Personal income tax

Compensation payments (compensation for the use of a car and the amount of reimbursement of expenses associated with its use) are not subject to personal income tax within the limits established by current legislation (clause 3 of article 217 of the Tax Code of the Russian Federation, article 188 of the Labor Code of the Russian Federation).

Situation: is an organization obliged to apply the norms provided for by Decree of the Government of the Russian Federation of February 8, 2002 No. 92 when calculating personal income tax on compensation for the use of a personal car?

Answer: no, you are not obliged to.

All types of compensation payments (within the limits of the norms) established in accordance with the law and related to the performance of labor duties are exempt from personal income tax (clause 3 of Article 217 of the Tax Code of the Russian Federation). Chapter 23 of the Tax Code of the Russian Federation does not establish compensation standards for the use of an employee’s personal car. Therefore, in this situation, the organization should be guided by the provisions of the Labor Code of the Russian Federation.

Article 188 of the Labor Code of the Russian Federation, which obliges the organization to pay compensation to employees for the use of personal property, does not contain any restrictions regarding their amount. It only says that the amount of reimbursement for expenses associated with the use of an employee’s property is determined by agreement of the parties to the employment contract. Thus, compensation for the use of an employee’s personal car does not need to be subject to personal income tax up to the amount specified in the written agreement between the employee and the employer.

In this case, the organization must document the validity of the appointment and the amount of compensation for the use of the employee’s personal car, as well as the fact that he incurred expenses. In particular, you need to have the following documents:

- confirming the organization’s need to use an employee’s car;

- evidence that the car belongs to this employee (for example, a copy of the vehicle passport (PTS));

- justifying the calculation of the amount of compensation (for example, an order assigning compensation). Determine the amount of compensation for each employee based on the brand and price of fuel per liter, fuel consumption per 100 km, number of working days in a month, vehicle mileage;

- confirming the actual use of the car in the interests of the organization (for example, orders, waybills);

- expense reports, cash receipts, etc.

Similar clarifications are contained in letters of the Ministry of Finance of Russia dated June 28, 2012 No. 03-03-06/1/326, dated March 24, 2010 No. 03-04-06/6-47, dated December 23, 2009 No. 03- 04-07-01/387 (brought to the attention of the tax inspectorates by letter of the Federal Tax Service of Russia dated January 27, 2010 No. MN-17-3/15).

This approach is confirmed by arbitration practice (see, for example, resolutions of the Presidium of the Supreme Arbitration Court of the Russian Federation dated January 30, 2007 No. 10627/06, FAS of the Ural District dated March 18, 2008 No. Ф09-511/08-С2, North Caucasus District dated 17 April 2007 No. F08-4799/2006, Volga District dated August 19, 2008 No. A06-6865/07, dated April 10, 2007 No. A72-7503/06-7/283, Northwestern District dated January 23 2006 No. A26-6101/2005-210).

Situation: is it necessary to withhold personal income tax from the amount of compensation payments (compensation for the use of a car and the amount of reimbursement for expenses associated with its use) if an employee drives a car that is registered to another person?

Answer: yes, it is necessary.

All types of compensation payments established by law, related, in particular, to the performance of work duties by an employee (clause 3 of Article 217 of the Tax Code of the Russian Federation) are exempt from personal income tax.

According to Article 188 of the Labor Code of the Russian Federation, compensation is paid to the employee for the use of a personal car in the interests of the employer, and expenses associated with its use are also reimbursed (in the amount established by agreement of the parties to the employment contract). Compensation payments for the use of property that does not belong to the employee are not provided for by the Labor Code of the Russian Federation.

Thus, the compensation payment is considered legally established and, accordingly, is not subject to personal income tax only if the car is the personal property of the employee. This, in turn, implies that the car is owned by the person. If an employee drives a car registered to another person, then such a vehicle is not considered his personal property, and the amount of compensation payment is subject to personal income tax on a general basis.

Similar clarifications are contained in letters of the Ministry of Finance of Russia dated May 3, 2012 No. 03-03-06/2/49, dated February 21, 2012 No. 03-04-06/3-42, dated September 21, 2011 No. 03- 04-06/6-228 and the Federal Tax Service of Russia dated October 25, 2012 No. ED-4-3/18123.

However, there is an exception to this order. It concerns the case when the car is jointly owned by an employee and another person. This situation may arise, for example, if the car is joint property of the spouses. As a general rule, property acquired by spouses during marriage is their joint property, unless otherwise established by agreement between them (Clause 1, Article 256 of the Civil Code of the Russian Federation, Article 34 of the Family Code of the Russian Federation). And in this case, the employee driving the car, which is jointly owned, is one of the owners of the car, that is, the car is considered his personal property. Accordingly, the amount of compensation payment for the use of the car is exempt from personal income tax on the basis of paragraph 3 of Article 217 of the Tax Code of the Russian Federation. Such clarifications are contained in the letter of the Ministry of Finance of Russia dated May 3, 2012 No. 03-03-06/2/49.

Advice: there are arguments in favor of organizations not withholding personal income tax from the amount of compensation payments if an employee drives a car registered to another person, and in other cases. They are as follows.

The concept of personal property is absent in the legislation. Therefore, the personal property of an employee can be recognized as property that belongs to him on any legal basis. A person (organization) has the right to issue a power of attorney to an employee to drive a car. A power of attorney is a written authority issued by one person to another for representation before third parties (Clause 1 of Article 185 of the Civil Code of the Russian Federation). Therefore, it can be recognized as the legal basis for ownership of the vehicle. That is, a car that a person uses by proxy can be considered his personal property. Since the employee uses the car in the interests of the organization, compensation payments for the operation of a car driven by proxy are not subject to personal income tax (clause 3 of Article 217 of the Tax Code of the Russian Federation). The legitimacy of this approach is also confirmed by arbitration practice (see, for example, the resolution of the Federal Antimonopoly Service of the Ural District dated April 22, 2014 No. F09-1388/14).

In this case, the organization must document the validity of the appointment and the amount of compensation payments for the use of the employee’s personal car, as well as the fact that the employee incurred expenses.

Following this position in practice, check whether the payments made to the employee are truly compensation. For example, this condition is not met when the power of attorney is issued to the employee by the employing organization, which is the owner of the car and bears the costs of its maintenance and operation. If the organization makes any payments to the employee for the use of the car, then personal income tax must be withheld from these payments. This is explained by the fact that the employee is not entitled to compensation at all, since he does not incur any expenses. This conclusion follows from the totality of the provisions of Articles 164 and 188 of the Labor Code of the Russian Federation. Accordingly, payments to the employee will not be considered compensation.

Reimbursement of expenses for personal transport and insurance premiums

Note!

The Presidium of the Supreme Court of the Russian Federation, in paragraph 3 of the Review dated October 21, 2015, summarized the judicial practice and came to a very important general conclusion.

The receipt by an individual of benefits in the form of goods (work, services) and property rights paid for him is not subject to personal income tax, if the provision of such benefits is determined, first of all, by the interests of the person transferring (paying for) them, and not by the purpose of primarily satisfying the personal needs of the citizen. The mere fact that as a result of providing a citizen with the benefits paid for him, the personal needs of the individual are satisfied to a certain extent, is not sufficient to conclude that taxable income in kind has arisen. 217 Tax Code of the Russian Federation. Provisions expressly providing for the exemption from taxation of amounts of compensation by the employer in accordance with its

Insurance premiums

The standards established by law must also be taken into account when calculating:

- contributions to compulsory pension (social, medical) insurance;

- contributions for insurance against accidents and occupational diseases.

Within their limits, compensation for the use of an employee’s personal car is not subject to insurance premiums (subparagraph “and” paragraph 2, part 1, article 9 of the Law of July 24, 2009 No. 212-FZ, paragraph 10, subparagraph 2, paragraph 1 of Art. 20.2 of the Law of July 24, 1998 No. 125-FZ).

The norms provided for by Decree of the Government of the Russian Federation of February 8, 2002 No. 92 are intended only for calculating income tax. Therefore, in order to calculate contributions, apply the standards established in accordance with Article 188 of the Labor Code of the Russian Federation. Namely: the amount of compensation agreed upon by the parties to the employment (collective) agreement. Within these limits, insurance premiums do not need to be charged on compensation for the use of an employee’s personal car. In this case, the amount of compensation will not be subject to contributions only if the use of the car is related to the employee’s performance of his job duties (traveling nature of work, official purposes) (subclause “and” clause 2, part 1, article 9 of the Law of July 24, 2009 No. 212-FZ, paragraph 10, sub-clause 2, clause 1, article 20.2 of the Law of July 24, 1998 No. 125-FZ).

A similar point of view is reflected in the letter of the Ministry of Health and Social Development of Russia dated March 12, 2010 No. 550-19, paragraph 3 of the letter of the Ministry of Health and Social Development of Russia dated August 6, 2010 No. 2538-19.

Situation: is it necessary to charge insurance premiums on the amount of compensation for the use of a car and the amount of reimbursement of expenses associated with this if the employee does not drive his own car?

Answer: yes, it is necessary.

Compensation for the use of a car and related expenses is not subject to insurance premiums only when the car is owned by the employee. That is, the title and vehicle registration certificate are issued to him, and not to someone else. And the employee submitted copies of such documents to the accounting department.

The fact is that all types of compensation payments established by law, related, in particular, to the employee’s performance of work duties, are exempt from insurance contributions (sub-clause “and” clause 2, part 1, article 9 of the Law of July 24, 2009 No. 212 -FZ, paragraph 10 subparagraph 2 clause 1 article 20.2 of the Law of July 24, 1998 No. 125-FZ).

The procedure for paying compensation for the use of employee property (including a car) is established by Article 188 of the Labor Code of the Russian Federation. It says here that for the use of a personal car in the interests of the employer, the employee is paid compensation, and the expenses associated with its use are also reimbursed. The amount of such compensation is specified in the employment contract. But compensation payments for the use of property that does not belong to the employee are not provided for by the Labor Code.

It turns out that the compensation payment is considered legally established and, accordingly, is not subject to insurance premiums only if the car is the personal property of the employee. This, in turn, implies that the car is owned by a person (including jointly, for example, with a spouse), which is documented (for example, copies of the title and vehicle registration certificate).

When an employee drives a car that is registered to another person, such a vehicle is not considered his personal property. This means that the amount of compensation payment is subject to insurance premiums.

Similar conclusions follow from the letter of the Ministry of Labor of Russia dated February 26, 2014 No. 17-3/B-92 and paragraph 3 of the letter of the Ministry of Health and Social Development of Russia dated August 6, 2010 No. 2538-19.

Advice: insurance premiums may not be charged on the amount of compensation paid, even if the employee drives a car registered to another person. But in this case, be prepared for disputes with inspectors. The following arguments will help here.

The concept of “personal property” is absent in the legislation. Therefore, any property that belongs to a person on any legal basis can be recognized as such. Such a basis may also be a power of attorney to drive a car. After all, this is a document that confirms in writing a person’s authority in relation to a thing (clause 1 of Article 185 of the Civil Code of the Russian Federation). That is, the car transferred to the employee by proxy is actually in his possession and use.

And since the employee uses the car in the interests of the organization, compensation payments for operating the car under a power of attorney are not subject to insurance premiums (subclause “and” clause 2, part 1, article 9 of the Law of July 24, 2009 No. 212-FZ, paragraph 10 subparagraph 2, paragraph 1, article 20.2 of the Law of July 24, 1998 No. 125-FZ).

The legitimacy of this position is confirmed by arbitration practice (see, for example, the ruling of the Supreme Arbitration Court of the Russian Federation dated January 24, 2014 No. VAS-4/14, the resolution of the Federal Antimonopoly Service of the Ural District dated September 23, 2013 No. F09-9554/13, dated May 29, 2013 No. F09-4358/13, Volga District dated October 9, 2012 No. A12-2881/2012).

In this case, the organization must document the amount of compensation payments, their validity, as well as the fact that the employee actually incurred expenses.

How can you document the use of a personal car?

In order to protect both the organization and the employee when using an employee’s personal car, the relationship must be formalized in writing. You can do this in the following ways:

| Employment contract | Additional agreement to the employment contract | Lease contract |

| When concluding an employment contract, it is necessary to specify a condition on the payment of compensation. Moreover, compensation occurs only if the employee’s car is used of his own free will, with the permission and in the interests of the employer, and the amount of the compensation payment is directly indicated in the employment contract. An indication that payment of compensation must be fixed in writing is contained in the appeal ruling of the Perm Court dated August 16, 2017 in case No. 33-8949/2017 | If an employment contract has already been concluded, and the use of the car for business purposes began later, then an additional agreement is drawn up, which spells out what exactly, how much and when the employee will receive in the form of compensation. | The company and the employee can enter into a rental agreement for a car without a crew. The amount of remuneration to the employee in this case is agreed upon in advance. As a general rule, the organization bears all costs for using the car. The only condition is that all costs must be justified and supported by documents. It should be remembered that, according to Part 1 of Article 5 of Law No. 125-FZ of July 24, 2008, the amount of compensation is not subject to insurance contributions, but personal income tax will have to be transferred from these amounts. It is advisable to set the rental amount depending on the intensity of work. If an employee goes on vacation or sick leave, the lease agreement continues to be valid. |

Confirmation of expenses in the case of fixing the possibility of compensation in an employment contract or an additional agreement to it is made according to the provided documents for expenses. In the case of renting a car, a contract and an act of acceptance and transfer of the car are drawn up once . This procedure is enshrined in letter of the Ministry of Finance No. 03-03-06/4/118 dated October 13, 2011.

Income tax

Compensation for the use of an employee’s personal car for business trips will reduce taxable profit only within the limits established by Decree of the Government of the Russian Federation of February 8, 2002 No. 92. Compensation within the limits is included in other expenses associated with production and sales (subclause 11 Clause 1 of Article 264 of the Tax Code of the Russian Federation).

Cost standards for payment of compensation are established depending on the engine size of a passenger car. If the engine capacity is less than 2000 cc. cm (inclusive), then the compensation rate will be 1200 rubles. per month. If the engine capacity is over 2000 cc. cm – 1500 rub. per month. For motorcycles, the monthly compensation rate is set at 600 rubles.

Amounts of compensation exceeding the standards established by Decree of the Government of the Russian Federation of February 8, 2002 No. 92 cannot be included in expenses. Consequently, they do not reduce taxable profit (clause 38, article 270 of the Tax Code of the Russian Federation). In accounting, the amount of compensation is recognized as expenses in full. Because of this, a permanent difference and a permanent tax liability will arise (clauses 4 and 7 of PBU 18/02).

Situation: is it possible to take into account compensation for the use of an employee’s personal truck (minibus) when calculating income tax?

Answer: yes, you can.

For the use of an employee’s personal property for official purposes, the organization must pay him compensation (Article 188 of the Labor Code of the Russian Federation). This rule fully applies not only to cars, but also to trucks.

In relation to passenger cars, compensation for their use for business purposes is taken into account when calculating income tax within the limits of the norms.

The costs of paying compensation for the use of personal trucks (minibuses) of employees are not provided for in Chapter 25 of the Tax Code of the Russian Federation.

However, the list of other expenses associated with production and (or) sales is open (Article 264 of the Tax Code of the Russian Federation). Therefore, if all necessary conditions are met, compensation to employees for the use of their personal trucks (minibuses) for business purposes can be taken into account when calculating income tax in full (subclause 49, clause 1, article 264 of the Tax Code of the Russian Federation). That is, in the amounts agreed upon by the parties to the labor (collective) agreement (Article 188 of the Labor Code of the Russian Federation).

This conclusion follows from letters of the Ministry of Finance of Russia dated March 18, 2010 No. 03-03-06/1/150, dated August 15, 2005 No. 03-03-02/61.

It should be noted that with regard to compensation for the use of a minibus, the Russian Ministry of Finance indicated that subparagraph 11 of paragraph 1 of Article 264 of the Tax Code of the Russian Federation allows only compensation for the use of an employee’s personal car to be included in expenses (letter of the Russian Ministry of Finance dated April 24, 2008 No. 03 -03-06/1/293). At the same time, the letter does not say anything about the possibility of taking into account compensation for the use of a minibus in expenses on the basis of subparagraph 49 of paragraph 1 of Article 264 of the Tax Code of the Russian Federation.

However, in connection with the release of later clarifications from the financial department, which allows compensation for the use of modes of transport other than passenger cars to be taken into account in expenses (letter dated March 18, 2010 No. 03-03-06/1/150), when attributing them to compensation expenses for the use of a minibus, the organization can be guided by them.

Advice: when using an employee’s personal car, the organization also has the right to enter into a vehicle rental agreement with him. In this case, instead of compensation, the employee will need to pay rent. It will completely reduce taxable profit (subclause 10, clause 1, article 264 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated April 24, 2008 No. 03-03-06/1/293).

Situation: is it possible to take into account the costs of purchasing fuel and lubricants when taxing profits if the organization reimburses them to the employee in addition to compensation for the use of a personal car?

Answer: no, you can't.

The standards approved by Decree of the Government of the Russian Federation of February 8, 2002 No. 92 already include compensation for all costs arising during operation (wear, fuel, lubricants, maintenance, repairs). Therefore, an organization that, in addition to paying compensation according to these standards, also reimburses an employee for the cost of fuel and lubricants, does not have the right to take into account the costs of purchasing fuel and lubricants when taxing profits.

Similar conclusions are contained in letters of the Ministry of Finance of Russia dated September 23, 2013 No. 03-03-06/1/39239, Federal Tax Service of Russia for Moscow dated March 4, 2011 No. 16-15/020447). This position is supported by some arbitration courts (see, for example, the ruling of the Supreme Arbitration Court of the Russian Federation dated January 29, 2009 No. VAS-495/09, the resolution of the Federal Antimonopoly Service of the Ural District dated December 8, 2008 No. F09-9153/08-S3).

Advice: to take into account the costs of fuel and lubricants when calculating your income tax, instead of paying compensation, enter into a vehicle rental agreement with your employee.

In this case, the costs of fuel and lubricants can be included in expenses when taxing profits, both when they are included in the rent, and when they are paid separately (letters of the Ministry of Finance of Russia dated February 13, 2007 No. 03-03-06/1/81, dated November 29, 2006 No. 03-03-04/1/806). The legitimacy of this approach is confirmed by arbitration practice (see, for example, the resolution of the Federal Antimonopoly Service of the North-Western District dated February 20, 2006 No. A44-3149/2005-9).

Situation: can compensation for the use of an employee’s car be taken into account when calculating income tax if the car is registered to another person?

The answer to this question depends on who the car is registered to.

As a general rule, subclause 11 of clause 1 of Article 264 of the Tax Code of the Russian Federation allows you to reduce taxable profit by the amount of compensation for the use of an employee’s personal car (within the limits of the norms approved by Decree of the Government of the Russian Federation of February 8, 2002 No. 92).

If the car is jointly owned by an employee and another person, the amount of compensation can be taken into account when calculating income tax. This situation may arise, for example, if the car is joint property of the spouses. As a general rule, property acquired by spouses during marriage is their joint property, unless otherwise established by agreement between them (Clause 1, Article 256 of the Civil Code of the Russian Federation, Article 34 of the Family Code of the Russian Federation). And in this case, the employee driving the car is one of the owners of the car, that is, the car is considered his personal property. And, accordingly, the norms of subparagraph 11 of paragraph 1 of Article 264 of the Tax Code of the Russian Federation clearly apply to the amount of compensation for its use. Similar conclusions follow from letters of the Ministry of Finance of Russia dated December 5, 2012 No. 03-03-06/1/629 and dated May 3, 2012 No. 03-03-06/2/49.

The car can be registered to the employing organization, which is the owner of the car and bears the costs of its maintenance and operation. If an organization makes any payments to an employee for the use of a car, do not take such payments into account when calculating income tax. This is explained by the fact that in this case the employee is not entitled to compensation at all, since he does not incur any expenses. This conclusion follows from the totality of the provisions of Articles 164 and 188 of the Labor Code of the Russian Federation. Accordingly, the payment to the employee will not be considered compensation.

The question of whether compensation for the use of a car in other cases can be taken into account when calculating income tax is controversial.

According to experts from the Ministry of Finance of Russia, for the purposes of Chapter 25 of the Tax Code of the Russian Federation, only property that an employee owns by right of ownership is recognized as personal property. That is, it is possible to reduce taxable profit by the amount of compensation for the use of an employee’s personal car if the person is its owner. Accordingly, compensation that an organization pays to an employee who drives a car that is registered to another person (except for the case where the employee owns the car as joint property) cannot be taken into account when taxing profits. Such conclusions follow from letters of the Ministry of Finance of Russia dated December 5, 2012 No. 03-03-06/1/629, dated May 3, 2012 No. 03-03-06/2/49, dated March 18, 2010 No. 03- 03-06/1/150.

At the same time, Chapter 25 of the Tax Code of the Russian Federation does not contain requirements that the employee be the owner of the car. The concept of personal property is absent in the legislation. Therefore, the personal property of an employee can be recognized as property that belongs to him on any legal basis. A person (organization) has the right to issue a power of attorney to an employee to drive a car. A power of attorney is a written authority issued by one person to another for representation before third parties (Clause 1 of Article 185 of the Civil Code of the Russian Federation). Therefore, it can be recognized as the legal basis for ownership of the vehicle. That is, a car that a person uses by proxy can be considered his personal property. Since the employee uses the car in the interests of the organization, compensation payments for the operation of the car can be taken into account when taxing profits (within the limits of the norms approved by Decree of the Government of the Russian Federation of February 8, 2002 No. 92). But if the conditions provided for in Article 252 of the Tax Code of the Russian Federation are met:

- compensation must be economically justified. It can only be taken into account if the employee’s work involves traveling;

- compensation must be documented. To do this, it must be paid on the basis of an order from the head of the organization, which specifies the amount of compensation.

Previously, specialists from the financial department recognized the possibility of taking into account compensation in expenses if an employee uses a car by proxy (without putting forward conditions regarding ownership) (letter of the Ministry of Finance of Russia dated December 27, 2010 No. 03-03-06/1/812). A similar position is reflected in the letter of the Federal Tax Service of Russia for Moscow dated January 13, 2012 No. 20-15/001797.

Taking into account the later position of the Russian Ministry of Finance, risks may arise when including in tax expenses amounts of compensation for an employee who drives a car registered to another person (and is not the owner of the car). Arbitration practice on this issue has not yet developed.

How to calculate the amount of compensation

The employee and the enterprise can establish in a mutual agreement that the amount of compensation will be fixed - this is more convenient from the point of view of calculations. Decree of the Government of the Russian Federation No. 92 of 02/09/2004 provides compensation standards by type of transport:

- for passenger vehicles with an engine capacity of up to 2,000 cm3 - 1,200 rubles. per month;

- over 2,000 cm3 - 1,500 rubles;

- for motorcycles - 600 rub.

Emelyanenko Natalya Leonidovna

Worked as a legal assistant in a law firm for 6 years

Ask a Question

In this case, the parties can establish large amounts of compensation, since the rules have not changed for 16 years. Then the enterprise will be able to include only the amounts established by the Government as expenses taken into account for the purpose of determining the tax base.

The second way to calculate compensation for the use of a personal car is to establish your own calculation methodology at the enterprise. It can be “borrowed” from taxi companies or developed independently. In this case, the key factor will be either the time the car is used or the mileage. Experts recommend taking into account the actual condition of the car, the degree of wear and tear, operating conditions and intensity of use.

A specific calculation of compensation may be contained in an employment contract or a local act of the organization, and its amount may be in a pay slip, order or agreement (if a fixed amount is accepted).

Calculation of compensation when establishing a fixed amount:

- Ivanov I.I. and Romashka LLC entered into an agreement under which the employer pays the employee compensation for using the car for business purposes in the amount of 10,000 rubles monthly in accordance with the days actually worked.

- Ivanov worked 18 days in June, and 21 days in July (39 days worked in total). In this case, the number of working days in the period is 20 + 21 = 41 days.

- Let's calculate the amount of compensation for 1 working day: 10,000 x 2 months: 41 days = 487.8 rubles.

- The amount of compensation for June-July will be 487.8 x 39 = 19,024.2 rubles.

- Separately, the employee is paid for the cost of fuel and lubricants based on the submitted receipts and payment for keeping the vehicle in the parking lot based on receipts.

Calculation of compensation if it takes into account mileage and wear and tear:

- A car costs 1,000,000 rubles, its useful life is 5 years. Accordingly, depreciation per month will be 1,000,000: 60 months = 16,666.7 rubles.

- The average daily mileage is 25 km. Compensation is set at 10 rubles. per km.

- The cost of using paid parking is RUB 5,000. per month.

- Vehicle washing and interior dry cleaning once a month - 6,000 rubles.

- Ivanov I. And in July he worked 19 days.

- We calculate the amount of compensation. First by mileage: 25 x 10 x 19 = 4,750 rubles. Then we sum up: 16,666.7 + 4,750 + 5,000 + 6,000 = 32,416.7 rubles.

- Costs for gasoline, maintenance and current repairs will be paid based on cash receipts, receipts and other financial documents additionally.

Point at which expenses are recognized

Both under the accrual method and under the cash method, the moment of recognition in tax accounting of expenses in the form of compensation for the use of a personal car will be the date of transfer of money from the current account (payment from the cash register) (subclause 4, clause 7, article 272, clause 3, art. 273 of the Tax Code of the Russian Federation).

An example of how expenses for payment of compensation for the use of an employee’s personal car for business trips are reflected in taxation

The organization applies a general taxation system. To calculate income tax, the organization uses the standards approved by Decree of the Government of the Russian Federation of February 8, 2002 No. 92.

In April, employee of Alfa CJSC A.S. Kondratiev was accrued and paid compensation for the use of his personal car for business trips.

The amount of compensation is 3000 rubles. per month. The amount of compensation is set taking into account the employee’s expenses for maintaining a car, purchasing gasoline, etc. (order on the assignment of compensation). The car's engine capacity is 2500 cubic meters. cm.

Alpha pays income tax monthly and uses the accrual method.

The compensation rate for cars with an engine capacity of more than 2000 cc. cm is 1500 rub. per month (Resolution of the Government of the Russian Federation of February 8, 2002 No. 92). Up to this amount, compensation will reduce the organization's taxable income. Excess amount of compensation in the amount of 1500 rubles. (3000 rubles – 1500 rubles) will not affect the calculation of income tax.

When calculating personal income tax, the Alpha accountant does not apply the norms of Decree of the Government of the Russian Federation of February 8, 2002 No. 92. Therefore, the entire amount of compensation (3,000 rubles) is not subject to personal income tax.

Compensation within the amounts established by the order (3000 rubles/month) is not subject to contributions for compulsory pension (social, medical) insurance and insurance against accidents and occupational diseases.

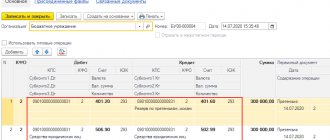

In April, Alpha’s accountant made the following accounting entries:

Debit 26 Credit 73 – 3000 rub. – compensation has been accrued for the use of a car for business trips;

Debit 99 subaccount “Continuous tax liabilities” Credit 68 subaccount “Calculations for income tax” - 300 rubles. (RUB 1,500 × 20%) – reflects a permanent tax liability that arose due to the excess of the amount of compensation over the norms established by law for calculating income tax.

Personal income tax - official and personal vehicles, taxes

Moreover, this amount is accepted by written agreement between the employer and employee. And it is formalized by an additional agreement to.

But this compensation is included in income tax expenses only within the limits established by Decree of the Government of the Russian Federation dated 02/08/02 No. 92 (subclause 11, clause.

1 ). Note: These standards are: for passenger cars with an engine capacity of up to 2000 cubic meters. see inclusive - 1200 rub. per month, and over 2000 cubic meters.

see — 1500 rub. per month. In addition to the amount of compensation itself, the employer must also pay the employee his expenses for maintaining the employee’s personal car, including the cost of fuel and lubricants.

simplified tax system

If an organization has chosen income as the object of taxation, then the costs of paying compensation for the use of an employee’s personal car do not reduce the single tax. With this object of taxation, no expenses are taken into account, including expenses for salaries and other payments to employees of the organization (clause 1 of Article 346.18 of the Tax Code of the Russian Federation).

Simplified organizations that pay a single tax on the difference between income and expenses can include compensation for the use of an employee’s personal car as an expense that reduces the tax base. But only within the limits established by the Government of the Russian Federation. This is stated in subparagraph 12 of paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation. Recognize costs only after they have actually been paid (clause 2 of Article 346.17 of the Tax Code of the Russian Federation).

The maximum amount of compensation that can be taken into account when taxing organizations on a simplified basis is established by Decree of the Government of the Russian Federation of February 8, 2002 No. 92. The cost norms for payment of compensation depend on the engine size of the passenger car. If the engine capacity is less than 2000 cc. cm (inclusive), then the compensation rate will be 1200 rubles. per month. If the engine capacity is over 2000 cc. cm – 1500 rub. per month.

Amounts of compensation exceeding these standards cannot be included in the organization’s expenses. Consequently, they will not reduce the tax base for the single tax during simplification (clause 1 of Article 346.16 of the Tax Code of the Russian Federation).

Similar conclusions are contained in the letter of the Ministry of Finance of Russia dated January 31, 2013 No. 03-11-11/38.

Situation: is it possible to take into account compensation for the use of an employee’s personal truck when calculating the single tax on the difference between income and expenses? The organization applies simplification.

Answer: no, you can't.

The list of expenses that reduce the tax base for the single tax is closed (clause 1 of Article 346.16 of the Tax Code of the Russian Federation). It allows you to take into account for taxation only those compensations that are paid for the use of personal cars and motorcycles (within the limits established by Decree of the Government of the Russian Federation of February 8, 2002 No. 92). Reimbursement for the use of personal trucks cannot be included in expenses.

Advice: to pay an employee money for the use of his personal truck, enter into a vehicle rental agreement with him. In this case, instead of compensation, the employee will need to pay rent. It will completely reduce the taxable income of the organization (subclause 4, clause 1, article 346.16 of the Tax Code of the Russian Federation).

Situation: when calculating the single tax on the difference between income and expenses, is it possible to take into account compensation for the use of an employee’s car if the car is registered to another person?

Answer: no, you can't.

Subclause 12 of clause 1 of Article 346.16 of the Tax Code of the Russian Federation allows you to reduce the tax base for the single tax by the amount of compensation for the use of an employee’s personal car (within the limits of the norms approved by Decree of the Government of the Russian Federation of February 8, 2002 No. 92).

If the car is jointly owned by an employee and another person, then the amount of compensation can be taken into account when calculating the single tax. This situation may arise, for example, if the car is joint property of the spouses. As a general rule, property acquired by spouses during marriage is their joint property, unless otherwise established by agreement between them (Clause 1, Article 256 of the Civil Code of the Russian Federation, Article 34 of the Family Code of the Russian Federation). And in this case, the employee is one of the owners of the car, that is, the car is considered his personal property. And, accordingly, the norms of subclause 12 of clause 1 of Article 346.16 of the Tax Code of the Russian Federation clearly apply to the amount of compensation for its use. Similar conclusions follow from letters of the Ministry of Finance of Russia dated December 5, 2012 No. 03-03-06/1/629 and dated May 3, 2012 No. 03-03-06/2/49.

The car can be registered to the employing organization, which is the owner of the car and bears the costs of its maintenance and operation. If the organization makes any payments to the employee for the use of the car, then do not take such payments into account when calculating the single tax. This is explained by the fact that in this case the employee is not entitled to compensation at all, since he does not incur any expenses. This conclusion follows from the totality of the provisions of Articles 164 and 188 of the Labor Code of the Russian Federation. Accordingly, the payment to the employee will not be considered compensation.

The question of whether compensation for the use of a car in other cases can be taken into account when calculating the single tax is controversial.

According to experts from the Russian Ministry of Finance, only property that an employee owns by right of ownership is recognized as personal property. That is, it is possible to reduce income by the amount of compensation for the use of an employee’s personal car if the person is its owner. Accordingly, the compensation that an organization pays to an employee driving a car that is registered to another person (except for the case where the employee owns the car as joint property) cannot be taken into account when calculating the single tax. Such conclusions follow from letters of the Ministry of Finance of Russia dated December 5, 2012 No. 03-03-06/1/629, dated May 3, 2012 No. 03-03-06/2/49 and dated March 18, 2010 No. 03- 03-06/1/150.

At the same time, Chapter 26.2 of the Tax Code of the Russian Federation does not contain requirements that the employee be the owner of the car. The concept of personal property is absent in the legislation. Therefore, the personal property of an employee can be recognized as property that belongs to him on any legal basis. A person (organization) has the right to issue a power of attorney to an employee to drive a car. A power of attorney is a written authority issued by one person to another for representation before third parties (Clause 1 of Article 185 of the Civil Code of the Russian Federation). Therefore, it can be recognized as the legal basis for ownership of the vehicle. That is, a car that a person uses by proxy can be considered his personal property. Since the employee uses the car in the interests of the organization, compensation payments for the operation of the car can be taken into account when calculating the single tax (within the limits of the norms approved by Decree of the Government of the Russian Federation of February 8, 2002 No. 92), but subject to the conditions provided for in paragraph 2 of Article 346.16 and Article 252 of the Tax Code of the Russian Federation:

- compensation must be economically justified. It can only be taken into account if the employee’s work involves traveling;

- compensation must be documented. To do this, it must be paid on the basis of an order from the head of the organization, which specifies the amount of compensation.

Previously, specialists from the financial department recognized the possibility of taking into account compensation in expenses if an employee uses a car by proxy (without putting forward conditions regarding ownership) (letter of the Ministry of Finance of Russia dated December 27, 2010 No. 03-03-06/1/812). A similar position is reflected in the letter of the Federal Tax Service of Russia for Moscow dated January 13, 2012 No. 20-15/001797.

Taking into account the later position of the Russian Ministry of Finance, risks may arise when including in tax expenses amounts of compensation for an employee who drives a car registered to another person (and is not the owner of the car). Arbitration practice on this issue has not yet developed.

Despite the fact that the above letters are addressed to income tax payers, the conclusions drawn in them can also be extended to simplified organizations (the norms of subclause 12 of clause 1 of Article 346.16 are similar to the wording of subclause 11 of clause 1 of Article 264 of the Tax Code of the Russian Federation).

Labor Relations

From the point of view of labor legislation, compensation includes monetary payments established to reimburse employees for costs associated with the performance of their labor or other duties (Part 2 of Article 164 of the Labor Code of the Russian Federation).

In accordance with Art. 188 of the Labor Code of the Russian Federation, when an employee uses personal property with the consent or knowledge of the employer and in his interests, the employee is paid compensation for the use, wear and tear (depreciation) of this property, and also reimbursed for expenses associated with the use of this property. The amount of reimbursement of expenses is determined by agreement of the parties to the employment contract, expressed in writing.

In the situation under consideration, the employee uses for business purposes a car that belongs to another person, which he has the right to use on the basis of a power of attorney issued by the owner of this car. In this regard, the question arises whether such a car can be considered personal property for the purposes of applying the provisions of Art. 188 Labor Code of the Russian Federation.

According to the judicial authorities, personal property should be understood as property that is in the possession or use of a specific person not only by right of ownership, but also on other legal grounds. A car transferred by proxy in relation to third parties cannot be perceived otherwise as being in the possession and use of a specific person. It is these powers that are necessary to use a car for business purposes, which allows the employer to compensate for the costs of using a car owned by an employee on the basis of a power of attorney (Determination of the Supreme Arbitration Court of the Russian Federation dated January 24, 2014 N VAS-4/14, Resolution of the Federal Antimonopoly Service of the Ural District dated May 29. 2013 N F09-4358/13 in case N A76-18948/2012, FAS Volga District dated 10/09/2012 in case N A12-2881/2012).

According to the provisions of Art. 188 of the Labor Code of the Russian Federation, the payment of compensation does not depend on whether the employee uses for business purposes a car that belongs to him by right of ownership or on the basis of any other right. In this regard, and also taking into account arbitration practice, we can conclude that compensation paid to an employee for using a car for business purposes, which he, not being the owner, has the right to use, should be considered as compensation paid on the basis of Art. 188 Labor Code of the Russian Federation.

However, official bodies interpret the content of this norm differently, explaining that a vehicle driven by an individual under a power of attorney is not his personal property, and therefore such compensation cannot be considered compensation paid in accordance with Art. 188 Labor Code of the Russian Federation (see, for example, Letters of the Ministry of Labor of Russia dated 02/26/2014 N 17-3/B-92, Federal Tax Service of Russia dated 10/25/2012 N ED-4-3/ [email protected] , Ministry of Finance of Russia dated 02/21/2012 N 03-04-06/3-42).

We note that in connection with this interpretation of the provisions of Art. 188 of the Labor Code of the Russian Federation, when an organization pays compensation to employees for the use of cars that do not belong to employees by right of ownership, tax consequences may arise, which are discussed below in the relevant sections.

In this consultation, the arising tax consequences are considered on the basis of the assumption that the organization is guided by the point of view of official bodies and does not recognize the amount of compensation paid to employees for the use of property that does not belong to employees by right of ownership as compensation established by Art. 188 Labor Code of the Russian Federation.

How to register correctly

Compensation to a company employee is paid based on the order of the manager. To do this, the citizen submits an application to the administration, indicating the following information:

- circumstances of using the car for business reasons;

- frequency of use of the car.

The following documents are attached to the application:

- for the car, including registration certificate and certificate;

- waybill;

- checks and other documents confirming the employee’s expenses for the car.

When the manager receives an application and documents from an employee, he issues an order. The document contains the following information:

- car technical passport number;

- technical characteristics of the vehicle;

- subsidy amount;

- the basis for providing compensation is a reference document that was concluded with the citizen;

- justification for the amount allocated.

The document indicates the period for issuing money. Funds are usually provided until the end of the current month.

The order is provided to the employee for review against signature. By signing the document, the citizen agrees to receive the specified amount within the established time frame.

When all formalities are completed, the order is transferred to the accounting department. Based on this, the employee is provided with money.

The head of the company may refuse to issue compensation. Causes:

In what cases can you expect compensation?

Reimbursement for expenses for using your own vehicle is provided if the traveling nature of the work activity is specified in the job responsibilities or agreement concluded with the citizen.

Compensation is issued on the basis of one of the following documents:

- additional agreement on the use of the car for work purposes;

- a rental agreement under which the employer rents a car from a citizen;

- an agreement on transportation services is concluded with employees if a personal car is not used constantly, but from time to time.

The employer reimburses expenses for:

- gasoline, lubricants;

- repairs in case of car failure;

- paid parking during business hours;

- washing

The issue of reimbursement of costs for using your own machine during working hours is regulated by Article 188 of the Labor Code of the Russian Federation.