- About the district District boundaries

- Driving directions

- History of the area

- Characteristics of the area

- Head of the council

- Procedure for entering the civil service

- News

- News

- Helpful information

- State Budgetary Institution of Moscow "Zhilishchnik of the Northern Izmailovo District"

- Regulations

- general information

- New model of ground transport

- Paid city parking on the street Parking in the area

- How to use parking

- Where are the parking lots located?

- 2018 Planned

- Planned

- Planned

- PLANNED

- general information

- Federal Law On the procedure for considering appeals from citizens of the Russian Federation

- general information

- Community advisor in your home

- Compound

- State Budgetary Institution "Leisure

- State Duma of the Russian Federation

- Moscow Government Hotline

- Regulatory legal acts in the field of anti-corruption

- Phones

- News

- News

- News

- Renovation program for blocks of the first period of industrial housing construction

- About terrorism and extremism

- News

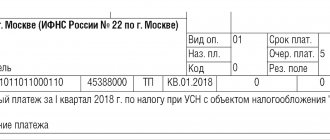

> KBK for payment of an individual entrepreneur’s patent for 2019-2020

Which BSCs are used for PSN?

If the KBK is incorrect: consequences

Which BSCs are used for PSN?

To pay for a patent, an individual entrepreneur must independently find the necessary BCCs and indicate them in the payment order. The Federal Tax Service, recording information on the amount and terms of payment on the reverse side of the patent, does not reflect information on the BCC.

It is necessary to use the following BCC of the patent for individual entrepreneurs for 2019-2020:

- If the territory of patent activity is a city of federal significance (Moscow, St. Petersburg, Sevastopol):

- 18210504030021000110 (tax);

- 18210504030022100110 (penalty).

- If the business is conducted in an urban district:

- 18210504010021000110 (tax);

- 18210504010022100110 (penalty).

- If the individual entrepreneur works in the territory of a municipal district:

- 18210504020021000110 (tax);

- 18210504020022100110 (penalty).

- If the individual entrepreneur works in an urban district with internal divisions:

- 18210504040021000110 (tax);

- 18210504040022100110 (penalty).

- If the individual entrepreneur works in an intracity territory:

- 18210504050021000110 (tax);

- 18210504050022100110 (penalty).

The tax is paid to the municipality in which:

- activities under a certain patent are permitted - in accordance with the regulatory act adopted by the constituent entity of the Russian Federation (subclause 1.1, clause 8, article 346.43 of the Tax Code of the Russian Federation);

- The individual entrepreneur is registered under the PSN - if the patent is valid in the territory of the entire constituent entity of the Russian Federation (clause 2 of Article 346.51 of the Tax Code of the Russian Federation).

It is advisable to indicate the IP KBK 2019-2020 patent correctly. However, mistakes do happen. Next, we will consider what their consequences may be when reflecting the BCC in the payment slip for the payment of tax under PSN.

KBK for individual entrepreneurs for a patent in 2021

In accordance with the order of the Ministry of Finance of Russia dated June 8, 2021 No. 132n “On the Procedure for the formation and application of budget classification codes of the Russian Federation, their structure and principles of purpose”, when paying for a patent, individual entrepreneurs must indicate the following BCCs:

| KBK patent 2021 for payments to the budget | KBK |

| Moscow, St. Petersburg and Sevastopol | 182 1 0500 110 |

| Urban districts | 182 1 0500 110 |

| Urban districts with intracity division | 182 1 0500 110 |

| Municipal districts | 182 1 0500 110 |

| Intracity areas | 182 1 0500 110 |

If the KBK is incorrect: consequences

Errors when filling out a payment order can be divided into:

- Critical - which lead to non-transfer of payment to the budget (and as a result, the emergence of arrears for which penalties are charged).

Such errors include (subclause 4, clause 4, article 45 of the Tax Code of the Russian Federation):

Don't know your rights? Subscribe to the People's Adviser newsletter. Free, minute to read, once a week.

- indication of an incorrect UFC account;

- indication of the incorrect name of the bank in which the Federal Tax Service account is opened.

- Non-critical - which are not accompanied by non-transfer of payment to the budget, but can lead to the payment falling into the category of unknown.

Incorrect indication of the KBK is among such errors. The Federal Tax Service, having received a payment with an incorrect BCC, with a high degree of probability, based on other details, will correctly classify and credit the payment. But if the available data is not enough, the tax authorities will add the payment to the outstanding receipts. In this case, the entrepreneur should submit to the Federal Tax Service a clarification of the payment indicating the correct BCC.

Read more about the actions of the individual entrepreneur in the material “An error was made in the KBK in the payment order.”

***

When paying for a patent, the individual entrepreneur must indicate the correct BCC on the payment slip. It is selected based on the type of settlement (municipality) in which the activity is carried out. Incorrect indication of the KBK may lead to tax authorities entering the payment into the category of unclear cash receipts.

***

New about KBK 18210102030011000110: decoding and registration in payments

Read in the article:

- What tax are we talking about?

- Decoding the code

- Code in the payment document

- All personal income tax codes

- Useful documents

Attention! When paying taxes, penalties and fines, you will need the following documents. Download for free:

KBK Directory for 2021 All codes in one document. Download for free Sample of filling out a receipt for personal income tax payment Complies with all legal requirements. Download for free A guide to filling out payment slips in 2021. It will help you fill out each field of the payment slip correctly. A reference book on the structure of the KBKU. Know the meaning of each digit of the code. Breaking news. Starting from July 1, 9 new regions are participating in the FSS project, and accountants must submit an important statement to the Fund before August 1

For other documents that will help you in your work, see the article.

KBK, or as it is also called, the budget classification code, is mandatory information for non-cash payments, including payments to companies, entrepreneurs and citizens with a budget. KBK consists of 20 characters, which encrypt information about the type and recipient of the payment.

Non-cash payments pass through banking structures, whose task is to send funds to the desired recipient. For this purpose, a special field 104 is provided in the payment document to indicate the BCC. An error in the budget classification code leads to the fact that the payment does not reach the recipient or administrator, but is credited to another budget or is included in outstanding receipts. This creates additional problems for the payer.

KBK 18210102030011000110: what is the tax

It is not difficult to understand what tax to pay for a particular BCC if, knowing the structure of the code, you look at what values are in each of the digits. The general scheme for all KBK is given below:

As can be seen from the diagram, the twenty-digit encoding consists of several parts, and each digit of the code contains the information necessary for non-cash payment. What is encrypted in each of the bits, read in Table 1.

Table 1. KBK 18210102030011000110: what tax

| Code digits | Encrypted payment information | KBK 18210102030011000110 transcript |

| First - third | Who administers the payment | Federal Tax Service (182) |

| Fourth - sixth | Which group and subgroup of budget revenues does the payment belong to? | Income tax (101) |

| Twelfth - thirteenth | What budget should the payment be credited to? | To the budget at the federal level (01) |

| Fourteenth - Seventeenth | Payment type | Amount of tax or arrears on it (1000) |

| Eighteenth - twentieth | Replenishment of the budget or withdrawal from the budget | Budget replenishment (110) |

KBK 18210102030011000110: transcript

Knowing the general structure of budget classification codes, it is easier to understand which payment any KBK belongs to, including KBK 18210102030011000110. We are talking about a tax payment on income credited to the all-Russian budget, and this payment is administered by the Federal Tax Service. In other words, this is personal income tax on the income of individuals who received taxable amounts listed in Article 228 of the Tax Code, including:

- Proceeds from the sale of property, including personal property, or property rights that a person owned for less than the minimum period established by the Tax Code.

- Amounts received by tax residents of Russia from outside the country.

- Rewards to individuals from whom tax agents did not withhold personal income tax and did not report the impossibility of withholding tax.

- Gambling winnings up to 15,000 rubles received from sweepstakes and bookmaker organizations.

- Gifts in the form of real estate, transport, shares, shares in the authorized capital of companies received not from relatives or family members, etc.

Individuals pay tax on this income on their own and report to the tax office in Form 3-NDFL.

The BukhSoft program automatically generates payment orders with current details. The program itself will set the correct BCC, payment order and tax period code. Try it for free:

>KBK 18210102030011000110 in the payment document

You can see the finished receipt for payment of personal income tax by an individual in the window below, it can be downloaded for free.

Features of the patent tax system

The patent taxation system is provided only to individual entrepreneurs with an average number of employees of no more than fifteen people and conducting their activities in accordance with Art. 346.43 Tax Code of the Russian Federation .

The patent tax system implies the potential income of an entrepreneur for the tax period established by the state.

In case of purchasing a patent, the entrepreneur will be exempt from a number of taxes:

- personal income tax;

- property tax for individuals (except for taxable items provided for in Article 378.2 of the Tax Code of the Russian Federation);

- VAT (except for the import of goods from foreign countries into the territory of the Russian Federation and when carrying out activities in accordance with Article 174.1 of the Tax Code of the Russian Federation)

It is necessary to clearly understand that these tax breaks are possible only in relation to those types of activities of an individual entrepreneur in respect of which the patent tax system can be applied.

In accordance with the Tax Code (Article 346.51 of the Tax Code of the Russian Federation), tax payment deadlines are determined depending on the validity period of the rights to conduct business activities under the patent taxation system:

· 2/3 of the amount within a period not exceeding the period of validity of the patent.

KBK 18210102030011000110 and all personal income tax codes

Separate BCCs are established by law for cases of personal income tax payment:

- tax agents,

- individuals from the income specified in Article 228 of the Tax Code of the Russian Federation,

- entrepreneurs and private practitioners who do not have employees;

- foreigners obtaining a patent to work in Russia.

All personal income tax codes are given in Table 2.

Table 2. KBK 18210102030011000110 and all personal income tax codes

| Taxable amount | KBK for personal income tax | ||

| By payment | By penalties | For fines | |

| Taxable income of individuals from Article 228 of the Tax Code | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Rewards to individuals from tax agents | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income of entrepreneurs and private practitioners who do not have employees | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Payments for foreigners obtaining a patent to work in Russia | 182 1 0100 110 | ||

Individuals and tax agents have to pay penalties for personal income tax if the inspectorate does not receive the tax payment after the deadline for its payment has expired.

Example

A tax resident of Russia received an income in the amount of 210,000 rubles in 2021. in the form of rent for renting out their housing located in Kazakhstan. According to the rules of the Tax Code, a citizen pays tax on such income independently, since this is income from outside Russia.

Let’s assume that when filling out a receipt, a citizen made a mistake in the KBK, as a result of which his payment was included in the outstanding payment, although it was paid on time, before July 15 of the next year. He had to pay a penalty in the amount of 1050 rubles. and remit the tax. When filling out receipts, the citizen indicated:

When drawing up a payment order for tax payments, in column 104 you must indicate a special 20-digit code. The KBK UTII 2021 for individual entrepreneurs and legal entities is regulated by the Ministry of Finance of the Russian Federation (Order No. 65n, dated 07/01/2013). The purpose of the code is to systematize budget revenues.

Decoding KBK 18210502010021000110

In Russia, for calculating taxes and maintaining accounting, there is a basic taxation scheme and special regimes (SNO). Depending on the SNO used, the payer indicates the corresponding BCC on the receipt. Most often, legal entities and businessmen work under a special regime - a single tax on imputed income (UTII). This scheme replaces most fees and the tax rate is 15%. The peculiarity of imputation (UTII) is that the fee is calculated not from earned profit, but from approximate income, which is established by the Tax Code of the Russian Federation for a certain type of work. This special regime is used by companies that do not operate in all areas.

Working on UTII, the payer deposits tax funds using a standard payment, indicating KBK 18210502010021000110. The code consists of 20 digits, divided into seven blocks. For each, the corresponding meaning applies:

- 182 - department to which the funds were sent: Federal Tax Service Inspectorate.

- 1 - category of budget revenues: tax.

- 05 - specific type of collection: tax on complex income.

- 02010 - budget category, source from which the fee is calculated: imputed profit transferred to the regional budget.

- 02 - specific type of treasury: budget of a constituent entity of Russia.

- 1000 — purpose of payment: standard. Under this special regime, other types of KBK UTII 2021 income for individual entrepreneurs are also used.

- 110 - generalized group of income: income.

KBK for UTII in 2021

Each number in the cipher has a specific information attribute. The KBK EVND 2021 for legal entities is identical to the code for payment of obligations by private entrepreneurs. This payment falls within the scope of administration of the Federal Tax Service, which is confirmed by the first three digits in the code – “182”.

Within one type of tax, several subtypes of budget revenues are distinguished:

- Number combination 182 1 0500 110 (KBK decoding 2018). What tax does this BCC mean? It is used to pay the main amount of a single “imputed” tax, which is transferred according to the declaration, as well as to pay arrears and recalculations.

- If the deadline for transferring money for tax obligations is missed, a penalty will be charged. Payment of penalties is carried out indicating a separate BCC UTII. In 2021, for individual entrepreneurs and legal entities it looks like 182 1 0500 110. The procedure for calculating penalties is regulated by Art. 75 of the Tax Code of the Russian Federation. When making a payment, you can refer to the reconciliation report with the Federal Tax Service or the tax inspector’s requirement.

- If a tax violation is detected, the inspectorate issues a fine. To repay it, the payment document indicates the intended purpose of the funds with code 182 1 0500 110. Collection in the form of a fine, incl. may be assigned for failure to comply with the deadlines allotted for filing a tax return, or non-payment of tax (Articles 119, 122 of the Tax Code of the Russian Federation).

The KBK UTII 2021 number for LLCs or individual entrepreneurs is not affected by the period for which payment is made. The same numerical combination will be entered in the payment order when transferring funds both for the 1st quarter of 2021 and for any other period. For example, when paying the KBK tax, UTII for the 2nd quarter of 2018 (as well as for the 3rd and 4th quarters) must be indicated in the payment order with the code 182 1 0500 110.

An exception is obligations that arose before 2011; other BCCs apply to them:

KBK for payment of penalties

In case of untimely payment of the UTII fee, or failure to pay at all, penalties are accrued in accordance with Art. 75 of the Tax Code of the Russian Federation. The lower rate is calculated until 31 days of delay, then the sanction rate increases. Thus, up to 31 days of non-payment, the refinancing rate according to the Central Bank of the Russian Federation is calculated as 1/300, and then – 1/150. But the amount of the penalty cannot exceed the amount of the delay.

Thus, in order to pay penalties, you will have to pay an amount multiplied by the number of overdue days and the refinancing rate. When paying a fine, the offender indicates KBK 18210502010022100110 on the payment slip.

Where is KBK 18210504010021000110 used?

The patent system, like other types of taxation, has its own specific nuances and advantages. But, despite the special features, just like in other cases, tax payment occurs only according to a code specially allocated for this. And most often it is used as KBK 18210504010021000110.

Yes, the patent system is one of the youngest. After all, it was introduced only in 2013, and perhaps this is also one of the reasons why at the moment it is still not in particular demand among individual entrepreneurs. But this system has plenty of advantages. First of all, it is worth mentioning the declaration. If in other applicable taxation systems its completion is mandatory and in case of failure to fulfill this obligation the taxpayer is expected to face penalties and fines, then in the situation with the patent system, all these difficulties are absent. Since filing a declaration in a situation with the patent system is not carried out.

There is also no need to worry about timely deductions of contributions to the Pension Fund and the Social Insurance Fund, provided that the activity is not related to retail trade or leasing of real estate. Each individual entrepreneur has the opportunity to simultaneously use several types of patents, the validity of which extends to certain regions. For selected patents, the individual entrepreneur can independently set their validity period. But it is worth considering that the duration of a patent cannot exceed 1 year.

Transfers of tax - the cost of a patent - are carried out in the form of an advance payment, which must be paid by the individual entrepreneur exclusively at the time of validity of the patent, and not based on the results of the activity. A patent is not a kind of restriction from the use of other types of taxation systems. Therefore, each individual entrepreneur has every right, if desired, to combine a registered patent with other necessary tax accrual systems.

How to pay for a patent

First of all, it is worth noting that this patent is not subject to the same type of payment as other types of taxation systems. The amount of tax on a patent is calculated using a 6% rate. Thus, it turns out that by paying for a patent, the individual entrepreneur immediately covers the entire amount of tax. In each case, the cost of the patent will be different, because it is calculated on the basis of the amount obtained as a result of calculations of the maximum amount of income that an individual entrepreneur can receive during the annual period of activity.

The cost of a patent is paid using a special document indicating the correct BCC. The fact is that each territory has a special KBK code and if it is entered incorrectly, the individual entrepreneur may not only experience unpleasant moments associated with correcting the error and redirecting funds, but may even receive a fine for late payment. In most cases, KBK 18210504010021000110 is used, since it is intended for transferring payments to the budget of the city district.

Payment for the patent is made in the form of an advance payment. A certain period is allocated for this operation, and if payment is not made during this period, the payer will face unpleasant consequences. Despite the pleasant advantages present in the patent, the penalty for failure to fulfill the obligations of the payer is very serious. Perhaps these exact penalties applied are not the last reason for the low demand for the patent tax system.

If the required amount is not deposited within the specified time frame, the individual entrepreneur will be required to pay penalties and fines assessed by tax authorities at the rate used for the general taxation system. And they will be accrued from the month when the patent began.

BCC for patent payment for individual entrepreneurs

| NAME | PAYMENT TYPE | KBK |

| Tax levied on the budgets of urban districts | tax | 182 1 05 04010 02 1000 110 |

| penalties | 182 1 05 04010 02 2100 110 | |

| interest | 182 1 05 04010 02 2200 110 | |

| fines | 182 1 05 04010 02 3000 110 | |

| Tax levied on the budgets of municipal districts | tax | 182 1 05 04020 02 1000 110 |

| penalties | 182 1 05 04020 02 2100 110 | |

| interest | 182 1 05 04020 02 2200 110 | |

| fines | 182 1 05 04020 02 3000 110 | |

| Tax levied on the budgets of federal cities (Moscow, St. Petersburg, Sevastopol) | tax | 182 1 05 04030 02 1000 110 |

| penalties | 182 1 05 04030 02 2100 110 | |

| interest | 182 1 05 04030 02 2200 110 | |

| fines | 182 1 05 04030 02 3000 110 |

The biggest convenience for individual entrepreneurs using this system is that there is no need to file a tax return.