List of documents for obtaining a deduction for the purchase of a plot of land with a house

- declaration in form 3-NDFL

- application addressed to the head of the tax authority at the place of registration for the provision of a property deduction

- application addressed to the head of the tax authority at the place of registration for a refund of income tax to your personal account

- passport of an individual (buyer) of a land plot with a residential building

- TIN of an individual (buyer) of a land plot with a residential building

- contract for the sale and purchase of a land plot with a residential building

- certificate of ownership of land

- certificate of ownership of a residential building

- certificate of income in form 2-NDFL for the reporting year (from all places of work for the reporting year)

- receipt of money

- act of acceptance and transfer of land with a residential building

- personal bank account details for tax refund

Using a tax deduction for several residential properties

Until 2014, the Tax Code contained a restriction that a tax deduction for the purchase of an apartment/house/land could be received by a person only once in his life. In this case, it did not matter at all for what amount the housing was purchased and in what amount of the deduction was used.

It was impossible to get it again. For example, if a citizen bought a share in an apartment for 100 thousand rubles in 2005 and received a deduction from it (he returned 13 thousand rubles), then he could not claim another deduction.

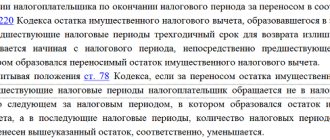

In the new edition of the Tax Code, this restriction has been changed: now, if the deduction is not received in the maximum amount (i.e. from an amount less than 2 million rubles), its balance can be received when purchasing other housing properties (paragraph 2, paragraph 1 3 Article 220 of the Tax Code of the Russian Federation).

However, you should not rush to rejoice for those who in the past did not receive a deduction in full (for an amount less than 2 million rubles). Unfortunately, you will not be able to receive the rest of the deduction when purchasing another home. This is due to the fact that the new rules apply only to legal relations that arose after January 1, 2014.

If you have already used the deduction for housing purchased before January 1, 2014, then the old rules apply to you - you can use (or rather have already used) the deduction only once in your life.

See Letter of the Federal Tax Service of Russia No. BS-4-11/ [email protected] dated 09.18.2013, Letter of the Ministry of Finance of Russia dated 07.26.2016 No. 03-04-05/43559, dated 03.13.2015 No. 03-04-05/13501, dated February 10, 2015 No. 03-04-05/5616, clause 2 of Art. 2 of Law No. 212-FZ.

Let's look at a few examples to better understand the situation:

Example: In 2006, Dostoevsky F.M. bought an apartment worth 500,000 rubles and received a tax deduction from it (returned income tax in the amount of 65 thousand rubles). In January 2020, citizen Dostoevsky bought a new apartment worth 3,000,000 rubles.

Having read about the changes in the law, he wanted to receive the rest of the deduction in the amount of 1,500 thousand rubles from a new purchase. Dostoevsky was denied a deduction for a new apartment, since he had already taken advantage of a deduction for housing purchased before 2014.

Example: In 2021 Pushkin A.S. bought an apartment worth 1,500,000 rubles, and in 2021 Pushkin A.S. bought a second apartment worth 1,000,000 rubles.

Since both apartments were purchased after January 1, 2014, Pushkin A.S. will be able to receive a deduction in the amount of 1,500,000 rubles from the first apartment (for a return of 195 thousand rubles) and an additional deduction in the amount of 500,000 rubles from the second apartment (for a return of 65 thousand rubles).

Please note: this rule does not apply to the mortgage interest deduction. Thus, you can receive a tax deduction on mortgage interest when purchasing a new home on credit, if you previously received the main deduction when purchasing another home (purchased before January 1, 2014). You can read more about this opportunity in our article - New opportunity to get a mortgage interest deduction.

Example: In 2014, Solodov A.V. purchased an apartment worth 1.7 million rubles with his own funds and received a tax deduction. In 2021 Solodov A.V. bought an apartment for 6 million rubles, while he took out 4 million rubles as a mortgage.

Since earlier Solodov A.V. already received a deduction when buying an apartment, but not for the entire amount of the deduction, he will be able to get a deduction for mortgage interest and the balance of the main deduction for the previous apartment (2 million rubles - 1.7 million = 300 thousand rubles).

It is important to pay attention to the following point: despite changes in the law, a deduction for mortgage interest is always provided for only one property, even if both properties were purchased with a mortgage after January 1, 2014. See paragraph 4, para. 2 clause 8 art. 220 Tax Code of the Russian Federation.

Example: In January 2021, Pushkin A.S. bought an apartment worth 1,500,000 rubles with a mortgage, and in February 2021, Pushkin bought a second apartment worth 1,000,000 rubles with a mortgage.

Since both apartments were purchased after January 1, 2014, Pushkin A.S. will be able to receive a deduction in the amount of 1,500,000 rubles from the cost of the first apartment (to be returned 195 thousand rubles) and to receive an additional deduction of 500,000 rubles from the second apartment (to be returned 65 thousand rubles).

However, he will be able to receive a deduction from the mortgage interest paid only for one of the apartments of his choice.

Documents for obtaining a tax deduction when purchasing an apartment

- declaration in form 3-NDFL.

- application addressed to the head of the tax authority at the place of registration for the provision of a property deduction

- application addressed to the head of the tax authority at the place of registration for a refund of income tax to your personal account

- certificate of income in form 2-NDFL for the reporting year (from all places of work for the reporting year)

- copy of the passport

- copy of TIN certificate

- copy of the apartment purchase and sale agreement

- copy of the Certificate of registration of ownership of the apartment

- copy of the transfer deed for the purchase and sale of an apartment

- copy of receipt for receipt of money

Delay in payment of tax deduction

If the money has not been received and the deadline for the desk audit has long passed, the taxpayer can contact the tax service for clarification.

A delay in payment means some kind of error in the declaration or in the documents provided. The tax service is obliged to notify about the presence of shortcomings during the desk audit. In practice, district tax inspectorates may not send notifications if there are errors. The taxpayer needs to independently control the progress of his business.

If a delay occurs, you should immediately contact the office department and find out when the money for the tax deduction will arrive. It is possible that not all documents were attached to the declaration. After eliminating the shortcomings, the tax inspector sends an order to transfer the refund. The taxpayer has the right to collect interest for violation of the return deadlines. All requests to the tax service should be submitted in writing to the head of the inspectorate.

The deadline for a desk audit cannot be accelerated. If the taxpayer wants to receive compensation faster, he is required to have a correctly completed declaration and a complete package of documents. This will avoid delays during the verification process.

Documents for obtaining a tax deduction when purchasing an apartment with a mortgage

- declaration in form 3-NDFL

- application addressed to the head of the tax authority at the place of registration for the provision of a property deduction

- application addressed to the head of the tax authority at the place of registration for a refund of income tax to your personal account

- certificate of income in form 2-NDFL for the reporting year (from all places of work for the reporting year)

- copy of the passport

- copy of TIN certificate

- copy of the apartment purchase and sale agreement

- copy of the Certificate of registration of ownership of the apartment

- copy of the transfer deed for the purchase and sale of an apartment

- a copy of the receipt for receiving the money.

- loan agreement for the purchase and sale of an apartment

Example 3: Buying an apartment with a mortgage

Conditions for purchasing property: In 2021, Ivanov I.I. purchased an apartment for 8 million rubles, of which 6 million rubles were taken out on a mortgage loan. In 2021 Ivanov I.I. paid interest on 100 thousand rubles.

Income and income tax paid: Ivanov I.I. earned 3 million rubles in 2029, from which he paid personal income tax.

Calculation of the deduction: The maximum amount of property deduction when purchasing a home is 2 million rubles. Additionally Ivanov I.I. can receive a tax deduction in the amount of 100 thousand rubles on mortgage interest paid. Total for 2021 Ivanov I.I. will be able to return 2,100,000 rubles. x 13% = 273 thousand rubles. He will be able to return this entire amount at once, because... the personal income tax he paid is more than 273 thousand rubles.

In subsequent years, Ivanov I.I. will only receive a tax deduction on mortgage interest, since he has already received the main deduction for housing. Since the loan agreement was concluded after January 1, 2014, the maximum amount of mortgage interest deduction that he can receive is 3 million rubles. (up to 390 thousand rubles to be returned).

Documents for obtaining interest deductions

- Declaration in form 3-NDFL.

- Application addressed to the head of the tax authority at the place of registration for the provision of a property deduction

- Application addressed to the head of the tax authority at the place of registration for an income tax refund to your personal account

- Certificate of income in form 2-NDFL for the reporting year (from all places of work for the reporting year)

- Copy of the passport.

- A copy of the TIN certificate.

- A copy of the apartment purchase and sale agreement

- Copy of the Certificate of registration of ownership of the apartment

- A copy of the transfer deed for the purchase and sale of an apartment

- A copy of the receipt of money.

- Loan agreement for the purchase and sale of an apartment

- Loan agreement for the purchase and sale of an apartment

- Certificate from the bank on interest paid for the reporting year

Example 2: Receiving a deduction by an individual entrepreneur using the simplified tax system

Conditions for purchasing property: In 2021 Petrov P.P. bought an apartment for 3 million rubles.

Income and income tax paid: Petrov P.P. works as an individual entrepreneur under a simplified taxation system and, accordingly, does not pay personal income tax at a rate of 13%.

Calculation of the deduction: The maximum deduction amount per apartment is 2 million rubles. (i.e. you can return up to 2 million rubles x 13% = 260 thousand rubles). But since Petrov P.P. did not pay income tax in 2020, he will not be able to receive a tax deduction for this year.

If Petrov P.P. in the future, if he gets another job where he will pay personal income tax, he will be able to apply for a tax deduction and get back up to 260 thousand rubles.

List of documents for receiving social deductions for treatment

- Declaration in form 3-NDFL

- A copy of the medical organization’s license to carry out medical activities

- Documents confirming the cost of treatment or purchase of medicines (certificate from a medical institution about payment for medical services for submission to the tax authority of the Russian Federation, cash receipts, contracts for medical services)

- Copy of the passport

- Copy of TIN certificate

- Certificate of income in form 2-NDFL for the reporting year (from all places of work for the reporting year)

- Application addressed to the head of the tax authority at the place of registration for the provision of a property deduction

- Application addressed to the head of the tax authority at the place of registration for an income tax refund to your personal account

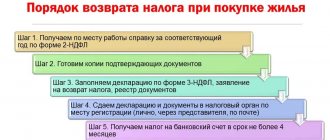

Deadlines for payment of tax deductions after filing the 3rd personal income tax.

After submitting the declaration and all accompanying documents to the tax authority, it carries out a desk audit, which includes a direct check of the declaration itself, as well as all provided documents for their authenticity, by requesting information from the relevant authorities that issued these documents. Upon completion of the desk audit, the Federal Tax Service makes a decision on granting or not granting a tax deduction.

The decision to provide a tax deduction must be made within 3 months from the date of filing the declaration, in accordance with Article 88 of the Tax Code of the Russian Federation.

It would not be amiss to note that if you have a personal taxpayer account, you can monitor the progress of the verification of your declaration in the “Taxpayer Documents > Electronic Document Flow” section. After the Tax Service makes a positive decision on the payment of the deductions due to you, you must transfer funds to the bank account specified in the application.

In accordance with Art. 78 of the Tax Code of the Russian Federation, the transfer of funds may take up to one month.

In total, in the worst case scenario, you will have to wait no more than 4 months for a tax deduction. If the payment period has been delayed for a longer time, you can contact your tax office to find out the reasons.

List of documents for receiving social deduction for education

- Declaration in form 3-NDFL

- Copy of the passport

- A copy of the child’s birth certificate (if we receive a deduction for a child)

- Documents confirming the fact of guardianship or guardianship (in case of guardianship)

- Copy of TIN certificate

- Certificate of income in form 2-NDFL for the reporting year (from all places of work for the reporting year)

- Agreement with an educational institution

- License of the institution to provide educational services

- Payment documents confirming payment for training, which must indicate the details of the person who paid for the training

- Application addressed to the head of the tax authority at the place of registration for the provision of a property deduction

- Application addressed to the head of the tax authority at the place of registration for an income tax refund to your personal account

List of documents for registration of deductions

In order to apply for a property deduction when purchasing an apartment, house or land through the tax office, you will need the following documents:

- Tax return in form 3-NDFL . The original is submitted to the Federal Tax Service .

- Passport or a document replacing it. Certified copies of the first pages of the passport (basic information + pages with registration) are submitted to the Federal Tax Service. Note: a copy of your passport is not included in the required documents by law, but many tax offices require you to attach it.

- Certificate of income in form 2-NDFL. You can obtain such a certificate from your employer. The original 2-NDFL certificate is submitted to the Federal Tax Service Note: if you worked in several places during the year, you will need certificates from all employers.

- Application for a tax refund with account details to which the tax office will transfer the money to you. The original is submitted to the Federal Tax Service . You can download a sample application here: Application for tax refund for property deduction.

- Purchase and sale agreement or equity participation agreement . A certified copy of the agreement is submitted to the Federal Tax Service.

- Payment documents confirming the fact of payment for housing (usually payment orders, payment receipts or receipts). Certified copies of payment documents are submitted to the Federal Tax Service.

- Extract from the Unified State Register of Real Estate (certificate of state registration of property rights). A certified copy of the extract (registration certificate) is submitted to the Federal Tax Service. Note: if you purchased an apartment under an equity participation agreement, then the extract (certificate) is not a mandatory document (accordingly, it does not need to be submitted to the tax authority).

- Acceptance and transfer certificate of housing. A certified copy of the act is submitted to the Federal Tax Service. Note: if you purchased an apartment under a purchase and sale agreement, then the transfer and acceptance certificate is not a mandatory document (accordingly, it does not need to be submitted to the tax authority).

If the purchase of an apartment was made with the help of a mortgage (or a housing loan) and a refund is made on interest paid , then additionally the following must be submitted:

- Loan agreement with the bank. A certified copy of the agreement is submitted to the Federal Tax Service.

- Certificate of interest withheld for the year (you will receive it from the bank that issued the loan to you). The original is submitted to the Federal Tax Service . Note: some tax inspectorates may also request copies of payment documents confirming the fact of payment of the loan (receipts, checks, payment orders, statements, etc.).

In case of purchase of property by spouses, joint ownership is additionally provided:

- Application for determination of shares . The original is submitted to the Federal Tax Service . You can download a sample application here: Application for determination of shares in joint property;

- A copy of the marriage certificate .

In case of receiving a tax deduction for a child, the following are additionally provided:

- Copy of birth certificate ;

- Application for determination of shares (if both parents participate in the share);

In case of self-construction:

- Consumable documents (checks, receipts) for construction materials. Certified copies of expenditure documents are submitted to the Federal Tax Service;

In case of receiving a tax deduction for finishing/repair :

- Contract for repair/finishing and consumable documents related to the contract (checks, receipts and receipts). Certified copies of documents are submitted to the Federal Tax Service.

To apply for a deduction you will also need:

- TIN number (must be indicated in the declaration). You can find it in your “Certificate of Registration with the Tax Authority” or on the website of the Federal Tax Service (https://service.nalog.ru/inn-my.do).

- Account details to which the money will be transferred (must be indicated in the tax refund application).

It should be noted that in order to avoid delays and refusals, you should contact the tax service with the most complete package of documents .

Necessary documents for preparing a tax return when selling a car

- Application for a deduction in the form of the tax authority;

- Passport of the individual who received income from the sale of the car;

- TIN of the individual who received income from the sale of the car;

- PTS of the sold vehicle;

- Purchase and sale agreement for the purchase and sale of a sold vehicle;

- A receipt confirming receipt of a sum of money when selling a car from an individual (legal entity).