Contents of the reporting form liability

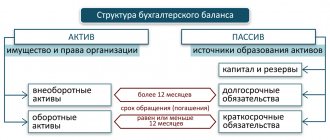

The asset reflects data on the enterprise's property assets, monetary resources and material reserves. This block of information shows what the company actually has.

In turn, the liability side of the balance sheet reflects information about the sources of formation of the enterprise’s property base. All liability sections systematize data on sources of financing, short-term and long-term obligations.

The balance sheet form has been approved by the Ministry of Finance. Its current template is given in the order dated 07/02/2010 under No. 66n. Structurally, the passive consists of three sections:

- Capital and reserves.

- Long-term liabilities.

- Short-term liabilities.

All sections are detailed by lines. Each indicator is assigned an individual code.

Strings

The information block dedicated to capital and reserve funds formed by the enterprise contains the following lines:

- code 1310 designates a group of articles for accounting of authorized capital;

- code 1320 is represented by the size of the company’s own shares, which were purchased from shareholders during the reporting period;

- 1340 – this line indicates information based on the results of the revaluation of assets with a long period of operation (non-current assets);

- 1350 – column to reflect the amount of additional capital without taking into account revaluation;

- in line 1360 enter data on the amount of reserve capital;

- in cell 1370 the amount of retained profit is entered, and in its absence - uncovered losses.

The company can provide explanations for different types of capital. The list of indicators that need clarification and the degree of detail of the enterprise are determined independently.

For long-term liabilities of business entities, the following categories of indicators are grouped in the liabilities side of the balance sheet:

- borrowed resources that were registered by the enterprise (line 1410) - it is necessary to decipher their composition in the explanations to the balance sheet form;

- the amount of deferred tax liabilities corresponds to the credit balance in account 77 and is given as one number in column 1420;

- 1430 – line in which all estimated liabilities must be reflected;

- 1450 - this line summarizes other types of obligations that have signs of long-term duration, but are not included in other articles of the section.

For all types of long-term liabilities, a total is summed up and the result is entered in line 1400.

Current liabilities in the balance sheet are divided into 5 groups of indicators:

- a separate line is allocated for borrowed funds - the amount is taken from the credit balance of account 66, the data is indicated in balance sheet line 1510;

- accounts payable with a maturity of less than 1 year should be shown as one amount in line 1520 (in addition, a detailed explanation of the structure of this indicator must be provided in the notes to the report);

- on line 1530 indicate income related to future periods;

- cell code 1540 is for estimated liabilities;

- The last element of the section is line 1550, which combines all types of short-term liabilities that are not reflected in other categories.

The total amount of short-term debt is given in line 1500.

Liabilities are divided into short-term and long-term according to the duration of their full repayment: if the debt must be closed in a period of less than 12 months, then it is short-term. Provided that the loan can be repaid over a period of 1 year or longer, it is classified as long-term.

Read also

30.06.2018

Balance sheet liability structure

An analysis of its property status can be considered a preliminary stage in obtaining more complete information about the financial condition of a company. The value expression of a company's property gives an idea of its property potential (assets).

This characteristic must be commensurate with the size of the sources (capital and liabilities), which gives the first idea of the financial condition of the organization.

The obvious fact is that all this information is presented in the balance sheet and, therefore, it is the basic form used to assess the property potential of the company.

Let us recall that the interpretation of assets enshrined in IFRS has now been recognized in Russia, according to which balance sheet assets represent the amount of an organization’s investments resulting from previous operations and financial transactions, and expenses incurred by it for the sake of future economic benefits, i.e. attention is focused not on the material, but on the financial nature of accounting objects. The value of assets, cleared of liabilities, is treated as capital.

The process of constructing a methodology for analyzing an organization’s property includes five successive stages:

- formulation of criteria for assessing the property structure;

- determination of indicators (basic indicators) of property valuation and key balance sheet ratios;

- analysis of the company's asset structure;

- analysis of the structure of the company's liabilities;

- assessment of the satisfaction of the balance sheet structure (compliance with the characteristics of a “good” balance sheet).

At the first stage of the analysis, it is necessary to obtain additional information about the company's assets and liabilities in order to ensure the reliability of future results.

It should be clarified what the degree of freedom of disposal of assets is, whether some of them are subject to collateral, etc. In addition, the specifics of the company’s activities may predetermine the possibility of a rapid loss of asset value (trade, food industry).

And finally, an important issue is the presence of frozen company accounts (temporarily idle money) and contingent liabilities. All these points largely determine the degree of liquidity of assets and, accordingly, influence the classification of assets according to the degree of their liquidity, carried out at each specific enterprise, as well as the value of the liquidity ratios themselves.

It is obvious that the structure of a company's property inevitably changes as a result of management decisions made and, as a consequence, business transactions carried out and reflected in accounting. But structural changes in the assets and liabilities of the balance sheet may indicate both positive changes and the presence of negative trends leading to “heavier” assets.

Thus, the main criterion for assessing changes in the structure of assets “with a plus sign” can be recognized as their mobility, in other words, an increase in the rate of asset turnover, leading to an increase in the total amount of income of the company.

Analysis of the company's property position is carried out on the basis of an aggregated balance sheet using horizontal, vertical and trend methods. In the process of analysis, the composition of assets and liabilities, the dynamics of their structure are studied, and the changes that have occurred are assessed. The information base must be formed from reports taken for at least two reporting periods (credit analysts consider at least three reporting periods).

Analysis of company assets. Asset items are located in the balance sheet depending on the degree of liquidity (mobility) of the property, i.e. on how quickly a given type of asset can be converted into cash with minimal loss of value. The asset sections of the balance sheet are also built in order of liquidity (Fig. 11.1).

As can be seen from Fig. 11.1, balance sheet assets are divided into non-current and current. Let's look at each of these groups.

Non-current assets (immobilized funds) include:

- intangible assets (patents, copyrights, licenses, trademarks and other valuable but intangible assets controlled by the enterprise);

- fixed assets (buildings, equipment, land, i.e. tangible assets with a useful life of more than a year or one operating cycle);

- capital investments (construction in progress, long-term financial investments, etc.);

- Deferred tax assets.

Current assets (mobile assets) include:

- inventories of inventory items (a set of items that characterize property:

- stored for sale,

- in the process of production for sale,

- constantly spent on production;

- accounts receivable;

- short-term financial investments (in securities, investments, etc.);

- cash.

Current assets are more liquid than non-current assets. This is due to the fact that non-current assets represent that part of the enterprise’s property that is not intended for sale, but is constantly used for the production, storage and transportation of products. Current assets participate in a constant cycle of converting them into cash. In turn, they can also be divided according to the degree of liquidity: the most liquid current assets are cash, securities, then accounts receivable, inventories and expenses.

Indicators of the company's property status presented in the balance sheet:

- the cost of non-current (fixed) assets;

- the cost of working (mobile) assets, i.e. total current assets;

- cost of material working capital;

- the amount of accounts receivable (including advances issued to suppliers and contractors);

- the amount of available cash (including securities and short-term financial investments);

- cost of equity;

- the amount of borrowed capital;

- the amount of long-term loans and borrowings intended, as a rule, for the formation of fixed assets and other non-current assets;

- the amount of short-term loans and borrowings, intended, as a rule, for the formation of current assets;

- the amount of accounts payable;

- ratio of non-current and current assets;

- ratio of equity and debt capital;

- ratio of receivables and payables.

The analytical work process begins with a review of the active portion of the balance sheet. The purpose of asset analysis is quite precisely formulated in the Rules for the conduct of financial analysis by arbitration managers (approved by Decree of the Government of the Russian Federation of June 25, 2003 No. 367), which emphasizes that the analysis of assets is carried out in order to assess the effectiveness of their use, identify internal reserves to ensure the restoration of solvency, and evaluate liquidity of assets, the degree of their participation in economic turnover, identification of property and property rights acquired on obviously unfavorable conditions, assessment of the possibility of returning alienated property contributed as financial investments.

An analysis of changes in items and the structure of the balance sheet asset shows:

- the amount of current and non-current assets, changes in their ratio, as well as from what sources they are financed;

- which items are growing at a faster pace and how this affects the structure of the balance sheet;

- the share of hard-to-sell assets in the balance sheet currency and its change;

- the share of assets “frozen” for a given period in inventories and receivables;

- dynamics of the most liquid assets;

- the book value of assets used in the production process, the degree of depreciation of fixed assets, the presence of encumbered fixed assets;

- the size of investments in intangible assets;

- the presence of losses and other “sick” items in the balance sheet;

- efficiency and feasibility of long-term financial investments;

- the amount of inventory that can be sold without damaging the production process;

- share of doubtful debts in accounts receivable;

- dynamic relationships: growth rates of receivables and payables, equity and borrowed capital.

Next, changes are analyzed for each item of current balance sheet assets as the most mobile part of capital.

Did not you find what you were looking for?

Teachers rush to help

Diploma

Tests

Coursework

Abstracts

In general, an assessment should be made of the rationality of the structure of attracting and placing funds in the balance sheet asset. Each analyst, having carried out a horizontal and vertical analysis of the balance sheet, comparing the reporting data with previous periods, with industry indicators, will be able to assess the company’s property position and identify existing problems. It may be necessary to use the so-called lightweight asset model in order to speed up their turnover, clearing the balance sheet of illiquid assets, inefficiently used assets, etc.

Analysis of the company's liabilities (capital). The liabilities side of the balance sheet reflects the sources of funds available to the enterprise. All sources are grouped for a specific date according to their affiliation and purpose. The financial condition of an organization largely depends on what funds it has at its disposal and where they are invested.

Analysis of the passive part of the balance sheet shows the amount of funds (capital) invested in the economic activities of the enterprise, and the degree of participation of its various parts in the creation of the enterprise's property.

In foreign practice, there is a slightly different interpretation of the essence of the liability side of the balance sheet as an obligation for the values received or claims for the resources (assets) received by the company.

The above definitions do not contradict each other, but in the modern accounting concept the latter is preferable.

Balance sheet liabilities are divided into equity and borrowed capital (Fig. 11.2).

For analytical studies and assessment of the liability structure, all liabilities are grouped according to the following criteria.

Legal affiliation:

- obligations to the owners of the enterprise (equity capital);

- liabilities to third parties (borrowed capital).

Urgency of return:

- durable goods;

- short-term use items.

Obligations to third parties have different repayment periods: less than one year - short-term, more than one year - long-term.

When analyzing the balance sheet, it is necessary to take into account the possibility of biased reflection of information in conditions of inflation at a certain time interval.

An analysis of liabilities is carried out in order to determine the degree of dependence of the company on borrowed funds, identify reserves to ensure the restoration of solvency, obligations that can be disputed or terminated, and assess the optimality of the capital structure.

An analysis of changes in items and the structure of the balance sheet liabilities shows:

- the total amount of capital the company has and its change over time;

- absolute amounts of growth and growth rates of equity and debt capital;

- the size and growth rate of the main elements of equity capital: authorized capital, reserves, additional capital, retained earnings;

- ratio of equity and debt capital;

- the share of short-term loans and accounts payable in current liabilities;

- the amount of mandatory payments within the total amount of accounts payable;

- the size of sustainable liabilities, the share of long-term liabilities in their composition.

In the process of analyzing the company's liabilities, it is necessary to study changes in their composition and structure, and evaluate these changes. This assessment will vary depending on the position of the user of the information: for an investor and a creditor, a situation seems more reliable when the share of equity capital is equal to or greater than 50% (in this case, situations that are an exception to the rule are not considered). Equity capital is the basis of the company's independence, which reduces the financial risks of creditors and investors. The company is interested in attracting borrowed funds. If it is able to provide a rate of return on invested capital higher than the rate on loans, then when attracting borrowed funds there is the possibility of a significant increase in the return on equity (financial leverage effect). Therefore, attracting borrowed funds as a source of financing the company’s activities is a normal phenomenon; it is only important to ensure the optimal ratio of equity and debt capital in order to remain within the acceptable level of risk.

In connection with the above, serious attention should be paid to the analysis of short-term liabilities, in particular accounts payable, and its structure. The presence of unjustified debt on mandatory payments to the budget, wages and other obligations, the occurrence of which can be disputed, predetermines a serious deterioration in the financial condition of the company as a result of a decrease in its financial stability.

It remains to resolve the issue of choosing a criterion for assessing changes in the structure of the company’s sources of financing. Most Russian analysts agree that the rate of return on equity (return on equity, ROE) can be used as such a criterion. The growth of this indicator is evidence of positive changes in the structure of the company's liabilities.

Thus, the analysis of balance sheet liabilities serves as a tool for assessing the rationality of forming sources of financing for the company’s activities and its financial stability.

Here are some signs of a “good” balance sheet (trends are assessed based on the results of several reporting periods):

- growth of net assets and working capital;

- no losses;

- compliance of the ratio of non-current and current assets with the specifics of the industry;

- excess of the growth rate of equity capital over the rate

- debt growth;

- balancing the turnover rate of receivables and payables;

- excess of current assets over current liabilities;

- Exceeding the growth rate of revenue over the growth rate of borrowed capital.

Based on the information received, managers make decisions on the management of current and non-current assets and capital, promptly identifying negative trends leading to a decrease in balance sheet liquidity and, as a consequence, a deterioration in the financial position of the company as a whole.