Let's study how to correctly account for input VAT when purchasing fixed assets in 1C 8.2 using an example.

Let’s say that CJSC “PK Shtorkin Dom” acquires fixed assets that will later be used in business activities. One fixed asset is immediately put into operation. Two other facilities remain uncommissioned at the end of the current quarter. All documents for capitalization of fixed assets are available, and invoices are also available. The organization, in turn, if all conditions are met, can claim such “input” VAT for deduction. It is necessary to calculate the VAT deductible and check the VAT entries. You should also check the entries in the VAT accumulation registers, create a purchase book and check the VAT calculation. To do this, in 1C 8.2 you need to formalize the following operations:

- Operation No. 1 for the acquisition of OS, registration of the “input” invoice.

- Operation No. 2 to commission the OS.

- Operation No. 3 for the acquisition of OS, registration of the “input” invoice.

- Create a purchase book and check its completion.

Parameters for operation No. 1:

Parameters for operation No. 2:

Parameters for operation No. 3:

Features of filling out documents for the receipt of fixed assets in 1C 8.2

Features of filling out the document “Receipt of goods and

Features of filling out the document “Invoice received”

register an “input” invoice by clicking on the link Enter an invoice in the lower field of the document Receipt of goods and services . The Reflect VAT deduction is not selected upon receipt of fixed assets, intangible assets, and equipment:

Postings for VAT accounting when purchasing fixed assets in 1C 8.2

According to accounting

Invoice document upon capitalization of fixed assets does not create postings and movements in VAT accumulation registers. The necessary entries for accounting for “input” VAT are generated by the document Receipt of goods and services:

For tax accounting

The following entries were created in the VAT accumulation register:

- Entry by movement type Receipt in the VAT register presented – event Presented by VAT supplier . This entry is a potential purchase ledger entry:

- Entry by the type of movement Receipt in the VAT register for acquired assets , type of value of fixed assets - for tax amounts accepted for accounting related to a specific batch of fixed assets:

- Entry by the type of movement Receipt in the VAT register for fixed assets, intangible assets , type of value of fixed assets . The tax amounts accepted for accounting on purchased fixed assets are registered in order to track the conditions under which these tax amounts can be accepted for deduction:

VAT refund

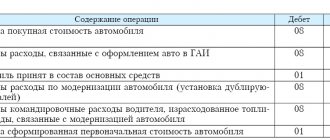

Example ZAO Aktiv purchased a machine that required installation for a new workshop. The cost of the machine, according to the contract, is 236,000 rubles. (including VAT - 36,000 rubles). The cost of services of a transport organization for delivery of the machine to the warehouse amounted to 11,800 rubles. (including VAT - 1800 rubles). The Aktiva accountant must make the following entries: Debit 07 Credit 60,200,000 rubles 0) - a machine requiring installation has arrived at the Aktiva warehouse (excluding VAT); Debit 19 Credit 60 RUB 36,000. — the amount of VAT according to the seller’s invoice is taken into account; Debit 60 Credit 51,236,000 rub. — the seller’s invoice has been paid; Debit 07 Credit 60 10,000 rub. (11,800 - 1800) - transportation costs are taken into account in the cost of the machine (excluding VAT); Debit 19 Credit 60 1800 rub. — the amount of VAT is taken into account according to the invoice of the transport organization; Debit 60 Credit 51 11,800 rub. — the invoice of the transport organization has been paid. Thus, on account 07 the cost of the machine intended for installation (assembly) in the new workshop is formed. It amounted to 210,000 rubles. (200,000 + 10,000).

If your organization received equipment that requires installation as a contribution to the authorized capital, then you must make the following entry: Debit 07 Credit 75-1 equipment received as a contribution to the authorized capital is capitalized (in the assessment agreed upon by the founders). For more details, see account 75 “Settlements with founders”, situation “Settlements with founders for contributions to the authorized capital of CJSC, OJSC, LLC”.

Postings for commissioning of fixed assets in 1C 8.2

According to accounting

When commissioning fixed assets, VAT accounting entries are not created:

For tax accounting

The following entries were created in the VAT accumulation register:

- Entry by type of movement Expense in the VAT register for fixed assets, intangible assets , type of value of fixed assets . The tax is written off from the register, because the conditions for accepting “input” VAT for deduction are met:

- in the VAT register for acquired assets with the movement type Expense , type of asset value. VAT is written off from the register at the time of commissioning:

Input VAT when purchasing fixed assets in the purchase book in 1C 8.2

Creating and filling out the document “Creating purchase ledger entries”

- Creating a document in the menu: Purchase – then select Maintaining a purchase book – then Generating purchase book entries;

- In the From – the end date of the tax period. Because The tax period is a quarter, then in our example the document date is 03.2013. ;

- When registering in the purchase book of invoices for received fixed assets from suppliers, the tab Deduction of VAT on purchased assets .

“Input” VAT on fixed assets that have not been put into operation will not be deducted, and these VAT amounts will not be included in the purchase book.

In our example, three fixed assets were capitalized, of which only one object, the Ford Tourneo Connect, was put into operation in the first quarter . Thus, the “input” VAT only for this object will be reflected in the purchase book. For the second object, the “input” VAT will be written off, and for the third object there will be a balance of “input” VAT at the end of the quarter:

- Accounting system: by debit of account 19.01;

- Well: VAT accumulation register, is a potential entry in the purchase book:

nds_pri_pokupke_os.jpg

On February 20, 2021, a taxpayer company purchased a used car with a faulty engine. The vehicle was transferred to the buyer along with an invoice in the amount of RUB 472,000. (including VAT RUB 72,000). On March 1, an engine was purchased at a car dealership 2021, which was immediately installed. Its price, together with the cost of work according to the invoice, amounted to 200,600 rubles. (including VAT RUB 30,600). On March 1, the car was ready for work.

Example: VAT deduction on the purchase of fixed assets

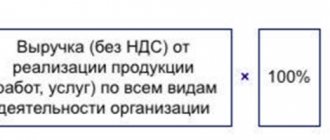

For example, VAT on the sale of fixed assets is charged on the full amount of the sale if the asset was purchased from a defaulter and was accounted for without VAT. If upon purchase the tax was taken into account in the price of the object, then when selling it, VAT is calculated on the difference in cost at a rate of 18/118. The cost of sales of fixed assets is fixed in the structure of general income, the residual value of assets is recorded in other expenses.

24 Oct 2021 stopurist 44

Share this post

- Related Posts

- What is a safe deposit box when buying an apartment?

- I Inherited A Dacha Can Sberbank Take It For Debts

- Does a pensioner have a land tax benefit?

- Benefits for the birth of the first child on a mortgage

Postings for accepting “incoming” VAT for deduction when commissioning the OS in 1C 8.2

According to accounting

When you include in the document Formation of purchase ledger entries records on the acceptance of “input” VAT for deduction on transactions of receipt and commissioning of OS in 1C 8.2, transactions are created for the debit of account 68.02: Dt 68.02 Kt 19.01 – for the amount of “input” VAT accepted for deduction :

For tax accounting

The following entries were created in the VAT accumulation registers:

- in the VAT register presented with the type of movement Expense. The “input” VAT is written off from the register at the time it is included in the purchase book:

- in the VAT Purchases , which generates the lines of the Purchase Book report:

The relationship between fixed assets and separate VAT accounting

The concepts of “fixed assets” (FP) and “separate accounting” (SA) are used jointly by companies and merchants:

- carrying out VAT-taxable and non-VAT-taxable activities;

- having fixed assets on the balance sheet.

Separate accounting greatly helps an enterprise to understand the value added tax, which is paid when an enterprise acquires fixed assets:

- include it as part of the deduction (in the case when fixed assets are used in taxable activities);

- increase the initial cost of fixed assets by the amount of VAT (this is the case when fixed assets are used in non-taxable activities);

- distribute VAT: include part of its amount in the cost of fixed assets, and take part for deduction (this is only if fixed assets are used simultaneously in both taxable and non-taxable activities).

Checking the calculation of “input” VAT for deduction when purchasing fixed assets in 1C 8.2

Step 1. Reconciliation of the balance of “input” VAT on fixed assets that have not been put into operation, in the context of accounting records

When purchasing fixed assets, assets are debited to account 08.04. When putting the operating system into operation, they transfer their value from the credit of account 08.04 to the debit of account 01.01. Thus, for fixed assets that have not been put into operation, at the end of the period there remains an account balance of 08.04.

In order to view the balance on account 08.04, you can create a turnover balance sheet for the account in the context of fixed assets. From the SALT it is clear that two fixed assets have not been put into operation, therefore the “input” VAT, which was recorded on account 19.01 for these objects, should also be recorded as a balance on this account.

To check, we will create a balance sheet for account 19.01 for counterparties and receipt documents. You can reconcile the balance of “input” VAT on operating systems that have not been put into operation in different ways: by reconciling with primary documents; arithmetic way, etc.

Let's check the data using our example:

- Let's check the balance of the “input” VAT on account 19.01 arithmetically:

- Account balance 08.04 = 46,525.42 rubles. - price without VAT;

- Calculation of “input” VAT = 46,525.42 * 18% = 8,374.58 rubles.

- The account balance of 19.01 at the end of the period is the same.

- According to the accounting system, operations to deduct “input” VAT on purchased fixed assets are reflected correctly.

Step 2. Reconciliation of the balance of “input” VAT on fixed assets that have not been put into operation, in the context of NU

Potential purchase ledger entries are generated in the VAT accumulation register presented

.

When the OS was received, an entry was made in this register with the form Receipt.

An entry with the type

Expense

is made at the moment the “input” VAT is included in the deduction or the “input” VAT is written off as expenses. Therefore, there must be a balance for “input” VAT on fixed assets that have not been put into operation at the end of the period.

We will generate information reflected in the VAT accumulation register presented

(menu

Reports

–

Other

–

List \ cross-table

– VAT accounting section

presented

). Let's check the data from our example:

- According to the NU, the amount of the balance in the VAT register presented is equal to the balance on account 19.01 according to the accounting system

- NU = BU = 8,374.58 rubles.

- “Input” VAT on received fixed assets in the first quarter was taken into account correctly.

On the PROFBUKH8 website you can read other free articles and video tutorials on the 1C Accounting 8.3 (8.2) configuration:

Full list of our offers:

Please rate this article:

Registered users have access to more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP

Registered users have access to more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP

I am already registered

After registering, you will receive a link to the specified address to watch more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP 8 (free)

By submitting this form, you agree to the Privacy Policy and consent to the processing of personal data

Login to your account

Forgot your password?

How to claim VAT on fixed assets or equipment for deduction

Fixed assets subject to state registration deserve special attention: buildings, structures and other real estate. As noted above, one of the conditions for obtaining a VAT deduction on fixed assets is the registration of these objects and documentary confirmation of this fact, as stated in paragraph 1 of Art. 172 of the Tax Code of the Russian Federation. Confirmation of the registration of such objects is a signed acceptance certificate. VAT deduction can be claimed during the period of signing the relevant act and without waiting for state registration.

Objects purchased by an enterprise can be immediately suitable for use in production activities and do not require assembly or installation. In this case, VAT on fixed assets is deducted during the period of registration of the object.