Accounting for payments to suppliers - a minimum of theory

If we talk about the essence of working with suppliers, we will say just two words - we buy and we pay. The details of this area are revealed in situations that arise when we buy or pay. For example.

We buy materials, goods, fixed assets, and services from suppliers. And if material assets came with additional amounts for transportation, then how to take them into account? And if it turns out that the delivery is defective, there is a shortage. How to proceed here?

The supplier may say that we owe him a certain amount, but we have a completely different amount in our accounts. What to do? Here you cannot do without reconciliation of mutual settlements. And that is not all.

The supplier to whom we owe formed a new company and transferred our debt to it. what should we do in this case?

You see, there are many different situations. But they are simple and with the correct understanding of the essence, you can easily guess what kind of wiring is needed.

In addition, these situations are rare cases for small enterprises. In general, there is nothing difficult or scary. Read the articles on the site, take part in practical classes and, in a very short time, you will understand everything. Well, now let's continue.

Primary documents for supplier accounting

The payments to suppliers section works in two directions: “we buy something from suppliers” and “we pay for purchases.” For each direction we have our own primary documents.

1. Primary documents from the supplier to us

Agreement

One of the very first documents is a purchase and sales agreement, which is concluded between companies. However, it may not exist, but firms cooperate. In practice, I noticed that when the tax office checks our company and draws attention to the lack of an agreement, then our company concludes one with the supplier.

In any case, the contract is insurance for each participant, supplier and our company, against any unpleasant affairs of one or the other. For example , a supplier supplied or provided us with something. Or, we paid the supplier in advance so that he would supply/bring us, for example, goods. And the supplier just “forgot” about us. In general, a contract is a legal document that describes the obligations of two parties and the consequences for failure to comply.

Invoice from supplier

The second document from the supplier is an invoice for payment, which indicates what exactly we are buying, how much it costs and bank details. This document does not have any legal force, but only provides background information. In this case, such a document serves as the basis for payment. Those. If our company decides to pay, then the basis for payment will indicate the account details: number such and such, from the number of such and such, from the counterparty of such and such, for such and such an amount.

Expense invoice, or Certificate of service, work performed

The supplier presents these documents to our company as the final result: goods and materials were delivered, service was provided, work was completed. The signature and seal of these documents on our part confirms our consent. And these documents already have legal force.

Supplier invoice

The supplier attaches this type of document to the Invoice, Certificate of Service or Work Completed. This document is issued by those supplier companies that pay Value Added Tax (VAT). This document repeats the contents of the Invoice for payment, the Invoice, and the Acts. But the main point of an invoice is to show how much VAT is included in the total amount of goods/services invoiced (we’ll talk about VAT in other articles).

2. Primary documents in our company

Making a purchase

As you understand, our company needs to prepare documents for the purchase. Regardless of what we buy: materials, goods, fixed assets, services, we draw up a document of the appropriate type “Receipt/Purchase of something”. If required, we register the supplier's invoice.

Making a payment

For our part, we pay the supplier. To decide which primary documents we will use, we need to decide How we will pay: Cash or Non-cash (Cash or non-cash). Once we decide, all we have to do is select the documents we need.

Examples of primary documents for accounting settlements with suppliers

Accounting: features and postings

It should be noted that when creating transactions, the type of payment for goods from the supplier is very important. Payment can be made:

- After capitalization of inventory items in full form;

- After the inventory items are capitalized, the money will be transferred partially;

- Funds for purchased goods are transferred according to the advance payment made.

At the same time, depending on the form of payment and the amount of transferred funds, the algorithm for not only reflecting accounting, but also tax accounting depends. VAT in the case of payment after capitalization and payment in advance is reflected differently. And this is important to know.

An example of a cycle of postings for advances made to the supplier is presented in the table.

Table - Example of correspondence

| Business operation | D-t | Kit |

| The company made an advance payment from the bank account for the purchased goods and materials | 60-2 | 51 |

| The listed advance reflects the receipt and capitalization of inventory items | 10 | 60-1 |

| VAT deductible on acquisition is reflected | 19 | 60-1 |

| Advance offset | 60-1 | 60-2 |

| VAT is accepted for deduction | 68 | 19 |

When transferring an advance according to account 90-2, the entire amount including VAT is reflected at once. If the delivery of goods is carried out without prepayment, then the posting cycle has a similar algorithm, only the number of operations is reduced:

- Goods received and posted:

D: 10; K: 60-1. The amount is indicated excluding VAT;

- VAT is accepted for deduction:

D: 68; K: 60-1.

- Payment transferred:

D: 60-1; K: 51 (50).

Regarding the analytical accounting of settlements with suppliers, each enterprise can independently determine the form of its management. But, as a rule, it is carried out separately for each entity with which a contract or agreement has been concluded. At the same time, additional sub-accounts can, of course, be opened to account 60, helping to carry out analytics more thoroughly and in detail. Sub-accounts are opened in such a way that all information is grouped according to the form of payment and the forms of documenting the relationship used.

Possible subaccounts:

01 – used for analytics on settlements with suppliers and contractors based on accepted and settlement documents;

02 – transactions for uninvoiced supplies are reflected, that is, those that do not have accompanying documents and are reflected in accounting without them;

03 – applies in the case of advance payments for inventory items that have not yet been delivered;

04 – settlements on issued bills of exchange;

05 – to reflect the relationship in terms of supplies with subsidiaries.

There are many more such subaccounts, but as a rule, in practice, the first 3 are the most popular.

When considering the accounting of settlements with suppliers and contractors, one cannot fail to mention such a category of costs as the service for the delivery of goods. Where should the costs be allocated in this case? Here, all transportation costs, regardless of the form of delivery, are reflected in the account credit. 60-01, but are debited either to the expenses of the period, or to the initial cost of the acquired assets. Or they are not reflected at all according to count 60.

In general, transportation can be carried out in the following forms:

- Self delivery. In this case, account 60 will not be indicated according to K., since it will not be in any way connected with the counterparty;

- Supplier. In this case, the amount for the service can be provided free of charge, which will not be reflected in the registers at all, or it can have its own fixed cost and then the amount of payment for the service on the credit account 60 is reflected;

- A separate transport company. The service will be paid, its amount will be reflected in the D. account. 10 (if materials are purchased), and according to the K. account. 60-1. Moreover, if the delivery service is not included in the initial cost of the object, then it is simply included in expenses, for example, invoice. 76, and according to K. the same account. 60-1. When direct payment for services is made, then invoice. 60-1 is closed according to D-th, and in K-th the account is indicated. 50 or 51 (depending on where the money is transferred from: from a cash register or a bank account).

Everyone knows perfectly well that in the process of economic activity of any entity, mistakes can be made. If we talk about this site, then as a result of capitalization, shortages of materials or their surplus may be identified. And this fact should also be reflected.

If, as a result of acceptance, warehouse workers identify facts of surplus inventory items for which there are no supporting documents, then they must capitalize them with the appropriate act (drawn up in 2 copies) and transfer it to the accounting department. In this case, an accounting employee can use two options:

- Reflect inventory items as income received and not report this to the supplier himself, then the D-t will be the account in which the specific material is accounted for, for example, invoice. 10, and according to K-tu the income account will be indicated, for example, account 91;

- Reflect the surplus as supplies without supporting documents, and again reflect the increase in the inventory account according to D-tu, and open a sub-account 60-2 for K-tu.

Also, in the course of business activities, there may be deliveries of products of inadequate quality, with defects, and then the company can return such products. In this case, accounting for the return of goods to the supplier has the following features: if a defect is detected, the buyer is obliged to open an off-balance sheet account 002, which serves to reflect inventory items accepted for storage. The entry is made for the amount indicated in the document - the price of such goods. After reflection by the buyer, that is, the organization, a corresponding claim must be drawn up, the form of which is not approved and is of an arbitrary nature. When the return itself is repaid, then 002 will be closed, and the receipt of monetary resources will be reflected in the entry: D 51 or 50, K 76.

Typical errors

Accounting for settlements with suppliers and customers is not without errors on the part of the accountant. At the same time, there are typical mistakes that, as a rule, are made by all subjects of activity. Among them are the following:

- The debt incurred by one entity is covered by funds received as an advance from another, that is, accounting is carried out not in an analytical context, but in a synthetic one. In this case, the main goal of the accountant is to keep the account balance. 60 in general was equal to 0 and it didn’t matter at the expense of whom;

- Failure to correctly determine the statute of limitations for debt, and, therefore, failure to timely write off such debt as expenses or income for the period. It is necessary to periodically review such debt and identify such facts;

- Carrying out VAT refunds on supplies that do not have documentary evidence;

- Incorrect or incorrect determination of exchange rate differences due to transactions in foreign currency;

- Not creating a reserve for doubtful debts;

- If there is a reserve, debt with an overdue statute of limitations is written off as expenses of the period, and not as a reserve;

- Other errors.

To prevent such errors, accounting must constantly take inventory of receivables and payables, check supporting documents, including agreements, contracts, etc. Such actions will help not only to avoid mistakes, but also to interact correctly with tax authorities. It is settlements with suppliers and buyers that are the main thing in the formation of VAT compensation, and here you need to know a lot of subtleties and nuances.

Accounts payable accounting itself is multifaceted, although there are not many typical transactions and accounts that are used. It is necessary to know the laws and guidelines perfectly so as not to make mistakes and do everything correctly.

Similar articles

- Accounting for settlements with suppliers and contractors

- Settlements with suppliers and contractors

- The double entry method in accounting means

- Documentation of settlements with suppliers and contractors

Interaction of the supplier settlement area with other accounts

I suggest you do the task yourself. From what you have read now, worked through the previous articles, write down the main accounting accounts with which account 60 interacts. If you can do it from memory, that’s great. If not yet, open the chart of accounts and try to choose. If you carefully studied the previous materials, then I’m sure you won’t need a chart of accounts.

Answers are available only to subscribers!

If you are subscribed to blog updates by email, enter the access code from the last mailing letter. To receive an access code, subscribe to blog news.

Interaction with other accounting accounts by debit

According to the principle of double entry, any business transaction must be reflected in the accounting documents in the debit of one account and the credit of another account for the same amount. In order to correctly draw up entries describing changes in the balance due to the receipt (decrease) of funds, you need to know the characteristics of each of the corresponding accounts. Answer the question: “Which count of 60 is active or passive?” is no longer difficult for readers: active-passive. An increase in liabilities will be shown in credit, and a decrease in liabilities - in debit.

What accounts does account 60 interact with? First of all, with the calculated ones: 50, 51, 55.1. They are used to pay off debts to suppliers. For example, an amount has been paid from the current account for the supply of goods. The posting will look like this: Dt 60 Kt 51. A similar account assignment is drawn up when transferring the advance payment. It is worth noting that such amounts must be accounted for in a separate subaccount. For example, Dt 60.2 Kt 51 - an advance is transferred from the current account.

In addition to money accounting accounts, debit account 60 can enter into correspondence with accounts 66, 67, 91. This happens if the debt was repaid by issuing a short-term or long-term loan (accounts 66, 67). Amounts with an expired statute of limitations are written off to 91 accounts, recognizing them as other income.

Chart of Accounts for Accounts Payable Account

Now it’s time to look at the chart of accounts and look at the 60 account, at its characteristics and think about what this gives us.

As you can see, accounting account 60 “Settlements with suppliers and contractors” has several subaccounts and subaccounts. For us now the scores of 60.1 and 60.2 are of interest. Why?

Because these two sub-accounts divide the information into “Asset” and “Liability”, look at the letters A and P. The information is divided in such a way that our debts to the supplier must necessarily be on account 60.1 (because “P”). But if we pay in advance, i.e. If we give an advance, then we must already indicate 60.2.

If we have a debt to the supplier, and we pay a little more, then we will first close 60.1, and the rest will go towards an advance, i.e. at 60.2.

Now another independent task. Write what the debt on accounts 60.1 and 60.2 will be called.

Answers are available only to subscribers!

If you are subscribed to blog updates by email, enter the access code from the last mailing letter.

To receive an access code, subscribe to blog news. Let's continue reading the account characteristics

— The balance on account 60.1 will go to the liability side of the balance — The balance on account 60.2 will go to the balance sheet asset

The subconto “Counterparties” will allow you to select a specific company name in the posting.

The “Agreements” subconto will allow you to select in a posting a specific contract of the counterparty within the framework of which the business transaction takes place.

These subaccounts and subcontos predict to us that in SALT for account 60 we will see the situation regarding counterparties and their agreements: who owes whom, how much, under what agreement. What we won't see is exactly why.

Accounting for bills of exchange issued to suppliers

In addition to the most common methods of payment in fact and in advance, there is also an option to pay for received assets, such as issuing a bill of exchange. Thus, the buyer gains a little time and guarantees that his obligations will be fulfilled on time. Accounting for issued bills is carried out on one of the subaccounts 60 of the account. Let's say this is a subaccount. 60.3. Let's look at the accounting entries that are made when performing this operation:

- Dt asset accounting account Kt “Settlements with suppliers” – received inventory items or completed work (services rendered) are taken into account.

- Dt “Settlements with suppliers” Kt “Bills issued” - a bill of exchange was issued to the supplier in payment of the amount due for the goods.

- Dt “Bills issued” Kt “Current account” – the bill is repaid on time.

Thus, organizing accounting in any of the possible payment methods for delivery is quite simple.

Account 60 is a kind of piggy bank of information on settlements with suppliers and contractors. This is one of the main items of the enterprise’s obligations, which is reflected in the annual reports and significantly affects the economic position of the company. Accounting on account 60 must be organized correctly, structured and provide all the necessary information about fulfilled, deferred, fulfilled and overdue obligations to suppliers.

operations require settlement transactions with suppliers. Above, we already touched upon settlements with suppliers, when we considered operations for the acquisition of materials, fixed assets, and intangible assets. In this lecture we will talk in more detail about payments to suppliers and contractors. The fact is that the processes of settlements with suppliers have some features, in particular of a legal nature, which must be taken into account by the accountant.

Suppliers are usually called organizations from which we purchase various types of goods. Contractors are usually those organizations that perform some work or provide services for us. Often, both are simply called suppliers - the accounting and legal regulation procedures for both are practically the same. Differences are observed only at the level of primary documents and the procedure for concluding transactions. In accounting, both suppliers and contractors look similar.

Agreement and invoice

Before any goods enter an organization or services are provided, an agreement must be concluded with a supplier or contractor. Only after the contract is concluded do actions begin to supply products, work begins, and so on. An agreement is not the only form of legal substantiation of relations with suppliers and contractors. The law will also be observed if, for example, you did not enter into an agreement with the supplier organization based on the invoice issued to you.

As a rule, large, important transactions are formalized using contracts. Moreover, usually the organization has a lawyer who is involved in drawing up and checking these contracts. The fact is that an error or inaccuracy in a contract can be very expensive and lead to very undesirable consequences. Typically, the contract reflects the type of obligation, for example, the delivery of goods, the timing of the contract, the procedure for acceptance and payment, and the responsibility of the parties. In accordance with Art. 432 of the Civil Code of the Russian Federation, an agreement is concluded by sending an offer (offer to conclude an agreement) by one of the parties and its acceptance (acceptance of the offer) by the other party. The agreement is considered accepted, that is, accepted, if it is signed by the heads of organizations or authorized persons and sealed by the parties participating in the agreement. If the requirements specified in the contract are met, but the contract itself is not signed, the contract is considered to be accepted.

If the terms of the agreement have changed, an additional agreement may be concluded. Typically, an additional contract refers to certain clauses of the original contract, changing their meaning.

The basis for accounting entries for a particular agreement are documents confirming its implementation. For example, these could be acts of acceptance of goods or work, invoices.

As we have already said, relations with a supplier can be formalized not only through a contract. Often the supplier simply issues an invoice to the buyer. The buyer accepts the supplier's products, pays the invoice and the transaction is considered completed.

The procedure for accounting for settlements with suppliers and contractors

To account for relationships with suppliers and contractors, account 60 “Settlements with suppliers and contractors” is provided. This is an active-passive account, the debit of which reflects the amounts paid to suppliers, and the credit - goods and services accepted from suppliers. The credit balance of this account is the organization's accounts payable - it shows the number of capitalized but unpaid assets. The debit balance of the account is the organization's receivables, which arise, for example, when paying an advance for goods or services.

The Chart of Accounts and the Instructions for its use provide the following characteristics of the objects accounted for on account 60:

Account 60 “Settlements with suppliers and contractors” is intended to summarize information on settlements with suppliers and contractors for:

- inventory items received, accepted work performed and services consumed, including the provision of electricity, gas, steam, water, etc., as well as for the delivery or processing of material assets, payment documents for which are accepted and subject to payment through the bank;

- inventory items, works and services for which payment documents were not received from suppliers or contractors (so-called uninvoiced deliveries);

- surplus inventory items identified during their acceptance;

- transportation services received, including calculations for shortfalls and overcharges of the tariff (freight), as well as for all types of communication services, etc.

When accepting goods and services on the basis of invoices, acts, invoices, contracts, the following entries are made on the credit of account 60:

D10 K60 - materials are accepted for accounting D41 K60 - goods are accepted for accounting D08 K60 - fixed assets, intangible assets received from the supplier are accepted for accounting D20 K60 - goods or services received from the supplier or contractor are accepted for accounting and included in the cost of production

Typically these entries are accompanied by an entry relating to accounting for input VAT:

D19 K60 - for the amount of VAT in accordance with the supplier’s invoice

Payment for goods and services is reflected in the following entries:

D60 K51 - paid for goods or services from the current account D60 K50 - paid for goods or services from the cash register

We said above that account 60 may have a debit balance, which reflects the amount of advance payment to the supplier, in fact, before the receipt of goods or services, this is the amount of his debt to our organization. The issuance of an advance is recorded as follows:

D60-A K51 - the supplier was given an advance from the current account

In this case, subaccount D60-A is used to account for advances issued to suppliers.

After, for example, the goods for which an advance was issued arrive, they are received in the usual way:

D41 K60 - goods were capitalized as an advance payment

And the advance payment itself is closed with the following entry:

D60 K60-A - the advance previously issued to the supplier is taken into account.

Various situations are possible in relationships with suppliers and contractors. We discussed some of them in the lecture on materials accounting. There, low-quality goods were received from the supplier, which, until the circumstances were clarified, we took into account on account 76 (sub-account “Settlements for claims”) with the following entry:

D76 K60 - received materials are taken into account, the quality of which does not correspond to the declared one.

These materials are taken into account in account 76 until the parties decide how to deal with them.

It is also possible that work or services were received, but our organization for some reason did not pay the invoice. For example, upon receipt of materials the following entry was made:

This situation arises not only if the purchasing organization is unwilling or unable to pay the supplier's invoice. It is possible that the buyer is ready to pay the invoice, but the supplier organization is no longer there. For example, the organization went bankrupt or ceased to exist. In this case, there will be no one to pay and the debt can also be written off against the income of the purchasing organization.

You might think that all you have to do is not pay your supplier invoices for three years and those invoices will automatically be cancelled. But it's not that simple. In particular, the Civil Code of the Russian Federation provides many grounds for suspending or interrupting the limitation period. Thus, if the supplier decides to file a claim before the expiration of this period, the period is interrupted. Well, if the supplier decides to file a claim after the expiration of the specified period - that is, three years - the court will have all the grounds for refusal - in accordance with Art. 199 of the Civil Code of the Russian Federation, which states that the expiration of the limitation period, the application of which is declared by a party to the dispute, is the basis for the court to make a decision to reject the claim. However, here, too, not everything is so simple - in the same Civil Code of the Russian Federation there are provisions that, if skillfully applied by the supplier’s lawyers, will make it possible to collect the debt in almost any case. From here we can draw a simple conclusion: if an organization has the opportunity to pay suppliers’ bills, it is better to do this before the supplier sues.

2. For inventory items, works and services for which payment documents have not been received from suppliers and contractors, i.e. so-called uninvoiced deliveries.

3. For surplus inventory items identified during their acceptance - when the actual quantity of incoming items exceeds the amount indicated in the suppliers’ payment documents.

4. For transportation services received, including calculations for shortfalls and overages of the tariff (freight).

5. For all types of communication services, etc.

Accounting on account 60 is carried out on an accrual basis, i.e. all transactions related to payments for acquired material assets, accepted work or consumed services are reflected regardless of the time of payment.

Accounting for account 60 is carried out in journal order No. 6. In this register, synthetic and analytical accounting are combined. Analytical accounts are opened for each supplier and contractor on a separate line.

In addition, account 60 takes into account calculations for advances issued for the supply of material assets or for the performance of work. To do this, a separate sub-account “Settlements for advances issued” is opened on account 60. Analytical accounting for the subaccount is maintained for each debtor.

If, to secure its debt, an organization issues its own bill of exchange to a supplier or contractor, then to account for such debt, a separate sub-account “Bills issued” is opened to account 60.

Register of analytical and synthetic accounting - journal order No. 6.

When an organization uses an automated form of accounting using the 1C: Enterprise software product, the registers of synthetic accounting are the turnover of account 60 (General Ledger), analysis of account 60, balance sheet, etc. The analytical accounting registers are the turnover balance sheet for account 60, analysis of account 60 by subconto, turnover between subcontos, account card 60, account card 60 by subconto, etc.

Main correspondence for account 60 “Settlements with suppliers and contractors”

| Contents of operations | Debit | Credit |

| Suppliers' invoices for material assets purchased from them have been accepted for payment. | 07, 08, 10, 15,41 | 60 |

| Accepted payment of contractors' invoices for work performed and services rendered | 20, 23, 25, 26, 44 | 60 |

| 19 | 60 | |

| Tax deduction for VAT | 68 | 19 |

| Claims were made to suppliers or contractors for shortages discovered during acceptance of valuables or work in excess of the norms of natural loss, discrepancies in prices, errors in shipping documents, violation of contract terms, etc. | 76-2 | 60 |

| Invoices of suppliers and contractors have been paid | 60 | 50, 51, 52, 55 |

| Debts have been offset (if the supplier is also a buyer of products (works, services) of this organization) | 60 | 62 |

| The debt to the supplier (contractor) was written off due to the expiration of the statute of limitations (3 years) | 60 | 91-1 |

| An advance was issued to the supplier (contractor) | 50, 51, 52 | |

| Accepted for deduction of VAT on advance payment | 68 | 60 subaccount “Settlements for advances issued” |

| Material assets for which an advance was previously paid were capitalized | 08, 10, 20, 26, 41 | 60 |

| VAT payable to the supplier (contractor) has been taken into account | 19 | 60 |

| Tax deduction for VAT | 68 | 19 |

| Advance taken into account | 60 | 60 subaccount “Settlements for advances issued” |

| VAT accepted for deduction after the advance payment has been restored | 68 | 60 subaccount “Settlements for advances issued” |

| Unused advance amounts were returned by suppliers (contractors) | 50,51,52 | 60 subaccount “Settlements for advances issued” |

| Own bill of exchange issued to the supplier (contractor) | 60 | 60 subaccount “Bills issued” |

Account 60 is used in the accounting of an organization to reflect information about settlements made with suppliers and contractors for goods and materials received, as well as work performed and services rendered, their surpluses, transportation services received, and others.

The account is credited for the cost of goods accepted for accounting (work performed, services provided) and corresponds with the accounts for their accounting. In synthetic accounting, the account is credited on the basis of the supplier's settlement documents, regardless of the assessment of values in analytical accounting.

The account is debited for the amounts of fulfillment of obligations, including advances and prepayments (they are accounted for separately) and corresponds with the accounts in which funds are recorded.

Analytical accounting for accounting account 60 is carried out separately, in the context of each presented invoice. At the same time, it is necessary to organize this accounting in such a way as to ensure the receipt of the necessary information on suppliers for settlement documents that have not yet become due for payment, for suppliers for settlement documents that have not yet been paid on time, for suppliers for bills of exchange issued that have not yet become due for payment, by suppliers according to the loan received and others.

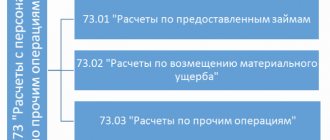

Among the subaccounts in accounting on account 60, the following are usually distinguished:

- — serves directly to reflect mutual settlements with creditors;

- — it reflects advance payments to suppliers;

- — a special sub-account for recording securities;

As well as accounts for accounting for mutual settlements in monetary units. and currency:

- — analogue for currency accounting;

- — analogue for calculations in conventional units;

- — analogue for calculations in conventional units.

Additionally

In trading or manufacturing enterprises, the supplier accounting accountant is closely associated with the warehouse operation. The accountant cooperates with the storekeepers. Storekeepers directly accept purchased goods and materials, check defects and quantities, and only then submit the supplier’s primary documents with their mark to the accounting department.

If necessary, claims are made to the supplier, a demand for the return of part of the money paid, or an additional payment.

An accountant and a warehouseman take inventory of the warehouse, where they compare accounting records and actual data in the warehouse. The results of the inventory, and this most often means shortages, surpluses, and re-grading, are documented in their own primary documents and accounting entries.