What is said in the Tax Code of the Russian Federation about the deduction of VAT on an advance invoice

Based on paragraphs.

1st and 12th Art. 171 of the Tax Code of the Russian Federation, the buyer has the right to deduct VAT calculated when paying an advance on account of future deliveries. As a general rule, the right to claim VAT for deduction is available within three years from the moment such an opportunity arises (clause 2 of Article 173 of the Tax Code of the Russian Federation). However, specifically in terms of deductions for advances, this rule is not applicable, and transfer of the deduction to later periods (quarters) is not allowed (letter of the Ministry of Finance of the Russian Federation dated 04/09/2015 No. 03-07-11/20290).

Find out more about the general procedure for deducting VAT on advances.

Calculations for “advance” VAT

The buyer has the right to deduct the amount of VAT charged to him by the seller when transferring an advance payment on account of upcoming deliveries of goods (performance of work, provision of services, transfer of property rights) (Clause 12 of Article 171 of the Tax Code of the Russian Federation).

The grounds for deducting VAT from the buyer are (clause 9 of Article 172 of the Tax Code of the Russian Federation):

- an invoice that the seller must issue no later than five calendar days from the date of receipt of the advance payment (clause 1, clause 3 of Article 168 of the Tax Code of the Russian Federation);

- payment documents confirming that money has been transferred for upcoming deliveries of goods (performance of work, indication of services), transfer of property rights;

- an agreement that must contain a condition for prepayment.

If the purchasing company does not fulfill at least one of these conditions, it will be denied a deduction.

The law establishes that if the seller has shipped goods whose cost is less than the advance payment received earlier, the buyer is obliged to recover VAT only in the amount indicated in the invoice for shipment.

If all of the above conditions are met, then the VAT transferred to the supplier as part of the prepayment can be deducted.

Please note that for the buyer, deducting VAT from the advance payment is a right, not an obligation. That is, by transferring an advance payment to the seller, the buyer may not count the “advance” VAT, but take advantage of the deduction only upon shipment. But if a deduction from the advance payment is claimed, upon receipt of the goods the tax should be restored (subclause 3, clause 3, article 170 of the Tax Code of the Russian Federation).

The commentary letter states that if the seller issued an advance invoice in one quarter, and the buyer received it in the next, then VAT can be deducted only in the period when the invoice was received by the buyer. The period of its exposure does not matter.

Example.

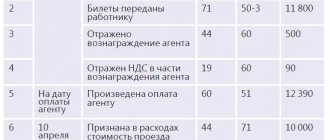

Deduction of VAT on a “late” invoiceA contract was concluded between the buyer and seller for the purchase of goods in the amount of 600,000 rubles. (including VAT - 100,000 rubles). The agreement provides for 100% advance payment. The prepayment was transferred on February 28, 2021. The seller issued an invoice for the prepayment received and sent a copy of the document to the buyer by mail, but it was received by the accounting department only on April 1, 2021. The supplier shipped the goods on April 20, 2021. On the day of shipment, the supplier presented the buyer with an invoice for the shipped goods. When posting goods, the accountant of the purchasing company must accept the “input” VAT for deduction and at the same time restore the VAT accepted for deduction from the advance payment. The accountant of the purchasing company will make the following entries: 02/28/2019 Debit 60, subaccount “Calculations for advances issued” Credit 51,600,000

rubles.

– prepayment was transferred to the supplier. In the first quarter, the transfer of the advance payment by the buyer did not entail any tax consequences. 04/01/2019 Debit 68, subaccount “Calculations for VAT” Credit 76, subaccount “Calculations for advances issued”

100,000 rubles.

– based on the invoice, VAT was accepted for deduction on the transferred advance. 04/20/2019 Debit 41 Credit 60, subaccount “Settlements for advances issued”

500,000 rubles.

– the goods are capitalized; Debit 19 Credit 60, subaccount “Settlements with suppliers”

100,000 rub.

– reflected “input” VAT on goods received; Debit 68, subaccount “Calculations for VAT” Credit 19,100,000

rub.

– accepted for deduction of VAT on goods received; Debit 60, subaccount “Settlements with suppliers” Credit 60, subaccount “Settlements for advances issued”

600,000 rubles.

– prepayment for the goods has been credited; Debit 76, subaccount “Calculations for advances issued” Credit 68, subaccount “Calculations for VAT

100,000 rubles. – the VAT accepted for deduction on the advance was restored.

What does the Ministry of Finance say about deducting VAT from an advance payment if the invoice was received in a different period

Along with the conclusion that transferring the advance deduction to other periods is generally unacceptable, the Ministry of Finance also clarifies the situation when, at the time of closing the VAT period, there is no VAT invoice yet.

In a letter dated 04/16/2019 No. 03-07-09/27004, officials clarify that if preliminary (partial) payment is made by the buyer in one tax period, and the invoice is received by the buyer in the next tax period, the VAT deduction should be made when actually invoice received.

VAT deduction on advances. Partially

When calculating the amount of VAT payable to the budget, does a taxpayer have the right to reduce the total amount of tax calculated on transactions recognized as the object of taxation by partially deducting VAT on an advance invoice in one period (when all the conditions for this have arisen - the advance has been paid, did the supplier issue an invoice for the advance payment), and partially in subsequent ones?

In accordance with paragraph 1 of Art. 171 Tax Code of the Russian Federation

When calculating the amount of VAT payable to the budget, the taxpayer has the right

to reduce the total amount of tax

calculated on transactions recognized as the object of taxation

by tax deductions

established by this article of the Tax Code of the Russian Federation, including in accordance with

paragraph 12 of Art. 171 of the Tax Code of the Russian Federation for the amount of the transferred payment

(partial payment)

on account of upcoming deliveries of goods

(performance of work, provision of services, transfer of property rights).

Deductions of tax amounts specified in clause 12 of Art. 171 Tax Code of the Russian Federation

, are made

on the basis of invoices issued by sellers

:

– upon receipt of payment, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights;

– documents confirming the actual transfer of payment amounts, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights;

– if there is an agreement providing for the transfer of specified amounts.

In letter dated November 22, 2011 No. 03-07-11/321, the Ministry of Finance of the Russian Federation noted that the Tax Code of the Russian Federation provides for the taxpayer’s right to deduct VAT on the listed amounts of advance payment

(partial payment),

and not the obligation to accept tax as a deduction

.

Therefore, partial deduction of VAT amounts

listed

as part of the prepayment does not contradict the norms of the Tax Code of the Russian Federation

.

The regulatory authorities indicate that VAT amounts charged to the taxpayer upon the purchase of goods (work, services) are subject to deduction in the tax period in which the taxpayer has the right to deduct the tax.

.

If implemented

In order for a taxpayer

to deduct VAT in tax periods following the tax period in which the right

to such a deduction arose, the taxpayer must submit to the tax authority

an updated declaration

for the tax period in which the right to apply a tax deduction arose.

Moreover, on the basis of the provisions of paragraph 2 of Art. 173 Tax Code of the Russian Federation

The taxpayer can submit such a declaration within three years after the end of the tax period in which this right arose (letter of the Ministry of Finance of the Russian Federation dated March 12, 2013 No. 03-07-10/7374, Federal Tax Service of the Russian Federation dated March 30, 2012 No. ED-3 -3/ [email protected] ).

In accordance with paragraphs 3 p. 3 art. 170 of the Tax Code of the Russian Federation, tax amounts accepted for deduction

by the taxpayer for goods (work, services), including fixed assets and intangible assets, property rights,

are subject to restoration

by the taxpayer

in the event of the buyer transferring payment amounts, partial payment

for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights .

Reinstatement of tax amounts is carried out by the buyer in the tax period in which the tax amounts

for purchased goods (works, services), property rights

are subject to deduction

in the manner established by the Tax Code of the Russian Federation.

Tax amounts are subject to restoration in the amount previously accepted for deduction in relation to payment, partial payment

against upcoming deliveries of goods (performance of work, provision of services), transfer of property rights.

If the taxpayer has partially deducted VAT from the advance amount

(that is, did not apply a deduction), then, according to the Federal Tax Service of the Russian Federation, the provisions

of paragraphs.

3 p. 3 art. 170 of the Tax Code of the Russian Federation ,

which provide for the rules for the restoration

of tax amounts accepted for deduction,

do not apply

.

In this case, the taxpayer also has the right to make a tax deduction

for goods (work, services) accepted for accounting, property rights acquired for the implementation of transactions subject to VAT, subject to the requirements stipulated by Chapter 21 of the Tax Code of the Russian Federation, in particular,

in the presence of primary accounting documents and invoices

(letter dated September 20, 2009 No. 3-1-11/651).

We accept VAT deduction on an advance invoice: conditions for different periods

We summarize the explanations of the Ministry of Finance and practical experience in applying VAT deductions not during the period of actual transfer of the advance.

In order to easily deduct VAT on an advance invoice received in the period following the advance payment period, you need to have:

- an agreement with fixed terms of advance payment;

- confirmation of the payment itself (payment order, bank statement);

- invoice from the supplier;

- confirmation that the invoice was actually received in the next tax period.

Obstacle #1 – inability to claim a deduction before submitting your tax return

According to the general rule established by clause 1.1 of Article 172 of the Tax Code of the Russian Federation, upon receipt of an invoice by the buyer from the seller of goods (work, services) after the end of the tax period in which these goods (work, services) were registered, but before the deadline Submitting a tax return for the specified tax period, the buyer has the right to deduct the amount of value added tax in relation to such goods (work, services) starting from the tax period in which the specified goods (work, services) were registered.

AUDIT of housing and communal services

That is, the above rule directly allows the buyer to deduct VAT retroactively on sellers’ invoices received after the goods (works, services) were accepted for registration.

MAINTENANCE OF ACCOUNTING REPORTS

However, the deduction of “advance” VAT is not provided for by this norm of the Tax Code of the Russian Federation. Therefore, upon receipt of an invoice for advance payment (partial payment) before the 25th day (inclusive) of the month following the tax period in which the amounts of such payment (partial payment) are transferred to the seller, the buyer does not have the right to claim the amount of VAT deductible presented by the seller under such invoice. Such tax amounts are accepted for deduction in the tax period in which the corresponding invoices were received (Letter of the Ministry of Finance of the Russian Federation dated March 24, 2017 No. 03-07-09/17203).

For example, if the taxpayer transferred an advance payment to the supplier on June 30, 2017, and the “advance” invoice was issued by the supplier on July 3, 2017, the buyer will have the right to an “advance” VAT deduction only in the third quarter of 2021.

Important!

In order to avoid such situations, you can include in the supply agreement a condition that the supplier undertakes to issue an advance invoice within five calendar days, but no later than the last day of the quarter in which the buyer transferred the advance payment to the supplier. And for violating this condition there is a fine.

HOW TO GET A VAT DEDUCTION FOR RETURNED GOODS?

How to confirm the date of actual receipt of an advance invoice?

You need to confirm the receipt of the invoice with an additional document, if possible, “from a third party.” There are several options depending on the situation:

- You can agree with the supplier to send the document by postal or courier service, with a description of the shipment and delivery against signature. This path is suitable for situations where receipt of a document is delayed due to some circumstances on the part of the supplier. For example, the supplier technically does not have time to issue and send an invoice on time. Documents from the service that delivered it will serve as confirmation of the date of receipt of the invoice.

- You can keep a log of incoming documents and record there the date of actual receipt of the invoice. There is an old, but still valid letter from the Federal Tax Service in Moscow dated 08/03/2009 No. 16-15/79275, in which taxpayers are offered exactly this confirmation option. However, it should be remembered that such a journal will have to be created in advance and entries will be made in it for all incoming correspondence. Let us add that to register invoices (incoming and outgoing) there must be another journal. But the presentation of this journal as evidence is not considered by regulatory agencies.

- An invoice can be sent electronically through an EDI operator. Then confirmation of the date of actual receipt can be requested from the EDF operator.

Please note that since the procedure for confirming the date of receipt of an invoice is not established by law, the Ministry of Finance in its clarifications recommends fixing the selected option(s) for confirming the date in the accounting policy.

Check if everything is correct in the accounting policy - 2020 .

Obstacle No. 3 - lack of advance payment amount in the contract

As practice shows, the existence of an agreement in writing (subject to the other conditions provided for in clause 9 of Article 172 of the Tax Code, clause 5.1 of Article 169 of the Tax Code of the Russian Federation) is not a reason for accepting “advance” VAT for deduction. Even if the agreement is concluded in writing and it provides for the transfer of advance payments, but does not specify its size, then, according to local tax inspectors, an “advance” VAT deduction is not allowed. And this despite the fact that in their explanations representatives of the financial and tax departments (Letters of the Federal Tax Service for Moscow dated June 28, 2010 No. 16-15/067490, Ministry of Finance of the Russian Federation dated March 6, 2009 No. 03-07-15/ 39) noted that if an agreement for the supply of goods (performance of work, provision of services), transfer of property rights provides for a condition on advance transfers without indicating the specific amount of such transfers, then VAT should be deducted, calculated based on the amount of the advance actually transferred (based on invoice issued by the seller).

But, unfortunately, the right to an “advance” deduction in such a situation sometimes has to be proven in court (Resolution of the Federal Antimonopoly Service of the North-Western District dated March 29, 2012 No. A52-2320/2011P).

IS A DEDUCTION POSSIBLE ONLY ON THE BASIS OF A CASH RECEIPT?

Results

If an advance is transferred to a supplier in one tax period, and an invoice for the advance is received in the next, you can deduct VAT on the advance in the period when the invoice is actually received. However, this will require fulfilling a number of conditions, the main of which is to confirm the date of actual receipt of the invoice.

Sources: Tax Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.