Normative base

Business trips are regulated by Article 166 of the Labor Code of the Russian Federation. The duration and purposes of official trips are established by order, signed by the director. Let's consider the nuances of business trips specified in the law:

- The employee retains his place of work and salary in the established amount throughout the trip.

- An employee has the right to receive sick leave payments on the basis of Article 167 of the Labor Code of the Russian Federation.

The procedure for registering a business trip is regulated by the following regulations:

- Federal Law “On Currency Regulation” dated December 10, 2013. This law specifies the conditions of the procedure, as well as the features of this process;

- Labor Code of the Russian Federation;

- Tax Code of the Russian Federation;

- Government Decree No. 173 of October 13, 2008;

- Local regulations (for example, collective agreements).

The employer is recommended to regularly monitor all changes in laws in order to correctly arrange a business trip.

Who can be sent on a business trip?

Some employees cannot be sent on business trips. This:

- Pregnant women.

- People with disabilities that prohibit travel.

- Persons under 18 years of age.

- Employees on study leave.

Some employees can be sent on foreign trips only with their written consent. This category of workers includes:

- Women with babies under 3 years old.

- Single fathers and single mothers with children under 5 years old.

- Parents with minor children with disabilities.

- People caring for incapacitated close relatives.

If there is no written consent, the employer cannot send the employee on a business trip. Otherwise, sanctions may be imposed on the company.

Personal card

The company transfers an advance payment for travel expenses to its employee to his bank card in rubles. The employee also pays with this card for expenses on business trips abroad. In this case, the Ministry of Finance believes that expenses should be determined based on the amount spent according to primary documents at the exchange rate set by the bank on the date of debiting the funds (letters dated January 22, 2016 No. 03-03-06/1/2318, dated July 17, 2015 No. 03-03-06/41128). A document confirming the rate can be an extract from the employee’s card account, where the write-off rate will be visible; such an extract must be certified by the bank (letter of the Ministry of Finance of Russia dated July 10, 2015 No. 03-03-06/39749).

Registration procedure

Registration of a business trip involves the creation of a number of papers. The first most important document is an order. The employee must be familiarized with it. The employee signs to confirm familiarization. An order will need to be issued. The business trip is taken into account in the time sheet, as well as in the journal. Accepted by Fr. Let's consider all the stages of registration of a business trip:

- Report to the manager on the travel arrangements.

- Issuance of an order specifying the purposes of the trip, its objectives and duration.

- Issuance of a travel certificate if an employee is sent to the CIS countries.

- Familiarization of the employee with the completed documents.

- Calculation of travel costs. This takes into account advances and exchange rates.

IMPORTANT! The procedure for registration of one-day trips is similar to registration of multi-day trips.

ATTENTION! The employee’s obligation to go on business trips must be established in the employment contract. If this condition is not specified in the agreement, the person may refuse the trip.

Funds for reporting

Let's start with the topic of issuing funds for reporting due to the fact that there have been changes in this issue in 2021. Now, in order to issue funds against a report, you can draw up an administrative document, and it is no longer necessary to require an application from the employee to issue money. It is also now possible to issue funds on account, even if the employee has not yet accounted for previously received money (Instruction of the Bank of Russia dated June 19, 2021 No. 4416-U). It is important that an administrative document is drawn up for each disbursement of funds. It can be issued, for example, in the form of an order. If it is customary for a company to write applications for the issuance of funds against a report, then it is necessary to take into account that the manager, in addition to his signature and the date of drawing up the document, must indicate the amount issued and the period for its return (letter of the Bank of Russia dated September 6, 2021 No. 29-1-1 -OE/20642).

I note that most companies issue funds in rubles, and employees themselves convert them into foreign currency, since this simplifies accounting; there is no need to create additional sub-accounts to account for amounts in foreign currency.

note

It is illegal to transfer a personalized corporate card from one employee to another. But in practice, such cases do occur; in such situations, I recommend attaching a memo to the expense report stating that the expenses were paid from the manager’s card.

Let us dwell in more detail on the situation when employees are still given amounts in foreign currency for travel expenses; this option is permitted by the legislation of the Russian Federation (clause 16 of the Regulations, clause 9, part 1, article 9 of the Federal Law of December 10, 2003 No. 173- Federal Law “On Currency Regulation and Currency Control”). When issuing an advance in foreign currency, the company is guided by PBU 3/2006 “Accounting for assets and liabilities, the value of which is expressed in foreign currency,” approved by Order of the Ministry of Finance of November 27, 2006 No. 154n, by virtue of paragraph 1 of Article 30 of Law No. 402-FZ. Currency revaluation takes place in accordance with the general procedure.

Let's look at receiving money for reporting using an example: on October 30, 2017, the company received foreign currency from the bank in the amount of $1,000 for travel expenses. On November 1, 2021, the currency was issued to an employee by order of the manager for a business trip to the United States. The employee submitted the approved advance report to the accounting department on November 20, 2021. An employee reported an overspend of $100. How to record these transactions in accounting?

October 30, 2021:

Debit 50 (sub-account “Settlements in foreign currency, US dollars”) Credit 52

The bank received foreign currency funds for travel expenses in the amount of USD 1,000 (RUB 57,500 at the rate of RUB 57.5/USD);

October 31, 2021:

Debit 50 (sub-account “Settlements in foreign currency, US dollars”) Credit 91.1

The exchange rate difference resulting from the revaluation of foreign currency on the reporting date in the amount of 500 rubles is reflected. ($100 × 58 rubles = 58,000 rubles – 57,500 rubles = 500 rubles);

November 1, 2021:

Debit 71 (sub-account “Settlements in foreign currency”) Credit 50 (sub-account “Settlements in foreign currency, US dollars”)

The currency was issued to a company employee on account of travel expenses in the amount of USD 1,000 (RUB 58,200 at the rate of RUB 58.2/USD);

Debit 50 (sub-account “Settlements in foreign currency, US dollars”) Credit 91.1

The exchange rate difference in the amount of 200 rubles is reflected. (58,000 rubles (as of 10/31/2017) – 58,200 rubles (as of 11/01/2017) = 200 rubles);

November 20, 2021:

Debit 10, 20, 26, 44 and other accounts for accounting for inventory and expenses accepted for accounting in the company Credit 71 (sub-account “Calculations in foreign currency”)

Expenses in the amount of USD 1,000 are reflected (RUB 58,200, exchange rate taken as of the date the currency was issued to the employee);

Debit 10, 20, 26, 44 and other accounts for accounting for inventory and expenses accepted for accounting in the company Credit 71 (sub-account “Calculations in foreign currency”)

Reflected expenses in the amount of 100 US dollars (5950 rubles at the rate of 59.5 rubles/US dollars). The overexpenditure is reflected at the exchange rate on the date of approval of the advance report, since no conversion document was provided.

I would like to note that in practice, it is much easier for accounting departments to issue funds against reporting in rubles if it is expected that payments will be made in cash on a business trip, but it is even more convenient to transfer an advance or reimburse expenses to the employee’s card.

Stages of preparation for a business trip

First you need to find out all the conditions offered by the receiving party. For example, a foreign company can pay for an employee’s accommodation. You need to find out from the employee whether he has a foreign passport. Let's consider all the stages of preparing for the trip:

- Visa registration, if required.

- Booking a hotel room.

- Preparation of all necessary documents.

- Calculation of travel expenses and daily allowances to determine the amount of the advance.

- Salary calculation for the business trip period.

- Payment of personal income tax and contributions.

Our calculator will help you calculate the amount of travel allowance, knowing your earnings for the billing period, the number of days worked during the billing period, the number of days on a business trip and the amount of daily allowance in the organization.

IMPORTANT! Until 2021, restrictions on the duration of business trips were established. They have now been removed. Long trips must be economically justified. In particular, the income from the trip must exceed the expenses.

ATTENTION! All primary documents related to the business trip are attached to the advance report after the end of the trip. It must be submitted within 3 days after the employee arrives.

Confirmation of spending

Employees must confirm all their expenses at the end of their trip. Checks, plane tickets, etc. can be used for this. The accounting department must accept the advance response and then reimburse the existing expenses. The advance payment issued before the business trip is first deducted from the amount of expenses.

Calculation example

To understand the calculation procedure, it is recommended to familiarize yourself with the example. This will also eliminate errors that could cause serious violations.

For example, a company representative goes on a working visit to France. The period of stay abroad is 15 days. In this case, the employee needs 1 more day to get to another city to the airport, and 1 day to return. Thus, the duration of the entire business trip is 17 days.

Calculation procedure:

- Daily allowance for a 2-day trip within the Russian Federation is 1,400 rubles (700 rubles * 2 days).

- The minimum daily allowance established by law for a trip to France is 65 euros - 4,490 rubles at the exchange rate for February.

- The period of stay in France is 15 days, hence 4,490 rubles * 15 = 67,350 rubles.

- To this amount should be added 1,400 rubles - daily allowance when traveling within the Russian Federation.

- The total amount is 68,750 rubles.

This amount exceeds the established norm. Therefore, they are included in the employee’s income and are taxable.

Procedure for providing an advance

Before sending an employee on a business trip, you need to draw up an estimate to determine the amount of the advance. It may include the following areas of expenditure:

- Directions

- Accommodation.

- Payment of daily allowances.

- Issuance of insurance.

- Transporting luggage.

- Telephone conversations.

- Registration of a foreign passport.

- Expenses when exchanging currency.

The estimate must be attached to the expenditure slip.

IMPORTANT! Currency exchange in the employee’s country of residence is difficult and involves additional expenses. Therefore, it is recommended to issue an advance in the currency of the state to which the employee is sent.

Who pays for obtaining a passport?

The employee himself must apply for a foreign passport. The associated fee is reimbursed by the company's accounting department. The employee must first present the appropriate receipt, as well as a copy of the passport. The costs of obtaining a foreign passport can be included in travel expenses. However, this point must be included in local acts.

Daily allowance

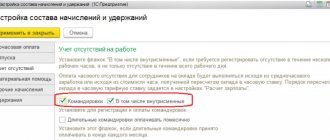

One of the accounting features when sending employees on business trips abroad may be the calculation and payment of daily allowances. Each company has the right to set its own daily allowance. The daily allowance established in the local regulatory act of the organization (“Regulations on business trips”) can be fully accepted as income tax expenses, but for personal income tax purposes limits are set - 700 rubles per day for business trips within the Russian Federation and 2,500 rubles per day for business trips abroad (Article 217 of the Tax Code of the Russian Federation). If the company accepts daily allowances in amounts exceeding these standards, then the employee will have to withhold personal income tax from the difference, as well as pay insurance premiums (clause 2 of Article 422 of the Tax Code of the Russian Federation).

Typically, the amount of daily allowance for Russia and for trips abroad differs. Daily allowances are paid according to the country of entry (clauses 17, 18 of the Regulations “On the Peculiarities of Sending Workers on Business Trips”, approved by Decree of the Government of the Russian Federation of October 13, 2008 No. 749, as amended on July 29, 2015). For business trips to countries included in the CIS, with which intergovernmental agreements have been concluded that border crossing marks are not made, the dates of departure and entry into the Russian Federation are determined by travel documents, and for business trips abroad - by border crossing marks in the international passport. For one-day business trips abroad, daily allowances are paid in the amount of 50 percent of the norm for business trips abroad (clause 20 of the Regulations on Business Travel).

It is noteworthy that if it is customary for a company to pay daily allowances for one-day business trips around Russia, then such payments are subject to insurance premiums. The Ministry of Finance, referring to paragraph 11 of the Regulations on Business Travel, explains that for a one-day business trip in Russia, daily allowances are not paid, therefore, paragraph 2 of Article 422 of the Tax Code of the Russian Federation does not apply, according to which, in particular, the daily allowances provided for in paragraph 3 of the article are not subject to insurance premiums 217 Tax Code of the Russian Federation. Therefore, daily allowances paid for a one-day business trip in the Russian Federation are subject to contributions. Moreover, if the employer reimburses expenses associated with a business trip, then such payments are not considered subject to insurance premiums, since they are not the employee’s income.

As for personal income tax, in letters of the Ministry of Finance dated October 1, 2015 No. 03-04-06/56259, dated March 1, 2013 No. 03-04-07/6189 (sent by letter of the Federal Tax Service of Russia dated March 26, 2013 No. ED-4 -3/ [email protected] ) the following position is indicated: “When sending an employee on a one-day business trip, the amounts of money paid to the employee in exchange for daily allowance are exempt from taxation in the amounts provided for in paragraph 3 of Article 217 of the Code.”

Taxation of travel expenses

Let's consider all the lists of costs, as well as the features of their taxation:

- Daily allowance. Must be recorded as an expense. If their amount does not exceed 2,500 rubles, the daily allowance will not be subject to personal income tax.

- Accommodation. Expenses will be included as expenses. Exception - the amount is highlighted as a stand-alone line in the invoice. An amount not exceeding 2,500 rubles per day will not be subject to personal income tax. Insurance premiums are not charged.

- Directions Expenses supported by documentation will be taken into account. If documents are missing, the amount will not be subject to personal income tax. Insurance premiums are also not charged.

- Taxi expenses. If taxi costs are justified and supported by papers, they are included in expenses. Expenses are not subject to personal income tax. Insurance premiums are charged.

- Medical insurance. Expenses for it will also be included in expenses. The amount will not be subject to personal income tax. Insurance premiums are charged.

These rules may change, and therefore you need to monitor all innovations in the Tax Code and related acts.

We pay and reimburse expenses

The accounting department of the enterprise accepts the advance report prepared accordingly and reimburses the costs incurred minus the advance received previously.

In addition to transportation, living expenses are also paid. The procedure for making reservations and renting housing is usually specified in a local document.

Sometimes it can be expensive to book a hotel room. In such cases, it is more profitable to rent housing. Then, when reporting, you need to attach a rental agreement.

Which exchange rate should be taken into account when calculating?

The Ministry of Finance of the Russian Federation, in its letter dated July 17, 2015, clarifies the advisability of paying for accommodation and daily allowances by using bank cards. Resolution of the Government of the Russian Federation No. 749 stipulates that the procedure for compensation is determined by a collective agreement.

Therefore, it is possible to issue foreign currency on account subject to compliance with the requirements of the legislation on currency regulation.

The currency exchange rate officially set by the bank is determined on the day the funds are written off.

How to formalize dismissal by transfer? Information is in our article. How to cancel an entry in a work book? Read here.

What polygraph questions do employers ask when applying for a job? Find out here.

Daily allowance in 2020

Calculation of daily allowances for business trips abroad is carried out taking into account the number of days of travel through Russian territory and from the moment of crossing the border according to customs marks.

Tax-free daily allowance standards are established by Article 217 of the Tax Code of the Russian Federation and amount to 700 rubles/day for Russian territory and 2,500 rubles for foreign territories.

Local documents may approve increased daily allowance rates, but then personal income tax is withheld from the difference.

An example of accounting transactions with daily allowances is reflected in the table below:

| Indicators | Amounts of funds (in rubles) | Postings |

| Condition: time spent abroad, including flight Moscow - Prague = 3 days | ||

| Issued for reporting to the employee at the rate of RUB 3,500/day. according to the collective agreement | 10500 | Dt 71 - Kt 50-1 |

| Reflected in the advance report | 10500 | Dt 20 - Kt 71 |

| Personal income tax withheld from excess amount ((3500-2500) * 13% * 3 days) | 390 | Dt 70 - Kt 68 |

Insurance premiums are not paid, since the amount of daily allowance is stipulated by the internal act of the organization.

Sometimes one day is enough for a trip abroad. Then the daily allowance is accepted at half the amount.

Accordingly, the standard will be 1250 rubles/day. (RUR 2,500 * 50%).

Costs for the production of a foreign passport and visa

During the preparation of documents for a business trip, it may become clear that the employee does not have a foreign passport.

The employee himself contacts the OVIR authorities to produce it. Payment of the state duty is reimbursed by the accounting department after presentation of the receipt and a copy of the completed passport.

You can apply for a visa yourself or with the help of a specialized company.

The costs of producing a foreign passport, obtaining a visa and possible courier services can be attributed to a business trip if such items are included in the local business trip document.

Accommodation standards

Legislative documents defining the norms of stay (residence) abroad have lost their force.

From 2021, only daily allowance standards for taxation apply.

The duration of the trip, accommodation conditions and reimbursement of travel expenses are stipulated by the company’s internal documents.

Procedure for issuing an advance

Before the traveler's departure, an estimate is drawn up to determine upcoming expenses.

Her articles are usually as follows:

- travel to and from the place of business;

- accommodation;

- daily allowance;

- registration of health insurance;

- transportation of luggage weighing up to 30 kg;

- telephone conversations;

- obtaining a visa and passport;

- expenses for currency exchange.

The estimate is attached to the expenditure order. To avoid difficulties with exchange, it is better to issue an advance to the traveler in the currency of the destination country.

Travel compensation

At the end of the official trip, the employee draws up a report providing all the primary information - tickets, boarding passes, baggage receipts, payment documents for consular and airport fees.

If you purchased an electronic ticket, then to receive compensation payments you will be provided with a printout of it and a boarding pass.

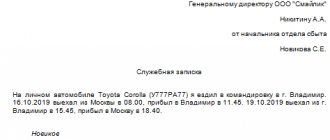

Traveling in a company car

The use of personal or official transport on a trip is possible if there is written permission from management.

To receive compensatory payments, the employee provides a waybill, paid bills, cash receipts, and receipts.

It is also necessary to provide a copy of the vehicle's registration certificate and a power of attorney in the case of driving a company vehicle rather than a personal one.

Rent a car

Nowadays, it has become popular to use a service such as car rental when traveling for business.

This is sometimes more economical than taking a taxi and allows you to more quickly solve your problems. To register, you need to contact the rental company and present your passport and driver's license.

In this case, the following documents are attached to the transport costs report:

- car rental agreement;

- vehicle return certificate;

- checks and invoices for payment for company services.

Using payment cards

It is very convenient for both business travelers and accounting departments to use corporate and personal bank cards during a business trip. After all, then the business traveler can pay for travel and accommodation costs by non-cash means, and also, if necessary, use an ATM to withdraw cash.

The accountant takes into account the following actual costs:

- payment of expenses at the Central Bank exchange rate on the day of approval of the advance report;

- conversion costs, confirmed by a bank statement.

Example:

An employee's business trip to Berlin for three days from February 1, 2020. The local document of the organization provides for a daily allowance standard for trips to Germany in the amount of 60 Euros per day. On February 1, 2016, daily expenses in the amount of 180 Euro were withdrawn in cash (according to the bank statement, 15,620 rubles were written off). 02/3/16 paid for a hotel room in the amount of 520 Euros (46,790 rubles written off). The employee's advance report was approved on 02/05/16, taking into account the payment of the cost of travel passes by the employer.

Expenses resulting from the trip are shown in the table below:

| Expenses | EURO exchange rate as of the date of report approval | Amount in EURO | Amount in RUBLES |

| Daily allowance for 3 days | 84,8104 | 180 | 15265,78 |

| Conversion costs | 354,22 (15620 – 15265,78) | ||

| Hotel accommodation | 84,8104 | 520 | 44101,41 |

| Conversion costs | 2688,59 (46790 – 44101,41) |

When paying with a bank card, do not forget to save your receipts!

Accounting and postings

Business trip expenses are accounted for the main type of activity.

The posting looks like this: Dt 20 (26, 44 ...) Kt 71 (“accountable persons”).

Conversion into Russian rubles is carried out at the time of issue of currency.

If we continue the example with a business trip to Berlin (Germany) and assume that the employee was given 100 Euros in cash for unexpected expenses on January 29, 2016, received from the bank on January 27, 2016, then the postings will be as follows:

- 01/27/16: Dt 50 subaccount “Currency cash desk” Kt 52 “Currency accounts” (currency received from the bank to the cash desk) 8888.58 rubles. (at the rate of 88.8858 rub./Euro);

- 01/29/16: Dt 71 - Kt 50 (issued to the employee from the cash register for travel expenses) - 8413.70 rubles. (at the rate of 84.1370 rubles/euro);

- 01/29/16: Dt 50 - Kt 91-1 (exchange rate difference accrued) - 474.88 rubles. (8888.58 – 8413.58).

If, as a result of the trip, an overexpenditure had arisen , then it should have been reflected in the posting Dt 71 - Kt 50 (the employee was issued an overexpenditure).

If the currency funds were underused and returned by the employee, then the posting is as follows: Dt 50 - Kt 71 (the balance of unused funds was returned to the cash desk).

Find out from our article what features the non-tariff wage system has. What does a salary certificate look like? Find out here.

Taxation

You can find out about expenses for business trips abroad, subject to taxes and contributions, from the table below:

| Expenses | Income tax | Personal income tax | Insurance premiums |

| Daily allowance | Are taken into account in expenses in the amount according to the local document | Not exceeding 2500 rubles are not taxed. for each day of a foreign business trip | Not credited |

| Accommodation (including booking) | Are taken into account in expenses if their cost is not highlighted as a separate line in the invoice | Not taxed in the amount according to the local act with documentary evidence. Not taxed up to RUB 2,500. per day, if there is no documentary evidence) | Not credited |

| Additional services provided by hotels | Are taken into account in expenses if their cost is not highlighted as a separate line | Not taxed in terms of the amounts established by the local act and within the limits of 2500 rubles. if there are no documents. | Not credited |

| Directions | Actual costs are taken into account if documents are available | Not taxed if documented | Not credited |

| Additional services (service fees, use of bed linen | Are taken into account in full in other expenses | Not taxed | Not credited |

| Fee for using the airport VIP lounge | Taken into account as part of other expenses, if provided for in a local document | Taxable | Accrued |

| Taxi payment | Taken into account in other expenses if there is an economic justification and confirmation by documents | Is not a subject to a tax | Accrued |

| Medical insurance | Taken into account in other expenses when the presence of an insurance policy is a condition of entry | Is not a subject to a tax | Accrued |

| Consular and airport fees | Are taken into account in the amount of actual expenses | Not taxed | Not credited |

| Fees for the right of entry or transit of vehicles | Are taken into account in the amount of actual expenses | Not taxed | Accrued |

Main Differences

In the table we have collected the main differences between business trips in Russia and abroad.

| in Russia | abroad | |

| When going on a business trip, you must | issue an order or instruction specifying the timing, destination, and purpose of the trip; mark business trip days on the time sheet | |

| obtain a foreign passport and, if necessary, a visa | ||

| An advance is issued to the employee | in rubles | can be issued both in rubles and in foreign currency |

| The amount of daily allowance that is not subject to personal income tax | 700 rubles | 2500 rubles |

| Supporting documents | documents in a foreign language must have a line-by-line translation, which can be done by the employee himself | |

| Reimbursable expenses | employees are reimbursed for travel and rental expenses, additional expenses associated with living outside their permanent place of residence (daily allowance), as well as other expenses incurred by the employee with the permission of the head of the organization | |

| a) costs for obtaining a foreign passport, visa and other travel documents; b) mandatory consular and airfield fees; c) fees for the right of entry or transit of motor transport; d) expenses for obtaining compulsory medical insurance; e) other mandatory payments and fees | ||

| Employee status | does not change | when staying abroad of the Russian Federation for more than 183 days, the status changes to non-resident, from this moment personal income tax must be paid in the amount of 30% |

Stay up to date with the latest changes in accounting and taxation! Subscribe to Our news in Yandex Zen!

Subscribe