Salary in accounting: basic operations

Payroll accounting is carried out within the framework of the following main operations:

- payroll;

- personal income tax withholding and salary contributions;

- making other deductions (for example, alimony under writs of execution);

- salary payments (advance, main part);

- payment of taxes and wage contributions to the budget.

These business operations may be supplemented by others, which are determined by the peculiarities of the production process at the enterprise. For example, by depositing salaries.

Each of the noted transactions must be reflected in the accounting registers. They are carried out at different times, which can be determined based on the specifics of tax accounting at the enterprise and the requirements of labor legislation.

Let's study how the timing of the noted transactions for accounting is established, as well as what entries are used when calculating and paying wages.

Postings when withholding personal income tax from wages

The main types of income for which personal income tax must be withheld are all kinds of accruals under an employment and civil service agreement. This list includes not only direct wages, but also bonuses, allowances, and some compensation received. Special formulas are used to calculate payments.

When personal income tax has been assessed on the amount, the posting of its deduction and transfer to the treasury is mandatory. After all, entities that transfer income to individuals, as a general rule, simultaneously become tax agents. Accordingly, their responsibilities include withholding and remitting tax payments.

Labor compensation accrued: postings

Salaries must be paid at least every half month. For example, until the end of the current month for the first half and until the middle of the next month for the second half. Thus, the generally accepted approach is that the components of salary are:

- An advance paid before the end of the billing month.

Accounting records only reflect the fact of payment of the advance (later in the article we will look at the entries used for such purposes).

- The main part of the salary paid at the end of the payroll month.

If wages are accrued, the posting is as follows: Dt 20 Kt 70 - for the amount of wages for the entire month (regardless of the amount of the advance payment transferred).

In this case, the posting can also be generated by debit of accounts:

- 23 - if the salary is intended for employees of auxiliary production;

- 25 - if salaries are transferred to employees of industrial workshops;

- 26 - if the salary is accrued to management;

- 29 - when calculating wages to employees of service industries;

- 44 - if salaries are paid to employees of trade departments;

- 91 - if the employee is engaged in an activity that is not related to the main one;

- 96 - if the salary is calculated from reserves for future costs;

- 99 - if payments are calculated from net profit.

The salary accrual date is determined based on tax accounting standards, according to which salaries are recognized as income only at the end of the billing month (clause 2 of Article 223 of the Tax Code of the Russian Federation).

The procedure for calculating personal income tax on material benefits (example)

When receiving a low-interest or interest-free loan from an organization, the employee receives a material benefit in terms of savings on interest.

NOTE! From 2021, new conditions for personal income tax assessment of this type of financial benefit have been introduced. See more details.

It matters in what currency the loan agreement is drawn up.

If it is issued in rubles, then the threshold rate is 2/3 of the current refinancing rate established by the Central Bank of the Russian Federation on the date of receipt of income (clause 2 of Article 212 of the Tax Code of the Russian Federation).

NOTE! From 2021, the refinancing rate is equal to the key rate (directive of the Central Bank of the Russian Federation dated December 11, 2015 No. 3894-U) and is:

- from September 19, 2016 - 10% (information from the Bank of Russia dated September 16, 2016);

- from March 27, 2017 - 9.75% (information from the Bank of Russia dated March 24, 2017);

- from 05/02/2017 - 9.25% (information from the Bank of Russia dated 04/28/2017);

- from 06/19/2017 - 9% (information from the Bank of Russia dated 06/16/2017);

- from September 18, 2017 - 8.5% (information from the Bank of Russia dated September 15, 2017);

- from 10/30/2017 - 8.25% (information from the Bank of Russia dated 10/27/2017);

- from December 18, 2017 - 7.75% (information from the Bank of Russia dated December 15, 2017);

- from 02/12/2018 - 7.5% (information from the Bank of Russia dated 02/09/2018);

- from March 26, 2018 - 7.25% (information from the Bank of Russia dated March 23, 2018);

- from September 17, 2018 - 7.5% (information from the Bank of Russia dated September 14, 2018);

- from 12/17/2018 - 7.75% (information from the Bank of Russia dated 12/14/2018).

If the loan is issued in foreign currency, then the established threshold value is 9% per annum (clause 2 of Article 212 of the Tax Code of the Russian Federation).

If interest is less than the threshold values or is not charged at all, personal income tax is withheld from the difference at a rate of 35%.

It is better to consider the postings for calculating personal income tax using a specific example.

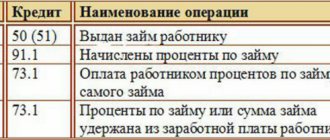

The organization issued a loan to employee Ivanov I.I. (resident of the Russian Federation) for a period of 1 year in rubles at a rate of 3% per annum with interest paid at the end of the loan term. Loan size - 500,000 rubles.

Dt 73 “Ivanov I. I.” Kt 50 - 500,000 rub. — the loan amount was issued to Ivanov on January 15, 2019.

Income from the amount of the benefit from 2021, regardless of the date of payment of interest, is determined monthly on the last day of the month. Let's calculate the amount of interest on the loan for January 2021. There was no partial repayment of the loan in January. The number of days for which material benefits are calculated from 01/16/2019 to 01/31/2019 is 16.

500,000 × 0.03 × 16/365 = 657.53 rubles.

Dt 73 “Ivanov I. I.” Kt 91 - 657.53 rub. — interest accrued for using the loan for January 2021.

We will calculate personal income tax on the amount of material benefit.

2/3 × 7.75% = 5.17% - threshold, taking into account the current refinancing rate.

5.17 – 3 = 2.17% - interest on material benefits.

500,000 × 0.0217 × 16 / 365 = 475.62 rubles. - material benefit for January 2021. Let's calculate personal income tax (35%) from it: 475.62 × 0.35 = 166 rubles.

If Ivanov were a non-resident of the Russian Federation, then the tax would be withheld at a rate of 30% (clause 3 of Article 224 of the Tax Code of the Russian Federation).

Dt 70 (73) “Ivanov I. I.” Kt 68 “NDFL” - 166 rubles. — Personal income tax on material benefits for January 2021 is withheld from the employee’s salary (or other income).

Dt 68 “NDFL” Kt 51 - 166 rubles. — Personal income tax from savings on interest for January 2021 is transferred to the budget.

Calculation of salary taxes and contributions: accounting features

Immediately after payroll is calculated:

1. Personal income tax

The fact of calculation and withholding of personal income tax is reflected in the accounting registers by posting Dt 70 Kt 68.

If a personal income tax deduction is applied to wages, then it does not need to be reflected in accounting.

2. Insurance premiums.

The fact of their accrual is reflected by posting Dt 20 Kt 69.

As in the case of salary postings, correspondence can also be generated by debits of such accounts as 23, 25, 26, 29, 44 and others that we discussed above.

The accrual of personal income tax and contributions is shown, like the accrual of wages, on the last day of the month.

Personal income tax and contributions are calculated on the total amount of salary without any adjustment for the advance payment.

From November 30, 2020, the cashier is not required to require a passport from the recipient of funds to identify him.

When the salary is issued, the postings will be as follows.

Withholding of personal income tax is reflected by posting

The main tax by which the state regulates income received by individuals is the personal income tax, which is calculated and paid in accordance with Chapter. 23 h. Submission of SZV-M for the founding director: the Pension Fund has made a decision. The Pension Fund has finally put an end to the debate about the need to submit the SZV-M form in relation to the director-sole founder. So, for such persons you need to take both SZV-M and SZV-STAZH!

When paying an employee funds for a business trip above the established daily allowance (by order of the manager), the income received is subject to personal income tax at a rate of 13%. Accrual of travel allowances and deduction of personal income tax, the posting will be reflected in the memorial order as follows: Debit Credit Transaction 71 50 (51) Advance issued to the employee for future expenses 44 (20, 26) 71 Accrued amount of travel allowances 70 68 Accrued income tax on the difference between the established daily rate and issued to the employee in the amount of 68 51 Tax transferred to the State Budget Penalty for non-payment of personal income tax Personal income tax entries on dividends Reflection of entries in accounting for the payment of dividends and the accrual of personal income tax entries will depend on whether the founder is an employee of this organization or not. In the case when the founder works at this enterprise, account 70 will be used, if he is not an employee of the company - account 75.

Salary issued (reflected on the employee’s personal account): postings

The fact of salary payment is reflected in accounting by posting Dt 70 Kt 51 (or 50).

A similar posting is used when paying an advance.

The date of formation of the above posting for salary or advance payment is determined based on the date of each payment.

In this case, the actual amount of the “basic” labor payment is calculated minus the advance and personal income tax. It turns out that the tax is “withdrawn” from the corresponding amount, although it is charged on the total salary (the summed amount of the “basic” payment and advance payment). This circumstance reflects the specifics of tax accounting.

In accounting, therefore, in any case, the following should be distinguished:

- advance amount;

- the amount of the “basic” payment.

Postings of payment of wages in terms of the advance and its second half are recorded in the accounting registers on the day the funds are issued to employees.

After all the transfers, the employees’ personal payroll accounts are filled out (on Form T-54). Information is entered into them monthly.

Types of postings for salaries and taxes

The total employee payroll for the month is displayed on the last day of that month. At the same time, the amounts for calculated tax (personal income tax) and accrued insurance premiums are formed.

In some cases, accrual occurs at other times. We are talking about payments when granting vacation, upon dismissal of an employee and other settlement cases.

Wages are generated using account 70. Accounting is kept separately for each employee. The cost account is determined depending on the employee’s employment in one of the structural divisions, on the specifics of the organization, for example:

- Dt 20 Kt 70 - wages accrued to employees of the main production;

- Dt 26 Kt 70 - salary of the management staff;

- Dt 44 Kt 70 - wages for employees of a trading enterprise.

The formation of wages and other payments is accompanied by the withholding of personal income tax and the calculation of insurance premiums. Income tax is withheld from the calculated amounts to employees, while the responsibility for transferring personal income tax falls on organizations as tax agents. Insurance premiums are calculated entirely at the expense of the employer.

To generate income tax data, a subaccount 68.1 is opened for account 68. When making records of insurance deductions, the following subaccounts are used:

- 69.1 - contributions to the Social Insurance Fund;

- 69.2 - insurance contributions to the Pension Fund;

- 69.3 - amounts in the Federal Compulsory Medical Insurance Fund;

- 69.11—accruals to the Social Insurance Fund for injuries.

Transactions on tax withholding and assessment of contributions are reflected in the following transactions:

- Dt 70 Kt 68.1 - personal income tax is withheld from accrued earnings;

- Dt 20 (23, 25, 26, 44) Kt 69 - insurance premiums have been charged.

Payment of taxes and contributions: postings

Personal income tax is withheld and transferred from the paid salary (“main” payment) no later than the day following the day the funds are issued.

Contributions are transferred by the 15th day of the month following the month for which the salary was accrued.

Information about this is reflected in the accounting registers when transactions are activated:

- Dt 68 Kt 51 - tax paid;

- Dt 69 Kt 51 - contributions transferred.

In order to reflect in accounting information about other types of labor payments - vacation pay, travel allowances - the same correspondence is used. But you need to keep in mind that in the entries used in payroll and those that characterize the issuance of, for example, vacation pay, the dates of deduction and calculation of personal income tax are determined differently.

The fact is that personal income tax on vacation pay is calculated not at the end of the month, but at the time the vacation is paid. Tax is withheld on the day the funds are issued to the employee. Personal income tax on vacation pay can be transferred on any day before the end of the billing month (clauses 4, 6, article 226 of the Tax Code of the Russian Federation).

Personal income tax – postings:

- Personal income tax is withheld from wages - posting D 70 K 68.1 is carried out when making payments to employees employed under employment contracts. The deduction for vacation pay is reflected in the same way.

- Personal income tax withheld under GPA agreements - posting D 60 K 68.1

- Personal income tax was accrued for material benefits - posting D 73 K 68.1.

- For financial assistance, personal income tax is assessed - D 73 K 68.1.

- Personal income tax is withheld on dividends - posting D 75 K 68.1, if the individual is not an employee of the company.

- Personal income tax is withheld on dividends - entry D 70 K 68.1, if the recipient of the income is an employee of the company.

- For short-term/long-term loans provided, the accrual of personal income tax is reflected - D 66 (67) K 68.1.

- Personal income tax was transferred to the budget - posting D 68.1 K 51.

An example of calculating income tax and generating standard transactions:

Employee Pankratov I.M. Earnings for January were accrued in the amount of 47,000 rubles. An individual is entitled to a deduction for one minor child in the amount of 1,400 rubles. We will calculate the amount of tax to be withheld and make accounting entries.

KBK NDFL for employees 2017

Personal income tax amount = (47000 – 1400) x 13% = 5928 rubles. There are 41,072 rubles left to hand over to Pankratov.

Postings:

- D 44 K 70 for 47,000 rubles. – earnings for January have been accrued.

- D 70 K 68.1 for 5928 rub. – personal income tax withholding is reflected.

- D 70 K 50 for 41072 rub. – reflects the cash payment of earnings from the company’s cash desk.

- D 68.1 K 51 for 5928 rubles. – the tax amount has been transferred to the budget.

Let's add the conditions of the example. Suppose Pankratov I.M. provided a loan to his organization in the amount of 150,000 rubles. with interest payment in the amount of 8,000 rubles. We will charge personal income tax on interest at an estimated rate of 13%.

Personal income tax amount = 8000 x 13% = 1040 rubles.

Postings:

- D 50 K 66 for 150,000 rubles. – the loan is reflected.

- D 91 K 66 for 8000 rubles. – interest is reflected.

- D 66 K 68.1 for 1040 rubles. - tax charged.

- D 66 K 50 for 151040 rub. – taking into account the due interest, the loan is repaid in cash.

Conclusion - calculating personal income tax using postings is a mandatory procedure for paying any income to individuals, with the exception of non-taxable transactions. Tax rates are regulated at the legislative level and vary by employee category.

If you find an error, please select a piece of text and press Ctrl+Enter.

Salary deductions: postings

Common types of salary deductions include:

- Withholding of alimony (based on writs of execution, based on an agreement with the recipient, at the request of the employee).

In the accounting registers it is reflected by posting Dt 70 Kt 76. Subsequent payment of alimony to the recipient is reflected by posting Dt 76 Kt 51 (50).

- Withholding amounts to compensate the employer for damages.

Here, to reflect deductions in accounting, posting Dt 70 Kt 73.2 is used.

- Retention of unconfirmed expenses issued for reporting.

In such cases, posting Dt 70 Kt 94 is used. Previously unreturned accounts are written off using posting Dt 94 Kt 71.

Deductions are made only after personal income tax is withheld from the employee’s salary (clause 1 of article 210 of the Tax Code of the Russian Federation, clause 1 of article 99 of the law “On Enforcement Proceedings” dated October 2, 2007 No. 229-FZ).\