What is the fundamental difference?

The difference lies in the method of recording income and expenses for the selected accounting period. Those. in which business transactions for the period are considered expenses and which are income. It is clear that during the entire existence of the enterprise, all receipts of money are income, and all payments are expenses. But we are not interested in the entire working time, but in each specific period. Quarter, month, week or even day. When we divide our time line into segments, the difference arises.

Under the cash method, income is considered to be any receipt of funds in the cash register or to a current account, and expenses are any payment or disbursement made during the accounting period. In this case, the relationship between income and expenses for the same period does not matter. We bought vodka, sold an hour of karaoke - it’s still income and expense.

Under the accrual method, income for a period is considered to be the sales value of goods sold and services provided in this period, regardless of their payment. And an expense is considered to be the cost of goods and services sold, as well as the enterprise’s consumption of goods and services, and also regardless of their payment to the supplier. Those. if Borscht is income, then everything related to this Borscht is considered an expense - food, cook’s salary, hall rent, electricity, etc. Those. everything that led to the opportunity to realize this particular Borscht.

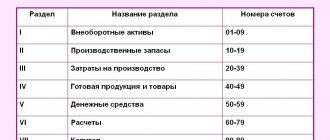

In case of sale of products

With this type of income generation, such as recognizing revenue from the sale of products, not everything is simple, since there is a method of determining “as ready” for products that has a long production cycle. To apply it, you need to be able to determine partial readiness or use the criteria for completing a stage of work (clause 13 of PBU 9/99). If we are talking about construction, then PBU 2/2008 “Accounting for construction contracts” is applied. Other products or works can be found in the list of Government Decree No. 468 dated July 28, 2006. But for them you need to obtain a special document from the Ministry of Industry and Trade according to the Order of the Ministry of Industry and Trade dated June 7, 2012 No. 750. Both the Decree and the Order are needed for correct accounting of VAT on goods and works long production cycle. But the definition and recognition of revenue from the sale of products in accounting and tax accounting can be carried out in the same way, since Regulation BU 9/99 does not provide any specifics on products and long-cycle work.

Which method is better?

It depends on situation.

The cash method is easier to implement because... is based on data from payment systems, which is very easy to collect - they are reflected in the cash register or banking system and are always confirmed by primary documents. In addition, the result of this method - profit - coincides with the cash balance, i.e. can be easily verified (by cash count).

The accrual method is more complicated, and its profit does not coincide with the cash balance, but it is more accurate in the sense that if the profitability or efficiency of the enterprise is calculated by the profit received, then it makes more sense, because income, expense and profit are interrelated.

The difference between them can be illustrated by the example of gasoline consumption in a car. Gas mileage is something we use to measure the “efficiency” of a car (and driving style). The lower the gas mileage, the better.

The “accrual method” is when we compare the distance traveled during a period with the volume of gasoline consumed during the same period. For this we use the on-board computer. We can drive 100 km in one week and spend 7 liters (7 l/100km), and drive 1000 km in another week and spend 60 liters (6 l/100km). Obviously, in the second week we drove more economically or “more efficiently”.

The “cash method” is when we compare the distance traveled during a period with the volume of gasoline purchased (filled in the tank) during the same period. We can fill 50 liters in one week and drive 1 km (5000 l/100km), and the next week add another 1 liter and drive 100 km (1 l/100km). Obviously, the results are not comparable, they make no sense.

Systems

It is equally important to take into account the features of the systems into which financial accounting based on the accrual method will be integrated, since they will create the very information useful for decision-making that was discussed so much above. It is important for the government to consider how incentives for using such information can be built into these systems, since the mere fact of its presence will not be enough.

Here's an example. Quite often the question arises whether, when switching to the accrual method, it is necessary to make financial management systems centralized or decentralized, distributed among various government departments. There is no clear answer, and quite often the choice is based on simple pragmatism, but in any case, even before starting, it is necessary to have a clear understanding of the expectations from the reform in various ministries and departments.

Experts also noted that changes in the very structure of the government apparatus and the introduction of new disclosure requirements must be considered in the context of identifying systems that are most suitable for the purpose of creating information useful for decision-making. As an example of a common recommendation in this regard, they cite the integration of the budget process, accounting process and government statistics into one system, which will make data comparison easier. Of course, such structural reform will require comprehensive cooperation at the state level.

When should you use the cash method?

The cash method, however, is not simply “simple but meaningless.” There are situations when it can and should be used.

1. If your income and expenses for the period are in no way related to each other. One example I can give: software development and sales. Licenses sold over the past month are not directly related to programmers' salaries. And in this sense, the moment of transferring the rights to the license to the client is no different from the moment of payment for this license. Therefore, it is difficult to calculate the “effectiveness” of a development company as a whole.

2. If at the boundaries of periods the size of inventories and debts remains constant. In particular, zero. Those. if by the end of the period you don’t owe anyone (zero “creditor”), no one owes you (zero “debtor”) and you have no inventory, then you can safely count your profit on the cash basis. The result will be the same as with the accrual method, only it’s easier to calculate. I repeat once again - the amounts of inventories and debts are zero or the same as at the beginning of the period.

Even according to Russian legislation for small businesses - i.e. for those whose annual turnover does not exceed 1 million rubles, it is allowed to record profits using the cash method. This is done because it is believed that for such enterprises the change in inventories and debts from period to period is insignificant. And they can be neglected in the calculation.

Additional terms

In addition to those described above, there are additional conditions for recognizing revenue in accounting - implementation options in which the amount of monetary valuation is indeterminable. But you can always calculate the expenses incurred in the production of work, services, etc. This amount should be considered a monetary asset receivable (clause 14 of PBU 9/99). Any other receipts that are defined as “other” and can be taken into account on account 91 must also meet the set of conditions set out in clause 12 of PBU 9/99. When approving revenue recognition in your accounting policies, refer to the regulatory documents that you use.

In 2021, amendments were made to the Accounting Regulations 1/2008, which allow the use of IFRS, Accounting Regulations and recommendations in the field of accounting for the formation of UE (clause 7.1 of Accounting Regulations 1/2008).

Legal documents

- Federal Law of July 24, 2007 No. 209-FZ

- Federal Law No. 402-FZ of December 6, 2011

- PBU 9/99

- PBU 2/2008 “Accounting for construction contracts”

- Order of the Ministry of Industry and Trade dated 06/07/2012 No. 750

- Regulation BU 1/2008

When should you use the accrual method?

Well, actually, the same two points, only in reverse.

1. If you have a clear relationship between income and expenses.

2. If you have accounts receivable and/or payable and they are constantly changing. And also if you have warehouse stocks and their volume at the boundaries of periods is also unstable.

In these cases, it makes sense to use the accrual method because:

1. The ratio of related income and expenses can show you the performance of your business for any given period. And they can and should be compared.

2. The error introduced by debts and changes in inventories is too large and has a significant impact on the result.

Stakeholders

What distinguishes the public sector of the economy from private business is the existence of large groups of “stakeholders” - or, in simple terms, users of government financial and budget reporting. These are not only ordinary citizens, but also government agencies, credit rating organizations, non-governmental entities, governments of other countries, and so on. This means that the process of introducing the accrual method also requires their possible participation, since the very creation of information useful for decision-making implies the ability to evaluate the progress of the reform and question it. Financial literacy of future participants in the process is not the least important factor.

The experts interviewed constantly emphasized the need for the active participation of government managers and politicians as leaders who can agitate and pull the entire process along with them. Successful transition to accrual accounting requires multiparty support. And to ensure that the reform is accepted by each of the key stakeholder groups, it is necessary that each group clearly understands the benefits that the accrual method brings to it. It is quite possible that getting the word out about these benefits will require the help of reform advocates who can talk clearly and colorfully about everything.

Which method should be used in restaurants?

In restaurants, of course, profits should be considered on an accrual basis. Because a catering company answers positively to both questions from the previous paragraph - the restaurant has a direct connection between the catering services provided during the selected period (dishes sold) and the expenses incurred (cost, wages, rent, services, etc. ).

You can use the cash method if you are a “grandma with pies”, or if you are not interested in your profit and efficiency, but only the cash balance is important (also a very real option).

Table

| Accrual method | Cash method |

| Involves the recognition of income or expenses upon the implementation of legally justified actions, which must be followed by financial calculations (but without taking into account the moment of their implementation) | It assumes the recognition of income or expenses upon the implementation of financial settlements, which must be followed by legally justified actions - delivery of goods, performance of work, services (but without taking into account the moment of their implementation) |

| Can be used by all organizations | Can be used by organizations with average quarterly revenue not exceeding RUB 1 million for 4 consecutive quarters |

Popular questions and answers

Question 1. An individual entrepreneur received an advance at the end of the quarter by placing an order for the manufacture of products. Receipt is included in income. A week later (the next quarter had already begun), the customer took the advance payment and terminated the agreement. Should the amount of previously paid funds be taken into account when calculating liabilities?

Answer. Since the advance amount was received back by the customer in the next quarter, it should be taken into account in the tax base for the previous period. In the coming quarter, income is allowed to be reduced by the advance amount.

Question 2. Under what circumstances can a company on OSNO lose the opportunity to use CM in accounting?

Answer. You will need to switch to MN if the average quarterly amount of revenue exceeds the established limit - 1.00 million rubles.

CM has not only advantages, but also disadvantages. The benefits of its use for a particular organization are not the same. They differ depending on the areas of activity and structure. Each firm or company, unless it uses the simplified tax system, must independently understand the pros and cons of the CM before giving preference to it over the accrual method.

Recognition of advance funds as income

One of the features of CM that does not work in favor of companies is that advances received from customers should be considered income. The danger is that the client may change his mind and demand his money back. Or the organization itself will not be able to fulfill its contractual obligations to the creditor who paid in advance. Similar situations with advance payments are a phenomenon that occurs quite often.

The situation, however, is not hopeless. The tax legislation states that in case of return of the advance, the company has the right to reduce income.

It should be taken into account that this is only possible when the receipts are received in the simplified taxation system operating mode. It will not be possible to reduce income if the company:

- started using a different special regime, for example, UTII;

- during the period when the advance payment needs to be returned to the client, there were no funds received.