provide for restoration VAT previously accepted for deduction when writing off expired goods.

The Federal Tax Service of Russia has a similar opinion (Letter dated 05/21/2015 N ГД-4-3/ [email protected] ).

But at the same time, there are explanations from regulatory authorities in which they insist on the restoration of VAT in such cases (see, for example, Letter of the Ministry of Finance of Russia dated January 21, 2016 N 03-03-06/1/1997). And although the decisions of the highest courts have priority over the explanations of the Ministry of Finance of Russia, the possibility of claims from regulatory authorities cannot be excluded (Letter of the Ministry of Finance of Russia dated November 7, 2013 N 03-01-13/01/47571 (sent for information and use in the work of the Letter of the Federal Tax Service Russia dated November 26, 2013 N GD-4-3/21097)).

How to reflect shortages of materials as a result of inventory

To carry out the inventory, a special inventory and a commission are created that will conduct the event. Inventory can be carried out in warehouses or inside any premises.

Postings:

Account Dt Account Kt Description of posting Amount of posting Document-basis 94 10.01 Identification of shortage of materials Amount of shortage Inventory list INV-3

Matching sheet INV-19

Accounting certificate-calculation

Postings for loss of materials within normal limits

Some finished products tend to decrease in weight or volume.

Reasons for leaving

Disposal of intangible assets listed in the organization may occur for the following reasons:

- expiration of a certificate, patent or other documents that confirm the company’s right to use intangible assets;

- unsuitability of the asset for further use;

- transfer of an intangible asset to the authorized capital of other business entities;

- gratuitous transfer of intangible assets;

- sale of these assets.

Note 1

In accordance with the 22nd paragraph of Accounting Regulation 14/2000, the value of intangible assets that are no longer used for the purposes of producing products, providing services, performing work or to meet the management needs of the organization is subject to write-off.

In parallel with the write-off of the residual value of intangible assets, the amount of accumulated depreciation is also subject to write-off, if this amount was previously reflected in accounting in the accounting account $05$ “Depreciation of intangible assets.”

Can not understand anything?

Try asking your teachers for help

Income and expenses received as a result of writing off intangible assets:

- reflected in the accounting records of the organization in the reporting period to which they relate;

- are included in the financial results of the organization.

The instructions for using the Chart of Accounts indicate that when writing off intangible assets, their value should be reduced by the amount of depreciation charges accrued during the period of operation, if depreciation was recorded on account $05$ “Depreciation of intangible assets.” This is reflected in accounting by the following entry:

- Debit $05$ “Amortization of intangible assets”

- Credit $04$ “Intangible assets”

The residual value of the disposed intangible assets is written off using the following entry:

- Debit $91-2$ “Other expenses”

- Credit $04$ “Intangible assets”

The balance of the $91$ “Other income and expenses” account is calculated every month by comparing debit and credit turnover. Then $91-9$ is written off from the subaccount to the $99$ “Profit and Loss” account.

Getting rid of unnecessary junk: writing off illiquid assets in trade

If the organization provides for the creation of a reserve for the depreciation of inventory items, their value is written off at the expense of this reserve. It should be noted that the formation of a reserve for a decrease in the cost of inventory and materials is a mandatory requirement for all organizations, except those that are granted the right to use simplified methods of accounting (paragraph 2 of clause 25 of the Accounting Regulations “Accounting for inventories” PBU 5/ 01 (approved by Order of the Ministry of Finance of Russia dated 06/09/2001 N 44n));

Disposal due to expiration of useful life

At the moment an intangible asset is accepted for accounting, the company determines its useful life. After this period, the intangible asset must be written off from accounting. The basis for writing off an intangible asset is an act drawn up by a specially organized commission, its composition determined by the head of the organization.

Based on the drawn up and signed act on the write-off of an intangible asset, which is approved by the head of the company, the object is written off from the register. This fact is recorded in the Intangible Asset Accounting Card.

Depreciation is accrued on an intangible asset in accordance with PBU 14/2000 and stops from the first day of the month that follows the month of repayment of the full cost of the intangible asset.

Example 1

The company owns an intangible asset. Its initial cost is $18,000 rubles excluding VAT. The useful life at the time the object was accepted for accounting was set at five years and ends in December of the current year. The amount of depreciation charges for the period of operation of an intangible asset in the account $05$ “Amortization of intangible assets” as of November $30 of the current year is equal to $17,700$ rubles. Thus, in December of the current year, the accountant must make the following accounting entries:

Picture 1.

Form of the act

Based on the Guidelines, organizations themselves develop forms and samples of primary documents. The albums of unified forms of primary accounting documentation do not provide for the form of an act on write-off of inventory items. Consequently, each organization can independently develop and approve an act on the write-off of material assets. However, you can use OKUD forms 0504230 and 0504143, which are used by state and municipal institutions.

How to take into account the write-off of illiquid inventory items in accounting, for income tax, VAT, and what documents should be used?

- Content:

- How to document the write-off of illiquid inventory items

- How to take into account the write-off of illiquid inventory items in accounting

- How to take into account the write-off of illiquid inventory items in tax accounting

Depending on the circumstances surrounding the write-off, the cost of illiquid inventory items can be attributed: to production expenses or selling expenses; on account of other settlements with personnel; on account of other expenses, if the perpetrators have not been identified; to the profit and loss account.

For the purpose of calculating income tax, costs associated with shortages or damage to inventory items can be taken into account as non-operating or other expenses.

The question of the need to restore VAT on illiquid inventory items written off from the balance sheet remains controversial.

The procedure for documenting the write-off of inventory items is set out in the justification.

Rationale : Inventory and materials may become illiquid as a result of physical and/or obsolescence.

Physical obsolescence is a fairly objective process, implying the deterioration of materials and the impossibility or limited possibility of their further use.

This can happen for several reasons: due to improper storage (transportation), due to any actions (intentional or careless), for objective reasons (for example, after the expiration date). Looking ahead, we note that the cause of damage affects the method of writing off inventory items in the organization’s accounting records, as well as the procedure for calculating taxes, and if the inventory items were insured, then also the procedure for paying insurance compensation. Therefore, this reason should be established reliably in each case.

Moral obsolescence is a process that is not as obvious as physical deterioration, especially if it is not accompanied by a change in the physical qualities of values. Inventory and materials can become obsolete on their own. A typical example is, for example, values related to the fashion industry - clothes, shoes, accessories, etc. Moreover, the more expensive and high-status the product, the greater the risk of obsolescence.

Such inventory items, such as spare parts for high-tech mechanisms and devices, may become obsolete due to the obsolescence of the devices themselves. For example, in the case of replacing such devices with more advanced ones.