Form MB-2 (Card for accounting for low-value items)

Organizations that own inventories organize a warehouse accounting system in the company to ensure their safety. This is due to the need to ensure proper control over the safety of valuables, as well as to comply with an important rule reflected in the Federal Law “On Accounting” - every fact of economic life must be documented.

Changes in 2013 allowed Russian enterprises and merchants to use independently developed forms of primary documents. For the most part, subjects of economic relations use the forms contained in the album of a unified “primary” as a basis.

Card MB-2 sample filling

Standard intersectoral form No. MB-2 Approved by Decree of the State Statistics Committee of Russia dated October 30, 1997 No. 71a

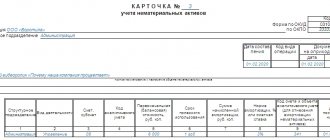

CARD No. accounting for low-value and wear-and-tear items

| Codes | |

| OKUD form | |

| Organization ________________________________________________ | according to OKPO |

| Structural subdivision ____________________________________ |

| Date of preparation | Operation type code | Structural subdivision | Kind of activity | Corresponding account | Recipient's personnel number | |

| account, sub-account | analytical accounting code | |||||

Last name I.

The data in the “Creation Options” tab is divided into three areas:

- General settings - area for entering parameters for creating cards for accounting for small business enterprises

- Accounting - area for entering parameters for writing off the cost of small business enterprises in accounting

- Tax accounting - area for entering parameters for writing off the cost of small business enterprises in tax accounting

The formation of an accounting card for low-value and wearable items is necessary to control the movement of this type of property within the enterprise.

In this material we will learn how Form MB-2 (Card for Accounting for Low-Value Items) is compiled and what requirements and recommendations exist for filling it out.

We will provide step-by-step instructions for filling it out, analyze common errors and answer the most common questions.

Form MB-2 (Card for accounting for low-value items) Organizations that own inventories organize a warehouse accounting system in the company to ensure their safety.

This is due to the need to ensure proper control over the safety of valuables, as well as to comply with an important rule reflected in the Federal Law “On Accounting” - every fact of economic life must be documented. Changes in 2013 allowed Russian enterprises and merchants to use independently developed forms of primary documents.

FORM No. MB-2

A sample card for recording low-value wearable items MB-2 is actually given in Resolution of the State Statistics Committee of Russia dated October 30, 1997 No. 71a.

The above warehouse accounting card is filled out for each individual type (group) of small items, the accounting of which is carried out in quantitative terms.

Let's consider the procedure for filling out the main columns of this accounting form: Column 1 - indicate the name of the IBP, brand (in accordance with the technical passport or similar document), the initial quantity in the warehouse; Column 2 – indicates the nomenclature number of this type (group) of IBP; Column 3 – the dates of issue of the MBP for production are indicated, i.e.

Is it a mandatory requirement to use the MB-2 form in accounting? Or does the organization have the opportunity to develop a sample document on its own? Answer: Companies are allowed to use both an approved form and one developed independently, provided it necessarily contains the necessary document details. Question No. 3.

It is recommended to fill out the document in one copy for storage directly in the organization. The company has the right to appoint any employee to fill it out, but in most cases the document is drawn up by a storekeeper or warehouse manager.

The first section of the document contains:

- card number in accordance with the numbering of the warehouse card file,

- full name of the enterprise (indicating its organizational and legal status),

- OKPO code (All-Russian Classifier of Enterprises and Organizations - the code is contained in the company’s constituent papers),

- date of document preparation.

Then the structural unit in which the product is contained is indicated.

Below is a table where the first column once again includes information (but more precisely) about the structural unit that is the recipient and custodian of these inventory items:

- his name,

- type of activity (storage),

- number (if there are several warehouses),

- specific storage location (rack, cell).

The following are product details:

- brand,

- variety,

- size,

- profile,

- nomenclature number (if such numbering is available, if it is not used, you can put a dash).

Then everything related to units of measurement is entered:

- code according to the Unified Classification of Units of Measurement (EKEI),

- specific name (kilograms, pieces, liters, meters, etc.).

Next, the cost of the material, the rate of its stock in the warehouse, the expiration date (if one is established) and the full name of the supplier are indicated.

The second part of the materials accounting card includes two tables. The first table contains the name of the inventory items, and also, if the composition contains precious stones and metals, their name, type, and other parameters, including data from the product passport.

The second table contains information about the movement of goods and materials:

- date of receipt or release from the warehouse,

- number of the document on the basis of which the products are transferred (according to document flow and in order),

- name of the supplier or consumer,

- accounting unit of issue (name of unit of measurement),

- coming,

- consumption,

- remainder,

- signature of the storekeeper with the date of the transaction performed.

In the last part of the materials accounting card, the employee who filled it out must certify all entered information with his signature with mandatory decoding. The position of the enterprise employee and the date the document was filled out should also be indicated here.

What is the MB-2 form?

If the organization has material assets in the form of equipment or work clothes, we can talk about the presence of low-value property. Despite the low cost, the accountant must ensure control over the issuance of this property to employees.

For this purpose, Goskomstat has developed a primary document in the MB-2 form “Card for recording low-value and rapidly wearing objects.” The document was approved by Resolution No. 71a of October 30, 1997. and has a form in accordance with the OKUD 0320001 classifier.

We recommend that you familiarize yourself with an example of the MB-2 form.

Important! The accounting card is used to reflect the fact of transfer of low-value and rapidly wearing property to a company employee for long-term use.

Rates

This album includes unified forms of primary accounting documentation for accounting for low-value and wear-and-tear items. The forms contain brief instructions on their use and completion. Recommended formats for primary accounting documentation forms are indicated in the list of forms.

Form MB-2. Card for recording low-value and wearing-out items The card for recording low-value and wearing-out items in the MB-2 form is used to record low-value and wear-out items issued against receipt to an employee for long-term use. Code on the OKUD form 0320001. Filled out in one copy by the storekeeper for each employee who received these items, or issued to financially responsible persons. To reflect the entry and movement of property that, according to accounting rules, has been transferred to fixed assets from the category of low-value and wearable items, unified forms of primary accounting documentation N MB-2, N MB-4, N MB-7, N MB-8 can be used.

Form MB-4. The act of disposal of low-value and wear-out items The act of disposal of low-value and wear-out items in the MB-4 form is used to document the breakdown and loss of low-value and wear-out items. The act is drawn up in two copies. One copy remains in the structural unit, and the second is sent to the accounting department. Code according to the OKUD form 0320002. Upon presentation of the disposal certificate, the employee is given a suitable one in exchange for an unusable or lost item. A corresponding entry is made about this in the record card for low-value and wearable items (Form N MB-2). Acts of disposal are subsequently attached to acts of write-off (Form N MB-8). To reflect the entry and movement of property that, according to the accounting rules, has become part of fixed assets from the category of low-value and wearable items, unified forms of primary accounting documentation N MB-2, N MB-4, N MB-7, N MB-8 can be used.

Form MB-7. Record sheet for the issue of workwear, safety shoes and safety devices The record sheet for the issue of workwear, safety shoes and safety devices in the MB-7 form is used to record the issue of workwear, safety shoes and safety devices to employees for individual use. (Used for automated processing of accounting data.) Code according to the OKUD form 0320003. Filled out in duplicate by the storekeeper of the structural unit. One copy is transferred to the accounting department, the second remains with the storekeeper. To reflect the entry and movement of property that, according to accounting rules, has been transferred to fixed assets from the category of low-value and wearable items, unified forms of primary accounting documentation N MB-2, N MB-4, N MB-7, N MB-8 can be used.

Form MB-8. Act on write-off of low-value and wear-out items An act on write-off of low-value and wear-out items in the MB-8 form is used to formalize the write-off of low-value and wear-out items that are worn out and unsuitable for further use. Code according to the OKUD form 0320004. Drawed up in one copy by the commission. After the written-off items are handed over to the scrap storage room, the act with a receipt from the storekeeper is submitted to the accounting department. For different types of low-value and high-wear items, write-off acts are drawn up separately. To reflect the entry and movement of property that, according to accounting rules, has been transferred to fixed assets from the category of low-value and wearable items, unified forms of primary accounting documentation N MB-2, N MB-4, N MB-7, N MB-8 can be used.

Step-by-step instructions for filling out

The unified card form can be divided into several parts, each of which must contain the information necessary for disclosure, namely:

- Document header – includes information about the organization;

- The table required to reflect the data on the document being compiled and the accounting accounts, let's call it Table 1;

- Information about the employee accepting valuables for use;

- A table used to disclose information directly about low-value property (Table 2).

Let's take a closer look at all the components of the MB-2 accounting card.

- Document header:

- Company name;

- Division name.

- Table 1:

- Date of drawing up the card;

- Operation type code;

- Subdivision;

- Kind of activity;

- Accounting accounts (correspondent account and analytical accounting account);

- Personnel number of the employee of the organization - the recipient of the valuables.

- Information about the company employee:

- Surname and initials;

- Profession;

- Position held in the organization.

- Table 2:

- The item to be transferred (name of the valuables and brief characteristics, nomenclature number accepted by the company);

- Information on the number of items issued, date of transfer and signature of the employee;

- Information about low-value property returned to the organization by the employee (quantity, date, signature of the receiving storekeeper of the company);

- Document – the basis for disposal of objects (number and date);

- Service life of low-value objects;

- Number of the technical passport of the property.

The completed document must be confirmed by the person who compiled it. For this purpose, the employee authorized to fill out puts his signature and transcript on the MB-2 card, and also indicates the position and date of preparation of the document.

We recommend that you familiarize yourself with an example of filling out the MB-2 form.

Important! The main meaning of the MB-2 card is to record the movement of objects during their use and reflect these actions in accounting.

Typical mistakes when drafting a document

Despite the fact that the accounting card does not belong to the category of documents difficult to fill out, some violations still occur in the work of responsible persons.

Let's look at the table for typical violations observed when filling out a low-value property registration card.

| p/p | Typical violations when filling out an IBP registration card | |

| Error | Adjustment methods | |

| 1 | The number of transferred valuables is incorrectly indicated on the low-value items registration card. | If this violation is not detected in a timely manner, a discrepancy between the actual amount of valuables and the accounting amount may occur. As a result, it is extremely important to detect errors in filling out in a timely manner and eliminate them. The incorrect cell value should be crossed out and the correct quantity indicated next to it. The correction must be certified with the signature of the employee of the organization responsible for filling it out, as well as with the phrase “believe the correction.” |

| 2 | The document in the MB-2 form does not reflect data on objects from the technical passport, such as service life and passport number. | Companies are allowed to use both standardized and independently developed sample forms, provided they contain the required details. Technical information is classified as mandatory for disclosure. Accordingly, regardless of the form of data presentation, it is necessary to indicate this information in the document. |

| 3 | The MB-2 registration card does not contain the signature of the person responsible for filling out the form. | The employee filling out the document is essentially the financially responsible person who transfers the IBP. Thus, if discrepancies are identified, responsibility can be assigned to the authorized employee. If there is no signature on the document, recovering the missing items will be problematic. |