Form 4-FSS for the year

The currently current form of Form 4-FSS was approved by FSS Order No. 381 dated September 26, 2016. The latest amendments to it were made by FSS Order No. 275 of 07/07/2017. There is no new form provided for the 4-FSS report for 2021.

From 2021 it is planned to introduce a new report form. The draft new order of the FSS provides for the entry into force of the new form 4-FSS, starting with the report for the 1st quarter of 2021 . This is due to the transition to direct payments: from this period, employers will transfer insurance contributions in full - they will not be reduced by the amount of benefit payments. The territorial branches of the Funds will assign and pay insurance payments.

The new form will be simplified. In particular, tables containing data on expenses of funds paid from insurance contributions will be excluded from it, and tables for calculations of contributions will be removed. At the same time, the table on contributions for insurers temporarily providing personnel to other employers will change in the form, and a new section will appear for companies with designated independent qualifying units.

Thus, the currently current 4-FSS 2021 form will be changed no earlier than the 1st quarter of 2021. For 2021, policyholders submit reports using the same form.

Purpose of the unified form KO-4

Form KO-4, called a cash book, is a tool for keeping records of the following transactions at the cash desk of an enterprise:

- receipt of cash;

- cash issuance.

ATTENTION! From November 30, 2020, the rules for processing cash transactions have been simplified. For example, separate divisions of organizations have the right not to maintain a cash book if they hand over cash to the head branch.

ConsultantPlus experts told us what other innovations in the procedure for recording cash transactions came into effect on November 30, 2020. Get trial access to the K+ system and go to the review material for free.

Information about outgoing and incoming orders is entered into the fields of the form.

Read more about some of the nuances of cash management at an enterprise in the article “Cash discipline and responsibility for its violation.”

Deadlines and features of form 4-FSS (year 2020)

The form is submitted in paper or electronic format if the average number of employees is no more than 25 employees at the end of last year, but if the number is larger, an electronic report is required.

In 2021, reporting deadlines remain the same. The policyholder submits a paper report for 2021 no later than the 20th day of the month that follows the billing period, i.e. no later than 01/20/2021. The deadline for submitting an electronic annual report is until the 25th of the next month, i.e. no later than 01/25/2021

You can download Form 4-FSS for 2021 at the end of this article. It is not difficult to compile a report; it consists of a title page in which data about the policyholder is entered, and six tables. The title, as well as tables 1, 2 and 5, must always be filled out, even if the employer has not made any accruals or payments for “injuries” (in this case, zero reports are submitted). The remaining sections are not required to be completed, except in cases where during the reporting period the policyholder had transactions to be reflected in them.

All amounts are given in rubles and kopecks.

The procedure for filling out the form is given in the same order No. 381.

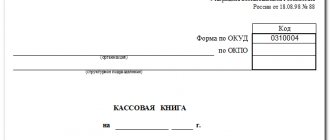

Cash book (form KO-4)

Home / Cash discipline

| Table of contents: 1. Is a cash book needed for online checkout? 2. Features of maintaining a cash book 3. Instructions for filling out form KO-4 4. Sample of filling out the cash book | Document: Download the cash book in excel or word Download sample filling KO-4 |

The cash book is an integral part of the financial documents of the organization and is intended to reflect information about the receipt and expenditure of cash.

The document has a unified format, developed and approved by Decree of the State Statistics Committee of Russia No. 88 of 08.18.98. (ed. 05/03/00), OKUD form 0310004.

Since 2014, individual entrepreneurs and organizations related to small businesses have the right to refuse to issue cash orders, set a cash balance limit and fill out a cash book in accordance with Bank of Russia Instructions No. 3210-U dated 03/11/14.

Based on Federal Law No. 209-FZ dated July 24, 2007. and Government Decree No. 265 of 04/04/16. Small businesses include companies:

- Having no more than 100 employees;

- With incomes of up to 800 million rubles per year;

- With state participation formations in the capital no more than 25%, shares of participation of other companies in the capital within 49%.

Do you need a cash book when checking out online?

In 2021, online cash registers were introduced. For this reason, many questions arise regarding the need to maintain a cash book. Officials provided official explanations on the use of primary cash documents in their activities.

In particular, in letter of the Ministry of Finance No. 03-01-15/54413 dated 09.16.16. It has been established that due to the fact that all necessary data is stored in the fiscal memory of new cash registers, it is not necessary to draw up primary cash documents.

However, these innovations do not apply to the need to fill out a cash book - the methodology for using this document is still regulated by the Procedure for Conducting Cash Transactions (No. 3210-U). As a result, companies must maintain a cash book without changes, using the current form.

Features of maintaining a cash book

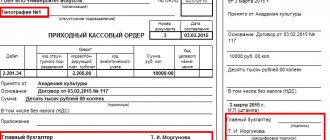

1) The responsibility for filling out a document in a company rests with the cashier or another person, for example, an accountant. All information in the cash book is entered on the basis of incoming and outgoing orders (forms KO-1 and KO-2, respectively).

2) Maintaining a cash book can be carried out both in paper and electronic format.

For a paper book, there is a main part of the document and a tear-off copy. In order to prevent unauthorized corrections to be made to a document, the law obliges those responsible for filling out the cash book to number its pages, lace them together and certify the book with a seal.

If the document is filled out electronically, then the main requirement in this case is to ensure the proper level of protection for the cash book. Information is also entered into the document during the day. Upon completion, the sheets must be printed and certified with the necessary signatures.

At the end of the year, all pages of the book are sewn together, sealed and signed by the responsible persons. If your organization has an electronic signature, you do not need to print the book every day.

3) It is important to remember that each company has the right to maintain only one cash book.

4) The document must be kept for 5 years.

Instructions for filling out form KO-4

Click on the instruction field of interest to see detailed information.

Title page

1. Name of the individual entrepreneur / organization (for example, Limited Liability Company “Elegy”, Individual Entrepreneur Ivanov I.I.) and its structural unit (if any). The company name must be indicated in accordance with the registration documents.

This requirement is enshrined in the Decree of the State Standard of the Russian Federation dated 03.03.2003 No. 65-st. The document ceases to be valid on July 1, 2018. An alternative to it will be GOST R 7.0.97-2016, which contains similar instructions. Thus, if in reg. The documents contain only the full name; this is what needs to be reflected.

In cases where documents also contain an abbreviated name, the company has the right to indicate it below the full name (or next to it).

2. OKPO code. This indicator reflects the type of activity of an organization or individual entrepreneur, and it is assigned by statistical authorities upon registration based on the company’s serial number. The OKPO code is one of the mandatory details and must be indicated in the document. However, due to the fact that no fines are imposed on the company for the absence of this indicator, in practice it is often left blank.

3. The period for which the cash book is compiled (calendar year).

Tabular part

The tabular part of the document is presented in the form of two identical sheets, one of which (the main part) remains in the cash book, and the second (the detachable part) is transferred to the accounting department as a cash worker’s report. Entering data into both parts of the document is carried out in exactly the same way.

Line before table

- The period for which the KO-4 form sheet is filled out. The procedure for conducting cash transactions (Instruction of the Bank of Russia No. 3210-U dated March 11, 2014) establishes that on those days when cash receipts and debit transactions were not carried out, it is not necessary to fill out the KO-4 form;

- Cash book sheet number.

Table

- Number of the primary document (receipt or expense order);

- Information about the person who transferred or received funds. This column can reflect information about both individuals - counterparties of the organization, and partner companies;

- Number of correspondent account. The account is indicated depending on the basis for receiving or issuing funds. For example, if money is issued from the cash register on account, account 71 should be indicated, and if money is issued to the supplier, then account 60;

- The amount of income or expense. Depending on whether the funds were received by the company or issued from the cash register, the amount is reflected in the corresponding “Income” or “Expense” column.

To reflect cash transactions during the day, two pages of the document are provided. The first contains information about the balance at the beginning of the day, as well as the timing for reflecting current cash transactions for the day. At the bottom there is a “Transfer” line, designed to summarize the page and transfer the remainder to the next page of the document.

In the event that there were few cash transactions and the sheet was not completely filled out, in order to prevent invalid entries from being made on the entire empty area of the table, the cashier must put the letter Z (this applies to both the first and second pages of the spread).

After all information about the receipt and expenditure of cash is reflected, it is necessary to add up the totals and indicate the cash balance at the end of the day. The balance is indicated taking into account the funds planned for the payment of wages and benefits. Cash discipline rules determine the ability of companies to keep money in the cash register in excess of the established limit during payroll periods for three days.

After filling out, the cashier responsible for compiling the cash book puts his signature and transcript in the document and transfers its detachable part, as well as incoming and outgoing cash orders to the accounting department.

The accounting employee checks the entries in the cash book, indicates the number of incoming and outgoing documents in words, puts his signature and transcript in the KO-4 form.

last page

The last page of the cash book must reflect information that the document is numbered (indicating the number of sheets), laced and sealed. It is also important to indicate information about the head of the company (position, signature and transcript) and the chief accountant.

Sample of filling out a cash book

Title page

Tabular part

last page

Did you like the article? Share on social media networks:

- Related Posts

- Receipt cash order (form KO-1)

- Journal of registration of incoming and outgoing cash documents

- Sample of filling out form T-49

- Cash payment limit in 2021

- Order to abolish the cash limit in 2021

- Order on accountable persons

- Cash accounting book (form KO-5)

- Advance report (form AO-1)

Leave a comment Cancel reply

How to display data in tables 1 and 1.1

Table 1 calculates the basis for calculating contributions for “injuries”. The data is reflected on a cumulative basis from the beginning of the billing period.

Columns 4, 5, 6 contain amounts broken down for the last three months of the billing period. Column 3 includes the year-to-date basis.

Table 1.1 is required to be completed only if the policyholder sent its employees to temporarily perform official duties for another employer in accordance with the contract. Here you indicate information about the host organization and the basis for calculating contributions. Acceptance LLC did not send its employees, therefore section 1.1 is not included in the report.

Form 4-FSS (current)

The required calculation sheets for filling out and submitting in Form 4-FSS are as follows:

- title;

- tables, and.

If during the year benefits were made for an industrial injury or other expenses counted against contributions for injuries to the Social Insurance Fund, also fill out Table 3. And in case of an accident at work, Table 4 (clause 2 of the Procedure for filling out Form 4-FSS).

In the “Average number of employees” field, enter the average number of employees for 2021, calculated in the usual manner (clause 5.15 of the Procedure).

In Table 5:

- provide all data as of 01.01.2021;

- Do not reflect special assessments and medical examinations carried out during 2021

In 4-FSS for 1 quarter, half a year, 9 months and a year, Table 5 will be the same.

Form 4-FSS is given in Appendix No. 1 to the order of the FSS of the Russian Federation dated September 26, 2016 No. 381, and the procedure for filling it out is in Appendix No. 2 to this order.

You can download this 4-FSS form for free using the link .

Procedure for filling out table 2

Table 2 is filled out according to accounting data on the status of settlements with the Social Insurance Fund for insurance premiums and expenses for the billing period.

On the left side of the table, the policyholder indicates the amount of contributions in terms of accruals for the year and for the last three months, balances at the beginning of the billing period and funds received from the Fund. On the right, the employer reflects the insurance payments made and the transferred insurance premiums (indicating payment details for the last three months).

The indicators are summarized, line 19 reflects the total debt (or overpayment) of the policyholder to the Fund at the end of the quarter.

Features of filling out form KO-4

The cash book in form KO-4 consists of 2 elements - the main part and a copy. Moreover, their structure and relative position depend on how the document is filled out - on paper or on a computer.

In the first case, the copy of the KO-4 form is tear-off. It is filled in simultaneously with the main part when using carbon paper. When filling out the document in question on a computer, a copy of the form can be obtained by reprinting its main part on a printer.

The legislation also provides for the option of maintaining a cash book in completely electronic form, subject to the use of automated systems.

You can download the unified form KO-4 on our website:

You can find a completed sample cash book in the article “Procedure for maintaining and filling out a cash book - sample”

Payouts: tables 3 and 4

Tables 3 and 4 are filled out if the corresponding indicators are available. The data in Table 3 reflects insurers who, in the billing period, had expenses for the payment of benefits related to occupational diseases, work-related injuries and accidents. The table is also filled out when funds are spent on purchasing PPE or carrying out preventive measures to reduce injuries and occupational diseases.

Table 4 includes the number of persons injured in insured events in the reporting year. Since Acceptance LLC did not have such payments, these sections are not filled out.

If a pilot project “Direct Payments” is operating in the region, i.e. Since the Social Insurance Fund transfers payments to victims directly, information about such payments is not included in Tables 2, 3 and 4.

Responsibility for failure to comply with deadlines for submitting Form 4-FSS

Legal entities and individual entrepreneurs, in case of delay in submitting a report, will have to pay a fine in the amount of 5% of the amount of contributions accrued for payment over the last 3 months. A fine is assessed for each month (full and incomplete) for which the company delayed submitting reports. The maximum fine does not exceed 30% of the amount charged, and the minimum is 1000 rubles. (Clause 1, Article 26.30 of Law No. 125-FZ of July 24, 1998).

Failure to comply with the electronic format, if required, will result in a fine of 200 rubles. (Clause 2 of Article 26.30 of Law No. 125-FZ).

In accordance with the Code of Administrative Offenses of the Russian Federation (clause 2 of Article 15.33 of the Code of Administrative Offenses of the Russian Federation), penalties are also imposed on officials of the policyholder in the amount of 300-500 rubles.

For whom is the use of the KO-4 form mandatory?

There is a misconception that Russian organizations are not required to fill out Form KO-4 from January 1, 2013 - due to the entry into force of the new accounting law and the appearance of corresponding clarifications in the letter of the Ministry of Finance of the Russian Federation No. PZ/10-2012, according to which organizations have the right not to use unified forms in your work.

The fact is that such preferences are established in relation only to those organizations that the legislator in certain legal acts does not directly require to use unified forms. A similar source of law operates in Russia - this is Bank of Russia Directive No. 3210-U, issued on March 11, 2014.

In accordance with paragraph 1 of the instructions, legal entities must unconditionally follow the rules contained in the provisions of the relevant act. In turn, individual entrepreneurs generally have the right not to keep a cash register, which means they are not required to use standardized forms, including document KO-4. At the same time, the practical need for registering incoming and outgoing transactions at the cash desk of an individual entrepreneur may well arise (for example, when issuing cash to employees on account), and in this case the KO-4 form should be used as a cash book.

Read the useful facts about cash transactions in the article “The concept and types of cash transactions (legal regulation).”