Let's create a balance sheet from accounts or turnover.

Balance sheet is the size of assets, capital, liabilities, accounts as of a certain date. (Or is a system for storing economic information for an enterprise)

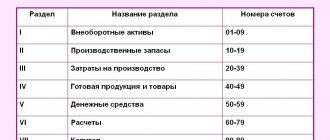

The balance consists of:

- ASSET: Section 1, Section 2.

- PASSIVE: Section 3, Section 4, Section 5.

Let's look at the main (popular) balance sheet items where the numbers come from. Two methods are OPTION 1 from the turnover (for the main accounts) and OPTION 2 (more detailed, more complex for most accounts with a detailed description)

Assets

The balance sheet asset consists of 2 sections:

-1. Fixed assets.

-2. Current assets.

SECTION 1 Non-current assets

Article 1110 “Intangible assets”

We take the balance on account 04 (Intangible assets) minus the balance on account 05. (Amortization of intangible assets)

Formula=04 count -05 count.

Article 1150 “Fixed assets”

We take the balance on account 01 “Fixed assets” and minus account 02 “Depreciation of intangible assets”

Formula=01 account-02 account

Article 1170 “Financial investments”

We take the balance of account 58 (financial investments in terms of long-term financial investments) + 55/DEPOSIT + 73/1 (loans issued to employees) - account 59 (reserve for impairment of financial assets in terms of long-term financial investments).

Formula=58+55/Deposit+73/1- 59 account

Article 1190 “Other non-current assets”

Formula =Dt balance on account 08+Debit balance on account 07+Debit balance on account 97 for more than 12 months. There is a letter from the Ministry of Finance saying that advance payments to suppliers for the purchase of fixed assets are reflected in the line “other non-current assets”, some kind of nonsense, but I will introduce this nuance to you.

Article 1100 “Result under Section 1”

We summarize all asset items in section 1 “Non-current assets”

Section 2 Current assets.

Article 1210 “Reserves”

Formula = Account balance 10 (materials) + Account balance 41 (goods) + Account balance 43 (finished products) + Account balance 15 + Account balance 16 + Account balance 45 (Goods shipped) + Account balance 20 (main production) + account balance 44 (sales expenses) + Account balance 97 (deferred expenses) + 21,23,28,29-Account balance 14

Article 1220 “VAT”

Formula = Debit balance on account 19 “Value added tax”

Article 1230 “Receivables”

Formula = Dt 46+Dt60/02+Dt62/01+Dt76+Dt68+Dt71+Dt73/damage compensation+Dt75/For contributions to the authorized capital.-Credit balance on account 63 (reserve for doubtful debts)

Comments: under account 60/02 (advances issued), VAT is calculated on the prepayment, as well as under account 76. In accordance with PBU, if account 60/02 is the amount of 10,000 rubles and 60/01 is 5,000 rubles, then we do not find the balance on account 60 and do not record one total balance in the balance sheet, PBU does not allow this, i.e. 60/02 will be in accounts receivable 10,000 rubles and 60/01 - there will be 5000 rubles in accounts payable in liabilities. (i.e. we do not offset accounts receivable and payable). (On account 60 there will be an expanded balance dt balance 10000 Kt balance 5000)

76 each if there are advances issued, 68 if there are receivables.

ATTENTION:

-If you have a balance on account 76/AB (VAT on advances and prepayments received), then it must be deducted from the Accounts Receivable line. (Section 2)

-There is a letter from the Ministry of Finance stating that 60-02 for prepayments issued to suppliers for the purchase of fixed assets does not need to be included in the “Accounts receivable” line, but in “other non-current assets”; you decide what to do.

Article 1240 “Financial investments”

Formula = Account debit balance 58 (financial investments in terms of short-term) + 55/deposits (special accounts in banks in terms of short-term) = 73/Loans issued to employees (in terms of short-term)

Article 1250 “Cash”

Formula = 50 balance account (cash) + 51 balance account (current account) + 55 account (except deposits) + 57 (transfers in transit).

Article 1260 “Other current assets”

Formula = Account balance 94+76/VAT (VAT accrued upon shipment of goods when ownership of the goods is transferred in a special manner after payment until the revenue is determined)

Article Result for section 2 current assets

Let's summarize all the articles in section 2

BALANCE (Balance currency is another

name )

sum up the total of section 1 + Total of section 2

Individual, consolidated and consolidated reporting

The forms of the above annual reporting and the procedure for their preparation are determined by the National Accounting and Reporting Standard “Individual Accounting Statements”, approved by Resolution of the Ministry of Finance of the Republic of Belarus dated December 12, 2016 No. 104 (hereinafter referred to as National Standard No. 104).

| Individual reporting (part one, clause 7, article 14 of Law No. 57-Z) | Consolidated reporting (part two, clause 7, article 14 of Law No. 57-Z) | Consolidated reporting (clause 8 of article 14 of Law No. 57-Z) | ||

Socially significant organizations (except for banks, joint-stock investment funds, management organizations of investment funds) are required to prepare annual consolidated statements

in accordance with IFRS in the official monetary unit of the Republic of Belarus (part one, paragraph 2, article 17 of Law No. 57-Z).

| For information Socially significant organizations - open joint-stock companies that are founders of unitary enterprises and (or) main business companies in relation to subsidiary business companies, banks and non-bank financial institutions, insurance organizations, joint-stock investment funds, management organizations of investment funds (paragraph 7 of Article 1 of Law No. 57-З). |

PASSIVE

The Balance Passage consists of the following sections:

- Capital

- long term duties

- Short-term liabilities

SECTION 3 CAPITAL

Article 1310 “Authorized capital”

Formula = Account credit balance 80 Authorized capital"

Article 1320 “Own shares”

Formula Debit balance for account 81. (item is reflected in brackets)

Article 1340 “Revaluation of non-current assets”

Formula - We take the balance on account 83 in terms of the revaluation of intangible assets and fixed assets.

Article 1350 “Additional capital”

Formula = Take the balance of account 83, except for the revaluation of fixed and intangible assets

Article 1360 “Reserve capital”

Formula = Take the balance of account 82 “Reserve capital” credit.

Article 1370 “Retained earnings (uncovered loss)”

Formula = Take the balance on the credit account 99 (profit and loss, if the balance on the debit then put a minus in front of the amount) + Take the balance on the account 84 (Retained earnings, if the balance on the debit then put a minus in front of the amount). If the amount turns out to be a minus (loss), then write the amount in parentheses. And when we calculate the total for section 3, we subtract this amount.

Article 1300 “Total for Section 3”

Formula = Authorized capital - Own shares + Revaluation of non-current assets, additional capital + Reserve capital + Retained earnings (if in parentheses with a minus, then subtract)

SECTION 4 Long-term liabilities

Article 1410 “Borrowed funds”

Formula = Credit balance on account 67 “Long-term loans and borrowings” (in terms of more than 12 months of repayment)

Article 1430 “Evaluated liabilities”

Formula = Credit balance of account 96 “Reserves for future expenses” (in terms of more than 12 months from the reporting date)

Article 1450 “Other obligations”

Formula = Account balance 86 (targeted financing in terms of long-term ones) + 60,62,68,69 (in terms of repayments over 12 months).

TOTAL for section 4

Let's summarize all the articles in section 4.

Balance sheet

Approved by Resolution of the Ministry of Finance dated October 31, 2011 N 111

BALANCE SHEET for _____________ 20__ ————————————————————————— ¦Organization ¦ ¦ +————— ————————+———————————+ ¦Payer’s account number ¦ ¦ +—————————————+———————— ———+ ¦Type of economic activity ¦ ¦ +—————————————+———————————+ ¦Organizational and legal form ¦ ¦ +————— ————————+———————————+ ¦Control body ¦ ¦ +—————————————+————————— ——+ ¦Unit of measurement ¦ ¦ +—————————————+———————————+ ¦Address ¦ ¦ ——————————— ——-+———————————- ————————————- ¦Approval date ¦ ¦ +——————+——————+ ¦ Date of dispatch ¦ ¦ +——————+——————+ ¦Date of acceptance ¦ ¦ ——————+—————— ————————————— ———————————— ¦ Assets ¦ Code ¦ On _______ ¦ On December 31 ¦ ¦ ¦ lines¦ 20__ ¦ 20__ ¦ +————————————-+ ——+————-+—————+ ¦ 1 ¦ 2 ¦ 3 ¦ 4 ¦ +————————————-+——+————-+—— ———+ ¦I. LONG-TERM ASSETS ¦ ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Fixed assets ¦ 110 ¦ ¦ ¦ +————— ———————-+——+————-+—————+ ¦Intangible assets ¦ 120 ¦ ¦ ¦ +————————————-+——+ ————-+—————+ ¦Income investments in material ¦ 130 ¦ ¦ ¦ ¦assets ¦ ¦ ¦ ¦ +————————————-+——+———— -+—————+ ¦Including: ¦ ¦ ¦ ¦ ¦investment real estate ¦ 131 ¦ ¦ ¦ +————————————-+——+————-+— ————+ ¦items of financial lease (leasing) ¦ 132 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦other income investments in ¦ 133 ¦ ¦ ¦ ¦material assets ¦ ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Investments in long-term assets ¦ 140 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Long-term financial investments ¦ 150 ¦ ¦ ¦ +—————— ——————-+——+————-+—————+ ¦ Deferred tax assets ¦ 160 ¦ ¦ ¦ +————————————-+——+ ————-+—————+ ¦Long-term receivables ¦ 170 ¦ ¦ ¦debt ¦ ¦ ¦ ¦ +————————————-+——+————-+ —————+ ¦Other long-term assets ¦ 180 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦TOTAL for section I ¦ 190 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦II. SHORT-TERM ASSETS ¦ ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Inventories ¦ 210 ¦ ¦ ¦ +—————— ——————-+——+————-+—————+ ¦Including: ¦ ¦ ¦ ¦ ¦materials ¦ 211 ¦ ¦ ¦ +—————————— ——-+——+————-+—————+ ¦animals for growing and fattening ¦ 212 ¦ ¦ ¦ +————————————-+——+—— ——-+—————+ ¦work in progress ¦ 213 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦finished products and goods ¦ 214 ¦ ¦ ¦ +———————————-+——+————-+—————+ ¦goods shipped ¦ 215 ¦ ¦ ¦ +——— —————————-+——+————-+—————+ ¦other stocks ¦ 216 ¦ ¦ ¦ +————————————-+— —+————-+—————+ ¦Long-term assets intended ¦ 220 ¦ ¦ ¦ ¦for sale ¦ ¦ ¦ ¦ +————————————-+——+— ———-+—————+ ¦Deferred expenses ¦ 230 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Value added tax on ¦ ¦ ¦ ¦ ¦ purchased goods, works, ¦ ¦ ¦ ¦ ¦ services ¦ 240 ¦ ¦ ¦ +————————————-+——+————- +—————+ ¦Short-term accounts receivable ¦ ¦ ¦ ¦ ¦debt ¦ ¦ ¦ ¦ +————————————-+——+————-+————— + ¦Short-term financial investments ¦ 260 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Cash and cash equivalents ¦ 270 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Other short-term assets ¦ 280 ¦ ¦ ¦ +————————— ———-+——+————-+—————+ ¦TOTAL for Section II ¦ 290 ¦ ¦ ¦ +————————————-+——+—— ——-+—————+ ¦BALANCE ¦ 300 ¦ ¦ ¦ —————————————+——+————-+————— ————— ———————————————————— ¦ Own capital and liabilities ¦ Code ¦ As of _______ ¦ As of December 31 ¦ ¦ ¦ lines¦ 20__ ¦ 20__ ¦ +——— —————————-+——+————-+—————+ ¦ 1 ¦ 2 ¦ 3 ¦ 4 ¦ +————————————-+ ——+————-+—————+ ¦III. OWN CAPITAL ¦ ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Authorized capital ¦ 410 ¦ ¦ ¦ +————— ———————-+——+————-+—————+ ¦Unpaid part of the authorized capital¦ 420 ¦ ¦ ¦ +————————————-+— —+————-+—————+ ¦Own shares (shares in the authorized ¦ ¦ ¦ ¦ ¦ capital) ¦ 430 ¦ ¦ ¦ +————————————-+—— +————-+—————+ ¦Reserve capital ¦ 440 ¦ ¦ ¦ +————————————-+——+————-+————— + ¦Additional capital ¦ 450 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Retained earnings (uncovered ¦ ¦ ¦ ¦loss ) ¦ 460 ¦ ¦ ¦ +———————————-+——+————-+—————+ ¦Net profit (loss) of the reporting ¦ ¦ ¦ ¦ ¦period ¦ 470 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Targeted financing ¦ 480 ¦ ¦ ¦ +——————— —————-+——+————-+—————+ ¦TOTAL for Section III ¦ 490 ¦ ¦ ¦ +————————————-+——+ ————-+—————+ ¦IV. LONG-TERM LIABILITIES ¦ ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Long-term loans and borrowings ¦ 510 ¦ ¦ ¦ +——— —————————-+——+————-+—————+ ¦Long-term liabilities for ¦ ¦ ¦ ¦ ¦leasing payments ¦ 520 ¦ ¦ ¦ +——————— —————-+——+————-+—————+ ¦Deferred tax liabilities ¦ 530 ¦ ¦ ¦ +————————————-+——+— ———-+—————+ ¦Deferred income ¦ 540 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Reserves for future payments ¦ 550 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Other long-term liabilities ¦ 560 ¦ ¦ ¦ +— ———————————-+——+————-+—————+ ¦TOTAL for Section IV ¦ 590 ¦ ¦ ¦ +——————————— —-+——+————-+—————+ ¦V. SHORT-TERM LIABILITIES ¦ ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Short-term loans and borrowings ¦ 610 ¦ ¦ ¦ +——— —————————-+——+————-+—————+ ¦Short-term part of long-term ¦ ¦ ¦ ¦ ¦obligations ¦ 620 ¦ ¦ ¦ +———————— ————-+——+————-+—————+ ¦Short-term accounts payable ¦ ¦ ¦ ¦ ¦debt ¦ 630 ¦ ¦ ¦ +————————————-+ ——+————-+—————+ ¦Including: ¦ ¦ ¦ ¦ ¦suppliers, contractors, ¦ ¦ ¦ ¦ ¦executors ¦ 631 ¦ ¦ ¦ +————————— ———-+——+————-+—————+ ¦on advances received ¦ 632 ¦ ¦ ¦ +————————————-+——+——— —-+—————+ ¦on taxes and fees ¦ 633 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦ on social insurance and ¦ ¦ ¦ ¦ ¦security ¦ 634 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦on wages ¦ 635 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦for leasing payments ¦ 636 ¦ ¦ ¦ +—————— ——————-+——+————-+—————+ ¦owner of property (founders, ¦ ¦ ¦ ¦ ¦participants) ¦ 637 ¦ ¦ ¦ +———————— ————-+——+————-+—————+ ¦other creditors ¦ 638 ¦ ¦ ¦ +————————————-+——+——— —-+—————+ ¦Obligations intended for ¦ ¦ ¦ ¦ ¦implementation ¦ 640 ¦ ¦ ¦ +————————————-+——+————-+— ————+ ¦Deferred income ¦ 650 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Reserves for future payments ¦ 660 ¦ ¦ ¦ +————————————-+——+————-+—————+ ¦Other short-term liabilities ¦ 670 ¦ ¦ ¦ +——————— —————-+——+————-+—————+ ¦TOTAL for section V ¦ 690 ¦ ¦ ¦ +————————————-+——+ ————-+—————+ ¦BALANCE ¦ 700 ¦ ¦ ¦ —————————————+——+————-+————— Manager _____________________ _________________________ (signature) (initials, surname) Chief accountant ________________ _________________________ (signature) (initials, surname) __ ________________ 20__

Balance form

The balance sheet is one of the forms of individual accounting statements (clause 3 of NAS “Individual Accounting Statements”, approved by Resolution of the Ministry of Finance of the Republic of Belarus dated December 12, 2016 No. 104).

The value of assets, equity capital and liabilities is reflected in gr. 3 and 4 forms of balance sheet. In gr. 3 – at the end of the reporting year, in gr. 4 – at the end of the previous year (opening balance).

Section I “Long-term assets” contains data on the balances of fixed assets, intangible assets, profitable investments in tangible assets, investments in long-term assets, equipment for installation and construction materials, long-term financial investments, long-term receivables, deferred tax assets and other long-term assets.

In Sect. II “Short-term assets” reflects information on the balances of inventories, long-term assets intended for sale, deferred expenses, “input” VAT, short-term receivables, short-term financial investments, cash and cash equivalents, and other short-term assets.

Line 300 of the balance sheet reflects the total amount of the organization's assets and characterizes the balance sheet currency.

Section III “Equity Capital” reflects the size of the organization’s own capital, including:

– funds and reserves;

– receivables of the founders for deposits in the UV;

– the cost of the organization’s own shares (shares in the UV);

– the amount of retained profit/uncovered loss;

– balances of target financing funds unused as of December 31.

Section IV “Long-term liabilities” of the balance sheet contains data on liabilities, the repayment of which is planned no earlier than 1 year after December 31.

Section V “Current Liabilities” reflects information about liabilities that will be repaid during the next reporting year.

The indicator on page 700 of the balance sheet corresponds to the size of the organization’s equity capital and its liabilities, and also characterizes the balance sheet currency. The data on page 700 must be identical to the data on page 300. If there is no equality, then errors were made when filling out the balance.>>>