Personal accounting account to reflect shortages

To record shortages in accounting, account 94 “Shortages and losses from damage to valuables” is intended (Chart of Accounts, approved by order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n).

Basic information about account 94 is presented in the figure below:

What amounts are reflected in the debit and credit of this account, see below:

What needs to be taken into account when calculating the residual value of a fixed asset (FPE), see the article “How to determine the residual value of fixed assets” .

Let's figure out how account 94 is used in business activities.

Shortages and losses from damage to valuables: count 94

The accrual of the amount of damage calculated based on the results of the inventory is reflected in account 94 “Shortages and losses”, the debit of which records the amount of the shortage, and the credit records its write-off to an established source. Depending on the type of asset that was missing, the formation of accounting entries to reflect the shortage of valuables will be different not only for the accounts involved, but also for the amounts involved in calculating the damage:

| Operations | D/t | K/t | For the amount |

| Shortage identified: | |||

| OS | 94 | 01 | residual value |

| Materials, goods, finished products in warehouse | 94 | 10, 41, 43 | production costs |

| Goods from the supplier (within the limits of loss norms) | 94 | 60 | actual losses |

| Goods from the supplier in excess of loss norms | 94 | 76 | |

| Uninstalled equipment | 94 | 07 | |

| Investments in non-current assets | 94 | 08 | |

| Money in the cash register | 94 | 50 | |

| Values lost in previous financial periods, or for assets, shortages of which are recovered at market prices (according to the rules established by the company) | 94 | 98 | market value |

The culprits have been identified: how to write off shortages identified during inventory

Regular monitoring of the availability and condition of property, carried out through an inventory, helps the company’s management:

- promptly identify shortages and damage to property;

- deal with the culprits;

- take measures to recover shortfalls from those responsible;

- write off damaged and missing material assets from accounting accounts and generate reliable information in reporting on company property;

- take measures to strengthen control over the safety of assets, increase the level of responsibility of financially responsible persons, etc.

The following articles talk about the nuances of inventory:

- “Inventory of inventories: order and nuances”;

- “Procedure for conducting an inventory of fixed assets”;

- “The procedure for carrying out a BSO inventory (nuances).”

To understand the postings for writing off shortages during inventory, we will use the conditions of the example.

After conducting an inventory at warehouse No. 3 (the financially responsible person is storekeeper N. G. Zavyalov), a shortage of goods and materials in the amount of 8,630 rubles was revealed:

| Name | Quantity | price, rub. | Cost, rub. | ||

| Cement PC-500 | 5 bags | 290,00 | 1 450,00 | ||

| Shovel with wooden handle (rail steel) | 4 pieces | 525,00 | 2 100,00 | ||

| Rack jack | 1 piece | 5 080,00 | 5 080,00 | ||

| Total amount: | 8 630,00 | ||||

Storekeeper Zavyalov N.G. agreed to voluntarily compensate for the shortage.

In the company's accounting, entries were made to write off the shortage to the guilty party:

| Accounting entries | Amount, rub. | Contents of operation | |

| Debit | Credit | ||

| 94 | 10 | 8 630,00 | The cost of missing valuables is transferred to the shortage account |

| 73 | 94 | 8 630,00 | The shortage is attributed to the person at fault |

| 70 | 73 | 8 630,00 | The shortage is withheld from the salary of the financially responsible person at his request |

How the presence of natural loss norms affects the procedure for writing off shortages is described here .

Important to consider! Recommendation from ConsultantPlus: Evaluate written-off inventory items in the manner established by the accounting policy.

In the debit of account 94, also write off the amount of deviations, including transport... (read more).

The shortage was identified before the goods were registered

If the organization reveals a shortfall in delivery (damage) when accepting goods (i.e. before registering the goods), then there is no need to conduct an inventory. To document the fact of such shortage (damage) by trade organizations, Resolution of the State Statistics Committee of Russia dated December 25, 1998 No. 132 provides standard forms:

No. TORG-2 (if goods of Russian origin are received);

No. TORG-3 (if imported goods are received).

In some industries, instead of form No. TORG-2 (No. TORG-3), other acts may be used. For example, in relation to medical goods in pharmacies - an act in form No. A-1.2 (Section 4 of the Methodological Recommendations approved by the Ministry of Health of Russia on May 14, 1998 No. 98/124).

Documents that record the fact of shortage or damage are the basis for filing a claim with the supplier (Articles 518, 519 of the Civil Code of the Russian Federation).

If the goods were transported by a specialized transport organization, to submit claims to the carrier you need to use the report form valid for transport. Such rules are established in the instructions approved by Decree of the State Statistics Committee of Russia dated December 25, 1998 No. 132. For example, when transporting by rail, a commercial act is drawn up (clause 2.1 of the Rules approved by Order of the Ministry of Railways of Russia dated June 18, 2003 No. 45). Its form was approved by Order No. 45 of the Ministry of Railways of Russia dated June 18, 2003. However, if a standard document form for reflecting losses during transportation by appropriate transport is not established, acts in forms No. TORG-2 and No. TORG-3 can be used to make claims to the carrier. In the absence of standard forms to reflect the fact of shortage (damage to goods) identified during acceptance of goods, the organization can draw up a document in any form, reflecting all the necessary details (Part 2 of Article 9 of the Law of December 6, 2011 No. 402-FZ ). For more information about this, see How to register and record a claim against a counterparty.

There is no one to blame for the shortage: we are sorting out the wiring

Situations when there is no one to blame for a shortage often arise. Company assets can be lost as a result of force majeure (flood, drought, earthquake) or stolen by thieves who cleverly cover their tracks.

First, the property owner must understand the true reasons for the shortage and take measures to find the perpetrators, as well as evidence of their involvement in the loss of valuables. To do this, the company can conduct an internal investigation itself or file a complaint with the police.

Let's look at an example to see what kind of postings are used when writing off a shortage if the culprit is not identified.

Construction materials worth RUB 2,654,399 disappeared from the construction site. 38 kopecks In the “Construction City” accounting, after conducting an inventory and completing the necessary documents, the following entry was made:

| Accounting entries | Amount, rub. | Contents of operation | |

| Debit | Credit | ||

| 94 | 10 | 2 654 399,38 | There is a shortage of building materials |

The company's management contacted the police to report the theft. As a result of the investigation, the culprits of the theft were not identified. After receiving from the internal affairs bodies a document on the suspension of the case of theft of valuables due to the absence of perpetrators, the following entries were made in the accounting records of Stroyka-Gorod LLC:

| Accounting entries | Amount, rub. | Contents of operation | |

| Debit | Credit | ||

| 91.2 | 94 | 2 654 399,38 | The loss from the shortage was written off as other expenses due to the absence of the perpetrators |

The same entry is made in accounting if the guilt of the financially responsible person in damage or loss of valuables is not proven. The basis may be an acquittal by the court (clause 5.2 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia dated June 13, 1995 No. 49).

Learn about the nuances of using account 91 from this material.

We write off the shortage

If any fact of theft, abuse or damage to property is detected, an inventory of valuables must be carried out (clause 2 of Article 12 of Law No. 129-FZ of November 21, 1996 (hereinafter referred to as Law No. 129-FZ)). Since only an inventory will confirm the correctness and validity of the listed amount of debt for shortages.

Inventory procedure

The procedure for conducting an inventory of property and recording its results is prescribed in the “Guidelines for the inventory of property and financial obligations” established by Order of the Ministry of Finance dated June 13, 1995 No. 49 (hereinafter referred to as the Guidelines). Inventory results are reflected using unified forms approved by State Statistics Committee Resolution No. 88 dated August 18, 1998 “On approval of unified forms of primary accounting documentation for recording cash transactions and accounting for inventory results.”

Briefly, the inventory procedure is as follows:

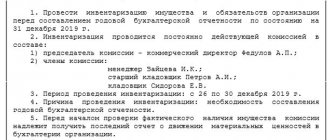

- an order to conduct an inventory is approved, indicating the date, composition of the commission and property for inspection;

- the commission receives the latest incoming and outgoing documents at the time of inventory;

- accounting determines balances of valuables based on accounting data;

- financially responsible persons give receipts;

- the inventory commission determines the actual availability of property;

- inventory records are drawn up;

- inventory results are checked against accounting data;

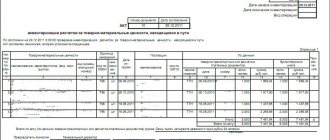

- For property, during the inventory of which deviations from accounting data are identified, comparison statements are compiled.

Note that in the matching statements (see Example 1) the amounts of shortfalls are indicated in accordance with their assessment in accounting (clause 4.1 of the Methodological Instructions). At the same time, separate matching statements are compiled for values that do not belong to the organization, but are registered (those in safekeeping, rented, received for processing).

Example 1

Box office subtleties

The cash register audit is carried out in accordance with the Procedure for conducting cash transactions in the Russian Federation, approved by decision of the Board of Directors of the Central Bank of Russia on September 22, 1993 No. 40 (hereinafter referred to as the Procedure for conducting cash transactions).

In this case, by order of the head of the enterprise, a commission is appointed, which subsequently draws up an audit report (see Example 2). Inventory consists of a complete recalculation of cash and checking other valuables in the cash register. The cash balance is verified with the accounting data in the enterprise's cash book (clause 37 of the Procedure for conducting cash transactions).

Example 2.

As a rule, strict reporting forms (clause 20 of Government Decree No. 171 of March 31, 2005) and securities (clause 3.11 of the Methodological Instructions) are inventoried with a check of cash and cash documents in the cash register. At the same time, an inventory of securities is carried out by individual issuers, indicating in the act the name, series, number, nominal and actual value, maturity dates and total amount (clause 3.12 of the Methodological Instructions). In turn, verification of the actual availability of strict reporting document forms is carried out by type of form, taking into account the starting and ending numbers (clause 3.41 of the Methodological Instructions) (see Example 2).

The results of the inventory must be reflected in the accounting and reporting of the month in which the inventory was completed (clause 5.5 of the Guidelines). To summarize information on the amounts of shortages and losses from damage to material and other assets (including cash), account 94 “Shortages and losses from damage to assets” is intended:

Debit 94 Credit 01 (03, 07, 08, 10, 11, 41, 43, 50, 60) – the amount of the deficiency is reflected.

Natural decline

Norms

Norms of natural loss are developed taking into account the technological conditions of their storage and transportation, climatic and seasonal factors (1). In the future, the norms are subject to revision at least once every 5 years (clause 1 of Government Resolution No. 814 of November 12, 2002).

Note that at present all non-cancelled norms of natural loss are in force (letter of the Ministry of Finance dated November 8, 2007 No. 03-03-06/1/783).

Re-grading

In accounting, inventory shortages within the limits of natural loss norms are determined after offsetting inventory shortages with surpluses due to re-grading. If, after offset, there is still a shortage of inventories, then the norms of natural loss are applied only by the name of the inventories for which the shortage was established (clause 30 of Order of the Ministry of Finance dated December 28, 2001 No. 119n). In this case, mutual offset of surpluses and shortages by re-grading can be allowed only as an exception for the same audited period, from the same audited person, in relation to inventory items of the same name and in identical quantities. At the same time, financially responsible persons provide the inventory commission with detailed explanations of the permitted misgrading (clause 5.3 of the Methodological Instructions).

Accounting

In accounting, the shortage of property and its damage within the limits of natural loss norms are attributed to production or distribution costs (subclause b, clause 3, article 12 of Law No. 129-FZ):

Debit 20 (23, 25, 26, 44) Credit 94 – the amount of the shortage is reflected within the limits of natural loss norms.

In tax accounting, losses from shortages or damage during storage and transportation of inventories within the limits of natural loss norms approved in the manner established by the Government are equated to material expenses (subclause 2, clause 7, article 254 of the Tax Code of the Russian Federation).

Please note that you do not have the right to attribute losses to material expenses within the limits established only by local acts of the organization (letter of the Ministry of Finance dated 04/04/2005 No. 03-03-01-04/1/146).

Technological losses

Technological losses during production or transportation are also equated to material expenses for profit tax purposes (subclause 3, clause 7, article 254 of the Tax Code of the Russian Federation).

Representatives of the Ministry of Finance in a letter dated August 29, 2007 No. 03-03-06/1/606 noted that the procedure for sectoral settlement of issues of development and approval of technological loss standards is not the subject of legislation on taxes and fees. Therefore, taxpayers have the right to determine the limit for the generation of irrevocable waste for each specific type of raw materials and materials used in production, based on the technological features of their own production cycle and the transportation process. They establish standards using technological maps, process estimates and other similar documents. Limits are developed by enterprise specialists who control the technological process and approved by persons authorized by the enterprise management.

Shortage due to theft

Material liability of employees

In accordance with Article 22 of the Labor Code, the employer has the right to hold employees financially liable in the manner prescribed by law.

The procedure for determining damage caused to the employer is as follows:

- a commission is created;

- an inventory of property is carried out;

- the causes of damage are established;

- a written explanation is required from the employee;

- if the employee refuses or evades providing an explanation, a report is drawn up.

Let us note that the financial liability of employees can be limited (within the limits of average monthly earnings) and full, individual and collective (2).

The amount of damage caused to the employer in the event of loss and damage to property is determined by actual losses, based on market prices prevailing in the area on the day the losses were caused, but not lower than the value of the property according to accounting data, taking into account the degree of depreciation of the property (Article 246 of the Labor Code of the Russian Federation ). Let us note that in cases where it is impossible to determine the day the damage was caused, the employer has the right to calculate its amount as of the day of discovery (clause 13 of the Resolution of the Plenum of the Supreme Court of November 16, 2006 No. 52, hereinafter referred to as Resolution No. 52).

The amount of damage caused, not exceeding the average monthly earnings of the guilty person, is recovered by order of the employer. The order must be drawn up within one month from the date the amount of damage is established. At the same time, voluntary compensation for losses is also possible (Article 248 of the Labor Code of the Russian Federation).

If the monthly period has expired or the employee does not agree to voluntary compensation for losses, and the amount of damage exceeds his average monthly earnings, then recovery occurs in court. Remember: the employer has the right to go to court in disputes about compensation for losses by the employee within one year from the date of discovery of the damage caused (Article 392 of the Labor Code of the Russian Federation).

Let us note that, when determining the amount of damage to be compensated for collective financial liability, the court takes into account the degree of guilt of each member of the team, the amount of official salary, the time that the employee actually worked as part of the team for the period from the last inventory to the day the damage was discovered (clause 14 of the Resolution No. 52). In this case, the methodology prescribed in the order of the USSR Ministry of Trade dated August 19, 1982 No. 169 “Instructions on the procedure for applying in state trade legislation regulating the financial liability of workers and employees for damage caused to an enterprise, institution, organization” (hereinafter - Order No. 169).

So, the amount of compensation for damage by each member of the team can be determined using the following formula (clause 7.3 of Order No. 169):

Amount of compensation for damage to a team member = Amount of damage caused by the team × Wages of a team member for the inter-inventory period / Wages of team members for the inter-inventory period based on salaries taking into account the time worked

Example 3

Based on the results of the inventory, a shortage of 5,000 rubles was discovered at Magazin LLC. The enterprise has established collective financial responsibility. A team of three people was found guilty.

The salary of each team member for the inter-inventory period was:

Antonov I.G. – 15,000 rub.,

Dubinin V.V. – 45,000 rub.,

Sergeev L.I. – 40,000 rub.

Let's calculate the amount of damages to be compensated by each member of the team:

Antonov I.G. = 5,000 rub. × 15,000 rub. / (15,000 rub. + 45,000 rub. + 40,000 rub.) = 750 rub.

Dubinin V.V. = 5,000 rub. × 45,000 rub. / (15,000 rub. + 45,000 rub. + 40,000 rub.) = 2,250 rub.

Sergeev L.I. = 5,000 rub. × 40,000 rub. / (15,000 rub. + 45,000 rub. + 40,000 rub.) = 2,000 rub.

At the same time, do not forget about the limitation on the amount of deductions from wages prescribed in Article 138 of the Labor Code. Also, deductions from payments that cannot be collected in accordance with federal law are not allowed.

Accounting

In accounting, the shortage of property and its damage in excess of the norms of natural loss is attributed to the guilty persons (subparagraph b, paragraph 3, article 12 of Law No. 129-FZ):

Debit 73 subaccount “Calculations for compensation of material damage” Credit 94 - the amount of the shortfall is attributed to the account of the guilty party.

The difference between the amount recovered from the guilty parties for missing valuables and the value listed in the organization’s accounting records is reflected in account 98 “Deferred income”:

Debit 73 subaccount “Calculations for compensation of material damage” Credit 98 - reflects the difference between the amount to be recovered from the guilty parties and the book value of the missing valuables;

Debit 98 Credit 91-1 “Other income” - reflects the write-off of the amount of the difference collected from the guilty party over the book value of the missing values.

Example 4

A shortage of goods in the amount of 10,000 rubles was discovered at Magazin LLC. (market value of the goods - 12,000 rubles). The manager of the organization was found guilty.

In accordance with the agreement between the director and the manager, the market value of the goods must be collected in equal parts within 4 months from the salary of this employee.

The following entries must be made in accounting:

Debit 94 Credit 10 – 10,000 rub. – based on the results of the inventory, the missing goods were written off;

Debit 73 Credit 94 – 10,000 rub. – the amount of the deficiency is attributed to the account of the guilty person;

Debit 73 Credit 98 – 2,000 rub. (12,000 rubles – 10,000 rubles) – reflects the difference between the amount to be recovered from the guilty parties and the book value of the missing valuables;

Monthly for 4 months:

Debit 70 Credit 73 – 3,000 rub. (RUB 12,000 / 4 months) – reflects the deduction of the amount to be collected from the employee’s salary.

Debit 98 Credit 91-1 – 500 rub. (RUB 2,000 / 4 months) – reflects the write-off of the amount of the difference collected from the guilty party over the book value of the missing valuables.

The amount of compensation for damage is recognized as non-operating income (clause 3 of Article 250 of the Tax Code of the Russian Federation). In this case, the moment of receipt of income is the date the debtor recognized the damage or the date the court decision entered into legal force (subclause 4, clause 4, article 271 of the Tax Code of the Russian Federation).

The Ministry of Finance in letter dated November 23, 2006 No. 03-03-04/1/793 noted that the amount of compensation for damage in connection with the loss of the leased asset by the lessee for profit tax purposes is included by the lessor in non-operating income.

The culprits have not been found

In accounting, the shortage of property and its damage in excess of the norms of natural loss, if the perpetrators are not identified or the court refuses to recover losses, is subject to write-off to the financial results of the organization (subparagraph b, paragraph 3, article 12 of Law No. 129-FZ).

The shortage of valuables in excess of the norms of loss and losses from damage to valuables in the absence of specific culprits, as well as the shortage of inventory items, the recovery of which was refused by the court due to the unfoundedness of the claims, is reflected as follows:

Debit 91-2 “Other expenses” Credit 94 - the amount of the shortfall is written off if the culprit was not identified or the court refused to collect.

Example 5

At LLC Standard, based on the results of the inventory, a shortage of the SBR-260/380 concrete mixer was discovered (initial cost - 25,000 rubles, depreciation - 5,000 rubles).

The culprits have not been identified.

The following entries must be made in accounting:

Debit 02 Credit 01 – 5,000 rub. – the amount of depreciation is written off;

Debit 94 Credit 01 – 20,000 rub. – the residual value of the fixed asset is written off;

Debit 91-2 Credit 94 – 20,000 rub. – the amount of the shortfall is written off in the absence of those responsible.

Losses from shortages of material assets in production and in warehouses at trading enterprises in the absence of perpetrators, as well as losses from theft, the perpetrators of which have not been identified, are equated to non-operating expenses. In this case, the fact of the absence of guilty persons must be confirmed by an authorized government body (subclause 5, clause 2, article 265 of the Tax Code of the Russian Federation). Documentary evidence is the decision to suspend the criminal case due to failure to identify the person to be brought as an accused (letter from the Ministry of Finance dated December 27, 2007 No. 03-03-06/1/894 and the Ministry of Taxes of Russia dated June 8, 2004 No. 02- 5-10/37).

At the same time, these losses are taken into account as part of the expenses of the reporting (tax) period in which this resolution was issued (letters of the Ministry of Finance dated May 2, 2006 No. 03-03-04/1/412 and dated August 3, 2005 No. 03-03 -04/1/141). In turn, another explanation from officials states that the organization has the right to increase expenses only after a decision to terminate the criminal case is issued (letter of the Ministry of Finance dated January 20, 2006 No. 03-03-04/1/52). A similar opinion is contained in the letter of the Ministry of Finance dated January 16, 2006 No. 03-03-04/1/18 regarding the write-off of damage caused to the organization as a result of a fire.

Judicial and arbitration practice

Subparagraph 5 of paragraph 2 of Article 265 of the Tax Code connects the taxpayer’s right to attribute losses from theft to non-operating expenses precisely with the fact of failure to identify the guilty person, and not with the termination of the criminal case due to the expiration of the statute of limitations for criminal prosecution (Resolution of the Federal Antimonopoly Service of the Volga Region dated July 5, 2007 No. No. A72-4858/06).

Let us note that there are court decisions that speak of the possibility of taking losses into account as expenses not at the time of the decision to suspend the criminal case, but at the time of its receipt .

Judicial and arbitration practice

The losses incurred by Cheboksary Aggregate Plant OJSC as a result of the theft of a bill of exchange became obvious to the organization from the moment it received the resolution of the Tverskoye Internal Affairs Directorate of the Central Administrative District of Moscow dated February 28, 2001 on the suspension of the preliminary investigation due to the failure to identify the person to be involved as accused in a criminal case, namely from May 26, 2004 (resolution of the Federal Antimonopoly Service of the Volga-Vyatka District dated October 29, 2007 No. A79-11442/2006).

Estimation of losses when accepting goods from suppliers

When accepting goods to assess losses, an organization should draw up an act on the established discrepancy in quantity and quality when accepting inventory items (TORG-2 or TORG-3), approved by the resolution of the State Statistics Committee “On approval of unified forms of primary accounting documentation for recording trade operations” dated December 25, 1998 No. 132 (letter of the Ministry of Finance dated August 15, 2006 No. 03-03-04/1/628). The specified form is issued if there are quantitative and qualitative discrepancies compared to the data in the supplier’s accompanying documents. In the future, this act is the legal basis for filing a claim with the supplier.

Judicial and arbitration practice

Acceptance of goods in terms of quantity and quality is carried out in the presence of the supplier or his representative who has a power of attorney, and is documented in a document. If the supplier or his representatives fail to appear when accepting the goods or the arriving representatives do not have properly executed powers of attorney, the buyer will independently accept the goods. The buyer has the right to document the shortage of goods by a unilaterally drawn up act (Resolution of the Federal Antimonopoly Service of the North-Western District dated January 21, 2008 No. A05-5927/2007).

Note that the procedure for drawing up acts for the transportation of goods by rail is prescribed in the Rules for drawing up acts for the transport of goods by rail, approved by Order of the Ministry of Railways of the Russian Federation dated June 18, 2003 No. 45.

Officials in the letter of the Ministry of Finance dated 04/03/2007 No. 03-07-09/3 noted that if the buyer identifies a shortage of goods, corrections can be made to the invoice, certified by the signature of the manager and the seal of the seller, indicating the date of the changes.

VAT

On the question of whether it is necessary to restore input VAT on missing values, there is a long-standing dispute between taxpayers and officials3.

So, the Ministry of Finance, in letter dated November 1, 2007 No. 03-07-15/175, answered questions about the application of VAT in relation to stolen property:

- disposal of property for reasons not related to sale or gratuitous transfer (for example, due to loss, damage, battle, theft, natural disaster, etc.) is not subject to VAT taxation;

- the amounts of tax previously lawfully accepted for deduction on the specified property must be restored. Restoration should be made in the tax period in which the missing property is written off;

- for depreciable property, VAT is subject to recovery in an amount proportional to the residual (book) value of the property without taking into account revaluation;

- when identifying the guilty persons and returning the property to the taxpayer in the case of using the returned values in transactions subject to VAT, a corrective tax return must be submitted for the tax period in which the deductions were restored;

- In case of compensation of damage by the guilty person in cash, VAT is not charged and the amounts of restored deductions are not adjusted.

Judicial and arbitration practice

The court came to the conclusion that when writing off inventory items due to their shortage, the object of VAT taxation does not arise and the taxpayer’s obligation to “restore” the VAT tax deduction does not arise (Resolution of the Federal Antimonopoly Service of the Moscow District dated November 20, 2007 No. KA-A40/11809 -07).

Note that earlier financiers argued that the disposal of property in connection with theft, when the perpetrators are identified, should be considered as an object of taxation with value added tax (letter dated August 14, 2007 No. 03-07-15/120). But later they realized the absurdity of the situation and canceled this explanation with the above-mentioned letter from the Ministry of Finance dated November 1, 2007 No. 03-07-15/175. Well, officials have said more than once that the amounts of VAT previously accepted for deduction on inventory items identified as missing during the inventory of property are subject to restoration (letter of the Ministry of Finance dated July 31, 2006 No. 03-04 -11/132). True, the restored input tax paid on the purchase of goods written off as emergency expenses due to a fire can be taken into account in non-operating expenses taken into account when determining the tax base for income tax, subject to documentary confirmation of the fact of the fire and loss of property (letter from the Ministry of Finance dated 06.05. 2006 No. 03-03-04/1/421).

Judicial and arbitration practice

Shortage of goods discovered during the inventory process does not apply to the cases listed in paragraph 3 of Article 170 of the Tax Code (Resolution of the Federal Antimonopoly Service of the Volga District of October 11, 2007 No. A55-733/2007, of the North Caucasus District of May 10, 2007 No. F08-2502/07-1036A, Volga District dated March 15, 2007, No. A55-9182/06-43).

In turn, the senior arbiters recalled back in 2006 that the obligation to pay into the budget VAT amounts previously legally accepted for offset should be provided for by law. At the same time, paragraph 3 of Article 170 of the Tax Code specifies all situations in which tax amounts accepted for deduction are subject to restoration. Shortage of goods is not one of these cases. Based on this, it was concluded that for shortages and thefts, the obligation to contribute to the budget the amounts of VAT previously accepted for offset is not provided for by law (decision of the Supreme Arbitration Court of the Russian Federation dated October 23, 2006 No. 10652/06).

1 Read more about commodity losses on page 24 of magazine No. 5` 2008

2 Read about the financial liability of the employee and employer on page 72 of magazine No. 1' 2007

3 How to reflect in accounting the amount of shortage or damage discovered upon acceptance of valuables received from the supplier, read on page 24 of magazine No. 5' 2008

Magazine Tax Accounting for an Accountant

How to write off the shortage at the expense of net profit

Net profit is the final financial result of the company's activities for the reporting period. Its indicator is formed on account 99 “Profit and losses” and with the final turnover at the end of the year is written off to the credit of account 84 “Retained earnings (uncovered loss)”. Retained earnings can be used to cover losses (for example, when a shortage is discovered). However, only the owners of the company can decide on this form of using profits.

This publication talks about where the company’s net profit can be directed.

If the owners make such a decision, the entries when writing off the shortfall at the expense of net profit will not affect accounts 99 and 84. The operation to write off the shortfall in accounting will be reflected in the correspondence of accounts Dt 91.2 Kt 94. Such writing off of the shortfall leads to discrepancies between accounting and tax accounting , since this amount will not participate in calculating the taxable base for income tax. As a result, a permanent tax liability must be reflected in the accounting accounts.

Attention! Hint from ConsultantPlus: There is a position of the Russian Ministry of Finance, according to which if the perpetrators have not been identified, then a document confirming the right to include losses from theft in expenses is... (read more).

Learn about the types of discrepancies between accounting and tax accounting from this material.

We document the inventory results in postings

The final stage of the inventory is the reconciliation of accounting data, and often there is a need to write off shortages or, on the contrary, to capitalize excess values.

How to reflect in postings the identified shortages during inventory

The shortage must be reflected on account 94 in correspondence with the account for the property being written off:

Dt 94 K 10(41,43,01)

Next, we proceed in one of two ways:

1) The perpetrators have not been identified (not found).

You can write off the shortage within the approved norms of natural loss as expenses for the main activity. Shortage during wiring inventory:

Dt 20 (23,25,26,44) Kt 94

If natural loss rates for certain types of property are not established or the shortage exceeds them, then it is charged to other expenses and reflected by posting:

Dt 91.2 Kt 94

It is important to remember that in tax accounting it is impossible to recognize expenses in excess of the norms of natural loss (Article 254 of the Tax Code of the Russian Federation). 2) The perpetrators are identified, the damage is compensated at their expense

2) The perpetrators are identified, the damage is compensated at their expense.

In this situation, an important role is played by the presence and content of an agreement on financial liability, as well as the norms of the Labor Code of the Russian Federation, which contain instructions on the maximum amount and procedure for deducting amounts from employees’ wages. If the guilty person is not an employee of the organization and agrees to compensate for the damage (it is better to draw up an agreement on voluntary compensation for damage), then you can deposit the money into the cash register or into a current account. The accountant will reflect the shortage by posting:

- Dt 73 Kt 94 – the shortage is attributed to the guilty person;

- Dt 50 (51) Kt 73 – the guilty person compensated for the shortage.

If compensation for the shortfall is determined at a market value exceeding the book value, then the excess amount is reflected in the following entries:

- Dt 73 Kt 98 - the difference in the cost of the shortage is reflected;

- Dt 98 Kt 91 - the difference is attributed to other income.

If a person does not plead guilty and does not agree to compensate for the damage, then the shortfall is written off as other expenses (as in the case of an unidentified culprit) and awaits a court decision.

How to reflect in postings identified surpluses during inventory

As a rule, surpluses are detected less frequently during inventory. They are accounted for at market value, which must be confirmed in one of the following ways:

- A company certificate compiled on the basis of an analysis of prices for similar property (invoices from suppliers, advertisements for the sale of similar objects in the media, a certificate from statistical authorities, etc.);

- A certificate prepared by an independent appraiser (more preferable).

Excess valuables at market prices are included in other income and capitalized using the following entry:

Dt 10 (41,01,50) Kt 91.1

Re-grading

If the audit reveals a shortage of one value and a surplus of another, this fact must also be reflected in accounting.

Situation: During an inventory of the spare parts warehouse, a shortage of three bushings costing 4,500 rubles per piece was revealed, and a surplus in the form of three injectors costing 6,700 rubles per piece.

Let's reflect in accounting:

| Dt | CT | Sum | Explanation | Document |

| 94 | 10.5 | 13 500,00 | A shortage of bushings was determined (writing off inventory items) | Inventory INV-3, statement INV-19 |

| 10.5 | 94 | 20 100,00 | Injectors are capitalized | Inventory INV-3, statement INV-19 |

| 94 | 91.1 | 6 600,00 | Other income recognized | Accounting certificate |

Results

Identified amounts of shortfalls, regardless of the presence or absence of perpetrators, are reflected in the debit of account 94 “Shortages and losses from damage to valuables.”

The amounts reflected in this account are written off to account 73 “Settlements with personnel for other transactions” - if the culprit is identified, or is recognized as another expense and written off to account 91 “Other income and expenses” - if the culprits are not found or their involvement in the shortage is not proven. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Postings

The account directly named as related to shortages is “Shortages and losses from damage to valuables” (94), but it is not always used.

During a planned inventory, if there is a shortage, make an entry Dt 94 Kt of valuables accounts; in case of force majeure (fires, natural disasters), it is included in profit and loss: Dt 99 Kt of valuables accounts.

If a shortage is identified when counting goods from counterparties, the scheme Dt 94 Kt of accounts of valuables is also used (within the limits of the volumes fixed by the contract). Volumes of shortages identified during the calculation that are larger than those provided for in the contract may give rise to claims. Then use the entry Dt 76 Kt of value accounts.

In account 76, a sub-account “Settlements for claims” is opened. The shortage is recorded depending on the type of goods and materials: Dt 94 Kt 01, 10, 41, 50. The detected shortage of fixed assets is recorded according to Kt 01 at the residual value, depreciation is written off separately: Dt 02 Kt 01.

Financially responsible persons are not obliged to compensate for shortfalls within the limits of natural loss. It increases the cost of production: Dt 20, 23, 44, etc. Kt 94.

The shortfall in excess of the loss norms is repaid from the funds of the guilty employees: Dt 73/2 Kt 94. If the culprit is not found or there is a court decision in favor of the financially responsible person about his innocence, the excess shortage is included in other expenses of the company: Dt 91/2 Kt 94.

Briefly about the main thing

- The write-off of shortages during inventory is carried out depending on its reasons.

- The shortage within the limits of natural loss norms and compliance with the terms of the agreement between counterparties is taken into account in account 94 and written off to the cost of production. If the lack of material assets is higher than the norm, the company’s losses are compensated by the guilty employee from his own funds. If the culprit is not found or determined by the court, the shortage will be written off as other expenses.

- Shortages resulting from disasters and natural disasters are included in profit and loss (account 99), and in a situation where goods received from a counterparty have a shortage not provided for in the contract, account 76, subaccount “Settlements for claims”, is used.

- The norms of natural loss are established by separate documents of the ministries and are applied depending on the industry, business area, and inventory object by members of the inventory commission when calculating damage.

- It is very problematic to hold guilty persons accountable if a liability agreement has not been concluded with them.

- The manager always has financial responsibility to the company; such an agreement is not concluded with him.

Accounting: markdown

If an organization plans to discount damaged goods, then make the following entries in accounting:

Debit 94 Credit 41

– the cost of damaged goods is reflected (based on the act in form No. TORG-15);

Debit 94 Credit 42

– the trade margin attributable to damaged goods is reversed (if goods are recorded at sales prices).

For the convenience of reflecting the markdown of goods to account 41, open a separate sub-account, for example, “Goods subject to markdown”.

Debit 41 subaccount “Goods subject to markdown” Credit 94

– goods subject to discounting have been capitalized (at market value, taking into account their physical condition);

Debit 44 Credit 41 subaccount “Goods subject to markdown”

– samples of damaged goods were submitted for examination (if examination is necessary for the sale of damaged goods);

Debit 44 Credit 60

– expenses for conducting an examination are reflected (if an examination is necessary for the sale of damaged goods);

Debit 62 Credit 90-1

– revenue from the sale of goods at a discount is reflected;

Debit 90-2 Credit 41 subaccount “Goods subject to markdown”

– the cost of discounted goods is written off (the cost at which they were capitalized);

Debit 90-3 Credit 68 subaccount “VAT calculations”

– VAT is charged on the sale of discounted goods (if the organization is a VAT payer);

Debit 90-2 Credit 44

– costs associated with sales are included in the cost of sales (if an examination is required to sell damaged goods).

If damaged goods cannot be used (sold) in the future, reflect their value in accounting on account 94 “Shortages and losses from damage to valuables” in correspondence with property accounting accounts (account 41). Moreover, if goods are recorded at sales prices, then simultaneously with the fact of damage to goods being reflected on account 94, the trade margin attributable to damaged goods and previously recorded on account 42 must be reversed. This is stated in the instructions for using the Chart of Accounts (account 94, 41, 42). When reflecting the fact of damage to goods in accounting, make the following entries:

Debit 94 Credit 41

– damage to goods is reflected;

Debit 94 Credit 42

– the trade margin attributable to damaged goods is reversed (if goods are recorded at sales prices).

This procedure for reflecting damage to goods in accounting is reflected in subparagraph “b” of paragraph 29 of Order No. 119n of the Ministry of Finance of Russia dated December 28, 2001.