Normative base

Order of the Ministry of Finance of Russia dated October 6, 2008 N 106n “On approval of accounting regulations” (together with the “Accounting Regulations “Accounting Policy of the Organization” (PBU 1/2008)”, “Accounting Regulations “Changes in Estimated Values” (PBU 21/2008)")

Order of the Ministry of Finance of Russia dated July 29, 1998 N 34n “On approval of the Regulations on accounting and financial reporting in the Russian Federation”

Resolution of the State Statistics Committee of the Russian Federation dated August 18, 1998 N 88 “On approval of unified forms of primary accounting documentation for recording cash transactions and recording inventory results”

Resolution of the State Statistics Committee of the Russian Federation dated March 27, 2000 N 26 “On approval of the unified form of primary accounting documentation N INV-26 “Record of results identified by inventory”

Any organization conducts an inventory of material assets at least once a year. To do this, it is necessary to appoint a special commission from among authorized employees and issue an order to conduct an inventory. The procedure and schedule for conducting an inventory in an organization must be enshrined in the accounting policy for accounting purposes (clause 4 of PBU 1/2008). However, an inventory commission is created for each specific case. Its composition, powers, as well as the timing of the inventory must be enshrined in a separate internal act of the organization.

In budgetary organizations, through an inventory, it becomes possible to check the availability and condition of property. Compare property data since the last inspection with the results as of the current date, identify the nature and reasons for possible discrepancies. And based on the data obtained, evaluate the correctness and compliance of the accounting carried out at the enterprise. In general, the reasons and procedure for inventory in a budgetary and commercial organization are approximately the same.

What is needed for this?

The head of the organization issues an appropriate order, on the basis of which the composition of the inventory commission is formed. Its members must have the authority to verify the compliance of the funds actually available with the data reflected in the accounting records. This could be a merchandiser, an accountant, a quality control specialist, etc., the main thing is that the number of members in the commission is at least 3 people.

The accounting department is obliged to transfer to the members of the commission all accounting data on the product, fixed assets or inventory items that are subject to the inventory. Depending on what is being inventoried, these can be accounting registers, book balances, reports on the movement of inventory items.

If necessary, the inspection location may be sealed. The commission begins its work and verifies whether the actual availability of valuables corresponds to the quantity indicated in the accounting documents.

When is inventory needed?

A sample order for inventory is usually required in some cases listed in clause 27 of Order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n, in particular:

- before drawing up the annual report;

- when appointing new financially responsible persons, including in connection with the transfer of property to third parties;

- after thefts or natural or man-made emergencies (fires, floods, explosions, etc.).

Typically, the order to begin an inspection is issued by the head of the organization, either scheduled or unscheduled. The person responsible for such an event is usually the chief accountant or another accounting employee. A special commission is engaged in counting material assets, the members of which must be familiarized with the relevant local act upon signature.

Let's sum it up

- Preparation for an inventory begins with the creation of an inventory commission and the issuance of an inventory order.

- Before the start of the main verification activities, the commission receives receipts from materially responsible persons stating that the assets under their responsibility have been capitalized, retired assets have been written off, and receipts and expenditure orders have been transferred to the accounting department or commissions.

- The commission must consist of at least 3 people, including representatives of the administration and accounting department.

- Financially responsible persons cannot be members of the commission.

If you find an error, please select a piece of text and press Ctrl+Enter.

Inventory order form

The main document of the inventory process is the order. Therefore, we will consider it in more detail and learn how to compose this document correctly. A unified sample order for inventory for 2021 can be found in Resolution No. 88 of the State Statistics Committee of Russia dated August 18, 1998. Form No. INV-22 is a universal form that can be used by organizations of all forms of ownership. The form can be used both when conducting scheduled and unscheduled inspections of material assets.

Sample of filling out an order to conduct an inventory of 2021 in budgetary institutions

Form of order to conduct inventory according to form No. INV-22

If for some reason this form is not suitable, you can develop your own. The main thing is that it is enshrined in the company's accounting policy. An arbitrary sample order for inventory of material assets 2021 may look something like this:

In any case, the document must contain the following mandatory details and information:

- company name;

- date of preparation and document number;

- the purpose of the inspection and what it will concern: goods, fixed assets, tangible assets, accounts receivable, all property of the company;

- divisions and departments of the company in which the inspection will be carried out: warehouse, store, accounting or the entire company as a whole;

- period and duration of the event - from what date to what date, when to provide the results of verification actions;

- composition of the commission and full name its chairman (the commission, in addition to the company’s employees, can include third-party auditors);

- details of the manager who signed the document.

After publication, the local act must be registered in a special journal to record control over the implementation of such decisions. Its recommended form can be taken from Goskomstat Resolution No. 88 (Form No. INV-23) or developed independently. All employees listed in it must be familiarized with the order. They can sign the acquaintance directly on the form or on a separate sheet of acquaintance with the document, which is filed with the order.

Inventory commission: formation, composition and minutes of the meeting

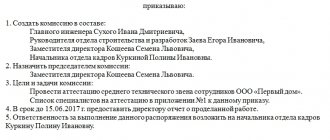

The organization's inventory is carried out by a special commission, the composition of which is appointed and approved by the director of this organization. He does this with the help of an order. In this regard, all managers should know what a sample order for the creation of an inventory commission looks like.

In the course of their activities, organizations must conduct inventories. This is necessary to verify the actual existence of the company’s property and liabilities.

To carry out an inventory, an inventory commission is created in the organization. It is approved by order of the director of the company. This order must be formatted as follows:

- The full name of the institution is indicated, indicating the organizational and legal form.

- Then the number of the order to create an inventory commission is written down.

- Then be sure to indicate the date and place of drawing up the document.

- After this they write that the order was drawn up in accordance with the methodological recommendations of the Ministry of Finance for conducting inspections required this year.

- Then follows the text of the order:

- I order the creation of an inventory commission with the following composition: the positions, surnames, first names and patronymics of the chairman and all members of the commission are indicated.

- Assign the following obligations to the commission: conduct an inventory of the company's assets and liabilities in accordance with the inventory schedule for the current year;

- timely and correctly document inventory results;

- ensure the accuracy and completeness of entering into the inventory information about the balances of inventories, products, money, fixed assets, as well as other property and liabilities.

- After this, the chairman and all members of the commission must confirm their familiarity with the order. To do this, they affix their signatures.

A sample order for the appointment of an inventory commission is given below:

Composition of the inventory commission

The composition of the inventory commission (both permanent and working) is approved by the head of the company with the help of an appropriate order. This order must be registered in the journal for monitoring the implementation of orders to conduct inventories.

The inventory commission may include:

- accounting staff;

- company administration employees;

- employees involved in internal audit in the organization;

- employees of independent audit companies;

- specialists from other fields.

In addition, the same employees can be members of several commissions at once. For example, commissions for inventory and commissions for the disposal and receipt of valuables.

It is worth noting that employees who are financially responsible cannot be part of the inventory commission. They can only be present during the inspection.

If an inventory of financial liabilities and assets is being carried out, the chief accountant must be present on the commission. And if an inventory of non-financial assets is carried out, the accountant cannot be a member of the commission. He will have to provide the information necessary for verification, as well as draw up an inventory.

If the chief accountant is the chairman of the commission, then the remaining members should be either heads of departments or ordinary employees.

Also, the chairman of the commission can be the manager of the company himself. In such a situation, he can assign control over the fulfillment of obligations to the chief accountant. This will make more sense for the company itself. This is due to the fact that if the chief accountant is the chairman, then he can only perform management responsibilities.

The director of the organization can independently decide how many members of the inventory commission there will be, based on the type of inventory being carried out and the specifics of the company’s activities. The legislation does not regulate this issue. Basically, organizations form commissions of four people.

If the composition of the inventory commission is incomplete, an inspection is unacceptable.

If the inventory requires a large amount of work, an additional working commission is formed. The personal composition of the working inventory commission is approved by the company manager. Such a commission may include employees of the same positions as the main inventory commission.

Minutes of the meeting of the inventory commission: sample

After the commission finishes taking inventory, it must hold a meeting. During this meeting, key findings and identified discrepancies are identified.

Also during the meeting, the commission must establish the reason for the identified inconsistencies and ways to correct the current situation.

Based on the results, a protocol of the meeting of the inventory commission should be drawn up.

This document has the following structure:

- full name of the company where the inspection was carried out, indicating the organizational and legal form;

- date and place of document preparation;

- the name of the unit that was subject to inventory;

- the name of the document being drawn up is the protocol of the inventory commission;

- a list of commission members, indicating their positions, as well as surnames and initials;

- description of the results of the inspection performed;

- a list of employees who spoke on this issue;

- the decision that was made on the issue under discussion;

- the conclusion made by the commission;

- identified violations (if any);

- employees guilty of violations, indicating positions, surnames and initials;

- information about the measures taken to eliminate the identified deficiencies;

- signatures of the chairman and all members of the commission.

The execution of this protocol must be accompanied by the following attachments:

- executed acts and inventories of the inventory carried out using INV type forms for each person bearing financial responsibility, facility, warehouse or division of the company. There are nineteen of them in total, depending on the type of inspection being carried out;

- a list of obsolete and unsuitable products for further use;

- a list of missing or surplus products, indicating their price;

- explanations of the workers who are responsible for the swearing. liability, and other officials regarding excess or shortage of valuables (acts, certificates, copies of primary documents).

During the meeting, the commission must make the following proposals:

- on the timing and methods of eliminating shortages, as well as on conducting internal investigations (if a shortage is detected);

- on the continued use of outdated and unsuitable products for subsequent use;

- other proposals regarding working with inventory items.

It is worth noting that if during the inventory no violations were found, as well as no workers responsible for this, there is no need to draw up an inventory protocol.

A sample minutes of the meeting of the inventory commission is given below:

Cases of invalidation of inventory results

There are several cases when inventory results can be invalidated:

- the director’s order does not contain a statement regarding the composition of the commission;

- not all members of the commission are present during the inventory;

- unauthorized citizens gained access to inventory documents;

- members of the commission did not put their signatures on the inventory lists;

- there were mistakes and blots made when filling out the documents;

- the financially responsible person was not present during the inspection;

- the order to conduct an inventory was issued incorrectly;

- the order of paperwork was violated.

Tasks and responsibilities of the inventory commission

There are two types of inventory commissions. Depending on the type of commission, its main tasks differ.

- permanent commissions;

- working commissions.

The tasks of the inventory commission, operating on a permanent basis, are:

- conducting scheduled and random inventories, as well as control checks;

- carrying out preventive work to ensure the safety and integrity of the company’s assets, listening to department directors regarding this issue at meetings;

- organizing inventories and conducting briefings for work commissions.

Inventory working commissions perform the following tasks:

- checking the accuracy of determining differences in inventory;

- control over the safety of assets;

- checking compliance by employees bearing financial responsibility with the rules for maintaining primary records and storing assets;

- Carrying out repeated comprehensive inspections when gross violations are detected;

- consideration of written explanations from employees who have caused damage or shortage of valuables, as well as other violations.

The responsibilities of the inventory commission include:

- obtaining the necessary documents before starting the inventory;

- before starting a check for the actual presence of valuables - obtaining the latest documents on receipts and expenses or reports on the movement of money and valuables;

- at the time of the inspection - ensuring the completeness and accuracy of entering into the inventory information about the balances of money, products, inventories, fixed assets, other property, as well as financial obligations; ensuring the accuracy and timeliness of registration of the results of the audit;

- if errors and inaccuracies are discovered in the inventories after the completion of the inventory, check the specified facts; if they are confirmed, the detected errors will be corrected in the prescribed manner.

The responsibilities of the inventory commission before the start of the inspection include:

- find out whether the organization’s territory is protected and whether there is a fire alarm on the premises;

- check whether there are liability agreements with relevant employees;

- check whether the organization has safes, warehouses and cabinets for storing valuables;

- check whether places where valuables are stored are equipped with measuring instruments;

- establish whether the company complies with the conditions for storing valuables that belong to third parties;

- clarify whether there is control over the removal of valuables from the organization and the procedure for issuing powers of attorney to receive them;

- check whether there is an order from the director of the company to appoint a commission that checks the safety of valuables.

The functions of the inventory commission are:

- conducting an inspection of property, money, securities, unfinished production and other valuables in places of production and storage;

- together with accounting staff, participate in determining the result of the audit and develop proposals regarding the accounting of surpluses and shortages;

- make their proposals on the issues of streamlining the release, storage and reception of valuables, improving control over them and their accounting, and the sale of property and valuables that the company does not need;

- drawing up a final protocol indicating the state of the warehouse; the results of the audit, as well as conclusions regarding them; proposals to offset surpluses and shortages, write off shortages within the limits of natural loss and overtime shortages;

- bearing responsibility for and compliance with the inventory procedure and its timeliness, in accordance with the order of the director of the company, for the accuracy and reliability of the information entered into the inventory list.

Source: https://okbuh.ru/inventarizatsiya/komissiya-formirovanie-sostav-i-protokol-zasedaniya

Step-by-step instructions for drawing up an order

Step 1. Specify the name of the document.

Step 2. In the appropriate fields, enter the name of the organization (IP), indicate OKPO, and write the date of compilation.

Step 3. Fill out the main part of the order. Here you should clarify the type of inspection and its purpose, as well as list the members of the inventory commission participating in the event and its chairman. Their first and middle names can be abbreviated.

Step 4. We indicate which material assets and in which departments and separate divisions of the company should be checked.

Step 5. We indicate the exact timing of the inspection with its start and end dates.

Step 6. We inform you about the reasons for the need to inventory valuables.

Step 7. We indicate the deadline for submitting the audit results to the accounting department.

Step 8. We certify the document from the manager.

Step 9. Assign a number and register it in a special journal.

Step 10. We introduce it to all interested parties, including employees of departments and divisions where the inspection will take place.

Inventory compilation and analysis

During the inspection, members of the commission fill out an inventory list. It records all the actual data on the availability of goods or material assets. The inventory can be compiled in free form, but it must contain the following data:

- name and nomenclature number of the unit;

- variety and its article;

- measure (kg, pcs., etc.);

- unit price;

- quantity on hand in actual and monetary terms.

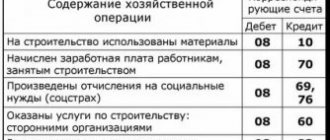

Information from the inventory is analyzed and verified with data submitted by the accounting department. If there are discrepancies between the data, the commission draws up a statement of results. For convenience, use the standard statement template No. INV-26, which was approved by Resolution of the State Statistics Committee No. 26 dated March 27, 2000.

This document indicates all identified surpluses and shortages.

Results of inspection of goods and materials and another order

At the end of the procedure for calculating and comparing the results, members of the commission must properly document the results of the inspection. All identified discrepancies must be recorded in the results record sheet (form No. INV-26) from Goskomstat Resolution No. 26 dated March 27, 2000. And after discussing the results and the inventory commission making a verdict, which is recorded in a special protocol, the manager must issue another order to this time about the results of verification activities and the results that were achieved. The reaction of the head of the company to the proposals of the commission members and instructions on the necessary actions should be given. This could be: additional verification, sanctions for perpetrators, introduction of additional security measures. The same local act appoints employees responsible for its implementation, who should also be familiarized with the document for signature. Control over the execution of orders is usually left to the director of the company.

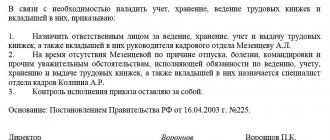

Creation of a commission for writing off inventory items in 2021

In accordance with the administrative document, the commission is obliged to carry out an inventory within the established time frame, and after that draw up an appropriate act and liquidate written-off inventory items. The manager’s order is confirmation of his agreement with the need to conduct an inventory. However, this document is not mandatory. It is drawn up only so that the entire process has formality, and during its implementation a certain procedure is observed. For example, if equipment is retired due to sale, then the basis for its write-off will be an agreement with the buyer. In this case, drawing up an order will not be required. But, as a rule, its preparation is necessary, especially when the reason for disposal of inventory items is moral or physical wear and tear.

We recommend reading: Orphanhood Statistics in Russia 2021

Commission for write-off of inventory items: composition

- name of company;

- place, date of issue of the order;

- name of the document, order number;

- grounds for drawing up the document;

- the main text containing the order on the creation of the commission, the purpose of its formation and inventory, the timing of the procedure, as well as the date of drawing up the act;

- information about the object (name, inventory number, reason for checking inventory, initial cost, as well as funds spent on depreciation);

- list of persons responsible for execution of the order;

- signatures of persons related to the document, signature of the manager.

- the results of the inspection are subject to approval;

- it is necessary to indicate the requirement to resolve discrepancies identified during the inventory and recorded in the relevant documents;

- an employee is appointed, usually from the accounting department, who is responsible for fulfilling the requirements of this order related to the elimination of discrepancies previously identified during the audit;

- an employee is appointed responsible for monitoring the implementation of the orders recorded in the provisions of the order on summing up the results.