Quite often, an accountant on staff of a company is faced with the need to make appropriate deductions from an employee’s accrued salary. In accordance with the nature of this operation, the postings and corresponding accounts will differ significantly, and the actions themselves will have a lot of nuances.

In order to avoid possible mistakes and carry out the withholding correctly in accordance with all the requirements of regulatory documents, we will consider possible situations in more detail.

Classification of deductions

The accountant will need to make appropriate entries in the accounts and withhold a certain amount from the employee's salary in several cases. In the first, the procedure will take place in favor of the company itself. In the second case, the benefit will be a specific individual to whom the worker has any obligations. The third situation dictates the need to collect amounts in case of non-payment of taxes, loans and any other debts to budgetary or commercial organizations. Each of the listed categories should be considered separately, since the case may be highly specific and require an individual approach to make the right decision.

Deduction from salary at the request of the employee

Thus, in any case (whether the deduction is made in accordance with the law or at the request of the employee), operations to withhold wages, wage payments, and scholarships are reflected in the debit of the corresponding analytical accounts of account 030200000 “Calculations for accepted obligations” (030211830, 030212830, 030213830, 030262830, 030263830, 030291830) and credit account 030403730 “Increase in accounts payable for deductions from wage payments” (clause 139 of Instruction No. 174n).

In accordance with paragraph 273 of Instruction No. 157n, account 30403 “Calculations for deductions from wage payments” is intended to account for calculations for deductions from wages and allowances, scholarships; non-cash transfers to deposit accounts of employees of the institution; contributions under voluntary insurance contracts; pension insurance contributions; amounts of trade union membership dues; writs of execution and other documents.

Deductions in favor of the employing organization

In accordance with the Labor Code of the Russian Federation, the employer has the right to return partially or fully the amounts accrued (paid) to the employee if the situation that arises falls into the following categories:

- the employee failed to fulfill the required labor standards within the time allotted for work;

- an error occurred during the calculation and calculation of wages and the amount does not correspond to reality;

- the employee received advance payments, but did not complete his work;

- when performing a business trip, the employee did not fully spend the advance paid to him;

- the employee suffered established damage to the enterprise, which was confirmed and agreed upon;

- the employee was issued a loan, which will subsequently be repaid from the amount of wages due;

- the worker did not return the balance of previously issued accountable amounts;

- the person will be fired before the end of the working year in which he has already received partially or fully paid leave. However, if the reason for dismissal is sufficiently compelling and concerns the employer directly, then the employee has the right to challenge the decision in his favor while maintaining payments.

It is also worth noting that retention can be recognized as legal only if the employee himself confirms the reason for it, and the period for returning voluntarily is no more than 1 calendar month. If at least one of these two conditions is not met, then the whole situation comes under the control of the judicial authorities.

Posting deductions made from wages

After the salary is accrued on the credit of account 70, and personal income tax and other deductions are withheld on the debit of account 70, the remainder is paid to the employees. Payment can be made either from the cash register or through a bank (money is transferred to the accounts of employees from the organization’s current account), i.e. Account 70 corresponds with either account 50 “Cashier” or account 51 “Cash Account”, posting:

If deposited wages appear in accounting reports, then the organization has an account payable to the employee. If an employee does not contact the accounting department with a request to issue him a salary, then such debt is written off after the expiration of the statute of limitations. After this, the debt is written off to account No. 91 “Non-operating expenses”. The statute of limitations is three years.

Examples of accounting entries for deductions in favor of the employing organization

- Dt 20 Kt 70 wages accrued to employees of the company’s main production;

- Dt 70 Kt 68.2 withheld personal income tax;

- Dt 70 Kt 73.2 a deduction was made for material damage caused by an employee of the organization in connection with the established financial liability;

- Dt 70 Kt 73 the shortfall in the issued accountable amounts is withheld from the wages of the perpetrator;

- Dt 70 Kt 73.1 the amount of the loan issued to the employee by the organization was withheld;

- Dt 70 Kt 50 advance payment of wages paid for half a month is withheld.

Deduction from wages posting

Occurs in case of damage or loss of property (Debit 70 Credit 73.2), debt on accountable amounts (Debit 70 Credit 71). The employer can also deduct part of the funds from the employee’s salary to repay a previously issued loan (Debit 70 Credit 73.1).

Another situation: an employee took full paid leave, but quit before the end of the period for which it was taken. Amounts of vacation pay for those days to which the employee is not entitled are withheld (Debit 70 Credit 73).

Deductions in favor of an individual under writs of execution (alimony)

If an employee of an organization has obligations to pay alimony, then, based on the writs of execution previously received by the company, the required amount will be regularly deducted from the wages due for payment every month. The maintenance of one minor child accounts for 25% of the employee’s income, for two – 33%, for three or more – 50%.

All enforcement documents that were sent to enterprises for the purpose of subsequent deductions must be genuine and executed in a strictly appropriate manner. If the first copy is lost for some reason, then its duplicate, issued by the judicial authority that made the decision to recover funds, will be valid. Each document must be registered, and both the claimant and the bailiff must be notified of receipt.

Accounting for deductions from wages: postings and examples

- 13% - if the employee is a resident of the Russian Federation;

- 30% - if a non-resident of the Russian Federation;

- 35% - in case of winning, savings on interest, etc.;

- 15% - from dividends of a non-resident of the Russian Federation;

- 9% - from dividends until 2015; interest on mortgage-backed bonds until 2007, from the income of the founders of the trust management of the mortgage coverage.

- If the amount of mandatory deductions exceeds the limit (70%), then the amount of deductions is distributed in proportion to the mandatory deductions. No other deductions are made;

- The amount of limitation on deductions initiated by the employer is 20%;

- At the request of the employee, the amount of deductions is not limited.

Deductions in favor of legal entities (including under writs of execution)

In the event that an employee of an organization is late in paying a loan, is a willful defaulter, or is completely hiding from repaying debts on taxes and other obligations, then the authorities responsible for collection send enforcement officials. According to a court decision, the company that employs the debtor is obliged to withhold from the funds that it must transfer to him for the work performed, and then transfer the amount of the debt to the collector.

The documents that an accountant should follow in this situation are the Tax and Civil Codes of the Russian Federation, the articles of which describe in detail the terms and procedure for collection. It does not require the direct consent of the employee himself who committed a delay in his obligations.

Application for deduction from wages

Also, without an application from the employee, vacation pay that was paid in advance to the employee, and he, without working it out, decided to quit, can be withheld.

True, if the dismissal is associated, for example, with a reduction in headcount or staff, the employer will not be able to withhold vacation pay of his own free will (parts 2 and 3 of Article 137 of the Labor Code of the Russian Federation). In the case where the employee himself requests a deduction from wages, the amount of such deductions is not limited. After all, an employee has the right to dispose of his salary at his own discretion (Letter of Rostrud dated September 26, 2012 No. PG/7156-6-1). For example, an employee may ask the employer to transfer his salary or part of it to pay off a mortgage loan, send money to charity or to another individual to pay off a loan provided to him.

Deductions from employees' wages

- according to the writ of execution. For example, payment of alimony;

- repayment of debt to the organization (by decision of the employer with written notification to the employee);

- repayment of unspent and not returned accountable amounts in a timely manner, or in the event of failure to provide documents confirming expenses;

- in case of early termination of the employment contract, the employee reimburses the employer’s costs associated with training the employee in proportion to the unfinished period (according to the training contract);

- reimbursement of an unpaid advance payment issued to an employee on account of wages;

- in other cases, with the written consent of the employee.

According to Article 93 of the Law of the Republic of Kazakhstan “On enforcement proceedings and the status of bailiffs” dated April 2, 2010 No. 261-IV, the total amount of deduction for one writ of execution should not exceed 100 MCI. This amount is collected in periodic payments.

Features of tax calculation

The main types of income for which personal income tax must be withheld are all kinds of accruals under an employment and civil service agreement. This list includes not only direct wages, but also bonuses, allowances, and some compensation received. Special formulas are used to calculate payments.

However, personal income tax postings are made in the following situations:

- when calculating salaries;

- when deducting tax;

- when issuing wages;

- after transferring the personal income tax amount to the budget.

If an organization has employees who are periodically sent on business trips, they are entitled to appropriate travel allowances, which are also taxed (subject to the legal limit).

So, after deduction of personal income tax, the posting is completed in accordance with the appropriate procedure.

In the situation with travel expenses, several types of postings are provided:

- when issuing an advance to an employee for travel expenses;

- when calculating expenses;

- if personal income tax is assessed on amounts for business trips that exceed the norm;

- After the personal income tax is transferred to the budget, the posting is also done.

If you purchase any services from an individual, you may also need to make tax payments. In this case, the organization must deduct the appropriate amount and provide the seller with funds, taking into account the payment of personal income tax. In such a situation, wiring is also done:

- when the product or service was purchased from an individual;

- posting when withholding personal income tax;

- when transferring personal income tax to the budget;

- when transferring the amount for services or goods to the seller.

When personal income tax has been assessed on the amount, the posting of its deduction and transfer to the treasury is mandatory. After all, entities that transfer income to individuals, as a general rule, simultaneously become tax agents. Accordingly, their responsibilities include withholding and remitting tax payments.

Regulatory regulation

The procedure for holding an employee financially liable for damage caused to the employer is established by Chapter 39 of the Labor Code of the Russian Federation. The employee is obliged to compensate the employer for direct actual damage caused to him (Article 238 of the Labor Code of the Russian Federation).

An employee's financial liability may be:

- limited (Article 241 of the Labor Code of the Russian Federation) - within the limits of the employee’s average earnings;

- full (Article 243 of the Labor Code of the Russian Federation) - in the following cases: the employee is charged with full financial responsibility for damage caused to the employer during the performance of his job duties;

- a shortage of valuables entrusted to the employee on the basis of a special written agreement or received by him under a one-time document was discovered;

- the damage was caused intentionally;

- the damage was caused while under the influence of alcohol, drugs or other toxic substances;

- the damage was caused as a result of the employee’s criminal actions established by a court verdict;

- the damage was caused as a result of an administrative offense established by the relevant government body;

- information constituting a secret protected by law was disclosed;

- the damage was caused while the employee was not performing his job duties;

- responsibility is established by the employment contract concluded with the deputy heads of the organization and the chief accountant.

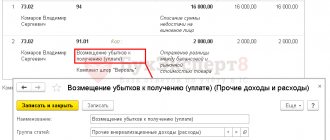

To account for settlements with employees, account 73.02 “Calculations for compensation of material damage” is used (chart of accounts 1C).

If the guilty person is identified, the shortage is assigned to him on the date (clause 8, clause 7, article 272 of the Tax Code of the Russian Federation):

- recognition of damage by the guilty party;

- the entry into force of a court decision to recover the amount of damage.

The amount of damage is calculated based on market prices, but cannot be lower than the value of the property according to accounting data (Article 246 of the Labor Code of the Russian Federation).

Control

To check accrued and withheld amounts, we will generate:

- pay slip on the Reports in the Payroll , select Pay slips ;

- report Account analysis for account 73.02 in the section Reports – Standard reports – Account analysis (can be detailed by day).

On the payslip, the amount of damages withheld is reflected in the Withheld .

The employee's debt to the organization has decreased.