The essence of the Unified Agricultural Tax tax 2021

The Unified Agricultural Tax system itself is one of 5 special tax regimes that are available to small businesses. Let us consider the very essence of the Unified Agricultural Tax special regime.

From the name it is clear that this tax relates to agriculture.

By choosing the Unified Agricultural Tax tax in 2021, you automatically get rid of taxes such as VAT and income and property taxes that are on the OSNO (general taxation system).

Agricultural activities for which the Unified Agricultural Tax can be applied:

- Plant growing;

- Livestock;

- Poultry farming;

- Fish farming.

In other words, the special tax regime of the Unified Agricultural Tax replaces the OSNO tax. And in this case it is necessary to report specifically on the Unified Agricultural Tax.

The Unified Agricultural Tax can be applied in conjunction with the UTII or PSN tax. In this case there will be separate taxation.

Despite the fact that it is allowed to use special UTII and PSN regimes with the Unified Agricultural Tax, the share of agricultural business must be at least 70% of the total business.

Transition to Unified Agricultural Tax

When initially registering an individual entrepreneur or organization, it is required to submit a notification about the use of the tax regime within thirty days. Otherwise OSNO will be installed automatically. The transition is carried out once a year.

In an existing business, the transition occurs from the beginning of the year. However, notification must be submitted by December 31st. Documents are submitted in two copies to the tax office at the place of registration.

The transition to the Unified Agricultural Tax is done by submitting an application to the Federal Tax Service

How to switch to the Unified Agricultural Tax in 2021

Switch to the Unified Agricultural Tax in 2021; you can submit a notice of application of the Unified Agricultural Tax until December 31, 2017, and in this case you can begin to apply the Unified Agricultural Tax from 01/01/2018.

I recommend submitting the notification itself somewhere on December 15, 2017, in order to be sure to receive permission to use the Unified Agricultural Tax in 2018. You do not have to wait until the last day, since you may not have time to register and you will not receive the right to apply the Unified Agricultural Tax.

Also, when submitting a notification about the transition to the unified agricultural tax, it is necessary to indicate the share of the agricultural business, as I said before - at least 70%.

Also, organizations and entrepreneurs who have just registered can switch to the Unified Agricultural Tax tax in 2021 - they are given 30 days to do this.

If organizations and entrepreneurs do not provide notification within the established time frame, then they do not have the right to apply the Unified Agricultural Tax.

When the Unified Agricultural Tax tax cannot be applied

- If the tax inspectorate refuses the right to apply a single agricultural tax;

- When the deadlines for submitting a notice of transition to the unified agricultural tax are violated;

- In the event that, at the end of the period, the taxpayer ceases to comply with the requirements of the special regime of the Unified Agricultural Tax.

If a taxpayer, being in the special unified agricultural tax regime in 2021, ceases to meet the requirements for which the unified agricultural tax is allowed to be applied, then he must notify the tax authorities about this within 15 days.

Who can apply the special regime of Unified Agricultural Tax in 2017

Taxpayers of the special regime of the Unified Agricultural Tax can be entrepreneurs, organizations and peasant farms that are agricultural producers.

Producers of agricultural products can be:

- Peasant farms (peasant farms);

- IP (individual entrepreneurs);

- LLC (limited liability company).

Regardless of the chosen form of ownership: peasant farm, individual entrepreneur or LLC, they must meet the following requirements:

- Produce agricultural products;

- Carry out primary processing and subsequent industrial processing of agricultural products;

- Sale of agricultural products.

All these requirements must be met simultaneously, that is, for example: you cannot simply sell agricultural products on the Unified Agricultural Tax.

All requirements are complex in nature and if they are violated, the entrepreneur is deprived of the right to apply the Unified Agricultural Tax.

Further, as I mentioned earlier, the share of agricultural business turnover should not be less than 70% of the total turnover of the organization.

Fishery organizations also have the right to apply taxation under the Unified Agricultural Tax.

Mandatory conditions for the transition to the Unified Agricultural Tax in 2021:

- The average number of employees should not exceed 300 people;

- 70% - the total turnover from the organization's activities.

The following organizations cannot apply the Unified Agricultural Tax:

- State, budgetary, as well as autonomous institutions;

- Organizations producing excisable goods;

- Organizations involved in the gaming business.

Calculation of the single agricultural tax: example

The income of Selskokhozyaystvennik LLC, which was credited to its current account based on the results of the first six months of 2021, amounted to 700 thousand rubles. Paid and actually incurred expenses included in the legislative list - 400 thousand rubles.

For the full year 2021, revenues amounted to 1.5 million rubles, expenses – 800 thousand rubles. In 2015, the company suffered a loss equal to 200 thousand rubles.

To calculate the amount of the advance tax payment, we substitute the semi-annual values into the formula:

Tax = (700–400)* 0.06 = 18 thousand rubles.

Agricultural tax based on the results of a fully worked year will be calculated using the formula:

Tax = (1,500,000 – 800,000 – 200,000)* 0.06 – 18,000 = 12,000 rub.

The amount of 18,000 rubles is paid to the budget no later than July 25, 12,000 rubles - until March 31 of the next year.

Tax rate of the Unified Agricultural Tax

Let's look at what the Unified Agricultural Tax rates are:

- Standard tax rate for Unified Agricultural Tax in Russia = 6%;

- Unified agricultural tax rate for Crimea and Sevastopol from 2021 to 2021 = 4%.

How to calculate the amount of the Unified Agricultural Tax in 2021

Let's look at how to calculate the Unified Agricultural Tax:

Unified Agricultural Tax for Russia = tax base * 6%;

Unified agricultural tax for Crimea and Sevastopol = tax base * 4%.

Tax return of the Unified Agricultural Tax

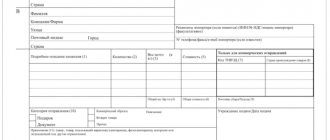

Field " TIN

" Individual entrepreneurs and organizations indicate the TIN in accordance with the received certificate of registration with the tax authority. For organizations, the TIN consists of 10 digits, so when filling it out, you must put dashes in the last 2 cells (for example, “5004002010—”).

Field " Checkpoint"

" The IP field of the checkpoint is not filled in. Organizations indicate the checkpoint that was received at the Federal Tax Service at the location of the organization.

Field " Adjustment number"

"

It is entered: “ 0—

” (if the declaration is submitted for the first time for the tax period (quarter), “

1—

” (if this is the first correction), “

2—

” (if the second), etc.

Field “ Tax period (code)

"

The code of the tax period for which the declaration is submitted is indicated ( see Appendix 1

).

Field " Reporting year"

" This field indicates the year for which the declaration is being submitted.

Field “ Submitted to the tax authority (code)

" The code of the tax authority to which the declaration is submitted is indicated. You can find out your Federal Tax Service code using this service.

Field “ at place of registration (code)

"

The code for the place where the declaration is submitted to the tax authority is indicated ( see Appendix 2

).

Field " Taxpayer"

" Individual entrepreneurs need to fill out their last name, first name and patronymic, line by line. Organizations write their full name in accordance with their constituent documents.

Field “ Code of the type of economic activity according to the OKVED classifier

" This field indicates the activity code of the Unified Agricultural Tax in accordance with the new edition of the OKVED directory. Individual entrepreneurs and LLCs can also find their activity codes in an extract from the Unified State Register of Individual Entrepreneurs or the Unified State Register of Legal Entities, respectively.

note

, when submitting the Unified Agricultural Tax declaration for 2021, this code must be indicated in accordance with the new edition of OKVED. You can transfer a code from the old edition to the new one using our service for comparing OKVED codes.

Field “ Form of reorganization, liquidation (code)

" and the field "

INN/KPP of the reorganized organization

".

These fields are filled in only by organizations in the event of their reorganization or liquidation ( see Appendix 3

).

Field " Contact phone number"

" Specified in any format (for example, “+74950001122”).

Field " On pages

" This field indicates the number of pages that make up the declaration (for example, “004”).

Field “ with attached supporting documents or copies thereof

" Here is the number of sheets of documents that are attached to the declaration (for example, a power of attorney from a representative). If there are no such documents, then put dashes.

Block “ Power of attorney and completeness of information specified in this declaration

"

In the first field you must indicate: “ 1

” (if the authenticity of the declaration is confirmed by an individual entrepreneur or the head of an organization), “

2

” (if a representative of the taxpayer).

In the remaining fields of this block:

- If the declaration is submitted by an individual entrepreneur, then the field “last name, first name, patronymic in full” is not filled in. The entrepreneur only needs to sign and date the declaration.

- If the declaration is submitted by an organization, then it is necessary to indicate the name of the manager line by line in the field “last name, first name, patronymic in full.” After which the manager must sign and date the declaration.

- If the declaration is submitted by a representative (individual), then it is necessary to indicate the full name of the representative line by line in the field “last name, first name, patronymic in full.” After this, the representative must sign, date the declaration and indicate the name of the document confirming his authority.

- If the declaration is submitted by a representative (legal entity), then in the field “Last name, first name, patronymic in full” the full name of the authorized individual of this organization is written. After this, this individual must sign, date the declaration and indicate a document confirming his authority. The organization, in turn, fills in its name in the “organization name” field and puts a stamp (if any).

Unified agricultural tax reporting in 2021

Since the tax period for the Unified Agricultural Tax is 1 year, once a year it is necessary to submit a tax return for the Unified Agricultural Tax and prepare a KUDiR book for reporting purposes.

- For organizations (LLC) – the deadline for submitting the Unified Agricultural Tax declaration is March 31, 2018;

- For individual entrepreneurs and peasant farms, the deadline for submitting reports in the form of a Unified Agricultural Tax declaration is April 30, 2021.

That's all I wanted to tell you about the single agricultural tax in 2021.

If you have any questions, please ask them in the comments or in my VK group “ ”. Happy business to everyone! Bye!

Reporting on the unified agricultural tax

For the Unified Agricultural Tax there are 2 periods - a year (tax) and six months (reporting). At the end of the reporting period, the company or individual entrepreneur pays an advance - before July 25 of the current year, and at the end of the tax period - the remaining amount of tax according to the declaration. Submission of the declaration and final payment of the Unified Agricultural Tax must be made before March 31 of the following year.

The declaration form for the unified agricultural tax is given in the order of the Federal Tax Service dated July 28, 2014 No. MMB-7-3/ [email protected]

For information about the deadlines for submitting reports if activities at the Unified Agricultural Tax are terminated early, read the material “Deadline for submitting reports to the Unified Agricultural Tax for individual entrepreneurs for 2015–2016.”

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How to count correctly

Let's look at how to calculate the Unified Agricultural Tax correctly, since many novice entrepreneurs are constantly confused with this simple task. For this, the following formula is used: EXSN = Nbx0.06 , where Nb is the tax base. This term means the amount of income reduced by the amount of expenses, and in some cases provided for by the tax code, by the amount of loss for the previous year. It is noteworthy that if a company recorded a loss for two or more years in a row, then they sign for the tax base in the sequence of accumulation.

As you can see, there is nothing complicated in the calculation; the main thing is to choose the right numbers and data from the reporting. It should also be taken into account that, according to the law, the tax period for this term is set at one year, while the reporting period is 6 months. Payers are required to pay an advance based on the results of the past half-year (reporting period) no later than 25 days after its end (that is, from July 1 to July 25 and from January 1 to 25).

Example:

farmer Zaitsev, who grows and sells tomatoes and their products, received an income of 650 thousand rubles in the first half of 2021. At the same time, the cost of growing and selling the crop amounted to 480 thousand rubles. Zaitsev must pay an advance payment in the amount of (650,000-480,000) x 0.06 = 10,200 rubles by July 25.

The advance payment is not constant - it can be recalculated depending on changes in income and expenses in the next six months or season. During the second half of the year, Zaitsev earned 800,000 rubles, having spent 550,000. In this case, the payment will be (800,000 - 550,000) * 0.06 = 15,000, which should be paid after the new year.