Can the date on the invoice differ from the date on the invoice?

According to Part 3 of Art.

168 of the Tax Code of the Russian Federation, When selling goods (work, services), transferring property rights, as well as upon receiving amounts of payment, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights, appropriate invoices are issued no later than five calendar days, counting from the day of shipment of goods (performance of work, provision of services), from the date of transfer of property rights or from the date of receipt of payment amounts, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights. The Department of Tax and Customs Tariff Policy has reviewed the letter on issues of issuing invoices for the sale of goods and reports. Clause 3 of Art. 168 of the Tax Code of the Russian Federation (hereinafter referred to as the Code) establishes that when selling goods, invoices are issued no later than five calendar days, counting from the day of shipment of goods. At the same time, when determining the date of shipment of goods for value added tax purposes, we recommend that you be guided by the following.

NTVP "Kedr - Consultant"

LLC "NTVP "Kedr - Consultant" » Services » Consultations on accounting and taxation » Other tax issues » About the correct deadlines for issuing a delivery note and invoice

The supplier issues a delivery note and invoice on the date of acceptance of the goods at the buyer's warehouse. Delivery was carried out by rail. Specific example: cargo was loaded for transportation on March 13, 2019, arrived at the destination station on March 26, 2019, the buyer accepted the goods on March 27, 2019. The supplier issues a delivery note and invoice on 03/27/2019. The contract contains a clause “Ownership of the goods passes to the Buyer at the time of transfer of the goods.

Question

Isn’t it a mistake that the supplier issued the documents on March 27, 2019, and not on March 13, 2019?

Expert's answer

The primary accounting document must be drawn up when a fact of economic life is committed, and if this is not possible, immediately after its completion. The person responsible for registration of the fact of economic life ensures the timely transfer of primary accounting documents for registration of the data contained in them in the accounting registers, as well as the reliability of this data. The person entrusted with maintaining accounting records and the person with whom an agreement has been concluded for the provision of accounting services are not responsible for the compliance of primary accounting documents compiled by other persons with accomplished facts of economic life.

(as amended by Federal Law dated December 21, 2013 N 357-FZ)

Art. 9, Federal Law of December 6, 2011 N 402-FZ (as amended on November 28, 2018) “On Accounting” {ConsultantPlus}

The dates of the invoice and the delivery note for which it is drawn up may not coincide, since they have different deadlines for preparation.

Thus, the delivery note is drawn up on the date of delivery of goods (Part 3 of Article 9 of the Accounting Law).

The period for issuing an invoice is five calendar days from the date of shipment (clause 3 of article 168 of the Tax Code of the Russian Federation). Thus, the invoice can be drawn up either on the same day as the delivery note or later. For example, the Alpha organization supplied chairs to the buyer according to delivery note No. 1250 dated 03/01/2019. The seller issued invoice No. 1311 and presented it to the buyer on 03/06/2019.

{Ready solution: Can the date of the invoice differ from the date of the delivery note (ConsultantPlus, 2019) {ConsultantPlus}}

Question: According to the contract, the buyer receives ownership of the consignment of goods after full payment. Shipment completed before payment. From what date should the period for issuing an invoice to the buyer of goods be counted?

Answer: In this case, you should follow the general rule - issue an invoice within five days from the date of shipment of the goods. The terms of the contract regarding the ownership of the goods do not affect the timing of the invoice.

Rationale: An invoice must be issued within five days from the date of one of the first (in terms of time of implementation) operations: shipment of goods or receipt of an advance payment.

If, when selling goods, the earliest of the dates established by clause 1 of Art. 167 of the Tax Code of the Russian Federation for the purpose of determining the tax base, is the date of shipment of goods; the seller’s obligation to calculate VAT arises on the date of shipment of goods, regardless of the moment of transfer of ownership established by the agreement (Letter of the Ministry of Finance of Russia dated August 28, 2017 N 03-07-11/55118 ).

Thus, the deadline for issuing an invoice in this case is five calendar days from the date of shipment (issue of the delivery note).

{Question: According to the contract, the buyer receives ownership of the consignment of goods after full payment. Shipment completed before payment. From what date should the period for issuing an invoice to the buyer of goods be counted? (“VAT: problems and solutions”, 2021, N 6) {ConsultantPlus}}

The first paragraph of paragraph 3 of Article 168 of the Tax Code of the Russian Federation (hereinafter referred to as the Code) establishes that when selling goods (work, services), invoices are issued no later than five calendar days, counting from the day of shipment of goods (performance of work, provision of services). In this case, in accordance with subparagraph 1 of paragraph 5 of Article 169 of the Code, the invoice must indicate the serial number and date of issue of the invoice.

According to the first paragraph of paragraph 2 of Article 169 of the Code, invoices are the basis for accepting tax amounts presented to the buyer by the seller for deduction when the requirements established by paragraphs 5, 5.1 and 6 of this article are met.

At the same time, in accordance with paragraph two of paragraph 2 of Article 169 of the Code, errors in invoices that do not prevent the tax authorities from identifying the seller, buyer of goods (work, services), property rights, name of goods (work, services) during a tax audit, property rights, their value, as well as the tax rate and the amount of tax presented to the buyer, are not grounds for refusing to accept tax amounts for deduction.

Taking into account the above, invoices issued by the seller of goods after the period established by the first paragraph of paragraph 3 of Article 168 of the Code are not grounds for refusal to accept the deduction of value added tax amounts by the buyer.

{Question: ...About VAT deduction based on an invoice issued by a supplier after the due date. (Letter of the Ministry of Finance of Russia dated March 14, 2019 N 03-07-11/16556) {ConsultantPlus}}

From the above it follows that a delivery note is issued at the time of shipment of goods, an invoice is issued within 5 calendar days after shipment of the goods or after drawing up a delivery note. Invoices issued by the seller of goods after the period established by the first paragraph of paragraph 3 of Article 168 of the Code are not grounds for refusal to accept for deduction amounts of value added tax by the buyer.

The explanation was given by the accountant-consultant of LLC NTVP "Kedr-Consultant" Natalya Borisovna Petrova in March 2021.

When preparing the answer, SPS ConsultantPlus was used.

This clarification is not official and does not entail legal consequences; it is provided in accordance with the Regulations of the CONSULTATION LINE ().

This consultation has passed quality control:

Reviewer - Bushmeleva Galina Vladimirovna, professor of the Department of Accounting and ACD, Izhevsk State Technical University named after. M.T. Kalashnikov

Providing character: what date to issue the act and invoice

In turn, tax accounting is carried out on the basis of data from primary documents, grouped in accordance with the procedure provided for by the Tax Code of the Russian Federation (Article 313 of the Tax Code of the Russian Federation). The basic rule for taking into account certain costs is set out in paragraph 1 of Art. 252 of the Tax Code of the Russian Federation: expenses must be economically justified, documented and aimed at generating income. In this case, documented expenses mean expenses confirmed by documents drawn up in accordance with the legislation of the Russian Federation.

According to clause 3.11 of GOST R 6.30-2003, adopted and put into effect by Resolution of the State Committee of the Russian Federation for Standardization and Metrology dated March 3, 2003 No. 65-st, the date of the act of provision of services is the date of the event recorded in the document. In this case, acts, as documents issued by two or more organizations, must have one (single) date.

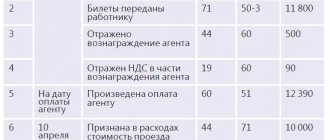

Abstract for one topic: ESChF

The procedure for applying for ESChF, as well as cases when ESChF |*| is not created, provided for in Art. 131 of the Tax Code of the Republic of Belarus (hereinafter referred to as the Tax Code). In particular, the ESHF is not created based on turnover from the sale of goods (work, services), property rights, which are not recognized as an object of VAT taxation in accordance with the law and are not subject to reflection in the VAT return (subclause 3.8, clause 3, article 131 of the Tax Code).

In the new edition of the Tax Code, even old norms are new, because they are set out in new articles of the code. How to correctly determine the period in which the right to deduct VAT begins? In the material provided, the author explains how to deal with this issue.

Date of invoice and work completion certificate

Registration of an invoice is not provided for by current regulatory legal acts. An invoice for payment for goods (work, services) does not belong to documents for which a unified form is provided; it does not have the nature of a primary document. As a rule, the invoice is drawn up on the organization’s letterhead indicating the details of the supplier (contractor), and the buyer, based on the invoice, makes payment .

Please tell me if, under the terms of the contract, payment is made on the basis of an invoice and a certificate of completion of work, the date entered in the documents should be the same or it is allowed for the invoice to be earlier than the certificate of completion of work and how many days it can be issued earlier.

Different dates in the Act and invoice

Since the period for issuing invoices is determined in calendar days, the taxpayer should remember the rule: if the last day of the period falls on a weekend or holiday, then the invoice must be issued on the last working day preceding the weekend.

Secondly, the deadline for issuing “advance” invoices is fixed by law. If before 01/01/2009 Ch. 21 of the Tax Code of the Russian Federation provided only for the terms for issuing invoices for the sale of goods (works, services), but now “advance” invoices also have their own terms for issuing.

We recommend reading: Demolition of Khrushchev buildings in St. Petersburg

About the date of preparation and date of issue of the invoice

5. When selling goods (work, services) by taxpayers exempted in accordance with Article 145 of this Code from fulfilling the duties of a taxpayer, invoices are drawn up

without allocating the corresponding tax amounts. In this case, the corresponding inscription or stamp “Without tax (VAT)” is made on these documents.

If we take the norms of the Tax Code of the Russian Federation more seriously, then hardly anyone will have any doubts that at the time of shipment a VAT tax base arises and, accordingly, an invoice should be drawn up for the same date. Other interpretations are fraught with tax disputes; moreover, the official position of the Ministry of Finance on this issue is on the side of budgetary interests, but not taxpayers:

Can an invoice come before a document?

The legislator determined the period within which the invoice must be issued - 5 calendar days from the date of shipment . Thus, a situation may arise in which the shipment occurred in one month (in the last days of the month), and the invoice was issued in another month, and the 5-day deadline was met.

In accordance with paragraph 2 of Art. 169 of the Tax Code of the Russian Federation, invoices are the basis for accepting tax amounts presented to the buyer by the seller for deduction when the requirements established by paragraphs are met. 5, 5.1 and 6 of this article of the Code. At the same time, paragraph 5 of Art. 169 of the Tax Code of the Russian Federation provides for an indication in the invoice, including the serial number and the date of its preparation.

The invoice was issued later than 5 days from the date of sale: what are the consequences?

According to the official position of the Ministry of Finance of the Russian Federation, set out in letters dated November 9, 2021 No. 03-07-09/39, dated February 17, 2021 No. 03-07-08/44, dated July 2, 2021 No. 03-07-09/20, account an invoice issued before the preparation of primary documents confirming the shipment of goods is considered to be drawn up in violation of the deadline provided for in clause 3 of Art. 168 of the Code. VAT cannot be deducted on the basis of such an invoice.

At the same time, for the purposes of applying value added tax, the date of shipment of goods is recognized as the date of the first drawing up of the primary document issued in the name of the buyer or carrier for the delivery of goods to the buyer (letter of the Ministry of Finance of the Russian Federation dated July 28, 2021 No. 03-07-09/23, dated November 1 .2021 No. 03-07-11/473).

We process financial transactions correctly: are the invoice and the certificate of completion interchangeable?

An invoice is a document drawn up on a special form indicating all the data of the buyer and seller, which displays the cost of goods, services or work, including construction, indicating the quantity and currency in which the transaction is executed. Already on the basis of the received invoice, accounting is carried out with the acceptance of input VAT for deduction.

Arguments that enable the performing company to issue an invoice for the provision of work before the fact of presentation and in the absence of prepayment (advance payment) are considered to be those that the supplier companies do not have any fundamental values for the timing of presentation of such documentation.

The deadline for issuing an adjustment invoice is 2021 if the price changes

The summary document contains information about the forwarder as a seller, and services purchased from a third party must be reflected in separate items. Information for this should be taken from the performer’s account.

Modern tools allow us to quickly find the necessary information, including filling out an adjustment invoice. However, it is important to understand that no matter how you formulate the request, the computer will produce many answers that will be difficult to navigate.

13 Jan 2021 lawurist7 117

Share this post

- Related Posts

- Alimony amount in 2021

- Where to Meet a Man for a Serious Relationship After 40 in St. Petersburg

- Article 228 with part 2 and 3 amendments for 2021

- What time do people in Kazakhstan retire?

Accounting and legal services

For the purposes of this chapter, the moment of determining the tax base, unless otherwise provided by paragraphs 3, 7 - 11, 13 - 15 of this article, is the earliest of the following dates 2) the day of payment, partial payment for upcoming deliveries of goods (performance of work, provision of services ), transfer of property rights. The period of incapacity for work is indicated by the doctor when issuing a sick leave certificate, but so as not to doubt the authenticity. N 24-1113100 to a very clearly formulated question, a reference is given to a letter from the Ministry of Taxes and Taxes of Russia dated What is the procedure for making corrections in the records of the executing organization in connection with the identification of facts of failure to draw up an act and failure to issue an invoice? What dates should be indicated on the report and invoice currently being processed for services provided in April? The performing organization should draw up an act of services rendered at the moment of discovering the fact of its erroneous non-execution and issue an invoice to the customer within five days from the date of execution of the act.

When you work with large state employees, you can’t slip them anything, and you can’t always replace documents. If you do not need an invoice for the advance payment, then yes, the date of payment. When drawing up invoices by merchants, you can come across different versions of them. Regarding services, I can’t understand how the payment plan (not for an advance payment) could have been issued earlier than the certificate of completion of work - apparently it was an error.

Seller invoice due date in 2021

In this case, as a general rule, an invoice is issued for each event separately, but it is also possible to draw up one document for all shipments made to one buyer during the day (letter of the Ministry of Finance of Russia dated May 2, 2021 No. 03-07-09/44). If the shipment is continuous (energy resources, rent), then the invoice, as well as the shipping document, can be issued once per month or quarter (letter of the Ministry of Finance of Russia dated September 13, 2021 No. 03-07-11/65642, dated 06.25.2021 No. 07-05-06/142 and dated 02.17.2021 No. 03-07-11/41).

The main question that arises in connection with the period allotted for issuing an invoice is the question of whether this period corresponds to the date indicated in the document. You usually have to choose from two options:

Invoice and act with different dates

This means that one invoice can indicate several operations: shipment of goods, performance of work, and provision of services, provided that the seller of the goods and the performer of services (works) are the same person, respectively, the buyer of the goods and the customer of services (works) are also one and the same person.

At the same time, in accordance with paragraph. 2 p. 2 art. 169 of the Tax Code of the Russian Federation, invoices that allow the tax authority to identify the seller, buyer, name and cost of goods, as well as the rate and amount of tax, cannot serve as a basis for refusing a deduction. Thus, if the information contained in the invoice is sufficient for identification, then to receive a deduction it does not matter when the invoice was issued - within 5 days from the date of shipment or before shipment.

We recommend reading: How long does it take to get a pension?

Invoice from January 1, 2021: form and sample filling

The invoice from January 1, 2021 continues to be filled out in accordance with the requirements of Government Decree dated December 26, 2011 No. 1137 as amended. from 02/01/2018. Without a correctly executed invoice, it is impossible to justify the right to reflect in accounting the fact of accepting VAT amounts for deduction. The invoice template has not changed since 2020, but when filling out the document you will need to indicate the updated tax rate due to the increase in the tax rate to 20% (the rate before 01/01/2020 was 18%). The deadline for issuing invoices in 2021 remained the same - 5 days (clause 3 of Article 168 of the Tax Code of the Russian Federation), counted from the moment:

This is interesting: Is it possible to buy a home for a Maternal Certificate with a Bad Key

The increase in the VAT rate affected only the basic tariff - instead of 18%, a 20% rate will begin to apply from 2021. When issuing an invoice, its value must be written down in the document so that it is clear at what rate the tax is charged and in what amount. Starting from 2021, an invoice reflecting the new tax rate must be issued for transactions that were completed after 01/01/2020. If the shipment (work, provision of services) was made before the end of 2021, the invoice will show a rate equal to 18% (Clause 4, Article 5 of Law No. 303-FZ dated August 3, 2018).

If the invoice is issued next month

Therefore, if in the situation under consideration, less than 5 days have passed between the date of issuing the act of services provided and the date of issuing the invoice, for example, the act was signed on November 30, 2012, and the invoice was issued on December 3, 2012, there are no violations. It does not matter that the date of the act of services rendered and the date of the invoice fall in different months. In this case, VAT on such an invoice should be deducted in December 2012 (Article 171 and Article 172 of the Tax Code of the Russian Federation).

In this regard, invoices for services rendered are issued by the seller no later than five calendar days, counting from the date of drawing up the act of services rendered (note that in letter dated 02/17/2011 N 03-07-08/44, the Ministry of Finance of Russia draws the attention of taxpayers that An invoice issued before the preparation of primary documents confirming the shipment of goods (work, services) cannot be used as a basis for deducting VAT amounts.

One invoice for several contracts

It happens that under an agreement or several agreements, the seller of goods and the performer of the service provided to the buyer, for example, delivery of products or installation of equipment, are one legal entity. In this case, the seller has the right to issue a consolidated invoice for the shipment of goods, services provided and work performed. When filling out a consolidated invoice, the seller indicates the product and service in one consolidated invoice on different lines, combining their costs into one total amount.

3. Advance invoice for several payments under one agreement per day

Once in the accounting department, the consolidated invoice, just like a regular invoice, is reflected in the purchase book and in an accounting program such as 1C. A consolidated invoice from a commission agent is no exception. If such a document exists, the accountant must perform such an operation as registering an invoice from the commission agent in the purchase book, then posting it in the 1C program to then generate a general report in electronic form. For an accountant, this procedure will not present any difficulties, just like reflecting the deduction in column 15 of the purchase book according to the consolidated advance invoice and entering it in 1C. When checking, tax authorities can request not only the invoices indicated in the purchase book, but also the originals of the primary documentation for the transaction, signed by the parties: invoices and acts that confirm the fact of delivery of products or provision of services. In this case, the names of goods or services in the consolidated invoice and in the primary documentation must coincide positionally.

Based on clause 3 of Art. 168 of the Tax Code of the Russian Federation, when selling goods (work, services), the corresponding invoices are issued no later than five calendar days, counting from the day of shipment of the goods (performance of work, provision of services).

Cancellation of acts and invoices, is this possible?

The lines of the invoice indicate: in line 1 - the serial number and date of the invoice used in calculations of value added tax; in line 1a - the serial number of the correction made to the invoice and the date of this correction. When drawing up an invoice before making corrections to it, a dash is placed in this line (paragraphs a, b, paragraph 1 of the Decree of the Government of the Russian Federation of December 26, 2011 N 1137 “On the forms and rules for filling out (maintaining) documents used in calculations of tax on added value" (hereinafter Resolution No. 1137)).

Thus, the legislation does not provide for the replacement of a primary accounting document previously accepted for accounting with a new document in the event of errors being detected in the primary accounting document. The date in the act can be corrected by making corrections certified by the date and signatures of the persons who compiled this document.

How do I register a late invoice?

The supplier issued the invoice late, in particular, after the end of the tax period to which the transaction related. How can an intermediary record this document in the journal of received and issued invoices?

The Ministry of Finance responded to the question in a letter dated April 26, 2018 No. 03-07-09/28450. Based on the provisions of the instructions from Resolution No. 1137 , officials came to the conclusion: if in the current period it is discovered that there is no entry in the journal about an invoice that was received in the past period, then such an entry must be made in a new line of the journal for that period in in which the document was drawn up. The rule applies to both the original and adjustment invoices.

Invoice, invoice and certificate of completion of work

In current business practice, the package of documents accompanying the transaction includes an invoice, an invoice and a certificate of completion of work. The accounting department files this set of papers after the work has been accepted by the customer and the necessary accounting operations have been completed.

The date in the work completion certificate is an important element that affects the reliability of the formation of information in accounting. On this date, the customer’s accounting recognizes expenses in the amount of the cost of work performed, agreed upon by the parties. In the contractor's accounting on the same date, revenue from the implementation of work is reflected and expenses associated with the fulfillment of obligations under the contract are recognized.

When is an invoice issued?

The seller must issue an electronic invoice in the approved format (approved by Order of the Federal Tax Service of Russia dated March 24, 2020 N ММВ-7-15 / [email protected] ), sign it with an enhanced qualified electronic signature of the head of the organization and send it to the buyer via telecommunication channels ( clause 2.4 of the Procedure and receipt of invoices in electronic form, approved by Order of the Ministry of Finance of Russia dated November 10, 2020 N 174n, hereinafter referred to as the Procedure). In response, the electronic document management operator will have to send confirmation that the file has been received. Then the invoice will be considered issued (clause 1.10 of the Procedure).

The seller must also issue an electronic invoice within 5 days after shipment of goods (performance of work, provision of services) or receipt of an advance payment. Of course, provided that the seller and buyer have an agreement to use electronic invoices.

Invoice from January 1, 2021

If necessary, additional details can be entered into this form (letter of the Federal Tax Service dated July 18, 2012 No. ED-4-3/11915). That is, include new lines or columns. Place them after the signatures of the manager and chief accountant or before the tabular part of the invoice. And if you need to add to the table, do not insert your columns in the middle. Add them to the right or left of the table section. The main thing is not to disrupt the existing sequence of columns (letters from the Ministry of Finance dated November 24, 2015 No. 03-07-09/68169, Federal Tax Service dated August 17, 2016 No. SD-4-3/15094).

Current legislation does not prohibit issuing one invoice for several acts of work performed and even for different contracts (letter of the Ministry of Finance dated November 10, 2015 No. 03-07-09/64493). However, the invoice must be issued within five calendar days after the completion of the work (rendering of services). This is the requirement of paragraph 3 of Article 168 of the Tax Code of the Russian Federation. Therefore, the invoice can only include the cost of those works that were completed no earlier than five calendar days before the invoice is issued. That is, certificates of work performed (services rendered) under all contracts must be signed either on the same day or on different days, but within five days.