What it is

According to the new federal standard, approved by Order of the Ministry of Finance No. 257n dated December 31, 2016, the residual value of fixed assets is an indicator of property assets in the current period.

It is formed after deducting depreciation charges and impairment losses. According to accounting standards, the residual value of fixed assets is determined as the accounting price for a specific date (end of the reporting period) - the original price reduced by the amount of accrued depreciation. Knowing the value of assets by balance, management sees the degree of their moral and physical deterioration and, accordingly, their efficiency of use. This allows you to plan the current renewal of the institution’s material and property funds.

Why do you need to calculate the average value of property?

Property (fixed assets) constantly changes its residual value, gradually transferring it to the products produced by the organization or the work performed or services provided. At the same time, their material, “material” form is preserved. Therefore, constant accounting and adjustment of their value in the balance sheet is necessary, which will reflect both the form of the asset and the amount of “transferred” value (depreciation).

In addition, since fixed assets (fixed assets) are dynamic, during the reporting period they can:

- change your qualitative state;

- get an “upgrade” and thereby increase the value;

- become obsolete physically and morally;

- change the total volume (the organization wrote off, sold or acquired property assets).

IMPORTANT! It follows that at the beginning of the reporting year, the residual value of fixed assets may differ sharply from the indicators at the end of this period. That is why average values are used in calculations, which increases the accuracy and reliability of accounting and reflection of the value of funds on the balance sheet.

In addition to the immediate tasks of accounting, the value of the organization’s property, determined as the average value for the selected period, is used for taxation purposes. This indicator represents the taxable base for corporate property tax. On its basis, the amount of advance quarterly payments and the final annual payment is calculated (clause 1 of Article 375 of the Tax Code of the Russian Federation), it forms the basis of the declaration for this tax.

Signs of initial and residual value

Non-current assets are characterized by various types of valuation, such as initial and residual value. The initial price is understood as the price that is paid for the fixed asset at the time of its acquisition. It is determined by a number of characteristics, which together form the price of the property:

- the direct price of the fixed asset itself;

- transportation costs;

- taxes, customs duties and duties;

- estimated cost of services for commissioning equipment.

The initial estimate is a constant value. It remains unchanged from the moment of acquisition and registration of the fixed asset and for the entire period of its use, except in cases of revaluation of the asset (revaluation or discount), its modernization or liquidation.

Residual value is a variable value. It decreases monthly as a result of depreciation charged on the original price. This is an indicator that is necessary to determine the current technical and moral condition of the main property.

The initial assessment is the indicator by which an object is accepted for accounting, and the residual assessment is a value characterizing the condition of the object during the period of its use.

Cadastre and average annual

The current tax legislation provides for the possibility of determining the property tax base in two ways:

- at cadastral value;

- at average annual cost.

The cadastral value is used only to calculate tax for certain types of objects. For example, this method is suitable for calculating tax for administrative, business and shopping centers (complexes) and individual premises in them, for buildings used to simultaneously house offices, retail facilities, catering and consumer services, office premises, etc. (Article 375, 378.2 of the Tax Code of the Russian Federation).

In other cases, the average annual value of the property is used to calculate property taxes.

Methods for calculating residual value

The value of the object by balance is calculated monthly - as of the time of reporting, based on the results of the inventory, or at the end of the period determined by the accountant. In addition to the initial and residual costs, replacement costs are also distinguished. It is determined only for those objects for which revaluation was organized at the reporting date.

Here is a formula that shows how to calculate the residual value of fixed assets:

In the formula:

- OSB(B) - initial, replacement cost. When using this formula to determine the operating cost, the organization does not have the right to choose between the initial and replacement cost. The replacement value is used if a revaluation was previously carried out for specific fixed assets, which determined the replacement value of the assets. In accordance with clause 15 of PBU 6/01, revaluation is carried out once a year as of December 31 of the reporting year;

- A is depreciation accrued at the reporting date.

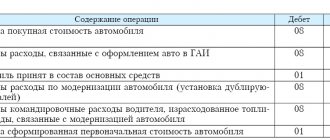

Here's how to determine the residual value of fixed assets when calculating the indicator using analytical accounting accounts:

The debit of account 01 takes into account the initial and replacement cost, and the debit of account 02 takes into account the depreciation accumulated on the calculation date. To make correct calculations, from the aggregate data of account 02, it is necessary to subtract the depreciation that was accrued on the funds accounted for in account 01, since the Kt of account 02 also takes into account the depreciation of fixed assets carried out under 03 “Income-bearing investments in material assets” (Order of the Ministry of Finance No. 94n dated October 31, 2000).

Depreciation charges are determined for all types of fixed assets. The rules for their calculation are enshrined in PBU 6/01. Depreciation for intangible assets is calculated in accordance with the procedure established by PBU 14/2007.

Negative result of the sale of fixed assets

Often in practice, the taxpayer is forced to sell one or another fixed asset item before the end of its service life. The reasons for this can be very different: one of the business lines has closed, the maintenance of the facility has become unaffordable, the car was involved in an accident and it is more profitable to sell it than to repair it.

Unfortunately, the sale of a fixed asset does not always produce a positive financial result. It happens that an object is sold at a loss, the reflection of which in tax accounting has its own characteristics. Which? Read in this article.

Features of reflecting losses from the sale of fixed assets: general procedure...

On the date of the transaction for the sale of depreciable property, the taxpayer determines profit (loss). Profit is subject to inclusion in the tax base in the reporting period in which the property was sold. The loss is reflected in analytical accounting as other expenses in accordance with the procedure established by Art. 268 Tax Code of the Russian Federation

.