Account 71 in accounting: what is it used for

At the enterprise, by order of the manager, a list of accountable persons is introduced to whom money can be issued for established purposes. Since it is mandatory that after the activities for which employees were allocated money are carried out, a report is required to be submitted to the accounting department with documents confirming the expenditure attached, these persons are accountable.

The current rules for settlements with accountants are regulated by the procedure for conducting cash transactions. In addition to company employees, citizens engaged under contract agreements can also act as accountable persons.

The chart of accounts provides that account 71 must be used to account for settlements with accountable persons.

It reflects information about the occurrence of the employee’s debt to the organization for the amounts issued to him, as well as its repayment by submitting expenses according to the advance report.

The company’s debt to the accountable person is also reflected here if he spent his own funds for production purposes. By order of the manager, it is reimbursed in the approved amount upon acceptance of the advance report.

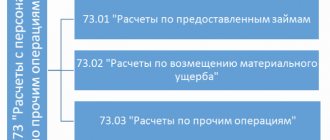

Important! Loans issued to employees cannot be taken into account in this account. For this purpose, a separate account 73 is used. Many business entities try to disguise loans provided to employees for short periods under the issuance of accountable amounts. However, this is a violation of the law.

Accountable amounts must be issued only for the purposes established in the order and the employee must report for them within a certain time frame or return the money. During inspections, the Federal Tax Service may identify these cases and assess additional taxes and fines.

To record settlements with accountable persons, you need to use journal order No. 7, which reflects during the month all expenses made by the accountable person, amounts issued for reporting, etc.

Accounts payable and its reflection

If the debit balance is the arrears of the staff, then the credit balance is the debt of the enterprise itself. If we evaluate accounts payable from an accounting perspective, then this is a financial assessment of the organization’s debt to other persons. Accounting is maintained on account 60 “Settlements with suppliers”.

This type of debt must be reflected in active-passive settlement accounts. Debt obligations are entered into passive accounting accounts. When recording accounts payable, the following rules should be followed:

- Offsetting should not be allowed between items of assets and liabilities.

- In the balance sheet, this type of debt is always presented as short-term and is reflected in section IV.

- If the debt is in a foreign currency, then when drawing up the balance sheet, it must be converted into Russian rubles at the rate that was established on the reporting date.

- If the organization has received at least part of the payment, then the debt is recorded in the balance sheet in the valuation minus the amount of VAT that has already been paid or is just about to be paid.

- If the debt has arisen from loans and credits, then it is reflected taking into account the accrued interest by the end of the reporting period.

Movements of funds should be reflected in accounting

Account characteristics

Synthetic accounting of settlements with persons to whom accountable amounts have been issued is organized on account 71. To answer whether this account is active or passive, you need to remember that its balance can be located either as a debit or as a credit. Thus, account 71 is an active-passive account with a double balance.

The balance at the beginning of the period in the debit of the account reflects the debt of the company's accountable persons for the money issued to them for established purposes. The account credit balance records the company's debt to the employee for expenses incurred at his own expense in the interests of the organization.

The debit of account 71 reflects the issuance of money for the purposes established by the enterprise or reimbursement to the employee of expenses approved by management that were previously made at his expense.

The credit of the account reflects the approved expenses of the accountable person, which are accepted by management, as well as the return of unspent funds to the cash desk or withholding them from the salary of the accountable person, if they are presented with an application for this method of repaying the debt.

To determine the ending balance, you must use the following algorithm:

- If the opening balance on account 71 is in debit, then you need to add the debit turnover on the account to it and subtract the amounts for the selected period on the loan. If you get a positive value, then the balance at the end will be a debit. Otherwise, it is reflected in the credit of the account.

- If the opening balance on account 71 is located in the credit of the account, then the turnover on the credit of the account should be added to it and subtract the total amount of movement on the debit of the account for the period under review. If the total value is greater than zero, it must be reflected as a credit to the account. A negative amount must be reflected in the debit of the account.

You might be interested in:

Chart of accounts for 2021 with explanations and entries

Accounts receivable from persons

All amounts of money that the company operates must be taken into account in accounting. Each line of the balance sheet must be completed by an accountant. If this is not done, then the inspection authorities may count the amounts provided to the accountable person as income of the organization or a targeted loan. And since this is profit, then tax must be paid on it, but since for obvious reasons this has not been done, tax officials have the right to impose penalties on the organization.

When a receivable is formed in the reporting, a separate document is created to reflect it. If any part of the funds remains unspent, then it must be returned to the enterprise's cash desk. In cases where this does not happen for some reason, the entire amount is deducted from the salary of the reporting person.

No matter how the money is returned to the cash desk, it must be reflected in the enterprise’s balance sheet with a special entry, based on the norms of current legislation.

Accounts receivable in accounting are reflected in the assets section of the enterprise. Despite the fact that this part of the property is in other hands, it is legally the property of the organization. When a report is drawn up, receivables should be arranged according to the dates of their formation. It is posted to account 62 “Settlements with customers”.

Next, you should find out how to reflect the debt on the forwarder's accountable amounts in the balance sheet: as an asset or as a liability. Here it should be understood that an asset is the finances and property that the organization owes, and a liability is what the organization owes. For example, money to pay for vacation is a liability. And the forwarder's debt for accountable amounts is an asset.

The unreturned portion of the money given to the accountable person may be deducted from his salary

Correspondence

Account 71 can participate in transactions with many accounts.

According to the debit of account 71, he can correspond to the credit of accounts:

- Account 50 - when issuing imprest amounts from the cash register;

- Account 51 - when transferring accountable amounts from a current account to a card;

- Account 52 - when issuing accountable amounts in foreign currency (for example, when traveling abroad);

- Account 55 - when issuing a report from special accounts;

- Account 76 - when issuing money, reporting according to the bank register;

- Account 79 - when issuing the account at the expense of the branch, separate division;

- Account 91 - when writing off exchange rate differences if the funds were issued in foreign currency.

By crediting the account, it can enter into transactions with the debit of the following accounts:

- Account 07 - when registering equipment for further installation purchased through accountable amounts;

- Account 08 - when reflecting costs (business trips, other costs) associated with the acquisition of non-current assets;

- Account 10 - when purchasing materials using imprest amounts;

- Account 11 - when purchasing animals for fattening using accountable amounts;

- Account 15 - when purchasing materials, if the accounting policy stipulates accounting using account 15;

- Account 20 - when writing off accountable amounts for the main production;

- Account 23 - when writing off accountable amounts for auxiliary production;

- Account 25 - when writing off accountable amounts for general production expenses;

- Account 26 - when writing off accountable amounts for administrative expenses;

- Account 28 - when writing off accountable amounts to correct a previously committed defect;

- Account 29 - when writing off accountable amounts for the costs of service and subsidiary farms;

- Account 41 - when reflecting the acquisition of goods through reporting;

- Account 44 - when writing off accountable amounts for the costs of selling products;

- Account 45 - when writing off accountable amounts for the purchase of goods that have not yet arrived at the organization;

- Account 50 - when returning unused imprest amounts to the cash desk;

- Account 51 – when returning unused imprest amounts to the current account;

- Account 52 – when returning unused imprest amounts to a foreign currency account;

- Account 55 – when returning unused imprest amounts to a special bank account;

- Account 70 - when deducting unreturned accountable amounts from wages (one-time deduction);

- Account 73 – when deducting unreturned accountable amounts from wages (multiple deduction);

- Account 76 - when closing a debt to a supplier for previously written off work or services;

- Account 79 - when transferring debt between branches and parent organizations;

- Account 91 - when reflecting a shortage of purchased materials within the limits of natural loss, when reflecting exchange rate differences when issuing a report in foreign currency;

- Account 94 - when reflecting a shortage, if the expenditure of the accountable amount is not confirmed by documents and it is not returned to the cash desk;

- Account 97 - when reflecting accountable costs that will be written off in future periods;

- Account 99 - when writing off accountable funds for liquidation of emergency situations and natural disasters.

Postings and accounting of unreturned imprest amounts

Amounts not returned on time by the accountable person are shown on credit account 71 in correspondence with account 94 “Shortages and losses from damage to valuables”:

Dt 94 Kt 71 - writing off amounts not returned by the accountable as shortages.

Thereafter, depending on the circumstances, such amounts may be reflected as follows:

- deductions from the employee’s salary - Dt 70 Dt 94;

- other settlements with employees - Dt 73 Dt 94.

The unspent amount of the account can be withheld from the employee’s salary only within one month after the date by which the advance must be returned (Article 137 of the Labor Code of the Russian Federation). The deduction is made on the basis of a written order from the manager with the consent of the employee.

In all other cases, this amount is included in other expenses with the employee.

NOTE! According to Art. 138 of the Labor Code of the Russian Federation, the amount of deduction cannot exceed 20% of the wages paid to the employee.

The procedure for issuing money for reporting

The issuance of funds to an employee can be carried out in several ways.

You might be interested in:

Account 03 in accounting “Profitable investments in material assets”, what is taken into account, correspondence of accounts, postings

The simplest and most common way is to issue money from the cash register. In this case, the cashier, at the time of issue, formalizes the operation with an expense cash order.

Until mid-2021, when issuing money, the employee must fill out an application for the issuance of the amount. This had to be done by any employee of the organization, including the director. Applications were allowed not to be filled out when reimbursing excess reporting and issuing daily allowances for business trips.

Since 2021, changes have been made to this procedure. The company can continue to use statements, or issue an order from the manager, which will indicate the full name. accountants, amounts and deadlines for reporting on funds received.

Attention! If there is no application or order, or if they are drawn up incorrectly, fines of up to 50 thousand rubles may be imposed on the company and responsible persons.

The application for the director should differ from the forms of ordinary employees - in it he does not ask for a report, but gives an order to perform this action.

The latest amendments to the procedure for cash transactions allow the issuance of a new amount if the employee has not yet reported the old one. Previously, such a step was prohibited.

In addition to cash, reports can also be issued by transferring from a current account to an employee’s card. For this step, he fills out an application and includes in it the bank details for making the payment.

If the application is not completed, the tax authority, upon inspection, will decide that income (salary) was transferred and will charge additional personal income tax on the amount. Also, the payment order must indicate that it is the issuance of the report.

If the issue is made to a card, then the employee can attach a receipt from the terminal, ATM, bank statement and similar forms as a supporting document. If the employee is on a business trip and an additional daily allowance is transferred to him, then there is no need to fill out another application. But you will need to report all amounts at the same time.

Attention! If the employee has not spent the accountable amount in full, then after completing the advance report, he must return the unused balance back to the cashier

Is a calculator an asset or a liability?

Reserves in the enterprise The reserve for doubtful debts refers to the liabilities of the enterprise. Now let's define the nuances, the reserve for doubtful debts is an asset or a liability in accounting. In this situation, it is appropriate to consider the basic terms. Note that the company's financial assets relate to its own part of the company's liabilities.

Accordingly, accountants reflect material and monetary funds formed to stabilize the liquidity of the enterprise in the passive part of the balance sheet. The formation of a reserve for doubtful debts is determined by special nuances. This amount, by law, is a maximum of 10% of the organization’s revenue. For this reason, specific figures here are calculated based on the determination of profit in the tax or reporting period. Moreover, here in accounting this position is reflected in credit account 63 with correspondence on the account. 91.02 “Other expenses”.

Help distribute household items. transactions on Debit and Credit accounts. I've already done the beginning, but it doesn't work any further. I can only use RAS, but I don’t know your work plan. Reflection in the accounting of expenses for payment of utilities during the period of work on the completion of the facility. Funds are issued to accountable persons in amounts and for periods determined by the head of the institution. Where do such accounts finally come from?))) This is Russia. Nobody knows the Ukrainian chart of accounts. Please help me understand the log of business transactions 1. How did you calculate the VAT on the received fixed assets? The VAT should be equal to 126,000 x 18% = 22,680, provided that the figure 18,000 is not given in your problem statement. Dina explained the rest of the errors to you.

What expenses can you give money for?

The legislative framework contains instructions for what purposes accountable amounts can be issued, these include:

- Payment for business trips and similar trips;

- Payment for services or work;

- Purchase of materials and goods;

- Incurring entertainment expenses;

- Other similar expenses.

An organization can establish the areas on which accountable persons have the right to spend the amounts issued to them by issuing an Accountability Regulation.

Important! The law prohibits the issuance of accounting funds for the acquisition of fixed assets. Also, accountable amounts cannot be used to make one-time transactions with organizations and entrepreneurs, the amount of which exceeds 100 thousand rubles.

An example of filling out a balance sheet

As of 04/01/2018, the accountable Simonov S. has an overexpenditure of one amount received under the report in the amount of 1000 rubles. and debt on the second in the amount of 5,000 rubles. The deadline for the report has not yet arrived. The amounts are reflected in the opening balances.

In the second quarter, S. Simonov received 1,000 rubles from the cash register. (debit turnover) and compiled an advance report for the second amount in the amount of 4,500 rubles. (credit turnover).

After this, another accountable Vasiliev A. received an amount for household needs - 2800 rubles. (debit turnover).

Now the ending balance in the statement will look like:

Simonov S. - final debit balance: 500 rub.

Vasiliev A. - final debit balance: 2800 rub.

The company records settlements with accountants using subaccount 71.01 “Settlements with accountants in rubles.”

NOTE! An employee can receive a new sum of money against the report before the previous one is fully settled.

Typical accounting entries

Let's look at how, in typical situations, accounting entries are made for reporting for dummies.

Purchasing materials through reporting

| Debit | Credit | Name of the situation |

| 71 | 50/1 | Money issued, report from the cash register |

| 71 | Materials were purchased for accountable amounts | |

| 19 | 71 | Accepted for VAT accounting on purchased materials |

| 10 | Purchased materials were released into production | |

| 50/1 | 71 | The person handed over the unspent balance of the accountable amount to the cashier |

| 71 | 50/1 | The accountable person was issued an overexpenditure on the accountable amounts from the cash register |

Travel expenses

| Debit | Credit | Name of the situation |

| 71 | 50/1 | Money was issued according to the cash register for a business trip |

| 20 | 71 | Expenses for purchasing travel tickets have been written off |

| 19 | 71 | Accepted for VAT accounting on purchased tickets |

| 44 | 71 | Hotel expenses and daily allowances written off |

| 19 | 71 | Accepted for VAT accounting for hotel stays |

| 50/1 | 71 | The accountable person returned the remaining funds to the cash desk |

How debt is written off

The mechanism for writing off each debt is very specific. All existing cases may differ radically from each other. To write off the balances of accountable amounts, you should do the following manipulations:

- Set the start date for the limitation period. If a person was obliged to return the money and report on July 7, 2015, then July 8 is considered such a date.

- Then count three years from this date. In this case, it is July 8, 2021.

- After which the amount of money is considered uncollectible and is written off in accounting against the reserve for doubtful debts.

Please note that a write-off is not a cancellation. For five years, the debt should be reflected in the balance on account 007.

Reflecting receivables and payables, even for an experienced accountant, sometimes poses a problem. All money in the organization’s circulation must be recorded when preparing accounting records. Therefore, you need to monitor periodically changing reporting rules.

You can learn about settlements with accountable persons from the video:

Attention! Due to recent changes in legislation, the legal information in this article may be out of date!

Our lawyer can advise you free of charge - write your question in the form below:

Free consultation with a lawyer Request a call back Still have questions? Call the number and our lawyer will answer all your questions for FREE

Definition

Count 71 is one of the most widely used

in the implementation of accounting records of transactions. Quotes from account 71, which is called “Settlements with accountable persons” or “Calculation of accountable amounts,” are used to reflect data on funds issued from the cash register and received by an employee of a business entity.

The tasks of issuing money to an employee are as follows:

:

- implementation of economic and operational activities;

- carrying out small wholesale purchases of goods;

- provision of travel and hospitality expenses.

In most cases, the need to issue financial resources arises when an employee completes tasks assigned by management to carry out the direct activities of the organization.

The peculiarity of the essence of account 71 is that the issued amount does not become the property of the accountable person and has a strictly intended purpose.

That is, an employee of an enterprise has the right to spend money only on the goals set by the manager, and also if they are a production necessity. If there is a balance of the amount received for reporting, it is returned to the cashier

.

An important point is compliance with cash discipline

relative to operating cash.

After the employee has fully completed the assigned task, it is necessary to provide a full report on the expenditure of the funds received within three working days

.

Otherwise, if for some reason the report is violated or the report is not provided at all, such amounts are regarded by the modern Tax Code of the Russian Federation as income of an individual

and are subject to taxation in conjunction with other employee income in accordance with Art.

137 Labor Code of the Russian Federation. Retention of unused and unreturned funds is carried out on the basis of Art. 138 of the Labor Code of the Russian Federation after submitting a written application and within the limits of up to 20% of wages

.

The modern regulatory framework of Russia does not regulate the period for issuing accountable funds; these points are stipulated by the internal documents of the organization. As accountable amounts, money can be issued exclusively to employees of the enterprise.

Turnover balance sheet

certain features in filling out advance reporting

.

It may have a balance on the debit side when the accounting policy of the enterprise is to issue advances for expenses stipulated by law. A credit balance is practiced during final settlements with “accountants” according to the scheme: expense - advance report - issuance of money

.

Due to the nature of operations, expense reports are usually handled by an experienced accountant or financial manager.

The formation of OSV in 1C is presented below.