Accounting is the theory and practice of bookkeeping and accounting. It is used in all organizations and enterprises and serves to accumulate data on all business transactions, property status and obligations of a legal entity to counterparties and regulatory authorities. Accounting involves the use of special numbers for each type of incoming and outgoing transactions.

Among them there is also a register that allows you to control current accounts. This is 51 accounting accounts. In this material, especially for dummies, we will examine in detail what account 51 is, whether it is active or passive, what the account card 51 looks like, what it is and with which registers it corresponds.

Accounting is based on recording all transactions in special positions

What it is

Settlements with suppliers of goods or raw materials, customers of these goods or personnel are one of the most important transactions in the life of every legal entity. 51 accounts in the accounting department is the “Settlement Accounts” register, designed to collect information about the availability of material assets in the national currency of the Russian Federation (in Russian rubles) and about their movement through the payment accounts of an organization or enterprise. Accounts, in turn, must be opened in financial and credit institutions. Register 51 is active, since the opening and closing balances for it can only be debit

Position 51 reflects the movement of all funds in current accounts

Basic definitions

Income that was not received from the main activities of the enterprise is considered other income. Other income may include:

- Cash receipts that arose from the provision for temporary possession or use of an element or several assets of an organization.

- The financial benefit of the company, subject to its participation in the authorized capital of other companies. Income from accrued interest or other income on securities.

- Funds received as a result of joint activities as part of a simple partnership on the basis of an appropriate agreement.

- Profit that was received in the process of selling fixed assets and other types of assets that are not cash, manufactured products and goods sold. They may be income acquired from the execution of existing debt obligations, benefits from third party promissory notes and the sale of intangible assets (intangible assets).

- Accruals on interest accrued in connection with debt obligations of other companies.

- Bank interest charges incurred on existing deposits or accrued on the balance of open accounts.

- Cash received from the payment of fines, penalties and other sanctions for unfulfilled or overdue obligations of other companies.

- Assets that were transferred to the enterprise free of charge.

- Income received when covering losses incurred by a company or compensating for damage.

- Profit for previous years, which was identified during the audit.

- Funds for credit and deposit debts that have expired.

- Reimbursement of exchange rate differences.

- The amount of revaluation of assets in the direction of increasing their value. Billed in monetary terms.

- Other income not received from the sale of goods or products.

Among other things, they also include means of compensation for losses incurred from the occurrence of an emergency, which include compensation under an insurance contract, as well as the valuation of assets that are not suitable for use or cannot be restored. Since 2007, this information has been recorded on account 91 - other income and expenses, and not on account 99 on profits and losses.

Expenses that cannot be classified as basic are called other. They are as follows:

- Related to the leasing of company assets.

- Appear in connection with participation in the authorized capital of other companies.

- Arising from the sale, write-off or disposal of fixed assets and other assets not related to cash (except for the currencies of other countries), goods sold and manufactured products.

- Interest paid on credit and loan obligations.

- Related to fees for services provided by a credit institution.

- Contributions to valuation reserves, which are created in accordance with all accounting rules and regulations (reserves for debts of dubious origin, finances in case of depreciation of securities).

- Established reserves that were created in connection with the recognition of contingent facts of the economic activity of the enterprise.

- Other category, including payments for accounting services provided by third-party companies.

- The amount of penalties, penalties and penalties incurred due to failure to comply with the terms of the contract or in connection with failure to comply with its terms. Displayed in accounting documentation in the amount established by the court or with the consent of the debtor.

- Payment for damage caused to an enterprise or repayment by an organization of a loss resulting from its fault.

- Expenses of past years that were recognized in the reporting year.

- The amount of receivables with a past presentation period.

- The total amount of outstanding debts that cannot be collected.

- Expenses for compensation of exchange rate differences.

- The amount of revaluation of assets in the direction of reducing the cost of their valuation.

- Expenses for transferring contributions to finance charitable activities.

- Produced for the purpose of paying for recreation, entertainment, sports, cultural events or other similar purposes.

- Arose due to emergencies related to the economic activities of the enterprise (natural disasters, major accident or nationalization of property).

Starting from 2007, in accordance with PBU standards, expenses of these types are recorded on account 91 - other expenses, and not on account 99 for profits and losses. All available information is collected in this account and displayed in the balance sheet. Account 91 at the end of the reporting period will not have a residual balance.

What is it used for?

Account 51 was created in order to keep records, control and analyze data on the material funds of a legal entity that are located in banking organizations. This register reflects only payment and acceptance in the national currency of Russia.

Cash received by 51 registers will be accounted for as a Debit, and the amounts of all write-offs will be recorded as a Credit, which is obvious. One of the grounds for displaying receipts from this account is bank statements, and the amounts of all money transfers are carried out on the basis of instructions to make a payment.

Important! Analytical accounting for 51 accounts is carried out in the context of individual suppliers and customers who perform payment and receipt transactions with the company, as well as in the context of types of operations, for example, settlements with counterparties, payment of wages to personnel or payment of debt.

It is better to carry out analytics by dividing into counterparties and types of operations

Account accounting rules 51

The account was created to record, control and analyze information about funds that are listed in the bank current accounts of the organization. This account is used exclusively to reflect settlements in rubles.

Funds received into the account are reflected according to Dt, the amount of write-offs - according to Kt. The basis for reflecting receipts on the account are bank statements; the amounts of funds transferred are posted to the account on the basis of payment orders. The organization of analytical accounting of the account is carried out in the context of counterparties with whom settlements are carried out, and in the context of the types of transactions performed (transfer of funds to the supplier, loan payments, payments to staff, etc.).

Account characteristics

The debit (Dt) of the account reflects the receipt of funds to the organization's current accounts in the banks in which it is a client. That is, all money that was credited to the name of a legal entity passes through Debit 51 of the register. It is worth remembering that for a financial institution these funds are credit funds, therefore they will be located in the “Credit” item on the statement.

Examples of basic receipt operations:

- Receipt of funds from the buyer Dt 51.01, Kt 62.01 Bank statement or client payment order (primary document);

- Crediting collection revenue Dt 51.01, Kt 57.01. Bank statement or transmittal statement;

- Receipt of money under a loan or credit Dt 51.01, Kt 66 Bank statement, loan agreement, loan agreement;

- Contribution of the founder of a legal entity Dt 51.01, Kt 75.01 Bank statement or bank order.

The operation diagram of register 51

Credit (Kt) also shows the debiting of money from the organization’s bank accounts. It displays all transactions in descending order of funds.

Posting examples:

- Receipt of funds in cash, Dt 50.01 Kt 51.01, Bank statement or check for cash;

- Payment to the counterparty for goods or services, Dt 60.01 Kt 51.01, Bank statement, payment order;

- Repayment of borrowed funds, Dt 66 Kt 51.01, Bank statement or loan agreement;

- Transfer of salaries to staff on a card, Dt 76.05 Kt 51.01, Bank statement, letter for refund.

Typical postings and examples of operations

The correspondence of accounts for account 51 “Current accounts” is presented in the table:

| Account Dt | Kt account | Operation description |

| 51 | 57 | Funds “on the way” arrived in the account |

| 51 | 58/66,67 | Repayment of the loan provided/receipt from the loan taken and other loans |

| 51 | 86 | Receipt of funds for targeted funding, from other organizations and individuals, the budget |

| 51 | 91 | Sales revenue |

| 81 | 51 | Redemption of shares (own shares) from participants |

| 84 | 51 | Payment for events (by decision of the founders) |

| 99 | 51 | Coverage of uncompensated expenses related to emergencies and natural disasters |

Example 1. Postings when opening a current account

Let’s say Leto LLC has one main bank account. Soon, in addition, Leto LLC opened a corporate card account, to which funds were credited from the current account. The bank's opening fee was also withheld. The main account has been replenished. All transactions were carried out in Russian currency.

Table – Postings for 51 accounts when opening an account:

| Account Dt | Kt account | Wiring Description | A document base |

| 51 | 50 | Receipt of funds to the main current account from the cash register | Payment order |

| 55.07 | 51 | Transfer of funds to a bank card account from a current account | Bank statement |

| 91.02 | 55.07 | Paid for bank services (commission) | Bank commission invoice |

Example 2. Postings for deposit transactions for 51 accounts

Let’s assume that Osen LLC transferred 2,000,000 rubles to the deposit. at 10.5% per annum (compound interest) for one year. At the same time, 50,000.00 rub. withdrawn from the current account for targeted on-farm expenses.

Posting table – Deposit transactions:

| Account Dt | Kt account | Transaction amount, rub. | Wiring Description | A document base |

| 55.03 | 51 | 2 000 000 | Funds are transferred to deposit | Payment order |

| 76 | 55.03 | 21 000 | Interest accrued on the deposit | Accounting information |

| 51 | 55.03 | 21 000 | Interest on the deposit is credited to the current account | Bank statement |

| 51 | 55.03 | 2 000 000 | Refund of funds transferred to the deposit | Bank statement |

| 50 | 51 | 50 000 | Withdrawing funds from a current account | Bank statement |

Example 3. Postings to 51 accounts when paying by bill of exchange

Let’s say Osen LLC purchased goods for a total amount of 114,550 rubles. An interest-free promissory note was issued to the supplier as payment. Paid after two months.

Table - Postings for payment by bill of exchange:

| Account Dt | Kt account | Transaction amount, rub. | Wiring Description | A document base |

| 10.01 | 60 | 114 550 | Goods received from supplier | Packing list |

| 60 | 60.03 | 10 500 | A bill of exchange was issued to the seller | Bill issued |

| 60.03 | 51 | 114 550 | Bill paid | Payment order |

Existing subaccounts

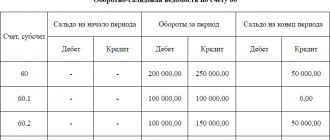

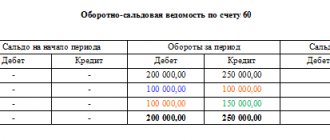

There are no official sub-accounts for 51 items. In accounting software like 1C: Enterprise or 1C: Accounting, you can create your own sub-accounts and even accounts. This is often used, but mistakes also happen often. By adding 51.01, 51.02 and other subaccounts, you can find that the ending balance for Debit and Credit will be the same at the end of one month, and then will be different.

Many people are accustomed to adding subaccounts to simplify work or to separate costs and profits for different types of activities. In new versions of 1C: Accounting 8, adding subaccounts may not end in the best way.

Important! Problems especially often appear at the end of the month, when it needs to be closed. The amounts in the subaccounts simply freeze, which requires additional modifications and procedures for closing the month.

The desire to add your own subaccounts and accounts in new versions of 1C may end badly

Features of the balance sheet

Why is it necessary to fill out a balance sheet? This question worries many ordinary people and officials who are entrusted with such a responsibility.

Despite the fact that the requirements for preparing the paper are not fixed in the current legislation, companies systematically complete it. The fact is that SALT allows you to obtain an objective assessment of the current financial situation in the company at any time. You don't have to wait for reporting to receive information.

Drawing up a balance sheet requires specific knowledge. The manipulation is not difficult, however, during its implementation, maximum care must be taken.

The presence of an error will require a recalculation of the data. The advantage of the statement is the possibility of verification. By checking the final data, the official responsible for drawing up the SALT will be able to immediately verify the correctness of the paper or the presence of inaccuracies.

Today there are several types of paper. They are similar, but have a number of significant differences that you need to familiarize yourself with in advance.

The company has the right to independently develop a statement form or use a ready-made sample. Having chosen the first option, you need to remember the need to include mandatory data in the paper. An analysis of current information on the topic will help identify their list.

Correspondence with other accounts

Register 51 corresponds with other accounts for Debit and Credit. List of interactions by Debit:

- 50 - Cash desk;

- 51 — Settlement registers;

- 52 — Currency registers;

- 55 – Special bank accounts;

- 57 — Transfers on the way;

- 58 - Financial investments;

- 60 — Settlements with suppliers and contractors;

- 62 — Settlements with buyers and customers;

- 66 — Calculations for short-term loans and borrowings;

- 67 — Calculations for long-term loans and borrowings;

- 68 — Calculations for taxes and fees;

- 69 — Calculations for social insurance and security;

- 71 - Settlements with accountable persons;

- 73 — Settlements with personnel for other operations;

- 75 — Settlements with founders;

- 76 - Settlements with various debtors and creditors;

- 79 — On-farm calculations;

- 80 — Authorized capital;

- 86 - Targeted financing;

- 90 - Sales;

- 91 — Other income and expenses;

- 98 - Deferred income;

- 99 - Profits and losses.

The current account position corresponds with a large number of other accounting positions for debit and credit.

Correspondence regarding the Loan occurs with:

- 04 - Intangible assets;

- 50 - Cashier;

- 51 — Current accounts;

- 52 — Foreign currency accounts;

- 55 – Special bank accounts;

- 57 — Transfers on the way;

- 58 — Financial investments;

- 60 — Settlements with suppliers and contractors;

- 62 — Settlements with buyers and customers;

- 66 — Settlements on short-term loans and borrowings;

- 67 — Settlements on long-term loans and borrowings;

- 68 – Payment of taxes and fees;

- 69 — Calculations for social insurance and security;

- 70 — Remuneration of personnel;

- 71 — Settlements with accountable persons;

- 73 — Settlements with personnel for other operations;

- 75 — Settlements with founders;

- 76 – Payment to various debtors and creditors;

- 79 — Intra-economic calculations;

- 80 — Authorized capital;

- 81 — Own shares (shares);

- 84 — Retained earnings (uncovered loss);

- 96 — Reserves for future expenses;

- 99 - Profit and loss.

Register analysis table for the accounting period in the 1C: Accounting program

Friends, today I would like to devote my article to setting up OSV in the 1C Accounting 8.3 program. The idea to write such recommendations arose after constant communication with clients, especially those starting to work in 1C programs. My tips will help you set up not only OSV, but also any of the standard reports in the Accounting 8.3 program.

So, in general, OSV in the 1C Accounting 8.3 program looks like this:

In this form, the reverse is not very informative. To change it, you need to use the “Show settings” button

In the form that opens, on the first tab “Grouping”, I recommend checking the “By subaccounts” checkbox

Now SALT will look like this, with each account broken down into subaccounts.

Many users with inquisitive minds often ask why there is an “Add” button on the “Grouping” tab and what it gives us for customization.

Let's get a look. Uncheck the “By subaccounts” checkbox and use the button to add an account, for example 10 with the “By subaccounts” checkbox and an empty subaccount.

The result was this OSV. With detailing for subaccounts of only one 10th account, and the rest of the accounts without detailing.

Once again, let's go back to the settings on the first tab. In the “by subconto” cell, click on the three dots and in the list that appears, select, for example, item.

We are forming the SALT and we have such a beauty, with details of the 10th account by subaccounts and by nomenclature.

Let’s continue studying the report settings (I returned the SALT to detailing by subaccounts of all accounts) and go to the “Selection” tab. If you are working with off-balance sheet accounts, then I advise you to check the appropriate box.

Then data on off-balance sheet accounts will appear at the bottom of the SALT:

We continue to study the possibilities of setting up OSV. And on the “Indicators” tab, check the NU box. This will allow us to see the data in circulation not only for accounting, but also for tax accounting. You can display permanent and temporary differences in the report.

On the “Additional Fields” tab, you can check the box to display the account name. This is convenient, since not every accountant remembers the name of this or that account in the chart of accounts.

After all our settings, the balance sheet will display information on the subaccounts of all accounts, data on accounting and tax accounting, as well as the names of the accounting accounts.

Someone especially curious asks, in the settings, the “Expanded balance” tab, why and how to use it? To illustrate this setting, let us return to the original form of SALT without subaccounts.

Let's look at account 62. Since this account is active-passive, it is not clear that the balance of 283957.56 is what the buyers owe us or is the amount of the buyers' debt so much greater than our shipment debt? Of course, it’s easier to expand 62 into subaccounts, but you can use the expanded balance without going through subaccounts:

Now let's create a balance sheet. This is the result we see in the 62nd count. The balance magically turned into two amounts:

The last tab in report customization will help you change the mood of your reports, i.e. set background color, text color, border.

In addition, at the bottom of the window of this tab you can display the name of the report, units of measurement and signature. This is necessary if you need to print the SALT.

Well, for example, we got this mood in the program.

And finally, a few words about the new features of the 1C Accounting 8.3 program. Sometimes it is necessary to compare, for example, balance sheets for two months. You can, of course, print out both OCBs and compare them on paper, but I want to show you how to display both of them on the program desktop.

So, we form two OSVs. You will get two tabs:

Right-click on the title of any balance sheet and from the proposed menu select “Show with others (vertically)” (or horizontally, as is convenient for you) and select the second SALT.

As a result, we were able to see two statements on the screen simultaneously.

Well, that's all I wanted to tell you today.

Work in 1C programs with pleasure!

Your consultant, Victoria Budanova, was with you.

Join our groups on social media. networks. The more questions you ask us, the easier it is for us to find topics for future articles.

| Head of care service Budanova Victoria |

Social buttons for Joomla

Accounting entries

The main item of transactions that can be carried out under 51 items are settlements with counterparties, who are suppliers of goods or raw materials, customers when performing services, and buyers. All these actions are carried out in accordance with previously concluded agreements. Typical transactions for such operations are as follows:

- Debit 51 Credit 62 - Receipt of funds from customers for goods or services (both as an advance payment and as a full final payment);

- Debit 51 Credit 60 - Returns by suppliers of goods or services before they are paid for;

- Debit 51 Credit 43 - Receipt of money for the provision of goods transportation services;

- Debit 51 Credit 76 - Receipt of money under concluded agreements with counterparties;

- Debit 60 Credit 51 - Payment to suppliers or contractors for services, goods or work rendered, both in the form of an advance payment and in the form of final payment;

- Debit 62 Credit 51 - Return to customers or buyers of funds that were credited by mistake earlier;

- Debit 76 Credit 51 - Accrual of money to other organizations and persons for other types of transactions;

- Debit 51 Credit 90 - Receiving revenue from the sale of products or performance of work (rendering services);

- Debit 51 Credit 91 - Receiving income from sales and other disposals, as well as reflecting non-operating income.

Important! Account assignments about changes in the state of accounted objects, described above, are not comprehensive for 51 registers, since it corresponds with a large number of positions, both for Debit and Credit. More wiring can be done.

Form of the Turnover balance sheet for 51 registers

conclusions

The turnover balance sheet according to account 51 is an important accounting register for non-cash money. It shows which financial institutions the business entity cooperates with to maintain current accounts.

It also reflects the balances of non-cash money at the beginning/end of the analyzed period, as well as information about receipts (debit turnover) and write-offs (credit turnover) according to bank details for the same time period.

The article describes typical situations. To solve your problem , write to our consultant or call for free:

+7 (499) 938-43-28 - Moscow - CALL

+7 - St. Petersburg - CALL

+7 — Other regions — CALL

Account Analysis

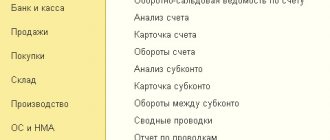

The analytics process involves deciphering the turnover and balance in the context of financial institutions for all of the accounts opened with them. Most often, in accounting and accounting systems, analytical accounting for 51 accounts is organized in the form of the following reports:

- The balance sheet for this register;

- Account Analysis 51;

- Account card 51.

Thanks to the formation of these documents, it is possible to control the movement of material assets at least every day and realize the possibilities for disposing of assets within the framework of the final balance. The analysis represents the correct formation of the balance at the end of the reporting period of any length. To calculate the balance, you need to add up the opening balance and debit turnover, and then subtract from this the total volume of cash movements on the loan in a given reporting period.

The balance sheet of register 51 is the balance for this register, which is displayed at the end of the month to close it. It should contain the beginning and ending balances, the total amounts of turnover for Dt and Kt. Also, SALT 51 is formed on the basis of a section of subaccounts.

Sample analysis card for 51 accounts, which is filled in automatically

Thus, 51 accounting registers are an accounting position that summarizes data on settlements of a legal entity with counterparties, customers and employees. It reflects the receipt of money into the organization’s accounts under Debit and its write-off under Credit. To analyze it, there is a card and OSV 51, which can provide the necessary data on a monthly basis.

https://www.youtube.com/watch?v=h5Q2PfrU45k

Account card 51: how to fill out

The card is generated daily based on accounting records and bank statements. Each transaction carried out on the current account is recorded on the card line by line, reflecting:

- remainder at beginning;

- the nature of the transaction (for example, receipt of payment, transfer of tax, payment for services of a counterparty/bank, etc.);

- the document on the basis of which it is drawn up;

- correspondence account;

- amount;

- ending balance. It is calculated by adding the balance at the beginning (it is always debit or equal to zero) with the debit turnover and reducing it by the amount of credit turnover.

For transactions with counterparties, their names, account numbers or agreements, which serve as the basis for making payment transactions or receiving funds, are entered on the card. Thus, the account card informs the user about each transaction performed and the balance of funds after it.