Author of the article: Sudakov A.P.

An obligatory element of production activities are financial settlements with counterparties, with authorized bodies, with employees and with founders. They can be implemented in terms of cash or non-cash transactions. Cash transactions are carried out through the institution's cash desk. How is cash withdrawal from the cash register processed and is it always legal?

Enterprise cash desk

What can funds issued from the cash desk be spent on?

The intended use of funds issued from the cash desk of a business entity is regulated by the instructions of the Central Bank of the Russian Federation. If the fact of their spending outside the established directions is recorded, a fine will be imposed on the company by the Tax Service and the servicing banking institution.

The direction of use of money from the cash register depends on the source of its replenishment. The cash register can be replenished through a direct withdrawal of funds from the current account of a business entity. Money can come from accountable persons returning funds that have the status of an advance that were not used for the purposes for which they were issued, or from the founders of the company in the form of a loan. If a company specializes in sales, then cash most often comes from customers.

Trade revenue, determined by the funds contributed by customers for purchased goods or services provided, can be used to a limited extent for the needs of the enterprise and to ensure its functioning.

Wage

You can pay hired workers from the cash register or by transferring the required amount to a card account. When making cash payments, funds can be used from the proceeds or withdrawn from the current account of the business entity. If the company’s employee is a non-resident of the country, then the payment under the wage item falls into the category of foreign exchange transaction, therefore, in order to avoid later troubles, the easiest way is to transfer the money to a bank account.

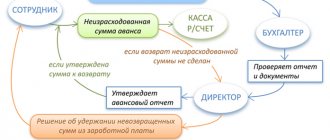

Money to report

In what situations is cash issued from the cash register?

Accountable money can be issued from funds in the institution’s cash desk, regardless of the source of its replenishment. To receive them you need:

- report on a previous similar operation;

- fill out an application that should reflect goals, amounts and deadlines;

- draw up an order for the release of funds;

- prepare payment documentation.

Legal acts do not regulate the limit amounts for issuance, therefore money in any quantity can be issued under this article, provided that their purpose is properly justified. The procedure for carrying out the operation of issuing funds on account must be regulated in local acts of the business entity covering the scope of accounting policies.

Material aid

Material assistance falls into the category of social benefits for which proceeds can be spent without restrictions. Payment is difficult to plan in advance, since the basis for its implementation is unplanned situations. A financial transaction must be preceded by its formalization, which consists of filling out an application from the employee with justification for the request and the reasons for the application. The document is the basis for drawing up an order, payment documentation and making payments from the cash register.

Debt to supplier

Registration of the procedure for issuing money

Debt to suppliers can be paid from the company's cash desk, regardless of the source of its formation. An exception is payment for rent of premises or equipment, which cannot be realized from cash proceeds. To pay off rent arrears, the head of the company will have to order money from the bank to withdraw from the current account, enter it into the cash register, and after withdrawal, pay the landlord. In order to prevent problematic situations with representatives of inspection authorities, the person responsible for conducting financial transactions must:

- do not exceed the cash payment limit;

- demand from the supplier a receipt confirming receipt of payment;

- keep powers of attorney from the supplier’s representative, executed by its management to receive funds.

Issuing money to persons who are not registered with the enterprise

If, as a result of production needs, it is necessary to issue money to persons who are not full-time employees, then the financial transaction is carried out using separate payment documents issued for each person. It is allowed to include the entire payroll of employees in the list, subject to a previously executed agreement.

The procedure for issuing money from the cash register

The issuance of funds to persons attracted to carry out contract work is carried out according to the statement. The document is drawn up separately for each enterprise from which employees were sent. It is certified not only by the management of the issuing organization, but also by the signature of the responsible employee of the company where the employees are on staff.

Documents for issuing money for reporting

The Central Bank has removed the requirements for an employee’s application to receive accountable funds. Previously, it had to contain the amount of cash, the period for which it was issued, the signature of the manager and the date. Now a simple statement is enough; there are no requirements for its content. Later, the Central Bank may establish the form of such an application.

The instructions also stipulate that it is possible to draw up one administrative document for several cash disbursements. There may also be more than one accountable person in the document. The main thing is to indicate the full names of all accountable persons, the amount of money and the terms for which they were issued. Previously, the Central Bank also allowed one order to be drawn up for several sub-reports, but now the rule has been formalized so that there are no disputes.

Penalties for violations

It is difficult to hold the management of a business entity accountable for spending funds for other purposes, since almost any waste of an enterprise can be justified.

Violation of the procedure for handling cash is subject to punishment. It can be checked by representatives of the Tax Service and banking institutions. It is worth noting that the bank can impose fines only if this type of collection is provided for in the service agreement. The Administrative Code provides for fines for violations of:

- exceeding the cash limit;

- exceeding the cash payment limit corresponding to 100,000 rubles;

- non-receipt of funds.

If a violation is detected in the cash register, officials, who may be the director and chief accountant, are assessed a fine of 4,000-5,000 rubles. The business entity will be subject to a penalty in the amount of 40,000-50,000 rubles, depending on the type of offense committed.

What exactly does the Bank of Russia classify as cash proceeds?

In accordance with the Directive of the Bank of Russia No. 3073-U dated October 7, 2013 (clause 2), for the purpose of applying this regulatory act, cash proceeds mean funds that:

- expressed in the currency of the Russian Federation – rubles;

- received by the cash desk from individuals, entrepreneurs and organizations;

- received at the cash desk as payment for goods sold, work performed and services rendered. In this case, the goods sold must be owned by the seller, and the work and services must be performed by the contractor himself. In other words, if an intermediary accepts payment for the specified goods, works and services, then this money is not the intermediary’s revenue . In particular, this applies to such categories of intermediaries as bank payment agents (or subagents) and payment agents. The funds that came to their disposal under the agreement in the process of performing operations to receive funds from the population, organizations and entrepreneurs cannot be spent by the specified agents at all, since they are not their property;

- or received by the cash desk as insurance premiums under insurance contracts.

All these conditions must be met at the same time. And then the amount of money received at the cash desk will be recognized as cash proceeds for the purpose of controlling its expenditure.

As for spending this revenue , this process, in turn, also has its own requirements:

- Directive No. 3073-U regulates a closed list of areas that can be paid for from cash proceeds;

- and additionally, the same act established a limit on cash payments between legal entities and individual entrepreneurs.

But first things first!

Video - cash accounting (cash: limit, calculations):

Issuing funds from the cash register. Procedure for completing the procedure

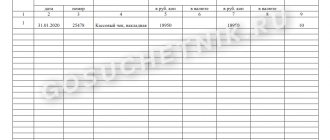

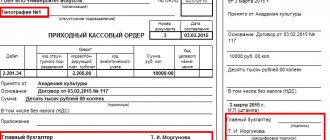

The basis for issuing funds from the cash register of an enterprise is an expense cash order.

As an alternative, a financial transaction may be carried out on pay slips, invoices or applications for the issuance of funds. When preparing documents, they require a stamp with the details of the cash order and the signature of the head of the company and the person authorized to approve the accounting documentation. Such details do not need to be filled out if the payment document is accompanied by papers on the basis of which the financial transaction is carried out.

Legislative regulation of the procedure

Companies specializing in the purchase of various products for the purpose of retail resale or use to ensure the functioning of production can pay cash from the cash register to account for the delivered raw materials. For all amounts issued during the daily period, at the end of the working day, a general cash order of an expense nature is issued, in accordance with the information from the receipts confirming the fact of the transaction.

What has changed - briefly in the table

The procedure for conducting cash transactions is regulated by Central Bank Directive No. 3210-U dated March 11, 2014. The latest amendments to it were approved by Central Bank directive No. 5587-U dated October 5, 2020 and come into force on November 30, 2021. These changes apply to the following categories:

- legal entities and individual entrepreneurs, including those from the SME register;

- employers who give employees money on account;

- organizations with separate divisions.

To make comparisons easier, we have collected all the latest changes in a table. Let's look at them in more detail next.

| Change | Was | It became |

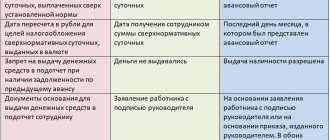

| Documents for issuing reports | The employee’s application contains the amount, the period for which they were received, the signature of the manager and the date An administrative document is drawn up for each cash disbursement | There are no requirements for the application One document is enough for several cash disbursements and accountants |

| Deadline for submitting advance report | Three working days from the date of return to work or from the day following the expiration of the period for which the money was issued | Installed by the manager or individual entrepreneur independently |

| Cash acceptance | No solvency control | Solvency control is required. All valid money must be accepted |

| Cash withdrawal | There is no quality check of banknotes before issuance | The cashier cannot issue banknotes with even one damage. They need to be handed over to the bank |

| Cash recipient verification | Identity card verification is mandatory; a special procedure for verifying a power of attorney is provided. | The cashier decides how to verify the identity of the recipient |

| Cash book in separate divisions (hereinafter referred to as OP) | Cash books are required for all OPs | You don’t have to keep a cash book if after each shift the OP’s cash is transferred to the legal entity’s cash register |

| Cash transactions without a cashier | Use of software and hardware | The use of automatic devices that accept and dispense cash and also check for security features on banknotes |

Documents that the recipient of the money must present

When issuing wages to employees through a cash register, one cash order can be issued for the total payment amount. His registration information appears on every document.

Funds based on documentation justifying the operation can be issued only upon presentation to the cashier of a document by which he can identify the person who contacted him. His data is recorded in payment papers. If they are compiled for several persons, then information about each of them is entered. They sign in the appropriate boxes, which confirms that specific people received the money. Information about identification papers is not included in the payment documentation.

If funds are issued to an employee of an enterprise, then it is possible to identify his identity using an internal ID issued by a business entity, provided that it contains a photograph and signature of its owner.

The fact of receipt of funds is recorded in a receipt, which is issued personally by the recipient. It should indicate in words and figures the amount of money received in hand. There is no need to display its value in words if the basis for the operation is a payslip.

Cashier's obligations

The cashier is responsible for the competence of performing his job duties, the main task of which is the correct conduct of monetary transactions through the cash desk of a business entity. To do this, it is necessary to check the documentation on the basis of which financial transactions are carried out, as well as its completeness and compliance with the list from the appendix to the main document. It is his responsibility to verify the presence and authenticity of all signatures.

If inaccuracies are identified in the documentation, it is necessary to return it to the accounting department for re-registration or correction. After the money is issued, the payment documentation is signed by the cashier. An appropriate stamp is placed on it with the date of the operation or a handwritten inscription with the same data “paid” is issued.