The concept of an organization's reserves. Types of stocks

Every company that operates needs a variety of resources . If we talk about production organizations, then inventories play one of the leading roles in it. Resources in this case are consumed to manufacture products and satisfy their current needs .

Take our proprietary course on choosing stocks on the stock market → training course

For example, an enterprise that produces paving slabs at least has at its disposal special forms and mixtures for its production. The manufactured product is already stored as a commodity in a warehouse. Another example is a small accounting firm that provides outsourcing services. Even such an organization has paper, computer equipment, and stationery.

It turns out that all organizations, without exception, have at their disposal certain reserves.

Due to the fact that there are a great many reserves, they were combined into several groups. There are several classifications of reserves. Let's take a closer look at what stocks there are depending on their form. The following types are distinguished by type:

| Stock name | Account | Explanation |

| Stocks of raw materials and material resources | 10 | These are all those material assets that are used in the future in production, provision of services or carrying out current activities |

| Unfinished production | 20 | If a company produces products, then it probably has work in progress, that is, products that have not yet gone through the full production cycle. Different types of products may be at different stages of production |

| Finished products | 43 | After the production process is completed, the output is a full-fledged product, which is intended for further sale to customers. While the product is in the warehouse, it is also included in the organization’s inventory. |

| Waste | 10 | This is all that is no longer needed in the production cycle and will not be used in the company |

| Accessories | 10 | Supplies used for equipment maintenance, repair and maintenance |

It must be remembered that raw materials are a broad concept that includes various types of supplies.

Organizational inventory accounts. Formula for calculating the amount of reserves

Since an organization’s reserves include many different types, there are quite a lot of accounts for their accounting. To calculate the amount of inventory for reporting, it is necessary to collect information on the following accounts:

- Account 10. It collects information about the cost of those material resources that are involved in the production of products. This includes the raw materials from which products are made, fuel, spare parts, containers, equipment and other similar property. Special clothing is also taken into account here.

- For livestock organizations, account 11 is relevant, which takes into account animals on the balance sheet

- When purchasing inventories, depending on the provisions of the accounting policy, accounts 15 or 16 can be used. When inventories are received from suppliers, in this case posting D15 (16) K60 is made. After registering, for example, fuel, a D10 K15(16) entry is made. But since this method of accounting is quite cumbersome and intermediate posting appears, these accounts are often not used

- The calculation involves accounts reflecting the presence of semi-finished products or defects - accounts 21 and 28, respectively. The amounts for them must be taken into account when calculating

- Information on different types of production is collected on accounts 20, 23 and 29

- The next large group for which information is collected when calculating data for line 1210 of the balance sheet concerns goods and products already produced. This includes accounts 41, 42, 43, 44, 45

- In addition, when calculating, the amount in account 97 is taken into account, but not all, but only that which relates to expenses written off during the year

Account 14 deserves special attention. The organization’s accounting policy may include a condition for creating a special reserve to reduce the cost of inventories. This reserve is created at the end of the year, before the balance sheet is formed. This occurs if the value of inventory at accounting prices is higher than at market prices. That is, the amount of the reserve is the difference between the book value and market value, multiplied by the amount of inventory .

The creation of such a reserve is reflected in D91 K14, and its write-off in D14 K91.

Accounting entries

The large number of accounting accounts, especially if we also take into account their subaccounts, leads to some confusion and hundreds of possible combinations. It is difficult to describe all the posting options, but we can highlight those that are most often used in accounting.

Fixed Asset Accounting

This includes all assets involved in production. Depending on the type of activity, these can be structures, tools, transport, perennial plants, animals. A special feature of this material base is their use time, which exceeds 12 months. If we talk about equipment that operates for a long period of time, its cost gradually decreases, approaching the cost of the product.

Postings of intangible assets

Intangible assets can be financially profitable without having a physical form, but with the ability to be identified. This may include the reputation of a unit or intellectual objects with a program, trademark or selection achievement.

Accounting for inventories

MTZ wiring is considered necessary due to the periodic purchase of component materials. This point is one of the simplest, so even for a novice accountant it is absolutely clear.

Important! Nowadays, fuel cards are very common and are used by many organizations related to transport movement. For inexperienced accountants, their accounting may be associated with some difficulties, because there is no precise legislative basis for this procedure.

Postings for production cost accounting

There are several required accounts for this action that can be confusing. In this case, it is necessary to specify the type of valuation taking place if it is planned to write off inventories from the balance sheet.

Accounting for goods and finished products

People who do accounting in trade organizations need to know the procedure for posting finished products. When purchasing goods from wholesale suppliers, you must carefully check the documents provided by the intermediary. Here you need to study all the conditions and not agree to an unfavorable offer.

Cash accounting

Almost all organizations and manufacturing enterprises work with financial turnover. For financial accounting, you need to work on accounts 50 and 51. Money is stored in a bank account or in a cash register; accordingly, there are several types of such transactions. It is important to remember the need to prepare all relevant documents for cash transactions, these could be advance reports, inventory reports, payment orders and cash orders.

Postings of loans and credits

Often in business activities financing or borrowed funds are used. To obtain a loan, a businessman needs to visit a bank. The accountant’s responsibilities include the formation of a credit transaction, which reflects the funds received and calculates the monthly payment schedule.

Accounting for final profit

Any entrepreneurial activity involves obtaining a final income. The result can be either unprofitable or profitable and is formed at the end of each reporting period. If the amount of income exceeds expenses, the company's profit increases. Revenue is recorded as a debit, and expenses as a credit. If at the end of the reporting period there is a credit balance, the organization makes a profit.

Important! Nowadays, there are many Internet services that lure inexperienced accountants by offering to prepare online entries absolutely free of charge. Of course, their use is not prohibited, but it should be understood that any financial transaction has its own nuances, so the result may not be entirely correct. Therefore, every accountant should thoroughly know all the accounts so that there is no need to use such programs.

Reflection of inventories in the organization's balance sheet

As can be seen from the above formula, account balances are involved in calculating the amount of inventory. In terms of materials, this means that all raw materials that are currently not used remain on the company’s balance sheet.

It must be remembered that materials are subject to accounting at actual cost, and VAT must be excluded from the cost.

An organization can account for inventories in account 10 at planned prices, using accounts 15 and 16.

| IMPORTANT! Information on line 1210 gives an idea of the financial stability of the company and the ability to perform this or that work. A missing inventory amount or a small line value is not a very good sign. If this is not related to serious problems in the company, then it is necessary to competently build a marketing line |

Reflection of the cost of finished products in the balance sheet

Finished products produced by the company are accounted for on account 43. They are one of the components of the organization's reserves and, in accordance with this, are shown in the balance sheet at actual cost.

However, there is a nuance here. Until the product has gone through all stages of production, it is impossible to calculate the actual costs of its creation. In this regard, it is customary for organizations to keep records of such products within a month at discount prices that are chosen by the company . At the end of the month, after all operations have been completed, actual production costs are collected and the cost of production is adjusted.

The following entries are made:

- The accounting value of products can be reflected as D43 K40 or D43 K20 (20, 29). The organization itself decides which method to choose.

- The difference between the accounting value and the actual value is reflected in D40 K20 (23, 29) or D43 K20 (23, 29). The posting is selected depending on which accounting method was selected

After the products are sold and written off, a balance appears, the amount of which should be reflected in line 1210.

Line 1210 “Inventories”: how to fill out correctly

Line 1210 “Inventories”

On line 1210

information about the organization's reserves is reflected:

(in terms of raw materials, materials and other inventories)

(in terms of raw materials, materials and other inventories)

(for expenses with a write-off period not exceeding 12 months)

The following assets are accepted as inventories:

- used as raw materials, materials, etc. in the production of products intended for sale (performance of work, provision of services);

- intended for sale;

- used for the management needs of the organization.

Finished products are part of inventories intended for sale (the final result of the production cycle, assets completed by processing (assembly), the technical and quality characteristics of which comply with the terms of the contract or the requirements of other documents, in cases established by law).

Goods are part of inventories purchased or received from other legal entities or individuals and intended for sale.

The actual costs of purchasing inventories include:

- amounts paid in accordance with the agreement to the supplier (seller);

- amounts paid to organizations for information and consulting services related to the acquisition of inventories;

- customs duties;

- non-refundable taxes paid in connection with the acquisition of a unit of inventory;

- remunerations paid to the intermediary organization through which inventories were acquired;

- costs for the procurement and delivery of inventories to the place of their use, including insurance costs. These costs include, in particular, costs for the procurement and delivery of inventories; costs of maintaining the procurement and warehouse division of the organization, costs of transport services for the delivery of inventories to the place of their use, if they are not included in the price of inventories established by the contract; accrued interest on loans provided by suppliers (commercial loan); interest on borrowed funds accrued before the inventory was accepted for accounting, if it was raised for the acquisition of these inventories;

- costs of bringing inventories to a state in which they are suitable for use for the intended purposes. These costs include the organization’s costs of processing, sorting, packaging and improving the technical characteristics of received stocks, not related to the production of products, performance of work and provision of services;

- other costs directly related to the acquisition of inventories.

This is interesting: How to obtain a weapons permit for a military personnel

When releasing inventories (except for goods accounted for at sales value) into production and otherwise disposing of them, they are assessed in one of the following ways:

- at the cost of each unit;

- at average cost;

- at the cost of the first acquisition of inventories (FIFO method).

In the financial statements, at least the following information is subject to disclosure, taking into account materiality:

- on methods for assessing inventories by their groups (types);

- about the consequences of changes in methods of valuing inventories;

- on the cost of inventories pledged;

- on the amount and movement of reserves for reducing the value of material assets.

Animals for growing and fattening include:

- young animals;

- adult animals in fattening and feeding;

- birds;

- animals;

- rabbits;

- bee families;

- adult cattle culled from the main herd for sale (without fattening);

- livestock accepted from the population for sale.

When forming expenses for ordinary activities, their grouping should be ensured by the following elements:

- material costs;

- labor costs;

- contributions for social needs;

- depreciation;

- other costs.

Products (works) that have not passed all stages (phases, redistributions) provided for by the technological process, as well as incomplete products that have not passed testing and technical acceptance, are classified as work in progress.

Work in progress in mass and serial production can be reflected in the balance sheet:

- according to actual or standard (planned) production cost;

- by direct cost items;

- at the cost of raw materials, materials and semi-finished products.

The goods shipped may include:

- finished products (finished products);

- goods;

- work;

- services;

- animals for growing and fattening;

- semi-finished products of own production;

- materials and other similar valuables.

Selling expenses

If the amount of transportation and procurement costs associated with the acquisition (procurement) of goods and their delivery to the organization constitutes a significant share in the total revenue from sales of goods (more than ten percent), as well as if their level is uneven throughout the year (products crop production, fishing, etc.), then a proportional distribution of these expenses is allowed between the actual cost of goods sold in a given month and their balance at the end of the month. In this case, the share attributable to the balance of goods not sold by the end of the month remains in account 44 “Sales expenses” and is transferred to the next month.

In organizations engaged in industrial and other production activities, account 44 “Sales expenses” may reflect, in particular, the following expenses: for packaging and packaging of products in finished product warehouses; for delivery of products to the departure station (pier), loading into wagons, ships, cars and other vehicles; commission fees (deductions) paid to sales and other intermediary organizations; on the maintenance of premises for storing products at places of sale and remuneration of sellers in organizations engaged in agricultural production; for advertising; for entertainment expenses; other expenses similar in purpose.

In organizations engaged in trading activities, account 44 “Sales expenses” may reflect, in particular, the following expenses (distribution costs): for the transportation of goods; for wages; for rent; for the maintenance of buildings, structures, premises and equipment; for storage and processing of goods; for advertising; for entertainment expenses; other expenses similar in purpose.

In organizations that procure and process agricultural products (beets, milk, wool, cotton, leather raw materials, flax, livestock, poultry, etc.), account 44 “Sales expenses” can reflect, in particular, the following expenses: other expenses ; general procurement expenses; for the maintenance of procurement and receiving points; for the maintenance of livestock and poultry at bases and reception points.

This is interesting: How to find out the taxes of an individual using the tax identification number

PBU 5/01 “Accounting for inventories”

Buyers are organizations, enterprises and individuals who purchase a product from an enterprise. Along with buyers, customers are also taken into account; these are enterprises and organizations to which this enterprise provides services or performs any work.

Settlements with them are formalized by settlement documents - these are invoices and invoices. Based on these documents, settlements with buyers and customers are reflected in accounting. These documents reflect all the details of the supplier and buyer:

— name of goods, works, services; - unit of measurement; - quantity; — price; - price; — VAT; - all to the calculation.

Documents are signed by the manager, chief accountant, and stamped. They are registered and sent to buyers for settlements.

Work in progress in the company's annual reporting

Everything that was unfinished in the reporting period is work in progress. These are products that have not passed all stages of the production process or quality control, or unprovided services.

Unfinished processes are reflected in accounts 20, 23, 29, 44, 46. Accordingly, the balances on these accounts will be the value of work in progress.

As a general rule, the volume of work in progress should be reflected in line 1210.

In addition, it is possible to select a separate substring if the amount is really large.

If production is very long, then information about work in progress can be reflected in the first section of the balance sheet.

An example of calculating the amount of reserves to be reflected in the balance sheet

Let's give a simple practical example of calculating the value of line 1210 of the balance sheet. We present the company's initial data in the table. It is assumed that there are no initial balances.

| Account | Turnover | balance | ||

| Debit | Credit | Debit | Credit | |

| 10 | 29000 | 17000 | 12000 | |

| 20 | 305000 | 300000 | 5000 | |

| 41 | 200000 | 150000 | 50000 | |

| 42 | 150000 | 200000 | 50000 | |

| 44 | 250000 | 200000 | 50000 | |

| 45 | 20000 | 15000 | 5000 | |

Based on the given data and guided by the calculation formula, in line 1210 you need to write down the final value - 72,000 rubles:

12000 + 5000 + 50000 – 50000 + 50000 + 5000 = 72000 rubles

One more thing. Many companies have insurance that is accounted for as deferred expenses. For example, on October 1, a car was insured. The cost of insurance was 12,000 rubles. These expenses are included in expenses in equal monthly shares. Therefore, the monthly amount will be 1000 rubles (12000/12 months). By the end of the year, 3,000 rubles (1,000*3 months) will be written off. The balance in the amount of 9,000 rubles (12,000-3,000) is transferred to the next year. This amount must be recorded in line 1210.

Chart of Accounts 2021

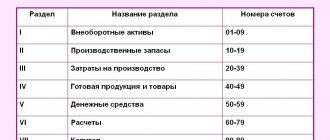

All synthetic accounts that can be used in accounting are indicated in the Chart of Accounts. A CHART OF ACCOUNTS or PLAN OF ACCOUNTS is a systematic list of accounting accounts. According to the Chart of Accounts, accounting must be organized at enterprises of all sectors of the national economy of the Russian Federation, regardless of subordination, organizational and legal form and form of ownership. The exception is banks, budgetary and insurance organizations, which have their own charts of accounts. The use of the Chart of Accounts ensures: – uniformity in the construction of accounting records of all economic entities on the territory of the Russian Federation. – obtaining comparable information and, as a result, generalized indicators on the scale of individual industries, enterprise associations and the national economy as a whole. In the Plan, all accounts are summarized in eight sections : 1 - Non-current assets 2 - Inventory 3 - Production costs 4 - Finished products and goods 5 - Cash 6 - Accounts 7 - Capital 8 - Financial results It can be seen that in the accounting plan they are first placed asset and process accounts and then liability and equity accounts. The final section is the one that forms information about financial results as the ultimate goal of the enterprise. Thus, each section combines accounts associated with a certain stage of the circulation of economic assets. Within each section, the accounts are arranged in a certain logical sequence. All synthetic accounts included in these sections are called balance sheet accounts - they participate in the formation of balance sheet items and serve to account for economic assets and their sources owned by the enterprise and brought into circulation by it. Balance sheet accounts in the plan are assigned two-digit code (number). For example, the “Cashier” account is assigned the number 50. This means that at any enterprise anywhere the , account 50 reflects information about the availability of funds in the enterprise’s cash register and their movement. Each account in the Chart of Accounts has Instructions (guidelines) for its use . It includes brief characteristics of the economic content and structure of all accounts and the general scheme of their correspondence. After the balance sheets in the Chart of Accounts there is a list of off-balance sheet accounts intended for accounting for economic assets that do not belong to the enterprise, but are in limited use, as well as funds taken by the enterprise for safekeeping (for example, leased fixed assets; materials accepted for processing; equipment accepted for installation, goods accepted for commission, etc.). Off-balance sheet accounts are assigned three-digit number. Based on the Chart of Accounts, the enterprise develops a working chart of accounts , taking into account the specifics of the enterprise’s activities and the management tasks to be solved. The working chart of accounts is approved in the order on accounting policies. To account for specific transactions, an enterprise can introduce additional synthetic accounts, consolidating its decision in its accounting policies. For this purpose, free code numbers are provided in each section of the Chart of Accounts, allowing, if necessary, to supplement the Plan with new accounts without changing the general numbering of accounts. Subaccounts can be used by an enterprise at its own discretion - you can clarify their contents, exclude them, combine them, or enter additional accounts. CHART OF ACCOUNTS FOR FINANCIAL AND ECONOMIC ACTIVITIES OF ORGANIZATIONS

| Attitude towards balance | Account number | Synthetic account name |

| Section I. NON-CURRENT ASSETS | ||

| A | 01 | Fixed assets |

| P | 02 | Depreciation of fixed assets |

| A | 03 | Profitable investments in material assets |

| A | 04 | Intangible assets |

| P | 05 | Amortization of intangible assets |

| A | 06 | Deferred tax assets |

| A | 07 | Equipment for installation |

| A | 08 | Investments in non-current assets |

| Section II. PRODUCTIVE RESERVES | ||

| A | 10 | Materials |

| A | 11 | Animals being raised and fattened |

| P | 14 | Reserves for reduction in the value of material assets |

| A-P | 15 | Procurement and acquisition of material assets |

| A-P | 16 | Deviation in the cost of material assets |

| A | 19 | Value added tax on purchased assets |

| Section III. PRODUCTION COSTS | ||

| A | 20 | Primary production |

| A | 21 | Semi-finished products of our own production |

| A | 23 | Auxiliary production |

| A | 25 | General production expenses |

| A | 26 | General running costs |

| A | 28 | Defects in production |

| A | 29 | Service industries and farms |

| Section IV. FINISHED PRODUCTS AND GOODS | ||

| A-P | 40 | Release of products (works, services) |

| A | 41 | Goods |

| P | 42 | Trade margin |

| A | 43 | Finished products |

| A | 44 | Selling expenses |

| A | 45 | Goods shipped |

| A | 46 | Completed stages of unfinished work |

| Section V. CASH | ||

| A | 50 | Cash register |

| A | 51 | Current accounts |

| A | 52 | Currency accounts |

| A | 55 | Special bank accounts |

| A | 57 | Transfers on the way |

| A | 58 | Financial investments |

| P | 59 | Provisions for impairment of financial investments |

| Attitude towards balance | Account number | Synthetic account name |

| Section VI. CALCULATIONS | ||

| P | 60 | Settlements with suppliers and contractors |

| A | 62 | Settlements with buyers and customers |

| P | 63 | Provisions for doubtful debts |

| P | 66 | Calculations for short-term loans and borrowings |

| P | 67 | Calculations for long-term loans and borrowings |

| P | 68 | Calculations for taxes and fees |

| P | 69 | Calculations for social insurance and security |

| P | 70 | Payments to personnel regarding wages |

| A-P | 71 | Calculations with accountable persons |

| A-P | 73 | Settlements with personnel for other operations |

| A-P | 75 | Settlements with founders |

| A-P | 76 | Settlements with various debtors and creditors |

| P | 77 | Deferred tax liabilities |

| A-P | 79 | On-farm settlements |

| Section VII. CAPITAL | ||

| P | 80 | Authorized capital |

| A | 81 | Own shares (shares) |

| P | 82 | Reserve capital |

| P | 83 | Extra capital |

| A-P | 84 | Retained earnings (uncovered loss) |

| P | 86 | Special-purpose financing |

| Section VIII. FINANCIAL RESULTS | ||

| A-P | 90 | Sales |

| A-P | 91 | Other income and expenses |

| A | 94 | Shortages and losses from damage to valuables |

| P | 96 | Reserves for future expenses |

| A | 97 | Future expenses |

| P | 98 | revenue of the future periods |

| A-P | 99 | Profit and loss |

| Off-balance sheet accounts | ||

| 001 | Leased fixed assets | |

| 002 | Inventory assets accepted for safekeeping | |

| 003 | Materials accepted for recycling | |

| 004 | Goods accepted for commission | |

| 005 | Equipment accepted for installation | |

| 006 | Strict reporting forms | |

| 007 | Debt of insolvent debtors written off at a loss | |

| 008 | Security for obligations and payments received | |

| 009 | Security for obligations and payments issued | |

| 010 | Depreciation of fixed assets | |

| 011 | Leased fixed assets |

Don’t know how to solve or complete a coursework or dissertation? Order a solution