What are these – short-term liabilities on the balance sheet

Liabilities reflected in the balance sheet are recognized as short-term if their maturity period is more than 1 year (counting starts from the reporting date). These include accounts payable to:

Take our proprietary course on choosing stocks on the stock market → training course

- lenders, creditors;

- extra-budgetary funds and budget;

- founders of the enterprise;

- employees of the organization;

- consumers (debts on advance payments received);

- suppliers (goods, works, services).

Important! In addition to the types of accounts payable listed above, the company's short-term liabilities also include reserves for future expenses.

Debts with a short repayment period include the following components:

- debts with a maturity of no more than 1 year;

- conditional payment;

- loans on bills of exchange that must be repaid in less than a year;

- money borrowed for a long time, but part of which is required to be paid back within 12 months;

- dividends to shareholders;

- accounts payable;

- tax payments;

- lost income;

- deposits for a period of up to 1 year, subject to return;

- borrowed funds on demand.

Important! Taxes are always included in the structure of current liabilities. Tax deductions include all types of payments to the budget.

Let's consider the features that characterize short-term liabilities of enterprises:

- The total amount of debt financing significantly affects the duration of the company's production cycle. The more short-term liabilities on a company's balance sheet, the less funds it is willing to raise to pay for current expenses in the course of business activities.

- The amount of debt with a short maturity is difficult to estimate in the long term, since it is not possible to accurately calculate the amount underlying the debt obligations.

- Debts with a maturity of up to 1 year serve as a substitute for a free source of debt financing.

- The volume of short-term debts varies depending on the frequency of payments on them, and this allows you to quickly work with sources of financing during business.

- The total volume of debt obligations is often determined by the degree of success in the sale of the goods produced by the company. A company that operates actively spends money all the time and attracts new borrowed funds.

- Sometimes debts with a payment term of up to 1 year can be paid using current assets. This money is required to carry out operational activities, and in order to use it to pay off short-term debts, it must be returned to circulation within 1 year from the moment the debt was formed.

- Short-term debts in the Balance Sheet are Liabilities.

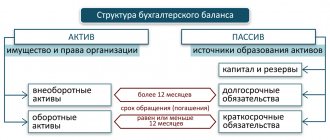

Balance sheet asset

Any property of an enterprise - machinery and equipment, real estate, financial investments, accounts receivable, etc. - are its assets. These are all things that can be converted into cash.

Assets are divided into:

- Non-negotiable

- Intangible assets

- Fixed assets

- Construction in progress

- Profitable investments in material assets

- Long-term financial investments

- Deferred tax assets

- Other noncurrent assets

- Negotiable

- Reserves

- Value added tax on purchased assets

- Accounts receivable (payments for which are expected more than 12 months after the reporting date)

- Accounts receivable (payments for which are expected within 12 months after the reporting date)

- Short-term financial investments

- Cash

- Other current assets

Short-term liabilities on the balance sheet: varieties

Debts with a short repayment period can be divided into 3 groups:

| Type of short-term liabilities | Details |

| Debts that must be paid within 1 year | The 12 month count starts from the date of reporting. |

| Operating | This may include: – tax payments, – advances received, – current payments to the budget, - rental payments, – advances paid, – debts for materials received for production activities, – accrued wages to staff (not yet paid). |

| Money to pay off debts with a repayment period of up to 1 year | This group includes: – staff vacation payments, – bonuses to salaries, – other short-term debts. |

Formation of indicators according to the lines of section V of the liabilities side of the balance sheet

The obligations of the enterprise are listed in 2 sections of the Liabilities of the Balance Sheet. The company's borrowed capital, which requires quick repayment (maximum 12 months from the date of inclusion in Liability), belongs to Section V. Let's break it down line by line:

| Line of section V “Current liabilities” of the balance sheet | Line Formation |

| 1510 "Borrowed funds" | Credit balance account 66 “Settlements on short-term loans and borrowings.” Part of the amounts from the loan account 67 “Settlements for long-term loans and borrowings” (only in the part that must be repaid within the next 1 year). |

| 1520 "Accounts payable" | The company has the right to split this line into several clarifying lines, for example: “Short-term debt to the budget”, “...suppliers”, “...employees”, etc. The total amount of short-term debts of all types (to the budget, extra-budgetary funds, individuals and legal entities). This is the sum of the credit balances of nine accounts in terms of “short” debts: 60, 62 (only in terms of short-term accounts payable for prepayments and advances received), 68-71, 73, 75 (account 2), 76. |

| 1530 "Revenue of the future periods" | To be completed only if the recognition of this accounting object is provided for by the accounting regulations of the enterprise. For commercial companies: the sum of credit balances account 98 and account 86. |

| 1540 “Estimated Liabilities” | Credit balance account 96 (except for long-term debts). |

| 1550 “Other obligations” | Other short-term debts that were not mentioned elsewhere in Section V. |

| 1500 “Total for Section V” | Sum of lines 1510-1550 (total volume of company loans). |

Important! In order to detail the indicator on line 1520, the company has the right to add decoding lines, because Accounting rules allow independent approval of details for financial reporting items.

So, the algorithm for calculating the above indicators is presented below:

| Index | Line code | Calculation formula |

| Borrowed funds | 1510 | K66+K67 (only debts with a maturity of up to 1 year) |

| Accounts payable | 1520 | K60+K62+K68+K69+K70+K71+K73+K75+K76 (only debts with a maturity of up to a year, less VAT taken into account on advances received and issued) |

| revenue of the future periods | 1530 | K98 |

| Estimated liabilities | 1540 | K96 (only estimated liabilities with fulfillment up to 1 year) |

| Other obligations | 1550 | K86 (except for long-term debts) |

Other obligations. Line 1550

This line reflects others not mentioned above and not included in other lines of section. V short-term liabilities of the organization (with a maturity period of no more than 12 months after the reporting date) (clause 19 of PBU 4/99).

It is necessary to take into account that the organization’s short-term liabilities, information about which is material, should be reflected in section. V Balance sheet separately. Therefore, significant indicators should not form the indicator of line 1550 “Other liabilities” (paragraph 2 of clause 11 of PBU 4/99, Letter of the Ministry of Finance of Russia dated January 24, 2011 N 07-02-18/01).

What may be reported as other current liabilities?

As part of other short-term liabilities, they may be reflected, provided that the indicators are not significant, for example, targeted financing received by developer organizations from investors and generating an obligation to transfer the constructed facility to them within 12 months after the reporting date. In accounting, such obligations are recorded in account 86 “Targeted financing” (clause “d”, clause 3.1.8 of the Regulations on accounting for long-term investments, Letter of the Ministry of Finance of Russia dated January 29, 2008 N 07-05-06/18, Instructions for use Chart of accounts).

If the amount of targeted financing received from investors is significant for the organization, then the organization can show it separately on a separate line in section. V “Short-term liabilities” of the Balance Sheet (clause 11 of PBU 4/99).

What accounting data is used when filling out line 1550 “Other liabilities”?

When filling out this line of the Balance Sheet, data on the credit balance of account 86 (in terms of other short-term liabilities), the credit balance of account 76 (in terms of other short-term liabilities) as of the reporting date can be used. Data on these accounts forms the indicator for line 1550 “Other liabilities” only if they are insignificant. Short-term liabilities of the organization, information about which is material, should be reflected in section. V of the Balance Sheet separately (paragraph 2 of clause 11 of PBU 4/99, Letter of the Ministry of Finance of Russia dated January 24, 2011 N 07-02-18/01).

Attention!

The balances of target financing received in foreign currency are not subject to recalculation for reflection in the financial statements. They are shown in the reporting at the exchange rate in effect on the date of their acceptance for accounting (clauses 7, 9 of PBU 3/2006).

Attention!

When reflected in reporting, offsetting between items of assets and liabilities (debit and credit balances on account 76) is not allowed (clause 34 of PBU 4/99).

Line 1550 “Other liabilities” = Credit balance of account 86 (in terms of other short-term liabilities) + Credit balance of account 76 (in terms of other short-term liabilities)

In general, the indicators on line 1550 “Other liabilities” as of December 31 of the previous year and as of December 31 of the year preceding the previous year are transferred from the Balance Sheet for the previous year.

The “Explanations” column provides an indication of the disclosure of this indicator.

Example of filling out line 1550 “Other obligations”

Indicators for account 86 in terms of short-term liabilities (there are no indicators for account 76 in terms of other short-term liabilities): rub.

| Index | As of the reporting date (December 31, 2014) |

| 1 | 2 |

| 1. Balance on the credit of account 86 (short-term obligations to investors for the transfer of construction projects) | 3 200 000 |

Fragment of the Balance Sheet for 2013

| Explanations | Indicator name | Code | As of December 31, 2013 | As of December 31, 2012 | As of December 31, 2011 |

| 1 | 2 | 3 | 4 | 5 | 6 |

| 5.3 | Obligations to investors regarding the transfer of construction projects | 1545 | 2800 | 3844 | 1600 |

| Other obligations | 1550 | — | — | — |

Solution

The amount of short-term liabilities, representing debt to investors for the transfer of construction projects, is:

as of December 31, 2014 - 3,200 thousand rubles;

as of December 31, 2013 - 2800 thousand rubles;

as of December 31, 2012 - 3844 thousand rubles.

These indicators are recognized by the organization as significant and are reflected separately in section. V Balance Sheet.

There are no other current liabilities as of December 31, 2014, December 31, 2013 and December 31, 2012.

A fragment of the Balance Sheet will look like this.

| Explanations | Indicator name | Code | As of December 31, 2014 | As of December 31, 2013 | As of December 31, 2012 |

| 1 | 2 | 3 | 4 | 5 | 6 |

| 5.3 | Obligations to investors regarding the transfer of construction projects | 1545 | 3200 | 2800 | 3844 |

| Other obligations | 1550 | — | — | — |

How to calculate the amount of current liabilities of an enterprise

Now that we know what data is reflected in the lines under code 1510-1550, we can move on to the algorithm for calculating the value of the enterprise’s current liabilities. Knowing the volume of total debt with a maturity of less than a year is important for assessing the solvency of a company :

- if it turns out that the company is unable to cope with the repayment of short-term (current) obligations, then it can be considered insolvent;

- the lower the indicator of short-term liabilities, the higher the solvency and liquidity of the organization.

So, below is a diagram for calculating the amount of short-term (current) liabilities of the company:

How do short-term liabilities appear on the balance sheet?

Obligations with a short period of fulfillment arise in the balance sheet for the reason that the accountant cannot predict the amount of income for future periods, as well as the amount of projected losses . For example, due to a man-made disaster, production disruptions and, accordingly, monetary losses may occur. The probability of such events can be assessed as small, medium or large.

Company accountants divide short-term debts into 2 groups:

- Precisely definable . These are payments planned for the future and subject to precise calculation (thanks to a calculation algorithm in a legislative act or the presence of an exact amount in an agreement with the borrower). If you have such debts, you should always check your capital to see if you have the means to pay them. Examples: dividends, bills, bills, bank loans.

- Calculated . Such obligations include debts, the amount of which cannot be determined until the payment date. And since the settlement date will come in any case, the accountant is required to accurately determine the amount to be transferred to the borrower. Examples: income tax, property tax, warranty claims, vacation pay.

Conclusions about what a change in indicator means

If the indicator is higher than normal

Not standardized

If the indicator is below normal

Not standardized

If the indicator increases

Usually a positive factor

If the indicator decreases

Usually a negative factor

Notes

The indicator in the article is considered from the point of view not of accounting, but of financial management. Therefore, sometimes it can be defined differently. It depends on the author's approach.

In most cases, universities accept any definition option, since deviations according to different approaches and formulas are usually within a maximum of a few percent.

The indicator is considered in the main free online financial analysis service and some other services

If you need conclusions after calculating the indicators, please look at this article: conclusions from financial analysis

If you see any inaccuracy or typo, please also indicate this in the comment. I try to write as simply as possible, but if something is still not clear, questions and clarifications can be written in the comments to any article on the site.

Best regards, Alexander Krylov,

The financial analysis:

- Other liabilities 1450 Definition Other liabilities 1450 are other liabilities of the organization, the maturity of which exceeds 12 months, which are not included in other groups of the 4th section of the balance sheet. Their presence...

- Estimated liabilities 1430 Definition Estimated liabilities 1430 are estimated liabilities, the expected fulfillment period of which exceeds 12 months. Despite not the simplest definition, in fact, estimated liabilities are...

- Reserves for future expenses and payments (or estimated liabilities) 1540 Definition Reserves for future expenses and payments (or estimated liabilities) 1540 are estimated liabilities, the estimated period of fulfillment of which does not exceed 12 months Despite not ...

- TOTAL for section V 1500 Definition of TOTAL for section V 1500 is the sum of indicators for lines with codes 1510 - 1550 - the total amount of short-term liabilities of the organization: 1510 “Borrowed funds” ...

- Borrowed funds 1510 Definition Borrowed funds 1510 are short-term (the repayment period of which does not exceed 12 months) loans and borrowings received by the organization. They may include...

- Deferred tax liability 1420 Definition Deferred tax liability 1420 is a liability in the form of a portion of deferred income taxes that will result in an increase in income taxes in one or...

- Accounts payable 1520 Definition Accounts payable 1520 is an organization's short-term accounts payable, the repayment period of which does not exceed 12 months. This indicator is important because if there is overdue debt...

- Other current assets 1260 Definition Other current assets 1260 are other current assets that are not reflected in other lines of Section II of the balance sheet: the cost of missing or damaged material...

- Deferred income 1530 Definition Deferred income 1530 is deferred income received in the reporting period, but relating to the following reporting periods: amounts of budget funds for financing capital...

- Deferred tax assets 1180 Definition Deferred tax assets 1180 are an asset that will reduce income taxes in future periods, thereby increasing after-tax profits. The presence of such an asset...

Answers to frequently asked questions on the topic “Current liabilities on the balance sheet”

Question: Do budgetary commercial organizations fill in line 1530 of Section V of the balance sheet if the enterprise has short-term liabilities?

Answer: No. If a commercial enterprise is financed from the budget, the funds allocated to it, which will be spent on the purchase of inventories or non-current assets, must be reflected in deferred income. If funds remain unclaimed (remains), they will be taken into account in the same way. Therefore, line 1530 is not filled in.

Question: What short-term liabilities of an enterprise can be reflected in line 1550 “Other liabilities”?

Answer: These may be amounts of value added tax (VAT) that were taken for deduction at the time of payment of the advance/prepayment, and which now need to be restored and transferred to the budget at the time of actual receipt of products, services, and works. Such funds are usually accepted for accounting on account 76. It may also be amounts of targeted financing that were received by the developer, and which now oblige him to deliver the completed construction project within 1 year from the reporting date (finances are taken into account on account 86)

3.1.5.3. Line 1530 “Deferred income”

This line reflects income from future periods, i.e. income (including other income) received in the reporting period, but relating to the following reporting periods (clause 20 of PBU 9/99).

3.1.5.3.1. What may be reflected in reporting

as part of deferred income

Until 2011, organizations reflected the following amounts as part of deferred income (Instructions for using the Chart of Accounts (explanations to account 98 “Deferred Income”), clause 9 of PBU 13/2000, clause 4 of the Instructions for reflecting in accounting transactions leasing agreement, clause 81 of the Regulations on accounting and financial reporting):

— payment for monthly (quarterly) travel tickets;

— subscription fee;

— one-time (lump-sum) payments for granting the right to use intellectual property;

— the value of assets received by the organization free of charge;

— the amount of budget funds allocated by a commercial organization to finance expenses;

— upcoming receipts for shortfalls identified in the reporting period for previous reporting years;

- the difference between the amount recovered from the guilty parties for missing material and other assets and their value listed in the organization’s accounting records;

- the difference between the total amount of lease payments under the leasing agreement and the cost of the leased property (if the organization, when recording transactions under a leasing agreement, is guided by the Instructions for reflecting transactions under a leasing agreement in accounting);

— a positive difference between the placement price of bonds and their nominal value (Instructions for using the Chart of Accounts (explanations for accounts 66 and 67));

- other income received in the reporting period, but relating to the following reporting periods.

The deferred income listed above was accounted for in accounting on account 98 “Deferred income” (in the corresponding sub-accounts).

Note that if an organization received rent in advance, then until 2011 the amount received was recognized by it as accounts payable, and not as part of deferred income (paragraph 7, 8, paragraph 12 of PBU 9/99). As a rule, amounts received under continuing contracts that do not provide for recalculations depending on the fact of provision of services were taken into account as deferred income.

From 01/01/2011, clause 81 of the Regulations on Accounting and Financial Reporting, which contained the definition of future income, became invalid (clause 19, clause 1 of Order of the Ministry of Finance of Russia dated December 24, 2010 N 186n). At the same time, the Instructions for using the Chart of Accounts have not changed; the concept of deferred income continues to be used, for example, in PBU 13/2000, Instructions for reflecting transactions under a leasing agreement in accounting.

It should be noted that the Instructions for the application of the Chart of Accounts only establish uniform approaches to the application of the Chart of Accounts for accounting the financial and economic activities of organizations and reflecting the facts of economic activities on the accounting accounts. The principles, rules and methods of accounting by organizations for individual assets, liabilities, financial, business transactions, etc., including recognition, assessment, grouping, are established by PBU, guidelines and other regulations on accounting issues (paragraph 1, 2 Preamble to the Instructions for using the Chart of Accounts). According to Letter of the Ministry of Finance of Russia dated March 15, 2001 N 16-00-13/05, the Chart of Accounts, unlike the PBU, is a document that does not have a regulatory nature. In this regard, in the financial statements for 2011, it is reasonable to reflect on line 1530 “Deferred income” only:

— budget funds allocated by a commercial organization to finance expenses (clause 9 of PBU 13/2000);

— the difference between the total amount of leasing payments under the leasing agreement and the cost of the leased property (clause 4 of the Instructions on reflecting transactions under the leasing agreement in accounting).

The indicated amounts are reflected in the credit of account 98 “Deferred income”. Other amounts recorded in account 98 are credited to the corresponding settlement accounts or are included in the organization’s income by the accounting entry dated December 31, 2010.

In addition, as part of deferred income, the balances of targeted budget financing provided to the organization that were not used at the end of the reporting period are shown, which are taken into account in accounting in account 86 “Targeted financing” (clause 20 of PBU 13/2000, Instructions for using the Chart of Accounts ). In a similar manner, in our opinion, targeted funding received in the form of grants, technical assistance (assistance), etc. is reflected in the reporting.

Attention!

If the amount of unused funds from targeted budget financing is significant for the organization, then the organization can show it separately on a separate line in section. V “Short-term liabilities” of the Balance Sheet (clause 20 PBU 13/2000, clause 11 PBU 4/99).

FOR MORE on this issue see:

Section “Accounting for target financing (account 86)” of the Guide to IB “Correspondence of accounts”

Section “Accounting for deferred income (account 98)” of the Guide to Information Security “Correspondence of Accounts”

3.1.5.3.2. What accounting data is used?

when filling out line 1530 “Deferred income”

When filling out this line of the Balance Sheet, organizations that are recipients of government subsidies, as well as leasing organizations, use data on the credit balance on account 98 (which reflects budget funds aimed at financing expenses, or the difference between the total amount of leasing payments under the leasing agreement and the cost of the leasing property) and on the credit balance of account 86 (in terms of targeted budget financing and targeted financing funds received in the form of grants, technical assistance (assistance), etc.) as of the reporting date.

Attention!

The balances of target financing received in foreign currency are not subject to recalculation for reflection in the financial statements. They are shown in the reporting at the exchange rate in effect on the date of their acceptance for accounting (clauses 7, 9 of PBU 3/2006).

Line 1530 “Deferred income” of the Balance Sheet = Credit balance on account 98 + Credit balance on account 86 in terms of targeted budget financing, grants, technical assistance, etc.

In general, the indicators on line 1530 “Deferred income” as of December 31 of the previous year and as of December 31 of the year preceding the previous one are transferred from the Balance Sheets compiled as of these reporting dates.

When preparing financial statements in 2011, the indicators in column 4 of line 640 “Deferred income” of the Balance Sheets for 2010 and 2009 are adjusted. To ensure comparability of reporting data on line 1530 “Deferred income” as of December 31, 2010 and as of December 31, 2009, only the amounts of subsidies aimed at financing expenses and the difference between the total amount of leasing payments under the leasing agreement and the cost of the leased property are indicated (Clause 10 PBU 4/99). If the indicators of line 640 in the Balance Sheets for 2010 and 2009. included other amounts, then these amounts are reflected in the Balance Sheet for the reporting periods of 2011, for example, on line 1520 “Accounts payable” or line 1370 “Retained earnings (uncovered loss)”. This adjustment is due to a change in the accounting policy of the organization associated with a change in the regulatory legal act on accounting (clauses 10, 14, 15 of PBU 1/2008).

EXAMPLE 5.3

Indicators for accounts 98 and 86 in terms of targeted budget financing (grants, technical assistance and other targeted financing are absent).

rub.

| At the reporting date | |

| 1 | 2 |

| 1. On the credit of account 98 (the amount of government subsidies directed by the organization to finance expenses) | 2 061 828 |

| 2. On the credit of account 86 in terms of targeted budget financing | 800 000 |

Indicators of the Balance Sheets for 2009 and 2010 (line 640 indicator forms only the amount of government subsidies directed by the organization to finance expenses).

thousand roubles.

| Column 4 “At the end of the reporting period” on line 640 “Deferred income” of the Balance Sheet for 2009. | 2710 |

| Column 4 “At the end of the reporting period” on line 640 “Deferred income” of the Balance Sheet for 2010. | 2786 |

Solution

Since the indicators in line 640 of the Balance Sheet for 2009 and 2010 form only the amounts of government subsidies aimed at financing expenses, these indicators are transferred to the corresponding columns of line 1530 of the Balance Sheet in 2011 without adjustment.

The amount of deferred income is:

as of the reporting date - 2862 thousand rubles. (RUB 2,061,828 + RUB 800,000);

as of December 31, 2010 - 2,786 thousand rubles;

as of December 31, 2009 - 2,710 thousand rubles.

A fragment of the Balance Sheet in Example 5.3 will look like this.