USN or PSN?

Special tax regimes help entrepreneurs reduce tax documentation and payments. Each mode has its own advantages for certain types of activities. If a businessman has several of them in his arsenal, it is worth thinking hard about the advisability of one or another special regime and, possibly, about replacing or combining them.

Common features of PSN and simplified tax system:

- the same tax rate – 6% of income;

- fixed insurance premiums “for yourself” (depending on the minimum wage);

- annual revenue is limited to 60 million rubles;

- accounting is not necessary;

- You can combine the regimes both with each other and with other tax systems.

What are the differences between the patent system and the “simplified” system?

- There is no need to generate reports and submit declarations, just fill out the Income Book.

- It is not necessary to install cash registers, but to issue strict reporting forms to all clients instead of checks.

- An entrepreneur is not required to pay a number of taxes:

- VAT;

- personal income tax;

- property tax for individuals if they are involved in business.

- The validity of a patent lasts from 1 to 12 months.

- Each subject of the Russian Federation is required to obtain its own patent.

- You can hire workers, but no more than 15 people.

- The single tax cannot be reduced, unlike the simplified tax system, where such a possibility is real for a single individual entrepreneur due to fixed payments.

RESULT: when is it profitable to switch to the patent system? The transition from the simplified tax system to a patent is advisable for an entrepreneur if in a given region he expects income from his activities in an amount significantly greater than the cost of the patent itself.

The procedure for transition to a patent tax system

Simplified tax system and patent at the same time - is it possible to combine the two modes?

Only individual entrepreneurs who have undergone official registration can switch to the patent system. The main condition for issuing a patent is that the types of activities used by the enterprise comply with the approved list of types of activities for the patent.

List of activities for which a patent is issued

Their complete list in each subject of the Russian Federation depends on the specifics of their legislation. But this definitely includes the activities of sewing workshops, hairdressing salons, dry cleaners, car repair and maintenance, services for transporting passengers and cargo, and some others.

Individual entrepreneurs whose average annual staff size exceeds 15 people have the right to use a patent.

The transition procedure consists of the following steps:

- Submitting an application.

- Obtaining a patent.

- Payment of tax.

- Organization of accounting.

The transition is possible only with the consent of the entrepreneur himself.

Who can plan the transition?

Not all businessmen have the right to change the current tax payment system to a patent one. For the replacement to be legally valid, 2 conditions set out by the Ministry of Finance of the Russian Federation in letter No. 03-11-12/50675 dated November 25, 2013 must be met:

- the patent tax regime is permitted for use in the relevant constituent entity of the Russian Federation;

- the type of business activity is contained in the transfer permitted for PSN, clause 2 of Art. 346.43 of the Tax Code of the Russian Federation, and cooperation is allowed with both individuals and organizations.

ATTENTION! This list can be expanded: you can add household services from OKUN to it (clause 8 of Article 346.43 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of the Russian Federation No. 03-11-11/45760 dated September 12, 2014), if they are provided only to individuals.

Who can't switch to PSN

If the type of activity of an individual entrepreneur, although included in the list of those permitted for a patent, is carried out under a simple partnership agreement (joint activity) or within the framework of trust management of property, PSN is not available for such persons.

Fully or partially?

If an entrepreneur has several relevant types of activity in his arsenal, the law allows him to combine the simplified tax system and the PSN in the way that seems more profitable to him. Or you can completely change the “simplified” form to a patent if the activities fall within those permitted under the PSN.

When combining tax systems, it is important to take into account the following nuances:

- profitability under both tax systems together should not exceed the limit of 60 million rubles;

- income from activities on the simplified tax system must be substantiated by a declaration that does not include income from the special tax system; this document is submitted in its own way at the end of the reporting year;

- if there were no violations of the conditions, the right to the simplified tax system, even if the regimes are combined, will remain with the individual entrepreneur for the next tax periods; it does not need to be specifically confirmed.

Can an individual entrepreneur be on a patent and the simplified tax system at the same time?

An entrepreneur has the right to combine two tax regimes for different types of activities. For the same species in the territory of one region, it will not be possible to combine the simplified taxation system and the PSN.

When combining, the following rules must be taken into account.

- Accounting for income and, if necessary, expenses (if the simplified tax system is income-expenditure) is carried out separately for each type of activity.

- To calculate the simplified tax system, data on revenue received from activities on the STS are not taken into account.

- General expenses and expenses that cannot be divided must be distributed to correctly reduce the tax base under the simplified tax system with the object “income minus expenses.” Distribution occurs in proportion to the share of income in total receipts.

- When combining a patent with the simplified tax system, the limit is 60 million rubles. applies to the total income of the entrepreneur. That is, in order to preserve the patent, the entrepreneur must under no circumstances allow the amount of income under both regimes to cross the specified threshold.

- An entrepreneur without employees has the right to fully include fixed contributions in expenses under the simplified tax system, if the simplified tax system is income-expenditure, or to fully use it as a deduction under the simplified tax system, if the object “income” is used (letter of the Ministry of Finance dated February 10, 2014 No. 03-11-09/ 5130). If an entrepreneur hires individuals, then insurance premiums from the latter’s salaries and fixed insurance premiums will be distributed depending on the specific activity in which these employees are engaged.

- To calculate additional contributions of 1% on the amount exceeding annual income of 300 thousand rubles. the potential income for the STS and the actual income received for the simplified tax system are summed up. Real patent income does not affect the amount of contributions.

Algorithm for switching to a patent

An individual entrepreneur can choose the option in which part of his activities will be taxed under a simplified system, and the part that is suitable by law is transferred to the STS, or make a complete transition, completely abandoning the simplified tax system. To do this, the following steps are required:

- Submitting an application at least ten days before the planned start of work on the patent, and it is required to indicate the desired period of activity of the patent (up to 12 months or before the end of the calendar year). It is enough to contact the tax office at the place of registration of the individual entrepreneur. You can submit a document:

- during a personal visit;

- through a representative (by proxy);

- send by mail;

- through the Internet.

- 5 days of waiting for the application to be considered by tax authorities.

- Issue of a patent in the form approved by Order of the Federal Tax Service of the Russian Federation No. ММВ-7-3/599 dated November 26, 2014, or refusal to issue in the form from Order of the Federal Tax Service of the Russian Federation No. ММВ-7-3/957 dated December 14, 2012. Simultaneously with the patent, the individual entrepreneur will receive a certificate stating that he is registered as a PSN payer (letter of the Federal Tax Service No. PA-4-6/22635 dated December 29, 2012).

IMPORTANT! A document confirming payment of tax under the patent system is not provided to the tax office.

NOTE! A newly minted individual entrepreneur can immediately choose a patent taxation system by indicating this in the application. Then he will be issued a patent simultaneously with registration documents.

How to switch to a patent

File a tax application. The deadline is no later than 10 working days before you plan to apply the patent. To switch to a patent from the beginning of the year, submit your application 10 working days before the end of the year. Usually this is mid-December, but in 2021 an exception was made. Regional laws did not have time to be adopted, so the tax office allowed sending applications until December 31 - Letter dated 12/09/2020 No. SD-4-3/ [email protected] ,

Article: How to fill out an application for a Patent

We do not recommend abandoning the simplified approach; let it be a safety net in case some income does not fall under the patent. Otherwise, you will have to report under a complex basic taxation system (OSNO).

Why can the Federal Tax Service refuse a patent?

The tax authority, having considered the submitted application, may not allow the entrepreneur to apply the PSN. There may be the following reasons for this:

- These types of activities do not fall under Art. 346.43 of the Tax Code of the Russian Federation, limiting the use of the patent system;

- the validity period of the patent is indicated incorrectly: it exceeds a calendar year, or this year no activity recognized as patent was carried out, or the conditions for the patent were not met;

- the individual entrepreneur has a tax arrears under the PSN;

- non-compliance with the conditions for PSN (based on the number of hired workers and/or annual income);

- the entrepreneur did not fill out all the required items in the application form.

Patent payment

The payment option for a patent depends on its duration. Clause 2 of Art. 346.51 of the Tax Code of the Russian Federation provides for the following:

- if the patent term is less than six months, the tax is transferred no later than the last day of the patent validity period;

- for a longer patent period:

- during the first 90 days you must pay at least 1/3 of the cost;

- the remaining portion must be transferred before the last day of the patent validity.

In the event of a tax recalculation upon loss of the right to use the patent system and/or deregistration with the Federal Tax Service, the individual entrepreneur must transfer the additional payment amount within 20 days. Read more about how to calculate the value of a patent here.

“No” simplified tax system, “yes” PSN

If an entrepreneur has made a choice in favor of a complete transition to a patent, he will lose the right to use the “simplified version”. In this case, you need to fully pay off the relevant tax payments and report on them:

- Patent tax is paid at the beginning of the quarter in which the entrepreneur loses the right to the simplified tax system.

- If monthly payments under the simplified tax system were not made on time, fines and penalties are calculated for this and they do not apply to the quarter in which the entrepreneur switched to the simplified tax system.

- It is necessary to notify the Federal Tax Service of the termination of the simplified tax system. To do this, the individual entrepreneur has a period of 15 days after completion of the “simplified” work.

- If an individual entrepreneur plans to later return to the simplified tax system, he will have to work in a different tax regime for at least a year (clause 7 of article 346.13 of the Tax Code of the Russian Federation).

Why should I switch to the simplified tax system if I am going to pay a patent?

In connection with the abolition of UTII, many are choosing between a patent and the self-employed regime. If you do not choose the self-employed mode, then we recommend that entrepreneurs, in addition to a patent, additionally switch to a simplified taxation system. This simplifies the life of entrepreneurs if they do not plan to work with VAT.

Our recommendation is for everyone to switch to the simplified tax system. After all, a patent can be lost, and only it is paid for the type of activity that is written in the patent. What if you decide to engage in another type of activity? Unfortunately, this recommendation - to additionally switch to the simplified tax system - is associated with the negative experience of many entrepreneurs with whom we worked. There were too many situations when individual entrepreneurs paid additional large taxes. So, if you chose a patent instead of UTII, still submit an application to switch to the simplified tax system. Now is the time for this! In theory, you simply don’t need the simplified tax system, because you plan to pay taxes according to the patent tax system. But experience says: you need to lay down straw. However, the straw not only makes the blow easier (advantages of using the simplified tax system), but also pricks a little (cons). Let's consider both consequences of applying the simplified tax system.

Advantages of using the simplified tax system 1. Instead of five declarations per year, according to the generally accepted taxation system, you only need to submit one. The fact is that often entrepreneurs do not immediately buy a patent. Upon registration, all entrepreneurs are initially subject to the generally accepted taxation system with VAT and personal income tax. This means that even if they had no income in the period before registering as payers of the patent taxation system, they must submit declarations according to the generally accepted taxation system. This is a VAT declaration until the 25th day of the month following the end of the quarter (or a single simplified declaration until the 20th day of the month following the end of the quarter) and 3-NDFL until April 30 of the following year. There are five declarations in total. The fine for late filing is 1,000 rubles per declaration. Total 5000 rubles. And if you switched to the simplified tax system, then you only need to submit one declaration - before April 30 of the next year. 2. If you suddenly have income that is not subject to payment of a patent, then you will pay taxes according to the selected simplified tax system with the appropriate rate, and not the generally accepted taxes VAT and personal income tax. The total burden, provided that you do not have supporting expenses, will be: with a simplified tax system of 6% - accordingly 6% of the income received, with a simplified tax system of 15% - 15% of the income received, and with the generally accepted taxation system - about 30% of the money received for checking account. Of course, this is rarely thought about, but in practice there are too many such situations. For example, when providing transport services for which a patent was paid, it was necessary to urgently sell the car. These incomes no longer fall under the patent taxation system, which means that taxes from the transaction will be paid in connection with a different taxation system. Another common situation is that the patent is paid for by the store, but a kindergarten or hospital has approached the individual entrepreneur with a request to sell the product, but only by bank transfer. Of course, this is beneficial for the individual entrepreneur. But! Such sales do not fall under the PSN! This means that they will again be subject to other taxes. And you can see their sizes above.

Disadvantage of using the simplified tax system 1. You need to submit a declaration every year. The fact is that if you pay a patent from year to year, then you will not have a period (the beginning or end of the activity) when you switch to a different taxation system, then it is very easy to forget to file a declaration under the simplified tax system. Another situation is when you do not have the listed situations for selling property or selling wholesale. The fine for failure to submit a declaration under the simplified tax system is 1,000 rubles. But even if you forget to submit it every year, it will still be cheaper than paying taxes according to the generally accepted taxation system in the case of the situations described in paragraph 2 of the “pluses”.

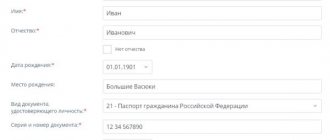

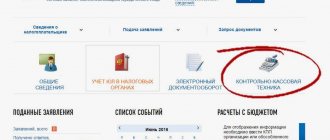

So, even if your planned taxation system is a patent, we still recommend switching to a simplified taxation system by submitting an application. You will see how to fill it out and the form itself in newspaper No. 10 in the article “How to switch to the simplified tax system. In addition, in order not to forget to submit your declaration on time, as well as pay your insurance premiums on time, we invite you to subscribe to the free newsletter on our website. In the “Notifications” section (see Figure 1) you need to indicate (see Figure 2): – your name (so that letters are sent to your name); – for which individual entrepreneur or legal entity you are reporting (for example, individual entrepreneur Ivanov I.I.); – what taxation system you have chosen. There are absolutely all options here, except for a patent. You need to choose from the options provided; – do you employ hired labor and pay taxes on employees? If yes, then you need to indicate the tax payment period - preferably monthly; – email address where letters will be sent; – telephone number (optional); – code – to prove that you are a person and not a program.

After registering, you will receive messages only for your tax system to the specified email. And also important messages for entrepreneurs, for example: check yourself in terms of inspections on the website of the Prosecutor General's Office with a link to the plan itself. This must be done annually, so you will also receive this message. Messages will be of three types: – you need to submit a declaration; – you need to pay tax; – you need to check yourself on the website of the prosecutor’s office, the statistics committee, etc. For each important event for you, you will receive a message twice a week before the hour “X” and 2 days before. Experience has shown that entrepreneurs quickly forget everything within a week. The service is absolutely free and operates throughout the country, because tax legislation in Russia is the same for everyone. We hope that our service will be useful to you! Well, before December 31, don’t forget to submit an application to switch to the simplified tax system!

Nadezhda Skvortsova Director of Regional Tax Consultation LLC, Editor-in-Chief of “Practical Newspaper for Entrepreneurs”