In what cases is it prescribed?

This document applies only in cases where the releasing and receiving units are actually located at a significant territorial distance from each other. Otherwise, it is recommended to use other forms of documents that also reflect the movement of inventory items.

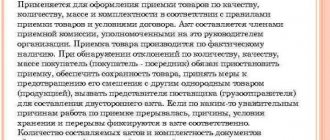

an invoice for the release of materials to the third party in the case when there is no sale of goods and materials when moving goods (for these purposes, a TORG-12 invoice is usually used). This operation can take place either within one organization or between two different enterprises by prior agreement. Such movements of inventory items include their transfer for safekeeping or transfer of customer-supplied raw materials.

When transferring goods and other inventory items for safekeeping

Material assets transferred without transfer of ownership rights to them, but with the obligation of the recipient to ensure their safety, are considered property under safekeeping.

The transfer of goods and materials for safekeeping is accompanied by the execution of a storage agreement and an invoice.

At the end of the storage period, material assets are returned . A similar document is issued for a return, only now the recipient is the sender.

For customer-supplied raw materials

Provided raw materials are materials that are received from the customer for processing or manufacturing of products.

In this case, goods and materials are accepted without payment of their cost and the performing organization is obliged to return them in processed form to the customer in full (paragraph 2, clause 156 of the Methodological Guidelines for Accounting for Inventories).

How to correctly fill out the M-15 consignment note ↑

The preparation of any document involves the implementation of certain rules. This also applies to filling out the invoice on form M-15.

The form must display information regarding material assets, in particular:

- Name;

- brand;

- nomenclature number;

- quantity;

- price;

- inventory number, etc.

When preparing invoices, continuous numbering is used. Moreover, starting from the new reporting year, it usually starts from the number 1. The signatures of the responsible persons are required at the bottom of the form.

There is often controversy over the need to print on the M-15. Will a document be valid without a seal? The standard form does not contain any space to print.

The list of mandatory details that primary documentation must have does not include printing. Thus, even without printing, the M-15 invoice is valid. The main thing is to fill out the form correctly and indicate all the required details.

In what cases is it prescribed?

The general purpose regarding the options for using the M-15 form sounds like the release of goods to the outside. However, there is no precise definition of what should be understood by the word “vacation”.

Most often, the M-15 form for drawing up an invoice is used in situations such as:

| Transfer of values to structural divisions of the organization | To use them in production activities, in case of remoteness of branches from the main enterprise |

| Transfer of goods or materials for safekeeping | To divisions or third-party organizations without transfer of ownership |

| Release of customer-supplied raw materials | For processing by other organizations |

In some cases, the M-15 consignment note can be used when selling goods to third-party companies. There is no legal prohibition of such use.

How to fill out the demand-invoice form according to the M-11 form, see the article: demand-invoice M-11. Read about electronic invoices in 1C here.

But the opinion of tax authorities often boils down to the fact that the concept of “vacation” does not mean “sale” at all. Therefore, if an organization decides to use an invoice in form M-15 when selling, then it may have to defend its opinion in court.

For outsourcing of materials

Filling out the M-15 invoice when distributing materials externally begins with indicating the basic details. The serial number of the document, the name of the organization, and the OKPO code must be indicated.

The small first plate indicates the date of issue of inventory items. If the organization uses a coding system, then the code corresponding to the operation being performed is indicated.

It also states which department is responsible for the supply. In the “Base” field, you must indicate the name of the document that serves as the basis for filling out the M-15 invoice.

Usually this is an administrative document drawn up by the manager (order). The “To” column is filled in with the name of the recipient of the valuables.

In the line “Through whom” the position and full name are written. the responsible person who accepts materials from the sender.

Next, you must fill out a table that contains a list of materials sold and a brief description of them. For accounting purposes, a corresponding account is indicated where the receipt of materials will be recorded.

For example, when releasing materials from warehouse to production, you need to indicate account 20 “Main production”. Then the names of the materials, their characteristics, nomenclature numbers, quantitative and price indicators are listed.

After filling out, the total number of items of goods and materials and the totality of their costs are written under the table.

The completed document is certified by the responsible persons. Since there are two copies, both of them must be identical.

For safekeeping

Consignment note M-15 can be used when transferring materials for safekeeping.

In this case, the document must contain information about the parties involved, the reasons for the transfer and the directly transferred objects. How justified is the use of the M-15 form in such a case?

According to the provisions of clause 1 of Article 886 of the Civil Code of the Russian Federation, under a storage agreement, the immediate custodian undertakes the obligation to preserve the thing transferred to him by the bailor and return it in its original form.

Clause 1 of Article 887, clause 1 of clause 1 of Article 161 of the Civil Code states that a storage agreement between legal entities is concluded in writing.

According to clause 2 of Article 887 of the Civil Code, the standard written form is considered to be complied with when the custodian’s acceptance of the thing from the bailor is confirmed by a receipt, safekeeping receipt or other document on which the custodian’s signature is present.

It follows from this that the transfer of materials for safekeeping can be carried out using form M-15.

The basis for drawing up the invoice in this case is the storage agreement. Otherwise, fill out the form according to the standard procedure.

As for accounting, the regulations do not establish which documents must be used when transferring property for storage to another organization on the basis of an agreement.

The composition and form of documents is determined by the official responsible for accounting (Part 4, Article 9 of Federal Law No. 402).

The main requirement is the presence of mandatory details in the primary document, the list of which is given in Part 2 of Article 9 of Federal Law No. 402.

For customer-supplied raw materials

Consignment note M-15 is used when transferring finished products to the seller. In this case, certain nuances must be taken into account.

So, if products are transported from the warehouse of a processing organization to the warehouse of the supplier organization by means of vehicles, then a consignment note must be issued in the unified form 1-T.

When products are shipped from the processor's warehouse to the supplier's warehouse directly, Form 1-T can be replaced by waybill M-15.

Special clearance is provided when goods are shipped by the processor to third-party warehouses. In this situation, two documents are drawn up:

| Form 1-T as a waybill | Which certifies the interaction between the processor and the recipient of the cargo. In this case, the consignor and consignee are indicated. The provider organization is indicated as the supplier |

| Form M-15 as an invoice for the release of materials to the third party | Confirming the movement of materials between the processor and the supplier |

It is necessary to clarify that shipment to third parties (buyers of the supplier) must be documented - in the terms of the contract between the supplier and the processor or in an additional agreement to this agreement or in a letter from the supplier.

Other cases

In addition to the listed cases, the M-15 consignment note is applicable in any cases of movement of materials within an organization or between its structural divisions.

You can use this form to transfer property to the authorized capital of another organization. In this case, there is no sale of property as such.

Video: why does a forwarder need TTN?

That is, we are talking only about the transfer of valuables for temporary use without payment. And yet, the M-15 invoice is often used when registering the sale of material assets.

How acceptable is this and does the purchasing organization have the right to accept the property for accounting on the basis of Form M-15?

The legality and appropriateness of use should be considered from the perspective of:

- Inspectorate of the Federal Tax Service;

- taxpayer;

- judicial authorities.

According to the Federal Tax Service, one should be guided by Resolution of the State Statistics Committee of the Russian Federation No. 132 of December 25, 1998.

It says that the sale of commodity and material assets to a third party must be issued with an invoice in the TORG-12 form. Therefore, this form cannot be replaced with another form.

From the taxpayer’s point of view, the M-15 invoice allows one to reliably determine the fact of delivery of valuables, their quantity, cost and the amount of VAT.

That is, form M-15 may well be used as a primary document when capitalizing purchased inventory items. Clause 2 of Article 9 of the Law “On Accounting” is cited as justification for this position.

It lists the basic requirements for the consignment note, which the M-15 fully meets, in particular the presence of:

- title of the document;

- dates of its creation;

- the name of the organization that compiled the document;

- contents of the business operation;

- measuring business operations in physical and monetary terms;

- names of positions of responsible persons;

- personal signatures of responsible employees.

From the court's perspective, the M-15 form cannot accurately reflect the trade transaction between the recipient and the supplier. It simply does not provide some necessary details.

For example, information about the seller and buyer (addresses, bank details, telephone numbers), information about the consignee and consignor indicating addresses, details and contact information.

That is why the M-15 form cannot replace the TORG-12 form. This is the court decision given in the Resolution of the FAS SZO No. A05-9970/2008 dated March 26, 2009.

Sample filling

Filling out form M-15 looks like this:

- Filling out the table. The date of preparation of the invoice, the sender, the transaction type code, and the recipient responsible for the supply of goods and materials are indicated.

- The “Base” is filled in indicating the type of document. The recipient's name and full name are also written down. the direct recipient and details of the power of attorney provided by him.

- Name of goods and materials and main characteristics (size, grade, brand, etc.).

- Number according to the nomenclature list.

- Code of measuring units according to OKEI.

- Name of units of measurement.

- Quantity of shipped materials to be shipped.

- The number of valuables actually released.

- The price of one unit of goods and materials excluding VAT (in rubles and kopecks).

- Total cost of issued inventory items excluding VAT

- Total VAT amount.

- The cost of all goods including VAT (column 10 + column 11).

- Inventory number.

- Passport number of goods and materials (for shipment of precious metals).

- Entry number in the special card for materials accounting.

Upon completion of filling, the number of items of value issued, the total amount of the invoice and VAT included in the total amount are indicated at the bottom of the form.

Then the document is signed by the responsible persons. At this point, the invoice is considered finalized.

In what form is it formatted?

The release of inventory items to a third party can be formalized by a document developed within the organization, or the enterprise can use the unified form M-15.

If an enterprise uses its own form, then the form must be approved by order and contain the required details :

- document's name;

- its serial number and date of compilation;

- name of the issuing and receiving party;

- basis for release of inventory items;

- data on material assets: name, unit of measurement, quantity, price and cost;

- information about the responsible persons who released and accepted the goods.

For the convenience of warehouse accounting, it is recommended to provide columns in the invoice form containing more detailed information about the goods being moved (item number, inventory number or warehouse card number).

It is more rational to use your own form within one organization ; you can add columns with internal accounting information or data not intended for third parties.

When moving material assets between different organizations, it is appropriate to use the unified form M-15, thus the third-party organization will not have claims against the releasing party regarding the documentation of the operation.

If a carrier organization is involved in the movement of material assets, it is recommended to issue an invoice in the form 0504205 according to OKUD. It indicates not only the data of the issuing organization and the organization receiving the goods and materials, but also the data of the carrier.

FAQ

Despite the fact that filling out the M-15 form does not cause any particular difficulties, thanks to the intuitive form, certain questions arise when using the document.

For example, how to prepare closing documents when conducting operations using the M-15 consignment note. What documents are needed for the operation to be considered completed.

Some disputes arise regarding the display of accounting accounts in the invoice. Is it necessary to indicate the accounts for which transactions will subsequently be made to reflect the transaction?

After all, materials are transferred, but they are listed in the organization’s records and it is necessary to somehow reflect the transfer of goods and materials.

What closing documents are needed for it?

Final documents are those that certify the completion of the transaction on the part of both parties involved in terms of the execution of the main subject of the contract.

In order for a transaction to be considered not only paid, but also legally completed, there must be written confirmation.

Invoice M-15 is drawn up on the basis of an agreement for the transfer of goods and materials, a storage agreement, an order from the manager to transfer materials to production and similar documents.

That is, the invoice closes these documents, confirming their execution, and is confirmation of acceptance of the goods.

It is on the basis of the invoice value that the value is written off in the accounting of the issuing value of the organization and accepted for accounting by the recipient of the value.

That is, the invoice itself is a closing document. It is important to know that only original documents have legal force.

If, due to certain circumstances, a copy of the invoice was provided at an intermediate stage of the transaction, then the original must still be present in the accounting registers.

The absence of final documents may be grounds for recognizing the transaction as not complete and not closed.

The consequence may be additional tax assessment, since the accountant does not have the right to include undocumented expenses in the declaration.

Is an invoice required?

Is it necessary to indicate an accounting account on the M-15 invoice? Specifying an account allows you to determine with which account the inventory account will correspond based on a specific invoice. The accountant indicates the required account.

If, according to the document flow rules adopted by the organization, the invoice is drawn up by another person (storekeeper or employee responsible for storing valuables), then the accountant fills out columns 1 and 1 of the main table M-15 before certifying the document:

Based on all of the above, when moving materials within an organization, including transfer to third-party organizations with subsequent return, you can use the M-15 consignment note.

In case of sale, in order to avoid claims from the tax inspectorate, it is more advisable to use the TORG-12 form.

When using M-15, you should pay special attention to the document serving as the basis and compliance with the rules for document execution.

The movement of material assets outside the territory of the enterprise (including in the case of their movement to other organizations) is taken into account in accounting. In case of such a movement, an authorized person draws up a primary document. Its name and form can be approved by the organization independently in compliance with the law. In addition, the official unified form of the primary document can be used - invoice M-15.

Filling rules

M-15

Form M-15 is filled out by employees of the organization or structural unit that issues goods and materials. This could be an accountant who issues and transfers the invoice to the warehouseman or the directly responsible warehouse employee. It is drawn up in two copies - one each for the releasing and receiving parties.

The invoice must contain the serial number and date of preparation, as well as the name of the organization that issued the document. The sending structural unit and the receiving structural unit are required. For ease of accounting, it is advisable to indicate the type of activity of these structural units (storage or production).

In the “Bases” column, details of documents authorizing the release of materials are written. This may be an order, an order for the release of materials, a work order or a power of attorney.

The tabular part of the M-15 form indicates information about the transferred material assets:

- name of the material indicating the brand, grade and size;

- its item number;

- unit of measurement;

- the quantity of goods and materials that must be issued according to the basis document, and the actual quantity of materials issued;

- price, amount, VAT amount and final amount of material assets including value added tax;

- additional information about the transferred materials - inventory number (if fixed assets are transferred for safekeeping).

Data on the quantity, amount and VAT of issued inventory items are summarized and indicated in words in separate columns.

Without data that allows one to sufficiently accurately identify the transferred goods and materials, their quantity and amount, and without data on the basis for such movement of materials, as well as without indicating the transferring and receiving parties, the invoice is invalid.

Below is the invoice form and an example of how to fill it out:

Forms 0504205 according to OKUD

The invoice in form 0504205 according to OKUD must also contain the number and date of registration . It indicates the name and tax identification number of the sender, recipient and organization transporting goods and materials.

In the “Bases” column, the details of the agreement between the sender and the recipient, the vacation order and the power of attorney to receive materials are indicated.

The tabular part of the document contains information about:

- material assets indicating the name, grade, brand and other necessary data;

- inventory number of goods and materials or passport number;

- unit of measurement and price;

- the amount of material assets that should be released and released in fact;

- cost of materials without VAT, the amount of VAT and cost of materials with tax.

Tabular data on quantity and cost are summarized, information on the total cost of materials including VAT is indicated in words in the corresponding column.

Form M-15. Invoice for issue of materials to the side

Despite complete freedom in developing an invoice, it is recommended to adhere to previously generally accepted standards, as well as take into account some norms and requirements of office work.

In particular, you should always indicate the name of the company that issues the invoice, information about the recipient, the date of its preparation, as well as the specific materials that are transferred under it and their cost. The document is filled out by the enterprise accountant and partly by the storekeeper. In addition, the invoice must be signed by the responsible employees of the organization and the recipient.

There is no need to put a seal with the company details on the document - as of 2021, legal entities have acquired the right not to use stamps and seals in their work. The invoice must be written out in two copies, one of which should be transferred to the warehouse of the company dispensing the materials, and the second should be given to the recipient.

We recommend reading: Tax refund on drugs

In the first part of the document, you must enter the invoice number in accordance with the internal document flow.

Signing the document

Form M-15 is signed by the person who authorized the release of material assets (for example, director, chief engineer, deputy for production or head of a structural unit). In addition, the invoice must be signed by the organization’s chief accountant and the financially responsible person.

The invoice in form 0504205 according to OKUD is certified by the responsible executor - this is, as a rule, the accountant of the material desk who issued the document. When releasing material assets, the invoice is endorsed by the materially responsible person shipping the materials.

Signatures of the manager and chief accountant are not provided here , because the release of material assets to third parties is carried out on the basis of an agreement concluded between two organizations and a power of attorney to receive goods and materials.

From the receiving side, the invoice is endorsed either by the storekeeper, who accepts the materials into his warehouse, or by the head of the production workshop, who will transfer the received materials to production.

All signatures must necessarily contain the name of the position of the person signing the document and a transcript of his signature. Without at least one signature, this document is invalid and cannot be taken into account.

Purpose of such a document

The document represents itself as an invoice where materials are moved, both within the company and leaving the company:

- The most common is the movement of raw materials within a warehouse, for example to another warehouse;

- If the goods are transported to the buyer, then TORG-12 can be used;

In this case, the type of material, their type and material value does not matter:

- Product;

- Raw materials;

- Mechanisms;

- Constructions.

! ATTENTION

If you are asked to provide documents upon first request by the official who is checking the cargo, you must provide them.

Do I need to stamp it?

Forms of form M-15 and form 0504205 according to OKUD do not provide for stamping on them . Accordingly, these documents are valid even without a seal.

However, it is customary for business rules to certify the signatures of both parties when exchanging documents between two different enterprises. Organizations can record this point in an appendix to the custody agreement or to the toll agreement.

You can also affix stamps when moving materials between different structural divisions of the same organization, if this is provided for by an internal local document.

Primary accounting document for moving the MC to the side

The document in question was previously included in the list of mandatory primary documentation forms approved by Resolution of the State Statistics Committee of the Russian Federation dated October 30, 1997 N 71a. However, at present, the mandatory use of it has lost its relevance (Information of the Ministry of Finance No. PZ-10/2012).

Today, organizations have the right to independently determine whether to use a unified form of primary documentation or to develop and approve such a form independently.

Business entities have the opportunity to independently develop and apply primary documentation that complies with the law related to the transfer of MC to the outside (including the form in question).

The self-approved form must, in particular, contain:

- name and date;

- name of the business entity;

- content of the corresponding operation (fact);

- measurement value;

- names of positions and signatures of persons responsible for registration of the relevant operation (fact).

Let us dwell in more detail on the use of the unified form M-15.

How is the fact of inventory movement recorded in accounting documents?

The invoice for the issue of materials is recorded in the journal of warehouse documents of the issuing and receiving parties. At the end of the reporting period (week, decade, month), the financially responsible person transfers primary documents to the accounting department through the register.

The accountant, based on the business transaction that was issued with an invoice for the release of materials to the third party, makes entries and reflects it in accounting.

If a transfer for safekeeping has been formalized, the receiving organization reflects them on off-balance sheet account 002 “Materials accepted for safekeeping.”

The sending organization does not write off inventory items from its balance sheet, and reflects their movement only on the subaccounts of analytical accounting of account 10 “Materials”.

Similarly, the sender will reflect material assets when transferring customer-supplied raw materials, but the organization carrying out processing records them in off-balance sheet account 003 “Materials accepted for processing.”

When transferring material assets between geographically distant structural divisions of one organization, accounting entries will depend on the purpose of the transfer.

- If this is a movement between warehouses, then postings will only be between different subaccounts of account 10 “Materials”.

- When materials are transferred to production, they are written off from the credit of account 10 to the debit of account 20 “Main production”.

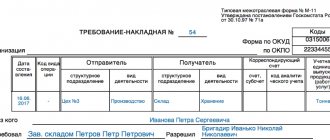

Instructions on how to fill out the invoice

The invoice for materials release consists of two parts.

The first part must be completed as follows:

| Invoice number | We put the number in the invoice, with our document flow; (For example: invoice No. 69) |

| Company name | You must provide the full name of the company; (For example: Stampgold LLC) |

| OKPO | Constituent documentation of the company; (For example:00866755) |

| date | When the invoice was drawn up; (For example:06.08.18) |

| Operation type code | If used, if not, put a dash; (For example: -) |

| Structural subdivision | The company issuing the document (for the sender and the recipient); (For example, for the sender: “Warehouse 2”, “Storage”; For the recipient: “Processing shop”, “production” |

| Kind of activity | |

| Delivery Responsible | Indicate without full name; (For example: “warehouse,storage,1234”); |

| To whom | Indicate who receives the material, full name. who exactly receives this product; (For example: “to: processing shop, Shop Manager Shorin.A.E); |

The second part includes a number of rules:

| Column | What does it include |

| 1 column | This column is filled in by the accountant, filling in: account, subaccount, accounting code; (For example: "15"); |

| 2nd column | |

| 3 column | The name of what is moving. (For example: corner, stamp;) |

| 4 column | We enter the number (code) that is assigned in the nomenclature; (eg:1233) |

| 5 column | Must enter the unit code according to the all-Russian measurement classification; (for example:123) |

| 6th column | You need to enter the specific name of the unit of measurement; (for example: ton); |

| 7 column | It is necessary to enter the exact amount of materials sold according to the invoice; (for example:0.66) |

| 8 column | It is necessary to enter the exact amount of materials that were released, this is filled in only by the storekeeper; (for example:0.66) |

| 9th column | We enter the total cost of the supplied material; (for example:3800.00) |

| 10th column | Enter the price excluding VAT; (for example:1320.00) |

| 11th column | We enter data on the amount of VAT; (for example:122.00) |

| 12th column | We pay the total amount, including VAT; (for example:1930.00) |

| 13th column | Enter the inventory number; (for example:13) |

| 14th column | This needs to be entered if suddenly there is a talk about the transfer of jewelry, if not, then put a dash; |

| 15th column | The serial number of the card in the warehouse is entered. (For example: 1289) |

Finally, the invoice must be signed only by the accountant and the storekeeper. It is not necessary to put a stamp, but if the recipient requires a stamp, then it is better to put it.

How long does it last?

Like all primary documents, the invoice for the release of materials to third parties must be stored in the organization for at least five reporting years , after which it can be destroyed. Storage is carried out, as a rule, by the accounting department of the enterprise. In large enterprises with a large volume of document flow, this function is assigned to a separate official.

It is important to know what other invoices there are. We suggest you read about the following types: for the release of goods, for the movement of inventory items within the enterprise, incoming and outgoing, outgoing and incoming, transport, TTN, return.

An invoice for the release of materials is issued for the movement of goods and materials within one organization, but between its geographically remote divisions, or between different organizations when transferring materials for storage or processing. An enterprise has the right to develop its own form or use standardized forms.

If you find an error, please select a piece of text and press Ctrl+Enter.

Use of customer-supplied materials.

Every year, the numbering of invoices starts from one. When filling out the form (outsourcing of goods and materials), in the first table you must indicate:

- Date of registration,

- Sender. You must indicate the name of the structural unit and the type of its activity,

- Code of the type of operation performed (if the organization uses a code system),

- Recipient. You must indicate the name of the department, its type of activity,

- Responsible for the supply of goods and materials. Contractor code, unit name, type of activity.

After this, the document that serves as the basis for issuing the invoice is indicated. In the “To” line, write the name of the recipient of the goods and materials (the business entity of its organization or a third-party organization). In addition, write down the full name of the recipient and details of the power of attorney provided by him. Column 3. Write the name of the goods and materials, their characteristics: brand, size, grade. Column 4. Nomenclature number (if not available, then put a dash). Column 5. The code of units of measurement according to OKEI is recorded. Column 6. The name of the units of measurement is indicated. Column 7. Write the amount of material required for shipment. Column 8. Filled out by the storekeeper, indicating the actual quantity of materials released. Column 9. The price of one unit of goods and materials in rubles and kopecks without VAT. Column 10. Price of issued inventory items without VAT. Column 11. Total VAT amount. Column 12. Total cost of goods including VAT. (in total columns 10 and 11). Column 13. The inventory number is recorded. Column 14. The passport number of goods and materials (precious metals) is recorded. Column 15. Entry number in a special materials accounting card.

Read more: Where to see the number of a higher education diploma

In the conclusion, indicate the number of items of goods and materials issued, the total amount of the invoice and additionally VAT, which is included in the total amount.

The invoice form is signed by: the responsible employee who authorized the release of goods and materials, the employee who released the goods and materials, the chief accountant and the recipient of goods and materials.

When are M-15 and TORG-12 used?

Form N M-15 “Invoice for the release of materials to the third party” <6> is used when releasing material assets:

(or) divisions of its organization located outside its territory;

(or) to third parties on the basis of contracts (including purchase and sale agreements).

As for the unified form N TORG-12 “Consignment note” <7>, it is used to register the sale (issue) of inventory items to third parties, that is, it is intended specifically for recording trade transactions.

It would seem that everything is simple. If an organization is engaged in trade, for example, in building materials, then it accounts for them precisely as goods and, when selling them, issues invoices in the form N TORG-12. If an organization is not engaged in trade, but it has a need to sell building materials that were accounted for in account 10 “Materials,” it can issue an invoice in Form N M-15.

<6> Approved by Resolution of the State Statistics Committee of Russia dated October 30, 1997 N 71a. <7> Approved by Resolution of the State Statistics Committee of Russia dated December 25, 1998 N 132.

What to write out when shipping materials externally: M-15 or Torg-12

There are two forms of invoices that document the transfer of inventories to third parties - NN M-15 and TORG-12. These forms differ slightly from each other, and, in principle, they are interchangeable. But sometimes accountants, when selling materials, begin to doubt which invoice to issue: in form N M-15 or in form N TORG-12. For example , when selling building materials left over after an office renovation. At first glance, it does not matter what document will be drawn up. However, there are heated discussions on this issue in accounting forums.