Home / Taxes / What is VAT and when does it increase to 20 percent? / VAT payers

Back

Published: 07/11/2017

Reading time: 5 min

0

454

Many organizations that are legally exempt from paying VAT wonder why many large companies refuse to enter into contracts as soon as they find out that they are operating without the allocation of VAT. The answer to this question is related to the peculiarities of taxation.

The fact is that OSNO companies issue invoices to their clients in which VAT is highlighted and the amount of VAT they paid can be deducted from the budget.

For example, a company on OSNO sold goods worth 10 million rubles, of which 1.53 million rubles. it must remit to the state in the form of VAT. But during the same period, she spent 7 million rubles on the services of other organizations at OSNO. This amount included her VAT expenses of 1.07 million rubles.

It is by this amount that she can reduce her tax burden in the form of VAT. Consequently, not 1.53 million rubles are paid to the budget, but 460 thousand rubles.

- Organization without VAT

- Features of interaction

- Answers to questions The invoice is issued without VAT, but the payer works with VAT

- Re-invoicing of services without VAT by VAT payers

- The counterparty invoiced VAT on the simplified tax system

- The organization sells on OSNO without VAT

Differences between the Federation Council if there is no taxation on products

To create a document, use the form approved by Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137, with amendments dated August 19, 2017 No. 981, which came into force on October 1, 2017.

An invoice without VAT is issued on the same form and according to the same rules as an invoice with VAT. The only difference is that in columns 7 and 8, where the tax rate and amount are indicated, “Without VAT” must be written.

If all shipped products are exempt from tax, when registering the SF, in all lines in which the names are listed, in columns 7 and 8, you must indicate “Without VAT.” The same entry is made in the line “Total payable” in column 8. If in the sold batch one part of the product is subject to VAT, the other is not subject to taxation, the entry “Without VAT” is entered only opposite the corresponding items.

The lines where taxable goods are listed indicate the rate and amount of VAT. In the “Total payable” field in column 8, enter the total tax amount, including only taxable items. Invoices for received advances are issued in compliance with the same rules.

For more information about what an invoice is and when it is used, read our article.

Is SF required if an organization operates without value added tax?

According to paragraph 3 of Art. 169 of the Tax Code of the Russian Federation, VAT payers are required to issue an invoice. SF is not issued if you work as an individual entrepreneur or legal entity that is not a tax payer.

When should such a document be issued?

A taxpayer who is a seller of goods or a provider of services is obliged to issue an invoice without VAT only if he uses the right to exemption from VAT in accordance with Art. 145 of the Tax Code of the Russian Federation (clause 5 of Article 168 of the Tax Code of the Russian Federation).

This right arises if a legal entity or individual entrepreneur:

- receives revenue of no more than 2 million rubles. for 3 consecutive months;

- does not sell excisable goods.

In other cases, is it possible for organizations that are not tax payers to issue tax invoices without VAT? According to the letter of the Ministry of Finance No. 03-07-09/8423 dated February 15, 2017, this is not necessary, but there is a right to this matter.

Read about who issues the invoice here.

Use Cases

The preparation of such a document is provided if:

- Only part of the goods sold is exempt from tax (Article 149 of the Tax Code of the Russian Federation). The company carries out transactions simultaneously with products subject to VAT and not subject to VAT. In this case, the accounting program will generate a general invoice and invoice for the entire batch of goods with the same total amount.

- If the entire batch of products sold is not subject to VAT , issuing an invoice along with invoices and acts makes it possible to create a convenient set of documents while maintaining the numbering.

Who fills out the form?

Only the seller of goods or the provider of services has the right to issue an SF. Thus, he documents the completion of the transaction.

Invoicing Procedure

To avoid any problems, you need to determine how to issue an invoice to the individual entrepreneur.

The process itself looks something like this:

- The client wants to purchase goods and services. To do this, he contacts the seller.

- Based on the buyer's wishes, the seller issues an invoice for payment and then sends the form to the client.

- The specified amount is paid to the contractor's bank account.

- After checking the fact of payment, the seller carries out the actions agreed with the client.

On video: The process of issuing an invoice for payment in 1c

It is recommended to pay special attention to whether VAT is highlighted in the invoice:

- if an individual entrepreneur issues an invoice without VAT, it means that he uses the simplified tax system. The document must indicate the total amount and about;

- if the debit is issued by an individual entrepreneur in the general mode or by an enterprise, then the VAT rate must be entered in the form, highlighting its amount.

How to send it to the recipient?

When setting the SF, you must adhere to the following rules:

- If the document is drawn up in paper form, the first copy must be given to the buyer, and the second remains with the seller (read why both the seller and the buyer need the SF). In case of electronic exchange, which is carried out through an accredited operator, the SF is issued in only one copy.

- The period for issuing the document is 5 days from the date of delivery.

- According to the letter of the Ministry of Finance No. 03-07-09/85517 dated December 21, 2017, the names of goods, services and works must comply with the contract.

- If corrections need to be made, a new copy of the SF is created. In this case, the serial number and date of the original document are preserved.

Why is an invoice required?

An invoice is the main document for VAT. If the recipient does not pay the tax, then the invoice is not allowed to be issued. Here you need the consent of the parties, drawn up in writing.

VAT defaulters need to issue similar invoices if:

- they act as tax agents;

- perform the duties of an intermediary;

- goods are imported from abroad.

Upon prepayment from the buyer, the supplier must issue an advance invoice. After the goods are shipped, the invoice is recorded in the purchase journal. If the customer neglects to issue the document, the tax inspector may impose a fine and charge unaccounted VAT on prepayments.

On video: How to issue an invoice to a client?

What columns and lines are present in the form?

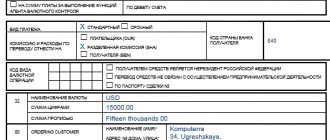

Information that must be present in the Federation Council is given in paragraph 5 of Art. 169 of the Tax Code of the Russian Federation.

- Lines 1-8 of the form are intended for the details (names, addresses, identification codes) of the participants in the transaction - the seller and the buyer, as well as the consignor and consignee, and indication of currency. The table shows the invoice part of the document.

- Columns 1-9 contain information about the product (name, units of measurement, quantity, price, cost with and without VAT, tax rate and amount, excise duty).

- Columns 10-11 – data on the origin of the goods.

Filling example

As of October 1, 2017, new requirements for the preparation of this document began to apply. The filling procedure is as follows:

- In line (1) we indicate the serial number and date of issue. For all types of SF there is a common numbering. They are recorded in chronological order (it is allowed to add a letter designation to the number). When making corrections, in line (1a) we indicate the number of the correction; when filling out for the first time, a dash is added.

- Lines (2), (2a), (2b) contain information about the seller:

- for legal entities, it is necessary to indicate the full or short name, detailed address as written in the Unified State Register of Legal Entities, identification numbers (TIN/KPP);

- for individual entrepreneurs, the full name, address as entered in the Unified State Register of Entrepreneurs, TIN and registration information are entered.

- If the shipper and the seller are represented by the same organization, in line (3) you must indicate “The same.” If the shipper is another company or person, enter the full or short name and address. We put a dash if the invoice relates to work or services.

- In line (5) you need to indicate the payment document number only if there is an advance payment; if there is no prepayment, then this item remains blank.

- Information about the buyer is entered in lines (6), (6a), (6b) similarly to (2), (2a), (2b). If the buyer and the consignee are represented by the same organization, in field (4) you need to put the “Same” checkbox. If the consignee is another organization, indicate its name and address. If the invoice is for work performed or services provided, a dash should be included.

- In line (7) select the name of the currency. Accounting programs automatically enter the digital code.

- Line (8) is for the government contract ID. For other contracts it is not necessary to fill it out.

- The following columns are filled in in the table:

- Column 1 contains the names of goods, works or services.

- Column 1a indicates the product code. This field concerns only deliveries to the countries of the Euro-Asian Economic Union.

- Units of measurement are entered in columns 2-2a in accordance with OKEI. If the invoice concerns work or services, dashes should be added.

- In column 3 we indicate the quantity or volume based on units of measurement. If 2-2a is not filled in, there will also be a dash here.

- In column 4 the price per unit is entered as it is given in the contract.

- The total cost of each item excluding tax is reflected in column 5. The final line will contain the total cost of the entire delivery.

- Column 6 is filled in only for excisable goods. Here you need to indicate the amount of excise tax included in the price. In other cases, the note “Without excise duty” is made.

- When registering a SF without tax, in fields 7 and 8 you need to make the entry “Without VAT”. If some items are subject to tax, the rate and amount are entered opposite them.

- Column 9 reflects the cost of goods, works or services including tax.

- Column 10 must contain the digital product code. Columns 10, 10a, 11 are filled in for goods produced outside the Russian Federation.

- Columns 5, 8 and 9 of the bottom line contain the totals.

In the Federation Council, it is allowed to indicate two addresses (letter of the Ministry of Finance of the Russian Federation No. 03-07-09/85517 dated December 21, 2017). If the actual address, which differs from that recorded in the register, is recorded in the contract, it should be entered in an additional line.

Invoices without VAT are signed according to general rules. The paper form is certified by the signatures of the manager and chief accountant or authorized persons. If the document is issued by an individual entrepreneur, it must contain the personal signature of the individual entrepreneur or an authorized representative. More information about the invoice for individual entrepreneurs can be found here.

Certification of an invoice with a facsimile signature is not acceptable (letter of the Ministry of Finance No. 03-07-09/49478 dated August 27, 2015). When exchanging documents electronically, a certificate of the electronic signature verification key is required (letter of the Ministry of Finance of the Russian Federation dated September 12, 2016 No. 03-03-06/2/53176, Federal Tax Service of the Russian Federation dated May 19, 2016 No. SD-4-3/8904).

The invoice is certified only by one enhanced qualified electronic signature of the manager or authorized person. The electronic document does not require the signature of the chief accountant.

More details on filling out an invoice can be found here.

From the video you will learn how to correctly fill out an invoice if the company is not a VAT payer:

Required details

Invoices are not official accounting documents. There is no set form that establishes or standardizes the generally accepted form of a document.

To issue an invoice for payment from an individual entrepreneur (electronic,

paper document), you must provide the following information:

- details of the enterprise/individual entrepreneur (identification code, legal form of the business entity, legal address of the LLC, name of the organization);

- bank details (BIC, name, actual address, account number);

- OKPO, OKONH (if available).

After entering the details of the entrepreneur and the recipient, the number assigned to the account and the date of creation of the document are provided. In addition to this data, it will be indicated whether the debit is issued with or without VAT. At the end of the document, the signature, surname, and initials of the business entity are affixed. A seal is not required.

You can develop an invoice form yourself in programs such as Excel or Word. After you create a blank form, you can use it as a template. The invoice can be issued on the seller's letterhead or without it.

Now there are many accounting programs that can facilitate the creation of such documents through automated generation of forms. You can also issue an invoice for payment from an individual entrepreneur online. To do this, you need to use the free program or purchase a paid, improved version.

The account must have an individual number. Numbering is reset at the beginning of the year and can have various types, from numeric to special. The sample invoice issued by the individual entrepreneur must comply with the established form.

On video: Sample invoice and filling it out

How to register?

An organization that enjoys the right to be exempt from VAT and is obliged to issue invoices registers them in a journal in the sales book with the note “Without VAT.” Other tax evaders are not required, but have the right to register the document in the sales ledger.

The buyer who receives such a document does not reflect it in the purchase book, since there is no tax. When issuing and receiving invoices from counterparties, it is necessary to carefully monitor changes in legislation governing the procedure for issuing and exchanging documents.