Repair, reconstruction and modernization of the OS

During operation, organizations have to bear costs to ensure the functioning of fixed assets. The ways in which these costs are reflected in accounting depend on their essence, so it is important to define concepts such as modernization, reconstruction and repair:

- According to paragraph 2 of Art. 257 of the Tax Code of the Russian Federation, modernization includes work that results in a change in the technological or service purpose of a fixed asset, as well as an increase in its capacity, performance, or the appearance of new qualities.

- Reconstruction is a reorganization of the operating system, which improves the results of its work, allows you to increase the variety of products produced, improve their quality or quantity. Also, the Tax Code of the Russian Federation uses the concept of “technical re-equipment”, which is associated with the use of the latest technologies and automation of production.

NOTE! These two concepts are united by the fact that as a result the fixed asset acquires improved performance or new functions.

- During repairs, technical and economic indicators do not improve, but remain the same. Its essence comes down to eliminating faults that have arisen or replacing worn parts.

How does a major overhaul differ from reconstruction and modernization? The answer to this question is in the ConsultantPlus legal reference system. If you have access to K+, proceed to the Typical Situation. If you don't have access, get trial access to the system for free.

See also “The workshop is turning into a warehouse and office - is this a renovation or reconstruction?” .

According to clause 14 of the accounting regulations “Accounting for fixed assets” PBU 6/01, approved by order of the Ministry of Finance of Russia dated March 30, 2001 No. 26n, and clause 2 of Art. 257 of the Tax Code of the Russian Federation, the costs of modernization, reconstruction, technical re-equipment and other changes of this kind (we will further use the word “modernization” to refer to them) increase the initial cost of fixed assets.

Unlike modernization expenses, expenses for repairs of fixed assets do not affect the value of property and are classified as other expenses in tax accounting (Clause 1, Article 260 of the Tax Code of the Russian Federation). In accounting, repair costs are included in the maintenance costs of the unit in which the fixed asset is operated.

From 2022, PBU 6/01 will no longer be in force. Instead, FSBU 6/2020 “Fixed Assets” should be used. The standard can be applied earlier by fixing the decision in the accounting policy of the enterprise.

An overview of changes to the new Federal Accounting Standards was prepared by ConsultantPlus experts. Study the material by getting trial access to the K+ system. It's free.

How is it different from reconstruction and repair of the OS?

OS reconstruction is considered to be a complete, radical change in the parameters of the object being taken into account.

This procedure helps modify the results of using a technical device.

It allows you to achieve a variety of products, significantly improve their properties, and increase production volumes.

In addition, the Tax Code of the Russian Federation contains the concept of “technical re-equipment”, which means the introduction of new, progressive production methods and depreciation of capital equipment.

A common point for the modernization and reconstruction of the operating system is the fact that the corresponding object ultimately acquires improved properties, becomes more productive, and allows the production of products with improved characteristics.

Current and capital repair work. Current ones are regularly carried out at the enterprise in relation to the OS and do not lead to an improvement in any technical parameters, functional properties or consumer characteristics. On major repairs of fixed assets.

All these points remain at the same level as a result of the repair.

The essence of this event is to eliminate the malfunctions that have arisen, eliminate the resulting breakdowns of the fixed asset, replace spare parts and components that have exhausted their service life or are completely out of order.

Another distinctive feature of repair work is the procedure for recording the corresponding expenses, carried out for both tax and accounting purposes.

Thus, according to a generally binding regulatory act regulating the accounting procedure for fixed assets, the costs of reconstruction, modernization or other re-equipment of fixed assets lead to an increase in the primary cost of the corresponding objects.

As for restoration (repair) costs, this category of costs does not in any way change the final cost of the objects.

In tax accounting, for example, repair costs are classified as other costs by default. This norm is established by the Tax Code of the Russian Federation (Article 260).

If we talk about accounting for repair costs, then these costs are always included in the costs associated with the need to maintain a specific unit using the object being restored.

Documentation - what documents need to be completed?

If the management of an organization decides to modernize the OS, it issues an order with the appropriate content.

This document must contain information about the responsible persons, the timing of the activities, and the reasons for the procedure.

If the modernization is entrusted to a third party (organization), an agreement is concluded with the contractor regulating all the nuances of this procedure.

When the modernized object is transferred to a contracting structure to carry out the work provided for in the contract, the parties draw up a special act recording the transfer and receipt of the device.

If the item being improved is transferred for work to a specific unit related to the structure of the company itself, a special invoice is drawn up certifying the fact of the intra-organizational movement of the object.

For registration, the standard form OS-2 can be used. If the modernization does not imply a change in the location of the technical device, there is no need to draw up any papers.

When the modernization is completely completed, an act is drawn up certifying the acceptance and transfer of the object in an improved condition. This form can be prepared according to the standard form OS-3.

This paper must be drawn up in any case, regardless of the method of modernization.

At the same time, for the economic method of performing the relevant work, the form of such an act is filled out in a single copy, and when carrying out activities by contract - in two copies, that is, one form for each of the parties.

Accounting and postings

Accounting for modernization is carried out by the enterprise according to the standard “Accounting for fixed assets” (PBU 6/01). For these purposes, this regulation provides for the use of account 08 – “Investments in non-current assets”.

If the need arises, it is advisable to create separate subaccounts for account 08 that take into account the costs of modernization.

Accounting entries that are often used when accounting for the costs of modernizing fixed assets are shown in the table below:

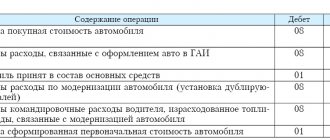

| Operation | Account debit | Account credit |

| Reflects the costs of purchasing materials for upgrading the facility | 08 | 10 |

| The costs of auxiliary production of the enterprise are reflected | 08 | 23 |

| The costs of paying for the contractor's services are taken into account | 08 | 60 |

| The amount of VAT is taken into account when using the contract method | 19 | 60 |

| The amount of VAT is calculated based on the business approach | 08 | 68 |

| The amount of VAT is taken into account in the business approach | 19 | 08 |

| Amount of VAT to be deducted | 68 | 19 |

| The primary cost of a specific OS object increases | 01 | 08 |

Tax accounting

Tax accounting of expenses for equipment modernization differs from accounting of these costs in the following aspects:

- Expenses that directly lead to a change in the primary cost of the modernized object may differ significantly in accounting carried out for accounting and tax purposes.

- Accounting allows the use of only one approach to calculating depreciation - linear. Tax accounting provides a choice of two possible methods - linear and non-linear.

- From an accounting point of view, modernization increases the useful life of the corresponding facility - no restrictions are provided in this aspect. As for tax accounting, in this area changing this deadline is not mandatory. For tax purposes, the differentiation of modernized fixed assets into depreciation groups is regulated, each of which provides for a strictly defined maximum permissible period.

How to modernize a fully depreciated object?

Sometimes there is a need to upgrade equipment that has zero residual value. We are talking about fixed assets for which the depreciation procedure has been completely completed.

Current standards do not provide specific guidance for this situation.

Thus, the corresponding costs should be taken into account by analogy with ordinary OS objects:

- An increase in the primary cost of depreciated equipment by the amount of costs associated with modernization.

- Audit of the useful life of the facility.

- Determining the amount of annual depreciation (new data is taken into account).

Modernization of fixed assets - postings

According to clause 42 of the Guidelines for accounting of fixed assets, approved by order of the Ministry of Finance of Russia dated October 13, 2003 No. 91n (hereinafter referred to as the Guidelines), account 08 “Investments in non-current assets” is used to account for modernization costs.

Read about how to account for fixed assets worth less than 100 thousand rubles here.

Upon completion of the work, the costs are included in the cost of the fixed asset or are accounted for separately on account 01 “Fixed assets” in the subaccount “Modernization of fixed assets”.

OS modernization is reflected in postings as follows:

- Dt 08 Kt 10, 60, 69, 70, 76 - modernization costs are collected;

- Dt 01 Kt 08 - when modernizing a fixed asset, this posting indicates an increase in its original cost.

For organizations with a large number of assets, it is also important to pay attention to analytical accounting.

To break down existing investments in non-current assets by type, a separate sub-account “Modernization costs” is opened on account 08 for the OS being modernized. On account 01 it is convenient to create a separate sub-account, where only objects that are in the stage of modernization will be listed, for example, “Fixed assets for modernization”.

When transferring fixed assets for modernization, the posting for their internal movement will be as follows:

Dt 01 subaccount “Fixed assets for modernization” Kt 01 subaccount “Fixed assets in operation”.

Accounting

The costs of modernizing fixed assets change (increase) their initial cost in accounting (clause 14 of PBU 6/01).

The organization is obliged to keep records of fixed assets according to the degree of their use:

- in operation;

- in stock (reserve);

- on modernization, etc.

This is stated in paragraph 20 of the Methodological Instructions, approved by order of the Ministry of Finance of Russia dated October 13, 2003 No. 91n.

Accounting for fixed assets by degree of use can be carried out with or without reflection on account 01 (03). Thus, during long-term modernization, it is advisable to account for fixed assets in a separate sub-account “Fixed assets for modernization”. This approach is consistent with paragraph 20 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia dated October 13, 2003 No. 91n.

Debit 01 (03) subaccount “Fixed assets for modernization” Credit 01 (03) subaccount “Fixed assets in operation”

– fixed assets were transferred for modernization.

After completing the upgrade, make the following wiring:

Debit 01 (03) subaccount “Fixed assets in operation” Credit 01 (03) subaccount “Fixed assets for modernization”

– a fixed asset adopted from modernization.

See also about entries in accounting for repairs of fixed assets

Modernization of depreciated fixed assets

OSes that are already fully depreciated and have a residual value of zero are often upgraded. There is no specific guidance in the regulations on how modernization costs should be taken into account in such a case. So you should proceed similarly to the general principle:

- In accounting, increase the initial cost by the amount of modernization costs. The residual value will be equal to the amount of modernization costs.

- Review the JPI, estimating how much longer the facility will be used, taking into account the work performed.

- Calculate annual depreciation based on new data.

How to take into account the modernization of a fully depreciated operating system in tax accounting, read here .

Tax accounting for modernization of fixed assets

According to paragraph 2 of Art. 257 of the Tax Code of the Russian Federation, modernization costs increase the initial cost of fixed assets, which continues to be repaid by depreciation.

Make sure you correctly distinguish between fixed asset repairs and upgrades for income tax purposes. Get trial access to K+ for free and proceed to expert explanations.

Example 2

On 04/05/2020, the organization modernized the machine. The cost of the work performed by the contractor was 130,000 rubles.

The useful life has not changed. The work lasted less than a year, depreciation was accrued all the time.

The initial cost of the object is 900,000 rubles. It belongs to the 3rd depreciation group. SPI - 5 years (60 months).

For tax accounting purposes, the monthly depreciation rate will be: 1 / 60 × 100% = 1.6666%.

Monthly depreciation amount: 900,000 × 1.6666% = RUB 15,000.

Initial cost of the modernized facility: 900,000 + 130,000 = 1,030,000 rubles.

In tax accounting, the amount of depreciation per month after modernization: 1,030,000 × 1.6666% = 17,167 rubles.

The Tax Code of the Russian Federation also provides for the possibility of increasing the useful life of an operating system if, after modernization, it can be used longer than the established period. According to paragraph 1 of Art. 258 of the Tax Code of the Russian Federation, it is possible to increase the SPI within the depreciation group to which the fixed asset belongs. If the SPI is equal to the upper limit of the depreciation group, it cannot be increased after modernizing the fixed asset.

You will learn about other nuances of tax accounting of fixed assets from the article “Procedure for tax accounting of fixed assets.”

Accounting

In accounting, modernization costs are included in the cost of fixed assets (PBU 6/01 clause 14). Investments in OS modernization flow into the account. 08, as a rule, with the opening of a corresponding sub-account. On the account 01, with whom the account subsequently corresponds. 08, a sub-account “OS Modernization” can also be opened, however, quite often the costs are taken into account directly in the cost of the modernized OS. Amounts are allocated in a subaccount, as a rule, if the number of fixed assets and the scale of modernization work are large enough.

Typically, accounts correspond here like this:

- Dt 08 Kt 10, 23, 60, etc. – write-off for modernization of inventory items, services of auxiliary production, works (services) of third-party organizations.

- Dt 01 Kt 08 – the cost of the operating system has been increased for modernization costs.

The accountant needs to remember: interest on the loan, if the funds were taken for the modernization of the operating system, are included in the costs and increase the book value of the modernized object. This is the position of the Ministry of Finance.

If subaccounts are used, when transferring for modernization, an internal transfer is made Dt 01/subaccount “Assets for modernization” Kt 01/subaccount “Assets in operation”. Similar to account 01, account 03 may be involved in postings when it comes to upgrading an OS object provided for temporary possession or use for a fee, used to generate income. Example: a building that is intended exclusively for rental.

Modernization is documented in the following documents:

- operating schedule;

- cost estimate;

- work orders, contracts for the performance of work, services (depending on how they were performed - on their own or with the involvement of third-party companies);

- acts of work execution;

- invoices, etc.

Materials are sold according to invoices, requirements, and limit cards. The increase in the cost of fixed assets as a result of modernization is reflected in the inventory card of the fixed asset.

By the way! Modernization and reconstruction are terms that are similar in meaning, but not identical. Modernization is always associated with work leading to changes in the technological and service purpose of the OS. The OS object is transformed into a more modern, more powerful one with improved qualities. Reconstruction is the reorganization of the operating system in order to increase the technical and economic indicators of product production: changing the assortment, improving quality, increasing production volume. These nuances follow from Art. 257-2 Tax Code of the Russian Federation. Repair is aimed at restoring worn-out operating systems; it is not directly related to fundamental improvements of objects.

Results

Important points when accounting for OS modernization are the separation of the concepts of “repair” and “modernization” and the organization of convenient analytical accounting. It is also necessary to take into account the differences in accounting and tax accounting for the modernization of fixed assets, which will require the accountant to take action to ensure the correct reflection of temporary differences.

Read more about all the nuances of fixed asset accounting in this article.

Sources:

- Tax Code of the Russian Federation

- Order of the Ministry of Finance of Russia dated March 30, 2001 No. 26n

- Order of the Ministry of Finance of the Russian Federation dated October 13, 2003 No. 91n

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.