When is it issued?

As a rule, only the company’s accountant is responsible for filling out the accounting certificate form . Senior management is not involved in this process.

Basically, this certificate is necessary when the rest of the “primary” data has already been collected, but for accounting, an additional calculation of some indicator is needed. In practice this could be:

- accounting certificate - calculation of interest, including on a loan;

- accounting certificate - calculation of benefits (for pregnancy and childbirth , etc.);

- accounting certificate - daily allowance calculation;

- accounting certificate calculating compensation for delayed wages (Article 236 of the Labor Code of the Russian Federation);

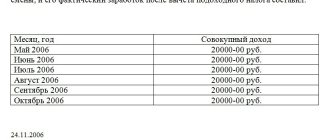

- accounting certificate - income tax calculation;

- accounting certificate calculating 5 percent VAT (clause 4 of Article 170 of the Tax Code of the Russian Federation);

- accounting certificate - calculation of penalties;

- accounting certificate - calculation of cost distribution;

- accounting certificate - calculation for write-off of gasoline;

- accounting certificate-calculation as an appendix to the certificate of incapacity for work , etc.

What you need to know when using different forms and samples of accounting statements

You should remember the following subtleties:

- Does not replace the document that must be drawn up by the transaction partners together. Therefore, it makes sense to record some operations in the certificate only for internal purposes.

- The certificate usually only confirms the information already provided in the internal accounting system. Therefore, a specialist must distinguish how to prepare a sample accounting certificate :

Such cases include drawing up an act of acceptance of goods received without documents. The tax office will consider that the submitted sample accounting certificate does not have a legal basis. As a result, expenses may not be recognized. It is impossible to take them into account when calculating tax. And challenging such a decision can be difficult.

- as a “primary”;

- for completely different purposes (informational, etc.). For example, to record a business transaction in a document that can become evidence in legal proceedings.

- In difficult situations, the accountant runs the risk of getting confused in the corrections. To prevent this from happening, we recommend including as much information as possible in the text of the certificate and attaching copies of settlement documents, as well as incorrectly completed documents.

What is the form of an accounting statement?

sample accounting certificate established by law . This means that for the accounting policy, it is advisable to develop its form independently, taking into account all the features of the enterprise and its document flow. And to approve it by a separate order of the head of the enterprise.

Also see “Order on approval of accounting policies for 2021: sample.”

If you are in doubt about how to correctly draw up a sample accounting certificate , be guided by Article 9 of the Law

- Company name;

- the essence of the operation and the calculation for it;

- Date of preparation;

- FULL NAME. responsible persons.

Also see “Details of accounting documents: basic and mandatory”.

The following is an example of an accounting statement :

On our portal, you can download the accounting certificate, if it suits you, here.

Also see “Accounting statement: how to draw it up correctly.”

Is it possible to make corrections to the accounting certificate?

If an error is found in a completed accounting statement, but it is not possible to write or print a new document and collect the necessary signatures, it can be corrected. To do this, you need to follow some rules:

- first, incorrect data must be crossed out with ink with the greatest care

- then you need to write corrective information on top of the crossed out data

- Finally, the surname, initials and position of the employee who made the corrections are indicated, his signature and the date of the correction are placed

Primary documents for accounting

Primary accounting documents are appropriately compiled and executed documentation that confirms the implementation of facts of economic activity by an enterprise. A fact is an event, operation or transaction that affects the cash flow of a company, its financial condition or the economic results of its work.

Primary accounting documents confirm the completion of such transactions and are formalized when they are carried out. In addition to their use for accounting purposes, they are also necessary for tax accounting, since they are the basis for recognizing expenses incurred by the company and allow the tax base to be correctly determined. Accounting documents are also used in litigation or disputes with counterparties and clients.

Law of December 6, 2011 N 402-FZ “On Accounting” prohibits the acceptance of documents for accounting if they document facts of economic life that did not take place in reality. This primarily applies to imaginary and feigned transactions.

General requirements for the preparation of primary accounting documents

There is no exhaustive list of primary accounting documents established by law that are required to be maintained by business entities. The enterprise itself can determine their volumes, types and forms - it depends on the purposes of their use. Only “primary” forms for cash transactions are regulated.

An enterprise can use standard forms, the presence of which is provided, among other things, in accounting programs, or create accounting documents independently. However, it should be remembered that for this documentation the law establishes a set of necessary details, without which they will not be considered correctly executed. These include:

- title of the document, date of its preparation;

- Business name;

- content of the fact of economic activity;

- quantitative (pieces, pack, etc.) and (or) monetary expression (rubles) of the transaction;

- Full name and signatures of representatives of the counterparties who carried out the transaction, their positions and other identification data.

The forms of primary accounting documents that the enterprise will use in its activities are determined by the head of the enterprise and approved by his order.

The primary accounting document must be drawn up when a fact of economic life is committed, and if this is not possible, immediately after its completion.

The primary accounting document can be drawn up:

- on paper

- in the form of an electronic document signed with an electronic signature.

The legislation of the Russian Federation or any agreement may provide for the submission of the primary accounting document to the counterparty or to a government agency on paper. In this case, the organization is obliged, at the request of another person, to make copies on paper of a copy of the primary accounting document compiled in the form of an electronic document.

The procedure for making corrections to primary accounting documents is also specified in the legislation. Thus, when making a correction, the date of correction is indicated in the primary accounting document, the signatures of the persons who compiled the document in which the correction was made are affixed, and their surnames and initials are indicated. Other details necessary to identify these persons may also be indicated.

The list of primary accounting documents required to accompany a particular business transaction depends on its type and may change. Mostly, its preparation and formation is carried out by the supplier of the product or service. Therefore, in transactions where your company is the buyer, and therefore a legal entity that bears the costs, pay attention to checking the correctness of the preparation of primary documentation by your supplier.

Types of primary documents in accounting

As mentioned earlier, the facts of the company’s economic activity are recorded through the formation of primary documentation. In this regard, the following types are distinguished:

- by volume of recorded data – primary, consolidated;

- by purpose - accounting, directive, executive, BSO (strict reporting forms);

- by method of displaying information - consolidated, one-time;

- depending on the place of compilation - external, internal;

- according to the method of formation - in paper form, electronic.

Primary documentation in accounting: list

Working with the “primary” is one of the main tasks of accounting, since the correctness of documentation is the basis for the legality of recognizing expenses and making deductions, as well as the basis for the correct formation of the tax base. Most often, accounting works with the following primary documents:

- business agreement with a counterparty*;

- invoice* (form approved by Decree of the Government of the Russian Federation No. 1137 of December 26, 2011);

- invoice for payment* (the form is not approved by law);

- commodity and consignment note (TTN), universal transfer document (UDD);

- expense reports;

- payment documentation confirming the fact of payment. It includes BSO, bank payment (demands and orders) and cash (receipt and expense orders) documents;

- accounting certificates;

- certificate of work performed (services provided) between the customer and the contractor (mostly there are no unified forms, however, for example, a certificate of construction work can be taken from the form approved by the Resolution of the State Statistics Committee of the Russian Federation No. 100 dated November 11, 1999, or you can create it yourself);

- documents on the wage fund and settlements with personnel;

- fixed asset accounting documents;

- waybills and other primary information.

*Documents such as, for example, a business contract, an invoice and an invoice for payment are not independent primary accounting documents.

Thus, in an agreement with a counterparty, agreements between the parties are fixed - the subject of the transaction, rights and obligations, terms of payment and delivery, sanctions for violating the provisions of the agreement, etc. However, without confirming acts (invoices, payment orders, etc.), the agreement itself is in the formation accounting transactions will not be involved.

The invoice reflects the amount at which the seller values his product (service). If it is not paid by the buyer, the fact of sale of the goods will not be reflected in the list of accounting transactions. Therefore, the invoice is more of an annex to the contract than a separate primary accounting document.

An invoice is drawn up for tax purposes - on its basis, the buyer counterparty receives the right to deduct the amount of VAT presented by the supplier counterparty. However, as in the case of a contract, the absence of other primary accounting documents confirming the transaction does not provide grounds for recognizing costs for a specific transaction and reflecting them in accounting.

It is important to remember that the primary documents used in accounting are also part of the tax and management accounting system.

Primary documents by stages of a business operation (transaction)

Each transaction of an enterprise is carried out in several stages. At the first stage, counterparties negotiate and come to an agreement on cooperation. The result of consensus is the signing of a business agreement, which records the agreements reached by the parties, and the issuance of an invoice for payment.

It is considered correct to formalize each transaction in a separate agreement. However, more often companies sign a general agreement with regular counterparties for similar operations. A number of transactions do not require a written agreement. So, for example, a retail sales contract is concluded from the moment the check is delivered to the consumer.

An invoice is an accounting document in which the seller offers his price for the product. In addition to the cost, it indicates payment terms, delivery procedures and other necessary conditions. However, this document does not give the supplier the right to demand payment from the buyer - it only fixes the price of the product or service. The buyer's consent is acceptance of the invoice.

The second stage is payments under the agreement. Accounting documents, depending on the type of payment, will be:

- cash receipts, sales receipts, receipt orders, etc. — for cash payments;

- statements from the current account, payment slips certified by the servicing bank - when paying by bank transfer (acquiring, settlements through payment systems, electronic payments, etc.).

The final stage of the transaction is the delivery (receipt) of products (services). Documentary confirmation of these facts is mandatory. Otherwise, the tax office will not recognize such a transaction as having taken place, and the tax base may be changed not in favor of the enterprise. At this stage the following will be completed:

- sales receipt - issued when selling goods at retail;

- commodity, or consignment note - confirms the fact of sale of goods under the supply agreement and is the basis for its subsequent receipt by the counterparty-buyer, prepared in 2 copies, one for each of the parties. Signed by authorized persons of the parties responsible for the delivery and receipt of goods;

- act of completion of work is a two-sided primary accounting document. In it, representatives of the parties testify to the compliance of the performed scope of work (services provided) with the contractual conditions and the very fact of the transaction.

Depending on the agreements, the second and third stages may change places, for example, in the case of delivery of goods on deferred payment terms.

Transfer of primary accounting documents to the accounting department

Accounting operations, incl. recognition of costs, sales, etc., is carried out by the accountant solely on the basis of primary accounting documents provided to the accounting department by the persons responsible for their preparation. It is these persons, and not the accountant, who are responsible for the compliance of primary accounting documents with accomplished facts of economic life. Therefore, employees of the enterprise who are responsible for conducting business transactions and working with primary documentation should submit them to the accounting department in a timely manner. The approval of document flow procedures in the company by order of the head and the development of memos for staff helps to establish document flow. The accountant, in turn, has the right to demand in writing that responsible persons comply with the established procedure for documenting the facts of economic life and submitting documents (information) necessary for maintaining accounting records. And the persons responsible for the preparation of primary documents are obliged to comply with the requirements of the accountant.

Shelf life

As a general rule, all primary records must be kept in the accounting department for at least five years after the reporting year. Specific periods for storing documents are established by the Federal Archives Agency. During the established storage period, the tax office has the right to request primary documents for verification from you or your counterparty. The current storage periods for accounting, personnel and other documentation can be found in Order of the Federal Archival Agency of December 20, 2021 N 236.

Sanctions for the absence of a “primary”

Violation of the rules for accounting for income and expenses, as well as the lack of primary accounting documents, is fraught with the onset of:

- liability according to Art. 120 Tax Code of the Russian Federation. The primary violation is punishable by a fine of 10 thousand rubles. Repeated violations detected in several periods are fraught with a fine of 30 thousand rubles. If such actions of the company led to a decrease in the tax base, it will be fined 20% of the amount of unpaid tax payments, but not less than 40 thousand rubles;

- liability under Art. 15.11 Code of Administrative Offenses of the Russian Federation - collection of a fine from officials in the amount of 5 thousand rubles. up to 10 thousand rubles for gross violation of accounting requirements.

Structure: how to write a sample accounting statement

Regardless of its purpose, the document must be executed correctly, since it plays the role of a primary one. Then there will be no unnecessary questions from the tax inspectorate. We recommend using an in-house template, since the legislation of the Russian Federation does not provide for a mandatory accounting certificate form .

The procedure for preparing this document consists of 3 stages:

- Creating a “header” and specifying the following data:

- information about what has changed;

- previous performance;

- correct method of calculation.

The following is an example of an accounting statement with the corresponding text:

| “Economist of LLC “Guru” N.V. Kurnosova made a technical error when calculating depreciation on fixed assets. For 2021, the amount was 21,000 rubles, while it was erroneously indicated as 22,500 rubles. Detailed calculation: ……. On February 1, 2021, N.V. Kurnosova corrected the error by posting Dt 44 Kt 02 - 21,000 rubles. Corrections were made by recording Dt 44 Kt 02 – 1500 rubles. (reverse)" |

- identification of persons;

- confirmation of the need to perform a business transaction.

Also see “Details of accounting documents: basic and mandatory”.

As was said, the company’s management has the right to independently develop and approve by order a sample certificate in order to use it to solve its business problems. At the same time, it is included in the accounting policy of the enterprise.

You can take as a basis accounting certificate 0504833 , which was developed by the Ministry of Finance for public sector institutions (order No. 52n of 2015).

Typically, this document is drawn up in electronic form, taking into account standard design requirements: no typos, filling out all details, exact names of organizations, etc. It is important not to make mistakes when entering dates.

On our website for accounting information you can use the following link.

Such certificates may contain so-called red reversals - postings with a negative number. They serve, for example, for:

- bug fixes;

- write-off of trade margins;

- adjustments to indicators of material and production costs.

Below is a sample of filling out accounting certificate 0504833 .

Pena is...

According to Art. 75 of the Tax Code of the Russian Federation, the penalty is the amount of money that the company is obliged to transfer to the budget if it fails to pay taxes, fees or insurance premiums on time. Paying penalties is an obligation, not a right, of the taxpayer. It is established in the event that an economic entity has violated its obligation to transfer payments to the budget within the time limits established by law.

If a payment arrear is discovered by the tax inspectorate, it will issue a demand for payment of the debt and penalties on it. If the taxpayer himself identifies this problem, he can independently calculate the amount of the penalty and pay it along with the debt, without waiting for a request from the Federal Tax Service.

Important! When transferring penalties, it is necessary to direct it to a separate KBK intended specifically for such payments for a specific tax or insurance premium.

What is an accounting certificate and why is it needed?

All people make mistakes, accountants are no exception. In order to correct errors, as well as to reflect non-standard business transactions in accounting, you can use an accounting certificate.

An accounting certificate is an official document that reflects adjustments to various registers of the chart of accounts in the event of an error, as well as calculations for non-standard business transactions.

How to write a reference for an employee? A sample and step-by-step instructions are contained in the publication at the link.

Thus, an accounting certificate is necessary in order to make changes to the reporting , as well as in order to reflect specific business transactions in accounting (separate accounting of activities, entertainment expenses).

Accounting certificate of debt for the court: sample

This document can be drawn up in a very general form with references to background data that the form wants to prove in court. It is not at all necessary to refer in the certificate to the fact that it is issued specifically for judicial purposes.

The following is a sample of writing an accounting statement about a “receivable”, which often has to be “knocked out” from the counterparty through the court.

| LIMITED LIABILITY COMPANY "GURU" Address: 105318, Moscow, st. Gogolya, 8, office 15. TIN 7722123456, KPP 772201001 Moscow February 06, 2021 Accounting statement No. 3-s As a result of the inventory of settlements with counterparties on February 06, 2021, receivables from Buben LLC were identified (TIN 7719456789, KPP 771901001, address: Moscow, Kvasovaya St., 9, building 6), for which the statute of limitations has not expired (inventory act dated 02/06/2017 No. 22-inv). This debt arose under the goods supply agreement No. 12/7 dated October 22, 2016. The amount of debt is 500,000 (five hundred thousand) rubles 00 kopecks. The payment deadline under the agreement is December 31, 2016 (inclusive). General Director ______________ /V.V. Krasnov/ Chief Accountant ______________ /E.A. Shirokova/ |

Read also

03.02.2017