Accounting for workwear and special equipment. inventory is strictly regulated by the legislation of the Russian Federation. Based on these standards, records are kept in the 1C Accounting 8.3 program.

In order to reflect the transfer of such materials and other low-value materials into operation, there is a document of the same name, which is located in the “Warehouse” section. Please note that materials must be received at the warehouse before they can be written off. This can be reflected in different ways, for example, by registering the purchase of documents “Receipt (Act, invoice)”.

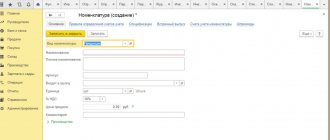

Workwear

First of all, let's fill out the header of the document. In it we will indicate the organization Roga LLC, the warehouse and the division where the materials are located.

Please note that this document allows you to transfer into operation at the same time special clothing, special equipment, as well as equipment and household supplies. In our case, the details for all groups of materials will be the same, so the data will be contained in the same document, only on different tabs.

Our team provides consulting, configuration and implementation services for 1C. You can contact us by phone +7 499 350 29 00 . Services and prices can be seen at the link. We will be happy to help you!

Let's consider the example of the commissioning of seven safety helmets and five jackets for construction workers. We will issue them to our employee Gennady Sergeevich Abramov. In the future, it is he who they will be listed as. These materials are special clothing, so we will indicate them on the first tab of the same name in the document.

Please note that both safety helmets and jackets for construction workers are workwear, which must be indicated in the item data cards.

To correctly reflect these materials in accounting, it is very important to correctly indicate the purpose of use in the corresponding column of the tabular section. The data here is selected from a special directory of the same name, which you can fill out yourself.

In our example, the intended use of safety helmets is “Helmets for construction workers”. We filled out all the data ourselves. In our example, the cost of safety helmets will be repaid on a straight-line basis over the entire useful life. It is 11 months.

We will reflect this type of expense on account 25. Depending on the work regulations at your enterprise, the invoice may be different.

Please note that in accordance with current legislation, workwear with a useful life of less than a year can be written off at a time. In our example, the terms for safety helmets and jackets for construction workers are less than 12 months.

After entering all the necessary data into the document, it can be processed. The resulting wiring in our example is shown in the figure below.

Transferring materials into operation in 1C 8.3 - step-by-step instructions

Let's consider the sequence of writing off inventories in the accounting of an enterprise when using the software solution - “1C: Accounting”.

You need to start by issuing materials in the “Transfer to Operation” section, the section is located in the “Warehouse-Workwear and Equipment” menu.

Items of the MPZ category are reflected in special account 10.10 designated as “Working clothing and special equipment in the warehouse.” After creating the balance sheet, it is easy to note that the balance sheet shows reflective vests in the amount of 10 pieces and insulated suits in the amount of 15 pieces.

The next step is to reflect the transfer of items into operation. To do this, create a document of the same name by pressing the “Create” button in the document log.

First, fill out the header of the document and enter basic data - location of materials, organization and warehouse where the transfer is made. The selection button allows you to add items. After which the number of items and the responsible person are indicated, the purpose of operation is filled out. The next step is to contribute funds to cover the cost and reflect expenses. The period of active use, calculated in months, must be indicated.

The service life of the company's materials is regulated by the Labor Code. The duration of operation is determined depending on the specialty of the employee, the activities of the organization, and climatic conditions. Thus, a jacket and trousers with special inserts, such as membranes reinforced with an insulated lining, are used for at least three years. After which the protective clothing is replaced. Winter boots are issued for up to four years. Clothing without membranes, reinforced with lining, must be replaced every two years. When issued, the boots have a two and a half year shelf life.

In accordance with the cost parameters and basic service life of workwear, which is necessarily taken into account in the MPZ, items are conditionally divided into categories:

The first group includes items with a period of active use of up to 12 months. The write-off operation is performed at a time, and the cost does not play a decisive role;

The second group takes into account goods with a useful life of more than one year. These positions are not included in working capital due to the cost criterion; for this reason, repayment of the cost is required in accordance with the terms of use in a straight-line manner.

It is important to take these features into account when entering information about the intended use. For example, a reflective vest has been in use for less than 12 months, which requires write-off in accordance with the rules of the first group.

The cost of items from the second group is written off proportionally over the entire period of use. At the same time, a one-time write-off is made in the accounting system, causing the emergence of a temporary difference.

There is another suppression option, used exclusively in relation to special equipment. In this case, they proceed from the volume of products or work done or services provided in equal proportions. When using this method, monthly data entry into the “Material Development” document is required.

In this case, the item “Method of reflecting expenses” shows the accounting settings.

Then you can proceed to posting the document. You can check the generated transactions by clicking on the menu item “Show transactions and other movements on the document.” From this document it is possible to print out the “Issue Statement”, and, if necessary, the “Requirements-Invoice”.

In this way, transactions will be generated for two balance sheet accounts: 10.11 and 10.10 and the debit of off-balance sheet accounts used to record valuables. And the cost of the reflective vest will be repaid upon commissioning.

In this case, the repayment of the cost of workwear in accordance with the method of reflection will be made only in tax accounting. For this reason, a temporary difference will appear between accounting and tax data.

The temporary difference is noted in the first month of repayment of the book value of workwear and is subsequently written off, i.e. will be repaid during the entire period of use of the material.

Special equipment

Special equipment includes special equipment, tools and devices. The features of its accounting and the rules for classifying materials into this group are strictly regulated and approved by order of the Ministry of Finance of the Russian Federation No. 135n dated December 26, 2002.

In this example, we need to put into operation a mold for casting chocolate Santa Clauses. We will enter this data into the previously created document, since both the transfer date and the rest of the header details will match.

In the tabular section on the “Special equipment” tab, almost the same data is indicated as in the case of special clothing. In this case, only the transfer count 10.11.2 will differ. The program will fill in some data automatically. To do this, it is important to indicate in the nomenclature card that the “Santa Claus” uniform is special equipment.

The document will generate movements similar to the case with workwear, only in this situation the off-balance sheet account MTs.03 is also used.

The procedure for writing off materials

To write off material assets, the creation of a special commission is required. It consists of financially responsible persons, as a rule, from different structural divisions of the enterprise. It is their responsibility to identify and examine damage, defects or malfunctions of equipment, machinery, furniture, household equipment, tools and other valuables contained on the organization’s balance sheet.

After recording such facts, they are authorized to draw up an act of write-off of materials. As a rule, in large organizations there are specially developed clear instructions for such actions.

To write off materials, there must be compelling reasons with documentary evidence.

Write-off of materials cannot occur without compelling reasons, confirmed by a certain evidence base. In particular, during the procedure for writing off materials, supporting documents can be used.

So this is:

- reports on products produced over a certain period (its volume, names, etc.);

- reports from financially responsible persons on the material assets used;

- written documents on the consumption of materials in excess of established standards (with justification for these facts);

- approved calculation according to material cost standards for the manufacture of a unit of goods;

- other financial and accounting documents.

Before writing off material assets, the enterprise must conduct an inventory of property and enter its results into the relevant documents.

Inventory and household items accessories

The last tab will reflect the commissioning of the office organizer. We took it to the inventory and household items. accessories. Filling out the tab is similar to the previous examples.

In this situation, in the way of reflecting expenses, we indicated that repayment of the organizer will occur when it is put into operation. We will attribute the costs for it to general business expenses in account 26. You can use another account for accounting.

It is especially important to correctly fill out and configure the methods for reflecting expenses in 1C 8.3.

The document formed only two movements to transfer the office organizer as equipment into operation. In this case, the off-balance sheet account MTs.04 is used.

Basic rules for drawing up a water act for operation

This document does not have a unified, mandatory form, so it can be compiled either in free form or according to a template developed and approved within the enterprise. The act can be written on a regular A4 sheet, or on the organization’s letterhead.

It must necessarily include information about the enterprise where the equipment is being put into operation, as well as detailed information about its name, technical characteristics, conditions of use, etc. The more complex the equipment, the more detailed information about it needs to be recorded and the more points the act may contain.

This document must indicate the compliance of the introduced equipment with the internal requirements of the organization and legal standards, and also record the presence of comments or identified malfunctions. If the facts of defects are confirmed, then a special defect report must be drawn up for the equipment and the equipment cannot be put into operation until the defects are eliminated.

It should be remembered that after signing the act of putting the equipment into operation, the manufacturer’s warranty begins to apply to it.

Rules for drawing up an act

Organizations can draw up an equipment acceptance and transfer certificate in free form or according to a template specially created within the enterprise, the main thing is that it contains detailed data about each of the parties, which must exactly match those specified in the agreement or contract. This is necessary to avoid the common situation where, due to one wrong letter (e instead of e) or an error, it may turn out that “they entered into a transfer agreement with one company, but accepted it from another.”

This act must include a list of equipment indicating manufacturers, brands, serial numbers, quantity and cost. It should also indicate the appearance, physical condition, equipment, malfunctions (if any), etc., that is, all those parameters that were recorded during the preliminary inspection of the equipment.

If the level of equipment requires the presence of a highly specialized specialist during acceptance and transfer, then his signature must also be contained in the document and confirm the quality of the transferred equipment.

The list of equipment can be included in the main document or issued as a separate appendix to the act. The act must be certified by the management of the enterprises between which the transfer took place.

The document can be drawn up either on the company’s letterhead or on a regular A4 sheet.

The act must be drawn up in two copies, and if third parties participate in the transfer procedure, the number of copies must be equal to the number of participants in the transfer procedure.

Each copy must be certified with original signatures. If necessary, special technical documentation can be attached to the document (information about it must be indicated in the act).

Instructions for writing an equipment acceptance certificate

- In the first part of the document, its name is written, and the city in which it is created and the date are indicated: date, month (in words), year.

- Then enter the full name of the enterprise transferring the equipment, indicating the official representative (here usually written either Director or General Director) and the document on the basis of which he works (“Charter”, Regulations”, “Power of Attorney”, etc.) .

- Next, the same information about the receiving party is entered into the document.

- The body of the equipment acceptance and transfer certificate includes clauses directly related to the purpose for which it is issued. Here it is necessary to record the fact of the transfer, as well as the document on the basis of which it took place (its name, for example, “Agreement” and the date of preparation).

- Then you need to include an item about the condition of the transferred equipment.

- Next, you should ensure that the receiving party has no complaints about the quality and quantity of the transferred equipment.

- In the next paragraph you must include the cost of the equipment (in numbers and in words), as well as information about VAT.

- The penultimate paragraph should contain information about the responsibilities of the parties, and finally the number of copies of the act should be indicated.

If it is in excellent condition, then this must be noted; if there are any defects and malfunctions in it, then this should also be recorded (preferably in a separate act, which is drawn up as an appendix to this document).