18.04.2018

| no comments

An agency contract for the provision of services is an agreement between an organization (principal) and a third party (agent) that helps the organization sell or obtain necessary goods or services and receives compensation for this. The availability of payment for the agent's services is an indispensable condition for concluding such contracts, which is why they are also called contracts for paid services.

In essence, we are talking about intermediary activities, in connection with which the name “agency agreement for the provision of intermediary services” is also used.

Sample agency agreement, its difference from a service agreement

Unlike a regular service agreement, remuneration is usually paid as a percentage of the amount of contracts concluded by the agent, and not as a fixed amount. An agency agreement is aimed at representing the interests of the customer when interacting with clients, while a service agreement is aimed at performing certain actions and obtaining results in a variety of areas.

The agency agreement is drawn up in two copies. His sample includes the following:

- number according to the register of agreements of the enterprise, date and place of registration;

- details of the persons drawing up the agreement;

- list of services performed;

- price policy;

- consideration of all possible situations;

- duration and termination of the contract;

- rights and obligations of the parties;

- dispute resolution;

- details, signatures of the parties.

Report prepared by agent

An integral part of the contract is the agent’s report on the fulfillment of the instructions given to him. The Russian Civil Code (Article 1008) makes the provision of this document the responsibility of an agent, but does not impose requirements on its form. The report form is developed by the parties to the contract, taking into account the specifics of their relationship. The law prohibits replacing it with other documents.

Read also: additional agreement for the provision of additional services

The report (usually monthly) shows the cost of services provided. Documents confirming the expenses incurred by the agent are attached to it. If the specifics of the concluded contract do not require other deadlines, the customer is obliged to pay the specified amount within 7 days from the date of receipt of the report.

The agency agreement imposes certain restrictions on both parties. The agent may require the customer not to use the services of other agents in the field of activity entrusted to him and not to take independent actions to achieve the goal set for the agent.

The customer may prohibit the agent from collaborating with competing organizations. However, it would be illegal for the customer to restrict the agent in choosing methods of work or territory of interaction with clients.

The procedure for considering the Application for accession to the Agency Agreement:

- If the data in the provided documents (specified in clause 3) do not coincide with the data in the Application for accession to the Agency Agreement, such Application IS NOT ACCEPTED for consideration and signing. A letter indicating the reasons for rejecting the Application for Accession is sent to the Travel Agent's email address specified in the Application or from which a scanned copy of the Application was sent. After making corrections, the Application for Accession must be re-sent to the Tour Operator in accordance with the procedure specified in clauses 1-4.

- The tour operator has the right to request additional documents to consider the Application for accession to the Agency Agreement.

- After the Tour Operator receives and processes scans of the signed Application for Joining and the necessary documents, a letter with registration data for entering the personal account of the Vodohod online booking system is automatically sent to the email address specified in the Application details. Within 10 working days from the date of receipt of the Application for Accession, the documents will be reviewed and information on the conclusion of contracts will be sent to the email address of the travel agent specified in the Application for Accession.

- A mark indicating acceptance of the Application for Accession is placed on the original Application only after the Tour Operator has received, reviewed and approved the original Application. The tour operator may, upon request, provide a copy of the Agency Agreement certified on its part, having previously agreed on the timing of its execution.

- The agency agreement is considered concluded from the moment the Tour Operator receives the original signed Application for joining the Agency Agreement and accepts it by the Tour Operator, which is marked and signed by the head (authorized person) of the Tour Operator on the Application.

- It is NOT REQUIRED to send the Agency Agreement for signing.

Attention

By transmitting his identification data, the Travel Agent guarantees its authenticity and expresses his consent to further verification of this data. If the provided data is found to be unreliable, the Tour Operator reserves the right to refuse to conclude the contract or terminate it unilaterally. Consultation on the procedure for concluding an agency agreement

You can get it from the managers of the Agency department by phone, e-mail: [email protected]

- When changing the manager, as well as changing the manager’s credentials (for example: last name, place of residence, passport details), contact details of the organization, legal name of the organization, legal and actual address, etc. (without changing the OGRN and TIN), it is necessary to provide to the address an information letter about the changes on the organization’s letterhead, certified in the prescribed manner by the seal and signature of the head of the organization (or individual entrepreneur), as well as a copy of the order on the appointment of a new head or change of the name of the head. The obligation to notify when changing details within the framework of a concluded agreement is provided for by the Civil Code of the Russian Federation.

- In the event of a change in the OGRN and TIN, the travel agent is obliged to conclude a new Application for Accession to the Agency Agreement in accordance with the established procedure. Information letter about changing details

Types of agreement

One of the types of agency agreement is an agreement for the provision of agency services for finding clients (buyers). It is concluded in accordance with the general model and necessarily contains a list of the main responsibilities of the agent:

- search for clients;

- enter into contracts with them on your own behalf or on behalf of the principal;

- accept payment from them to the principal.

An application form is attached to the document, where data about the new client is entered. If the application is approved by the principal, the agent will sign a contract with the buyer. If the latter has any complaints regarding the quality of the products provided, he resolves this issue with the principal.

An agency agreement for the provision of legal services assumes that the agent looks for lawyers, jurists, and notaries for the customer who care about protecting the customer’s rights. The agent's responsibilities include ensuring the timely receipt, provision and storage of all necessary documentation and reporting to the customer on the work performed by him.

No later than five days after the conclusion of the contract, the agent must be issued the relevant documents and powers of attorney.

An agency agreement for the provision of accounting services is often used by companies providing cellular communications when they enter into agreements with cash register stores.

Agency services

Subscribers pay for the principal's services through agents. The money goes to the agent’s bank account and is then transferred to the principal’s bank account. It should be taken into account that funds received by the agent’s cash desk are considered as income generated by this activity and are taxed.

For regular or one-time transportation of goods, an agency agreement for transport services is drawn up. The customer provides the agent with all information regarding the cargo (weight/volume, main characteristics, degree of danger to human life and health and the environment, etc.) and the type of transport. As a rule, the agent is entrusted with documenting cargo transportation and accompanying the cargo at all stages of transportation.

Postings under the agency agreement

In accounting, the agent's revenue received for providing services to the principal is classified as income from ordinary activities. It is reflected in account 90, subaccount “Revenue”. Expenses incurred by the agent in connection with intermediary services are indicated on account 26, “General business expenses.” This amount is debited from account 26 to account 90, subaccount “Cost of sales”.

Postings under an agency agreement on the part of the principal include the recognition of revenue (90), the accrual of remuneration to the agent based on his report (26), the write-off of costs for intermediary services (90), the accounting of profits received from buyers (clients) through the agent (51) and the reflection VAT.

Correct execution of an agency agreement for the provision of services protects both parties and contributes to the expansion of business activities.

If you need qualified advice regarding your situation, call the phone number listed at the top of the page, or send a question through the form at the bottom right of the screen. Our specialized lawyer will promptly respond and solve your problem!

Peculiarities of document flow under agency agreements

In tax planning, the practice of using intermediary agreements is common. However, the document flow when concluding such transactions has its own characteristics, so violations in it can lead to such consequences for both parties as refusal to deduct VAT, non-recognition of expenses under the contract for profit tax purposes, etc. Let’s consider how to avoid this.

There is a special procedure for issuing and receiving invoices for intermediary agreements. This procedure is established by the Rules for maintaining logs of received and issued invoices, purchase books and sales books for VAT calculations, approved by Decree of the Government of the Russian Federation of December 2, 2000 N 914 (hereinafter referred to as the Rules). The procedure is also clarified by Letter of the Ministry of Taxes of Russia dated May 21, 2001 N VG-6-03/404 “On the use of invoices for VAT calculations” (valid to the extent that does not contradict tax legislation).

When executing agency agreements regarding the issuance of invoices, it is necessary to take into account that the intermediary can act in relations with a third party either on its own behalf or on behalf of the principal. The procedure for issuing invoices depends on the choice of a specific option.

Agency agreement: document flow, parties, types, subject, definition

Some organizations, in order to run a successful business, often need to carry out certain operations and activities that are outside the scope of their normal activities or competence. This may be the need to study and organize sales markets, expedition, or provision of legal services.

If it is not possible to hire additional staff, the organization has the right to delegate such powers to outsiders who can act as intermediaries in carrying out such operations. This type of intermediary activity is called an agency agreement or agency.

What it is

A type of intermediary agreement, in which one party, called an agent, is obliged to perform certain actions on behalf of and on behalf of the opposite party, is called an agency agreement.

The second party, called the principal, is obliged to pay for the agent’s services after fulfilling the terms of the contract. This is regulated by Art. Art. 1005 – 1011 of Chapter 52 of the Civil Code of the Russian Federation. The amount, procedure, and method of payment are determined by the contract.

If not specified in the contract, payment must be made no later than 7 days after submission of the report. The agent is compensated for all expenses incurred during the execution of the contract. Therefore, it can be argued that the agency agreement is consensual, compensated and bilaterally binding.

The agent acts on behalf of the principal, his duties include the performance of functions of a legal and factual nature. This type of agreement has recently appeared in Russian legal practice.

This is due to the rapid development of intermediary services, as well as the fact that ordinary agency and commission agreements do not go beyond the boundaries of actions of a purely legal nature.

This agreement has:

- all the characteristic properties of contracts for the provision of services;

- distinctive features of the type of services offered under this agreement;

- their own specific properties, characteristic only of agency agreements.

Despite the fact that an entire chapter in the Civil Code is devoted to agency, it does not belong to an independent type, but, depending on the chosen model of activity of the parties, refers to commission or assignment agreements. But unlike them, it is not limited to services of a legal nature only

- On the one hand, agency has much in common with a contract of agency (Chapter 49 of the Civil Code of the Russian Federation), when an agent acts on behalf of the principal. When he executes an agreement on his own behalf, there is a similarity to a commission agreement.

- Another distinctive feature is the ability to restrict the agent and principal from concluding similar transactions.

AC sides

Participants in an agency agreement can be legal entities and individuals, as well as the state, government agencies or municipal authorities.

The exceptions are:

- Individuals in the public service, since agency is a business activity, these individuals are not entitled to participate in it.

- Legal entities , if the charter of their organization does not stipulate the possibility of participation in business activities or representative functions.

The party who acts as the customer gives the agent certain instructions related to the sale of goods, works and services is called the principal or customer.

- The agent must, under the contract, fulfill the principal’s assignment, as well as perform any other actions that contribute to the implementation of the contractual relationship. Even if he acts on behalf of the principal or at his expense, the latter may not even participate in the relationship with the buyer of goods or services.

- When an agent acts on his own behalf at the principal's expense, he bears responsibility and has certain rights, regardless of the principal's participation in the transaction and his direct relationship with the buyer.

- When an agent enters into transactions with third parties on behalf and at the expense of the principal, the latter acquires responsibilities.

Types of agreements

Based on the scope of rights and obligations assigned to the agent, contracts can be divided into the following types:

- Exclusive . Under such agreements, agents receive a preferential right to service the company with which an agreement is concluded for the sale of its services and goods.

- Non-exclusive . The company signs agreements with several agents at the same time.

Depending on what area the company’s activities belong to, that is, what services and goods will be sold by the agent, the contract is for:

When working with purchasers of products and services, the agent may disclose information about the principal, but he has the right not to do so.

- The agent is obliged to find a buyer and conclude supply agreements with him. If this is provided for in the text of the agency agreement, he is obliged to accompany the goods and provide warranty service. Usually this is where communication with the recipients of the product or service ends. This scheme is typical for cases when the agent acts on behalf of the principal.

- When an agent acts on his own behalf and does not mention that the goods belong to the principal, then the rights and obligations relate only to him. All claims regarding the quality of the supplied products relate to the agent. That is, it is similar to the activities of a distributor.

- The agent's powers include searching for potential clients, advertising and presentation of the products or services offered. Concluding transactions with buyers is not part of his scope of activity.

- The agent receives the right to enter into contracts with customers and sell goods and services on behalf of the principal.

Document flow

The document flow when concluding such transactions has its own characteristics. Violations of the procedure for drawing up and submitting documentation can lead to big problems, for example, the inability to obtain a VAT deduction or non-recognition of expenses when taxing profits.

The main type of document in the relationship between an agent and a principal is an invoice. The rules for their preparation and presentation are determined by Government Decree No. 914 of December 2, 2000.

According to the conditions specified in this Resolution, the procedure for submitting documentation depends on the content of the contract:

- When an agent acts on behalf of a principal and sells goods belonging to the principal, he is obliged to issue invoices to buyers on behalf of the principal.

- When operating on your own behalf, 2 invoices are issued in your own name. One of the copies should be sent to the buyer, the other should be filed in the Register of issued invoices. However, their reflection in the Sales Book is not necessary.

- After the sale of goods, the agent is obliged to inform the principal of the information on the invoice issued to the buyer. After this, the principal generates invoices (2 copies) with this information. The numbers must correspond to the numbering of the invoices issued to them.

- One invoice is entered into the Sales Ledger and the second is sent to the agent. The agent does not have to register it in the Purchase Book.

- The amount of the agency fee can be entered by both parties into one invoice indicating the cost of work, goods, services, and the amount of VAT.

- It is believed that the number of invoices can be reduced, since the law does not establish their exact number. That is, it is possible to provide one invoice at the end of the month with information included in it for all invoices of the agent. Although there is a risk of being late with the payment of VAT, and this leads to sanctions if they are not paid on time. For example, an invoice was issued in the wrong period when the product was shipped, but a tax case arises at the time of shipment.

- After the transaction is completed, the agent sends a report to the principal. The deadline for its submission is not defined by law; reports can be sent gradually as contractual actions progress. Therefore, the deadline for submitting the report should be indicated in the text of the contract. This is important in order to calculate and pay VAT on time. All documents must be attached to the report, confirming expenses made at the expense of the principal.

- According to clause 3 of Article 1008, it is possible to send an objection to the submitted report to the agent. The time limit for raising such an objection lasts 30 days after receipt.

What is the subject of an agency agreement

The subject of the contract is intermediary services of a legal and factual nature, which the agent is obliged to provide to the principal on his instructions. At the same time, the law does not limit the parties when choosing the type and nature of the agent’s actions.

Therefore, such agreements are often concluded to find suppliers and buyers. In addition, it is possible to conclude various types of transactions for the sale of goods belonging to the principal, carrying out advertising operations, studying the market and its development. All this makes the agency agreement extremely beneficial for the principal, who does not have enough time or knowledge to carry out such actions.

- Legal services under an agency agreement may concern, for example, registration of inheritance and conclusion of contracts.

- Actual services – this could be delivery of goods, advertising or information activities

Powers can be limited by the terms of the contract or written in a general form, with the transfer of authority to perform any actions leading to achieving the goal.

HELL

Before drawing up an agreement, it is necessary to determine its subject, that is, the list of actions that are entrusted to the agent.

There are no strictly established rules for drawing up an agency agreement. It can be written by hand or printed; the 1C program is often used for these purposes. When composing the text, you should adhere to some rules:

- Determine on whose behalf the agent will act, or provide that part of the actions will be on behalf of the agent, and part on behalf of the principal.

- Determine exactly the term of the contract (it can be concluded for a certain period or have an indefinite nature).

- Establish the conditions and deadlines for submitting the report.

- Specify the amount of the agency fee, the timing and procedure for its payment.

- Stipulate the rights and obligations of the parties. For example, the ability to enter into agreements of this kind with other persons. The agent may impose restrictions on the principal on concluding agency agreements with other agents.

- The principal may prohibit the agent from entering into contracts with other principals. At the same time, it is impossible to limit the agent in the choice of clients and customers when implementing services and work.

- Provide for the possibility of a subagency agreement. That is, the agent’s right to perform actions under this agreement independently or with the involvement of a subagent.

- Conditions for termination and termination of the contract. Such conditions may be: refusal of one of the parties from the contract, if the term is not limited, death or recognition of incapacity of one of the parties, bankruptcy of the agent.

Agency agreement in the wholesale business is the topic of this video:

Accounting and tax accounting

- For goods received by the agent from the principal for the purpose of sale, ownership does not pass to the agent. Therefore, this product does not need to be reflected on the principal’s balance sheet; it is recorded on off-balance sheet account 004 “Goods accepted on commission”, in the amount indicated in the transfer and acceptance certificate.

- After the goods are transferred to the buyer, their value is debited from the off-balance sheet account. When shipping goods, the agent takes into account accounts payable to the principal in account 76 “Settlements with various creditors and debtors.” Receiving payment and transferring it to the principal does not generate income or expenses for the agent.

- VAT is paid on the amount of the agent's remuneration if he is one of the payers of this tax. If an agent withholds remuneration from funds when transferring them to the principal, then this is considered an advance payment, which means the moment arises for determining the tax base for VAT.

- After submitting the report, the agent determines VAT on the amount of the remuneration. The previously calculated amount of VAT on prepayment is accepted for deduction.

- The agent does not pay income tax because he works with the property of the principal, he does not own anything, everything received under the agreement is the property of the principal.

- The total amount of funds received by the principal for goods or services sold on the date of submission of the report is considered his income (less VAT). The VAT payer under an agency agreement is considered to be the principal, even if invoices are issued to buyers by the agent.

- For tax purposes, expenses reimbursed to the agent are deducted from the principal's income.

Scheme of work on blood pressure

Source: https://uriston.com/kommercheskoe-pravo/dokumentatsiya/dogovor/agentskij/predmet-i-soderzhanie.html

Agent's golden rules

When an agent sells goods (works, services) to a principal, the following rules apply when issuing invoices. If the agent sells goods (work, services) under an intermediary agreement on behalf of the principal, then the invoice must be issued to the buyer on behalf of the principal. If the agent sells goods (work, services) of the principal on his own behalf, then the invoice is issued by the intermediary in two copies on his own behalf. In this case, the number in the invoice is assigned by the agent according to the chronology of the invoices issued by him. One copy of this document is handed over to the buyer, and the second is filed in the journal of issued invoices without registering it in the sales book (clause

Agency agreement: accounting by the principal and agent

3 of the Rules). Note that this option, when the agent acts on his own behalf, is the most complex.

After the intermediary has sold the product, he informs the principal of the invoice issued to the buyer. Then the principal issues an invoice with these indicators, as expected, in duplicate. The first copy is registered in the sales book with the principal, the second copy of the invoice is transferred to the agent. Please note that the numbering of invoices must correspond to the chronology of invoices issued by the principal. The intermediary does not register invoices received from the principal in the purchase book (clause 11 of the Rules).

Invoices issued by the agent for the amount of his commission are recorded in the principal's purchase book as the right to tax deductions arises. For the agent, such invoices are subject to reflection in the sales book.

The commission agent and the agent can indicate the amount of intermediary remuneration in one invoice with the cost of goods (work, services) on separate lines indicating the corresponding VAT amounts.

How to correctly draw up documents under an agency agreement received from the agent

Attention

We invite you to familiarize yourself with: A sample of filling out a cash expense order (RKO) for reporting in 2021

In this case, the delivery note is a supporting document confirming the transfer of ownership of the goods being sold (unless otherwise established by the supply contract for sale) and the buyer’s expenses in the form of the purchase price of the goods sold. In this situation, when shipping the goods to the buyer, the seller (principal) should be indicated in the delivery note in the “Supplier” line. The shipper is the owner (proprietor) of the cargo or a person who has a warehouse and acts as a shipper on behalf of the owner of the cargo, or a person performing actions on his own behalf, but at the expense and on behalf of the owner of the goods (letter from the Federal Tax Service of Russia for the city of No.

Moscow dated December 30, 2009 N 16-15/139277).

Lipetsk region49 – Magadan region50 – Moscow region51 – Murmansk region52 – Nizhny Novgorod region53 – Novgorod region54 – Novosibirsk region55 – Omsk region56 – Orenburg region57 – Oryol region58 – Penza region59 – Perm region60 – Pskov region61 – Rostov region62 – Ryazan region63 – Samara region64 – Saratov region65 – Sakhalin region66 – Sverdlovsk region67 – Smolensk region68 – Tambov region69 – Tver region70 – Tomsk region71 – Tula region72 – Tyumen region73 – Ulyanovsk region74 – Chelyabinsk region75 – Transbaikal region76 – Yaroslavl region77 – Moscow78 – St. Petersburg79 – Jewish Autonomous District83 – Nenets A O86 – Khanty -Mansi Autonomous District87 – Chukotka Autonomous District89 – Yamalo-Nenets Autonomous District91 – Republic of Crimea92 – Sevastopol99 – Baikonur Question: * Write to us Suggestion, comment, request or question.

Important

By virtue of paragraph 1 of Article 171 of the Tax Code of the Russian Federation, the right to deduction arises for the taxpayer if the following conditions are simultaneously met: - goods (work, services) must be accepted for accounting (clause 1 of Article 172 of the Tax Code of the Russian Federation); — goods (work, services) must be used in activities subject to VAT or intended for resale (clause 2 of Article 171 of the Tax Code of the Russian Federation); — the taxpayer must receive an invoice from the supplier (clause 2 of article 169, clause 1 of article 172 of the Tax Code of the Russian Federation). In the situation under consideration, the right to deduction for goods (work, services) purchased for the purpose of executing the principal’s instructions arises from the principal. Consequently, the basis for deducting VAT from the principal will be an invoice received from the intermediary (agent).

Thus, the reflection of product sales in the accounting and tax records of your organization (principal) should be based on the agent’s report, to which documents are attached confirming the expenses incurred by the agent. There are no special rules regarding the form and content of the report being compiled by law. Therefore, the parties to the intermediary agreement can independently determine for themselves the form of these documents and the list of information required by the principal.

The specified documents must be transmitted by the intermediary along with the report. Law No. 402-FZ establishes that the forms of primary accounting documents are determined by the head of an economic entity on the recommendation of the official charged with maintaining accounting records (Part 4, Article 9 of Law No. 402-FZ). Mandatory details of primary accounting documents are listed in Part 2 of Art. 9 of Law No. 402-FZ.

Agent report as process completion

The agent's report completes the document flow during the execution of agency contracts. The deadlines within which the report must be transferred to the principal are not established by law, so they should be specified in the agency agreement.

Attention! Specify the deadlines for submitting the report in the agency agreement. This is important for the purpose of timely payment of VAT by the principal, since if the agent is not informed in time, he may be late in paying the tax. Please note that the five-day period for issuing an invoice is counted from the day the agent sold the goods.

Agent's primary documents

The form of the document providing for the principal’s order to the agent to ship goods to a specific person is not established by law. We believe that the parties to the contract can independently determine the form of this document. Agent reports According to paragraph 1 of Art. 1008 of the Civil Code of the Russian Federation, during the execution of an agency agreement, the agent is obliged to submit reports to the principal in the manner and within the time limits provided for by the agreement.

If there are no relevant conditions in the contract, reports are submitted by the agent as he fulfills the contract or upon expiration of the contract. Unless otherwise provided by the agency agreement, the necessary evidence of expenses incurred by the agent at the expense of the principal must be attached to the agent’s report (Clause 2 of Article 1008 of the Civil Code of the Russian Federation).

Attention

According to the Civil Code of the Russian Federation, things transferred by the principal to the agent remain the property of the principal. In the case where the agent acts on behalf and at the expense of the principal, the rights and obligations under transactions concluded by the agent with the buyer immediately arise directly from the principal. In this case, all documents related to the conclusion by the agent of a transaction in the interests of the principal must be executed on behalf of the principal and kept by him.

How to reduce paperwork?

Some experts believe that it is possible to reduce the flow of documents between the agent and the principal, since clause 24 of the Rules does not say that for each invoice issued by the commission agent to the buyer, the principal must issue his own invoice to the commission agent. Consequently, it is enough for the principal (principal) to issue one invoice at the end of the month with the indicators of all invoices of the commission agent (agent).

It is important. Reduced document flow may result in incomplete payment of VAT on some transactions. In this case, liability will arise for late payment of tax.

Please note that this may result in incomplete payment of VAT on some transactions. For example , the shipment occurred in one reporting period, but the invoice was issued in another, and the taxpayer did not charge VAT. In this case, liability will arise for late payment of tax.

Trade without a waybill or invoice

If the agent carries out retail trade, issuing cash and sales receipts to the buyer instead of a delivery note and invoice, as when trading under supply contracts, the document flow procedure will be simpler.

During retail sales, the agent does not issue invoices to buyers; therefore, he cannot transfer to the principal the indicators of the invoice issued to the buyer.

Therefore, the agent is limited to submitting a report with the necessary documents attached (copies of cash receipts, other documents) confirming the fact of sale of goods to customers. Such a report serves as the basis for the principal to issue an invoice, which is recorded in the journal of issued invoices and in the sales book and sent to the agent.

How to manage document flow under a commission agreement

What documents are needed to formalize the transfer of property under a commission agreement?

Document the transfer of property from the commission agent to the principal and vice versa using any primary documents drawn up in accordance with the requirements of Part 2, 4 of Art. 9 of the Accounting Law.

You can use standard forms for recording trading operations in commission trading. These include, for example (clause 1.4 of the Resolution of the State Statistics Committee of Russia dated December 25, 1998 N 132):

- list of goods accepted for commission, according to Form N KOMIS-1;

- a list of vehicles (cars, motorcycles) and numbered units (units) accepted for commission in accordance with Form N KOMIS-1a;

- certificate of sale of goods accepted for commission, in form N KOMIS-4;

- card for recording goods and settlements under commission agreements in form N KOMIS-6;

- log of acceptance for commission and sale of vehicles (cars, motorcycles) and license plates (units) according to Form N KOMIS-8.

How to write a commission agent's report

Draw up the commission agent’s report in any form, taking into account the requirements of Part 2 of Art. 9 of the Accounting Law.

We suggest you read: Where you can complain about a court decision

Set the report form in the appendix to the commission agreement. Include in the report information about the execution of the commission agreement and the costs incurred in connection with the implementation of these actions, which the principal must reimburse. In addition, provide in the report the calculation of the commission agent's remuneration and indicate its amount.

Submit the commission agent's report to the principal after execution of the contract (Article 999 of the Civil Code of the Russian Federation).

How can a committent file objections to a commission agent’s report?

The principal files objections to the commission agent's report within 30 days from the date of its receipt or within another period specified in the commission agreement (Article 999 of the Civil Code of the Russian Federation).

We recommend that the contract stipulate that objections must be sent in writing (Article 160 of the Civil Code of the Russian Federation).

You can establish the form of objections in the annex to the contract.

In what cases and how does a commission agent draw up an act of provision of services?

If the commission agent's report only notifies about the execution of the contract and does not contain details of the work, draw up an act of acceptance of the commission agent's services. In the act, describe in detail your actions under the agreement.

Develop the form of the commission agent’s services acceptance certificate yourself, including all the necessary details of the primary accounting document (Part 2, 4, Article 9 of the Accounting Law).

We recommend that the form of the act be established in the appendix to the commission agreement.

How a commission agent prepares invoices and keeps a log of invoices

If you are purchasing goods for the consignor, reissue an invoice from the seller to him. If the consignor's goods are sold, issue an invoice to the buyer. Register such invoices in the invoice register (clause 3 of article 168 of the Tax Code of the Russian Federation, clause 3, paragraph “a”, clause 7 of the Rules for maintaining the invoice register).

In addition, issue an invoice to the principal for the amount of the commission. It does not need to be registered in the invoice journal (clause 1, article 156, clause 3, article 168 of the Tax Code of the Russian Federation, clause 1(2) of the Rules for maintaining the invoice journal).

We invite you to read: What tax should you pay on donating an apartment to a close relative in 2021?

Agency agreements for the purchase of goods, works, services

When an agent carries out instructions from the principal to purchase goods (order work or services), invoices are drawn up as follows. If goods (work, services) are purchased through an agent, but on behalf of the principal, then the invoice must be issued by the seller (contractor) in the name of the principal. Only in this case will it be the basis for deducting VAT on goods (work, services) purchased from the principal.

If the purchase of goods (order of work or services) is carried out by an agent on his own behalf, then the invoice is issued by the seller (contractor) in the name of the agent. In this case, the basis for the principal to accept VAT for deduction will be the invoice received from the agent. In this case, such an invoice is issued by the intermediary to the principal reflecting all the indicators from the invoice issued by the seller to the agent. Note that both invoices (both received and issued) are not recorded by the agent in the purchase book and the sales book. The agent does not register invoices received from sellers in the purchase book (clause 11 of the Rules).

A. Urvantseva

K. e. n.,

tax consultant

Kuzminykh and Partners LLC

Contents of the agency agreement

An agreement of this type is used in many areas of business: trade, real estate, tourism, cargo transportation, law, etc. That is why it contains a huge number of specific conditions and features, and there cannot be a standard form of agreement. The parties have the right to individually draw up all blocks of the agreement in a voluntary form.

As a basis, you can use any sample agency agreement with editing to suit your own cooperation standards. But there are a number of mandatory information blocks that must be indicated in the document.

- Subject of the transaction. The section should describe the actual and legal acts to be performed by the agent at the expense of the principal. Legal actions usually involve concluding contracts, but not only that. Actual actions are not at all clearly regulated by law, so the parties can indicate any information within the framework of preliminary oral agreements. It is recommended to outline the scope of responsibility and responsibilities, with the help of which it will be possible to further prepare powers for the agent.

- On behalf of whom transactions are made. If all transactions are concluded by an agent, then the rights and obligations fall on his shoulders and only then can they be transferred to the principal as part of an assignment or transfer of debt. But if transactions are concluded by an agent, but on behalf of the principal, then the latter party immediately assumes obligations and rights.

- Duration of the contract. At the request of the parties, it can be determined or made indefinite. The specified period is a limitation for the agent, i.e. a certain limit when he is obliged to fulfill his obligations. The principal should consider setting the deadline based on the terms and subject of the transaction. If the term is not provided for in the contract, then either party has the right to terminate it with one month’s notice.

- Volume and procedure for payment of remuneration. It is extremely important to reflect this point in the agreement. If it is not described, then legal requirements come into force. The agency procedure is a commercial activity, so each party wants to receive its benefit and know its volume in advance.

- Protection from competitors. Both the principal and the agent can establish a complete ban or restriction on the conclusion of such agreements, both generally and in a certain territory. In the interests of the agent, a ban on such activities on the part of the principal can be introduced. If agreements on a ban exist, the scope and conditions must be clearly defined.

- Monitoring and control. This applies to the agent, obliging him to prepare a report on the business activities. If the form and procedure for reporting are not established, this obligation still remains, but the format is not regulated. It is advisable to stipulate in the contract the situations in which objections are accepted when submitting reporting documentation.

- Subagency. When this issue was not discussed and not taken into account in the contract, the agent has every right to delegate his functions to a third party. It is necessary to discuss the prohibition or permission to enter into a subagency agreement and clearly state the main provisions.

Responsibility and obligation of both parties is the basis of any contractual agreement, including an agency agreement. Additionally, you should indicate the form, procedure and reasons for termination of the document. In addition to the reluctance of one of the parties to fulfill their obligations, there may be various reasons - bankruptcy, recognition by the court as incompetent, death and other circumstances.

In addition, the written form of the agreement must contain the details necessary for civil contracts:

- names of the parties (individual - full name and passport details, legal entity - information based on constituent documents);

- date of conclusion of the agreement;

- signatures of the parties;

- print.

It is not necessary to have the document certified by a notary, but this procedure can be performed if desired.

Agency agreement for the provision of services

Features of taxation when working under an agency agreement.

When working under an agency agreement, specific features arise in calculating the tax base for VAT and income tax.

2.1. VAT.

VAT taxpayers, when carrying out business activities in the interests of another person on the basis of agency agreements, determine the tax base as the amount of income received by them in the form of remuneration (or any other similar income) in the performance of agency agreements (Article 156 of part two of the Tax Code of the Russian Federation). The VAT tax base for an agency agreement is determined as the amount of income received by the agent in the form of remuneration (Article 156 of the Tax Code of the Russian Federation). Amounts received from the principal for the execution of a transaction (except for amounts due to them in the form of fees or any other income) are not included in the tax base. The procedure for issuing invoices for intermediary agreements is established by the Rules for maintaining logs of received and issued invoices, purchase books and sales books for value added tax calculations (approved by Decree of the Government of the Russian Federation of December 2, 2000 N 914). In accordance with clause 3 of these Rules, agents performing actions on their own behalf store invoices received from sellers for goods purchased for the principal in the journal of received invoices. The purchase book does not record invoices received by the agent from the principal for goods transferred for sale or from the seller of goods, issued in the name of the agent (clause 11 of the Rules).

2.2. Income tax.

1. Income in the form of property (including cash) received by the agent in connection with the fulfillment of obligations under the agency agreement (subclause 9 of clause 1 of Article 251 of the Tax Code of the Russian Federation) is not considered to be the agent’s income. 2. Income in the form of property (including cash) received by the agent to reimburse expenses incurred by him for the principal is not considered income of the agent, if such expenses are not subject to inclusion in the agent’s expenses in accordance with the terms of the concluded agreements. 3. Expenses in the form of property (including money) transferred by the agent in connection with the fulfillment of obligations under the agency agreement (subclause 9 of Article 270 of Part Two of the Tax Code of the Russian Federation) are not considered expenses of the agent. 4. Expenses made by the agent to pay expenses for the principal are not considered to be the agent’s expenses, if such expenses are not subject to inclusion in the agent’s expenses in accordance with the terms of the concluded agreements.

Consequently, the tax base for calculating income tax for an agent will be only the amount of the commission. Moreover, for tax purposes, such amounts are accepted depending on the method of recognition of income and expenses determined by the agent’s accounting policy in accordance with current tax legislation. If the agent uses the accrual method for these purposes, then the date of receipt of income from the sale of intermediary services is the date of actual provision of these services (Article 271 of the Tax Code of the Russian Federation), which is determined on the basis of the agency agreement: - upon completion of the operation (order); - on the last date of the reporting period under the contract (if the contract is long-term or provides for the performance of several operations during a certain period); - on the date of submission of the report by the agent. If the agent has the right to determine income and expenses using the cash method (subject to the requirements of Article 273 of the Tax Code of the Russian Federation), then the date of receipt of income is the day of receipt of funds from the principal (in the form of remuneration) to bank accounts and (or) to the cash desk, receipts in payment for other property (work, services) and (or) property rights, as well as repayment of debt to it in another way.

The agent must document all expenses incurred by him under the contract. Otherwise, the amount of their compensation will be considered gratuitously received funds and, accordingly, will be subject to inclusion in non-operating income and will be subject to income tax. Copies of all documents confirming the expenses incurred by the agent are, as a general rule, attached to the agent’s report. The amount of remuneration should not be established in the contract taking into account compensation for the agent’s expenses under the contract. This leads to an unreasonable overestimation of the agent's revenue. In addition, the agent cannot include such expenses in the cost price, since according to the Civil Code of the Russian Federation they must be reimbursed by the principal. For the same reason, the agent cannot deduct VAT on them.

About documents submitted by the agent to the principal

Often, enterprises use the services of intermediaries when selling their products (goods, works or services) or to purchase property, order work or services. All intermediary operations are formalized by appropriate agreements, which can be of three types: orders, commissions and agency agreements.

In this article we will consider agency agreements. The legal features of agency agreements are established by Chapter 52 of the Civil Code of the Russian Federation.

“Under an agency agreement, one party (the agent) undertakes, for a fee, to perform legal and other actions on behalf of the other party (the principal) on its own behalf, but at the expense of the principal or on behalf and at the expense of the principal.

Under a transaction made by an agent with a third party on his own behalf and at the expense of the principal, the agent acquires rights and becomes obligated, even if the principal was named in the transaction or entered into direct relations with the third party for the execution of the transaction.

In a transaction concluded by an agent with a third party on behalf and at the expense of the principal, the rights and obligations arise directly from the principal.”

According to Article 1008 of the Civil Code of the Russian Federation, the agent is obliged to submit reports to the principal, while the composition of the agent’s report and how this report is provided to the principal (for what period, within what time frame, etc.) is determined by the terms of the agency agreement. The agent's report must be accompanied by documents confirming the expenses incurred by the agent at the expense of the principal.

Article 1006 of the Civil Code of the Russian Federation establishes that the principal pays the agent remuneration in the amount and in the manner specified in the agency agreement.

In most cases, when purchasing services, income is the actual difference between how much the contract was concluded with the customer and how much the services provided actually cost.

An example of the procedure for calculating the amount of remuneration can be one of the following methods: 1) percentage of the cost of sold goods (work, services) of the principal; 2) percentage of the difference in the amounts of sale and receipt of sold goods (work, services) of the principal; 3) fixed amounts.

In accordance with Article 1011 of the Civil Code of the Russian Federation, provisions relating to other types of intermediary operations (orders and commissions) can be applied to agency agreements.

Therefore, depending on the terms of the agency agreement, the remuneration can either be transferred (paid) to the agent by the principal after approval of the report, or withheld by the agent from the amounts due to the principal (Article 997 of the Civil Code of the Russian Federation).

Also, the principal is obliged to reimburse the agent for all expenses incurred by him in the course of executing the principal’s instructions (Article 1001 of the Civil Code of the Russian Federation).

We invite you to familiarize yourself with: Sample cession agreement for compulsory motor liability insurance in case of an accident

Article 156 of the Tax Code of the Russian Federation states that VAT payers, when carrying out business activities in the interests of another person on the basis of agency agreements, determine the VAT tax base as the amount of income received by them in the form of remuneration (or any other similar income) in the performance of agency agreements.

In the case where the goods (work, services) of the principal are exempt from paying value added tax, this benefit does not apply to agency remuneration (clause 2 of Article 156 of the Tax Code of the Russian Federation), with the exception of intermediary services for the sale of the agreed list of goods (work, services) ).

The procedure for issuing and receiving invoices by an agent for intermediary operations is regulated by the Rules for maintaining logs of received and issued invoices, purchase books and sales books for value added tax calculations, approved by Decree of the Government of the Russian Federation dated December 2, 2000 No. 914.

The procedure for issuing invoices by an agent depends on whether the intermediary in relations with a third party acts on his own behalf, or on behalf of the principal, the principal.

Features of issuing invoices for agency operations are shown in Table 1.

Table 1

| Goods (works, services) are sold or purchased on behalf of | When an agent sells goods (works, services) to the principal | When an agent carries out instructions from the principal to purchase goods (order work or services) |

| principal | the invoice must be issued to the buyer on behalf of the principal, i.e. drawn up by the principal himself; | the invoice must be issued by the seller (contractor) in the name of the principal; |

| agent | The invoice is issued by the agent in 2 copies on its own behalf. In this case, the number indicated in the invoice is assigned by the agent in accordance with the chronology of invoices issued by him. One copy of this document is handed over to the buyer, and the second is filed in the journal of issued invoices without registering it in the sales book. The principal must issue the same invoice in the name of the intermediary (agent) with numbering in accordance with the chronology of the invoices issued by him. Moreover, this invoice is not registered in the purchase book of the intermediary (agent). | the invoice is issued by the seller (contractor) in the name of the agent. In this case, the basis for the principal to accept VAT for deduction will be the invoice received from the agent. In this case, such an invoice is issued by the agent to the principal reflecting all the indicators from the invoice issued by the seller to the agent. Moreover, both invoices (both received and issued) are not registered with the agent in the purchase book and sales book. |

For the amount of the agency fee, the intermediary issues a separate invoice to the principal under the agency agreement. This invoice is registered with the agent in the prescribed manner in the sales book, and with the principal - in the purchase book.

At the seminar, Vladimir Yakovlevich said that the agent is obliged to submit to the principal, along with the report, documents confirming income and expenses for transactions completed during the execution of the order.

This is really true {q} Yes. But this does not concern our situation; we act as agents on our own behalf. What will happen if we still don’t provide copies of transaction documents to the principal {q} M. A.: If the principal accepts your report without them, then, in general, nothing.

Once the agent’s report is accepted without objection, it means that the principal has recognized that the order was properly executed and must pay the agent a fee and reimburse expenses.

Moscow dated December 8, 2004 N 24-11/79072 clause 1 art. 998 Civil Code of the Russian Federation; clause 14 of the Information Letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated November 17, 2004 N 85; Resolution of the FAS Central District of August 26, 2002 N A48-605/02-12 Resolution of the FAS Moscow Region of October 12, 2005 N KG-A40/9722-05 First published in the publication “General Book. Conference Hall” 2010, No. 03

Unless the agency agreement provides otherwise, the agent's report must be accompanied by the necessary evidence of expenses incurred by the agent at the expense of the principal.

The principal who has objections to the agent’s report must notify the agent about them within 30 days from the date of receipt of the report, unless a different period is established by agreement of the parties. Otherwise, the report is considered accepted by the principal.

In addition to the report, the fulfillment of the intermediary’s contractual obligations can also be confirmed by drawing up a bilateral act signed by the parties to the contract. Both the service acceptance certificate and the intermediary’s report must contain the mandatory details provided for in clause 2 of Art. 9 of the Federal Law of December 6, 2011 N 402-FZ.

The taxpayer develops and approves the forms of these documents independently.

Features of accounting under an agency agreement.

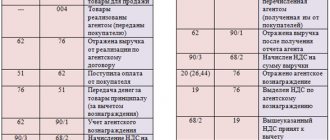

All settlements under the agency agreement in the Agent’s accounting are reflected in account 76 Settlements with other debtors and creditor. All expenses related to the agency agreement must be reflected in the Agent's account. 76 Settlements with other debtors and creditors, in order to deduct these expenses, together with the agency agreement, from the debt to the Principal when receiving proceeds from the sale of goods.

If the Principal provides the Agent with an advance for the execution of the order, then the advance should be reflected in the posting: D 51 K 76 funds were transferred to the agent from the principal for the production of goods. The funds that the agent received as compensation for costs under the contract are not considered revenue. Therefore, they are not taken into account in the credit of account 90 “Sales”.

The accounting entries for the agency agreement will look like this:

Debit 60 Credit 51 Contents of the transaction. Paid for work and services of organizations related to the execution of the contract (including VAT). Documentation 1. Bank statement.

Debit 76 Credit 60 Contents of the transaction. The costs of payment for work and services of third-party organizations are reflected, which are reimbursed by the principal under the contract (including VAT). Documenting. 1. Invoices received from performing suppliers (not recorded in the purchase book). 2. Invoices, acceptance certificates received from performing suppliers.

Debit 002 Contents of the transaction. The agent received finished products from performing suppliers. Documenting. 1. Invoice from the supplier. 2. Notification of the agent to the principal about the receipt of finished products.

Credit 002 Contents of the operation. The finished products are transferred to the principal. Documentation 1. Invoice on behalf of the agent, or deed of transfer. 2. Invoice on behalf of the agent for the amount of finished products transferred (not recorded in the agent’s sales book).

Debit 76 Credit 90.1 Contents of the transaction. The agency fee is reflected. Debit 90.3 Credit 76.N.1 or 68.2 Contents of the transaction. VAT is charged on the amount of the agent's remuneration. Documentation 1. Agent's report. 2. Copies of primary documents from performing suppliers. 3. Invoice on behalf of the agent for the amount of the agent's fee (registered in the sales book).

Debit 51 Credit 76 Contents of the transaction. Received from the principal compensation for expenses under the agency agreement (including VAT) and agency remuneration Documentation 1. Bank statement.

Information provided by AS-AUDIT

Accounting for the principal in the program “1C: Accounting 8”

To register the relationship between the agent and the principal in the program, an agreement is drawn up with the counterparty, which indicates the type of agreement: with the commission agent (agent) or with the principal (principal). For contracts of this type, in contrast to ordinary contracts with a supplier or buyer, it is possible to specify the procedure for calculating commissions.

The amount of commission in the program can be calculated as a percentage of the cost of goods or services sold, as a percentage of the difference between the cost at which goods or services were transferred to the agent and the cost of their sale to the buyer, and can also be set manually. The commission calculation parameters may remain blank; in this case, they will need to be specified manually each time when generating the documents Report of the commission agent (agent) on sales or Report to the principal (principal) on sales (see Fig. 1).

Rice. 1

Let's consider the most difficult situation, when an organization acts as an agent in the sale of the principal's goods, while the principal also provides services for the delivery of goods to customers. In addition, the organization also provides its own services to protect goods during transportation. The agent submits documents on his own behalf.

First of all, the document Receipt of goods and services is drawn up, with the help of which the fact of transfer of goods by the principal to the agent is registered. In this case, the document is drawn up in the usual way, using the transaction type Purchase, commission. Account 004 “Goods accepted on commission” is used as an accounting account.

Thus, an accounting entry is made to the Debit of account 004.1 for the cost of the transferred goods - see Fig. 2.

Rice. 2

Then we register the sale of goods to the buyer, but at the same time we also reflect the fact of the sale of the principal’s service and our own service.

To do this, on the Goods tab of the Sales of Goods and Services document, we indicate the list of the principal's goods being sold, on the Services tab, the service for protecting goods provided to the buyer on our own, and on the Agency Services tab, the principal's service for the delivery of goods.

It should be noted that on the Agency services tab of the document, columns with information about the principal, the agreement with him, within the framework of which the service is implemented, and the settlement account (in our case 76.09) must be filled in.

In case of mistaken entry of information about agency services into the services table and vice versa, the data in these tables can be mutually supplemented using the Transfer to “Services” and Transfer to “Agency Services” buttons.

When posting the document, the necessary entries will be made - see fig. 3.

Rice. 3

As can be seen from the entries, VAT on goods and services sold under an agency agreement is not reflected by the agent. It must subsequently be reflected to the principal.

The agent issues an invoice to the buyer for the total amount of the transaction, but only the cost of his own service should be included in the agent's sales book from this amount.

The buyer transfers payment for goods and services to the agent. This operation is formalized in the usual way using the document Receipt to the current account with the transaction type Payment from the buyer.

Debit 51 Credit 62.01

In our case, the entire payment amount is transferred upon the provision of services, but even in the case of an advance, this operation does not have any special features, compared to a similar operation under an agreement with the buyer.

After this, the agent draws up a report to the principal; for this, the document Report to the principal (principal) on sales is used.

This document is filled out with a list of goods and services sold in accordance with the agency agreement. The program implements the ability to automatically fill the table of goods and services with one of three possible algorithms:

The header of the document indicates the procedure for calculating the agency fee; information about it is inherited from the agency agreement (remember, at the very beginning we said that it is desirable, but not necessary, to indicate this information in the agreement). If the agreement does not specify the procedure for calculating remuneration, it can be indicated directly in the header of the report to the principal.

https://www.youtube.com/watch{q}v=ytcopyrightru

The amount of the agency fee is indicated for each product or service from the table of the same name in the document. For each line, the amount of VAT remuneration is also calculated.

The procedure for reflecting the sale of intermediary services in accounting is indicated on the Remuneration tab. The Withhold commission flag allows you to regulate the mechanism for paying agent commissions:

- if the flag is set, then the amount of remuneration is withheld from funds received from buyers as payment for the goods and services of the principal;

- if the flag is not set, then when posting a document in the usual way, either an offset to the advance payment (if the principal paid for agency services was made earlier) or the principal’s debt is registered.

We invite you to read: Deadline for reviewing documents under the compatriots resettlement program

On the Settlement Accounts tab, set the account for settlements with the counterparty (to reflect mutual settlements for the provision of agency services - by default account 62.01) and, depending on the selected method of payment for the agency fee, either the account for settlements with the principal or the account for settlement of advances.

When deducting the amount of remuneration from customer payments, the default settlement account with the principal is 76.09. If the payment of the agency fee is made in a separate payment from the principal, then here you need to indicate another account - settlements for advances 62.02.

On the Cash tab, the user manually enters information about funds received from the buyer.

Debit 62.01 Credit 90.01.1 – for the amount of agency fees – revenue is reflected; Debit 90.01.1 Credit 68.02 – for the amount of VAT on remuneration – VAT is reflected.

If remuneration is withheld from customer payments, a posting will also be made

Debit 76.09 Credit 62.01

– for the amount of agent’s remuneration.

The agent issues an invoice to the principal for the amount of remuneration, which is registered in the program directly from the Report to the Principal document.

https://www.youtube.com/watch{q}v=upload

Based on the report, the principal can register the document Write-off from the current account, with the help of which the fact of transferring funds to the principal for goods and services sold is formalized. If the amount of the agency fee was withheld from funds received from buyers, then the amount of receipts minus the amount of the agent fee will automatically be entered in the bank document.

Otherwise, the document will contain the full amount of payments made by buyers for goods and services of the principal from the current report to the principal.

Also, based on the report, the principal can enter the document Receipt to the current account, reflecting the fact that the principal has transferred the agency fee. This document is entered when the Withhold agent fee flag is not selected.

We also need to mention invoices. In our example, based on the results of the operation, two invoices should be included in the sales book: an invoice issued to the buyer, but only for the cost of the services provided by us for the protection of goods; an invoice issued to the principal for the amount of the agency fee (see Fig. 4).

Rice. 4

Let's now look at the same example from the principal's point of view.

When transferring goods to commission, a document Sales of goods and services is drawn up with the transaction type Sale, commission. Based on this document, you can subsequently register the document Report of the commission agent (agent) on sales. The document will be automatically filled in with the goods transferred to the commission; then you will also need to add a list of services sold under the agency agreement.

On the Remuneration tab, in a manner similar to the document Report to the principal (principal), the fact of offset of the agency fee from the cost of goods and services paid by buyers is drawn up.

From the principal's report, you can issue an issued invoice for goods sold and register the received invoice for the agency fee - see fig. 5.

Rice. 5

Debit 90.02.1 Credit 45.01 – sale of goods transferred on commission; Debit 62.01 Credit 90.01.1 – sale of goods transferred on commission; Debit 90.03 Credit 68.02 – VAT on sales of goods; Debit 62.01 Credit 91.01 – sale of delivery services; Debit 90.03 Credit 68.02 – VAT on the sale of delivery services; Debit 76.09 Credit 60.01 – for the amount of the commission agent’s remuneration; Debit 19.04 Credit 60.01 – VAT on the commission agent’s remuneration. Debit 60.01 Credit 62.01 – offset of agency fees against receipts from buyers.

Thus, we have illustrated that in the 1C: Accounting 8 program (rev. 2.0) the most complex version of the operation under an agency agreement is fully automated.