What do personal income tax codes mean?

The Tax Code obliges tax agents to keep records of income paid to individuals, not in any form, but using special codes.

Thus, paragraph 1 of Article 230 of the Tax Code of the Russian Federation states that each tax agent must compile tax accounting registers. They need to record income paid to individuals in accordance with the codes approved by the Federal Tax Service. The current codes are given in the Federal Tax Service order No. ММВ-7-11/ [email protected] (hereinafter referred to as order No. ММВ-7-11/ [email protected] ). They are used, including for filling out certificates in form 2-NDFL. This means that incorrectly assigning a digital code to income will result in an error in the 2-NDFL certificate. This, in turn, threatens the tax agent with a fine of 500 rubles. for each incorrectly completed income certificate (Article 126.1 of the Tax Code of the Russian Federation, clause 3 of the Federal Tax Service letter No. GD-4-11/14515 dated 08/09/16).

Fill out and submit 2-NDFL via the Internet with current codes

In addition, in many accounting programs, payment codes are tied to determining the date of actual receipt of income. And it is used when filling out line 100 of section 2 of the 6-NDFL calculation. Consequently, due to an error in income coding, the tax agent may incorrectly fill out the 6-NDFL calculation. For this violation, the fine is also 500 rubles. (Article 126.1 of the Tax Code of the Russian Federation).

Finally, this same pay encoding is used in most accounting programs to calculate average earnings. Therefore, incorrect assignment of a code may cause incorrect calculations with employees for vacation pay, business trips, sick leave, etc. If the payment turns out to be underestimated, the organization may be fined in the amount of 30,000 to 50,000 rubles, an official - from 10,000 to 20,000 rubles, and an individual entrepreneur - from 1,000 to 5,000 rubles. (Part 6 of Article 5.27 of the Code of Administrative Offenses of the Russian Federation). If the employee is transferred more than is due, there may be problems with the payment of various benefits compensated from the budget.

IMPORTANT. Errors in the application of codes can lead to underestimation or overestimation of vacation pay, travel allowance, sick leave and other payments “tied” to average earnings. Therefore, it is better to calculate these payments in web services, where current codes are installed and entered into reporting automatically.

Calculate your salary, vacation pay and benefits for free in the web service

Features of trips abroad

When sending an employee abroad, it becomes necessary to take into account additional costs:

- obtaining a visa for an employee;

- purchasing an insurance policy;

- possible consular fees;

- the right to travel by car.

In this case, the tax agent is exempt from withholding funds. It is important to document expenses. If the form was submitted in a foreign language, it must be translated and both copies delivered to the tax authority.

If, in the case of calculation, the amount of expenses is stated in foreign currency, the accountant’s task is to recalculate it into rubles at the current exchange rate at the time the tax agent contacts the inspectorate. The calculations must be secured with the contractor’s signature and date.

Pay attention to the Legal Entity Taxpayer program, with its help you can fill out a 2-NDFL certificate in just a few simple steps.

Income code 4800 with decoding

Let's start with the most universal code - 4800 “Other income”. It corresponds to any income for which there is no more suitable code in Order No. ММВ-7-11/ [email protected] (letter of the Federal Tax Service dated 07/06/16 No. BS-4-11/12127). For example, this code indicates income in the form of a one-time additional payment for vacation (letter of the Federal Tax Service dated August 16, 2017 No. ZN-4-11 / [email protected] ).

In addition, code 4800 can be used, in particular, in relation to the following income: average earnings saved for the days of medical examination; payment for downtime caused by reasons beyond the control of the parties; compensation for the delay in issuing a work book to a dismissed employee; the average salary retained for donors on the days of blood donation and on the days of rest provided to them; the amount of forgiven debt on the advance report; excess daily allowance, etc.

This code is also used for settlements with individuals who are not employees of an organization or individual entrepreneur. For example, using this cipher it is necessary to reflect the amount of winnings that a buyer or client received when participating in a lottery that was not held for the purpose of advertising goods, works or services. Also, code 4800 is used when “requalifying” interim dividends if, at the end of the year, the amount of profit turned out to be lower than the calculated one.

Coding of payments to individuals for personal income tax

Each remuneration paid to an individual has a corresponding coding. The full list is contained in Appendix 1 of the Federal Tax Service order No. ММВ-7-11 dated September 10, 2015. What code the bonus has in 2-NDFL depends on what it was accrued for: for production results or on other grounds.

The certificate indicates the income code bonus for production results 2002, if the remuneration is related to the employee’s performance of his job duties: for performing certain work, for exceeding the plan, etc. Thus, if a monthly, quarterly or annual bonus is paid, the personal income tax code is always will be 2002 (letter of the Federal Tax Service dated 08/07/2017 No. SA-4-1/).

If a one-time bonus is paid that is not related to the performance of work duties: for a holiday, a bonus for an anniversary date, indicate a different income code - 2003.

Table: income code bonus in the 2-NDFL certificate

| Code | Type of payment |

| 2002 | Bonus for labor performance:

|

| 2003 | Bonus due to profit:

|

Table of other income in certificate 2-NDFL

| Encoding | Type of payment |

| 2000 | Wage |

| 2010 | Payments under contract agreements |

| 2012 | Vacation pay |

| 2013 | Compensation for unused vacation |

| 2300 | Payment of sick leave |

Income code 2000 with decoding

The next most common code is 2000. According to Order No. ММВ-7-11 / [email protected] , this code corresponds to “remuneration received by the taxpayer for the performance of labor or other duties.”

Typically, the use of this code does not cause difficulties - everything that is reflected in the employer’s accounting as a salary accrued under an employment contract for the daily performance of job duties “passes” under code 2000. The same value is assigned to the average earnings saved for the period of a business trip, since it also is a salary (letter of the Ministry of Finance dated November 12, 2007 No. 03-04-06-01/383).

Automatically calculate the salary of a posted worker according to current rules Calculate for free

Income code "salary"

The employee's type of income must be completely clear to him. That is why it is necessary to decipher the codes on the payroll sheet. The employer can indicate it on each pay slip or familiarize employees with such information once.

The assignment of codes for each financial transaction to the accounting department is regulated by the Federal Tax Service order “On approval of codes for types of income and deductions” dated September 10, 2015 No. ММВ-7-11/ [email protected] (as amended by the Federal Tax Service order dated October 24, 2017 No. ММВ-7-11/ [ email protected] ). According to it, funds paid to an employee as payment for his work are assigned code 2000.

Income codes 2002 and 2003 with decoding

But bonuses for the purpose of coding income as wages are not recognized, although they are named in Article 129 of the Labor Code of the Russian Federation as part of remuneration. Moreover, bonuses are reflected in tax registers and in 2-NDFL certificates in three different codes.

The main code is 2002. It is used for awards that simultaneously satisfy three conditions:

- the payment is not made at the expense of profits, earmarked proceeds or special-purpose funds;

- the payment is provided for by law, labor or collective agreement;

- the basis for payment is certain production results or other similar indicators (i.e. indicators related to the employee’s performance of his or her job duties). This circumstance must be confirmed by an order for payment of the bonus.

Code 2003 reflects bonuses (regardless of the criteria for their assignment) and other remunerations (including additional payments for complexity, intensity, secrecy, etc., which are not bonuses), which are paid from special-purpose funds, targeted revenues or profits organizations.

For other bonuses, code 4800 must be used.

Also see: “Taxes on premiums: we calculate personal income tax and contributions, take them into account in expenses, and reflect them in reporting.”

What else is taken into account by code 4800

This code is used to take into account other income for which a personal code has not been established.

These include:

- Daily expenses for a business traveler, executed under a work contract or employment contract, paid in excess of the approved limit;

- additional payments at the expense of the enterprise’s own funds, which are made for sick leave and maternity benefits. It is important to remember that maternity benefits are not subject to personal income tax, as well as amounts paid to care for a child under the age of one and a half years; they are not shown in the declaration.

Therefore, before sending reports to the funds, you need to carefully review the amounts falling under code 4800; the tax office checks them first.

What income code is used in 2nd personal income tax when renting a car?

Income codes 2012 and 2013 with explanation

The 2012 code corresponds to the amount of vacation pay, that is, the average earnings retained by the employee during the vacation period. This code is used to make payments both for regular vacations and for additional ones, including educational ones.

Code 2012 can only be applied to vacation pay that is paid to existing employees. If the employer transfers compensation to the dismissed employee for unused vacation, this income must be assigned code 2013.

ATTENTION. The Labor Code allows for the provision of leave followed by dismissal (Part 2 of Article 127 of the Labor Code of the Russian Federation). In this case, the employee receives the final payment and work book before the vacation, and does not return to the previous employer after the vacation. However, from the point of view of labor legislation, the transferred amounts are vacation pay, and not compensation for unused vacation. Therefore, the code 2012 must be applied to such a payment.

Also see: “An employee is ill or recalled from vacation: what to do with personal income tax, contributions and reporting?”

Income codes in salary slips

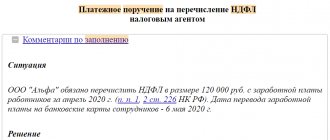

Why are income codes needed?

The Central Bank introduced three income codes for payment orders so that the bank could differentiate between an individual’s income and understand from which income the debt can be withheld under writs of execution and from which it cannot (Federal Law No. 12-FZ dated 02/21/2019).

Codes must be used for all payments to employees and contractors under GPC agreements. So now for this purpose the payment of income will have to be processed in two or three payments.

From June 1, for incorrectly indicating codes or failing to indicate them, an official may receive a fine of 15-20 thousand rubles, and an organization - 50-100 thousand rubles.

Where are the income codes placed?

They did not add a new field for the income code to the printed payment form, but reserved field 20 “Payment purpose code” for this purpose. Enter the code starting from June 1, 2021; before this date the field is simply not filled in.

What codes to indicate on salary slips

The Central Bank explains which codes and when to enter in field 20 in instruction No. 5286-U.

- code 1 when paying wages and income for which restrictions on the amount of deductions apply (according to Article 99 of Law No. 229-FZ of October 2, 2007). These are salaries, bonuses, sick leave benefits, vacation pay.

- code 2 when paying money from which debts cannot be collected (according to Article 101 of Law No. 229-FZ dated October 2, 2007). These are, for example, maternity benefits and child benefits.

- code 3 when paying money that is indicated as an exception in Part 2 of Art. 101 of the Law of October 2, 2007 No. 229-FZ. Income with code 3 includes only two types of payments: compensation for harm caused to health and compensation payments from budget funds to persons affected by radiation or man-made disasters. Payments upon the death of the breadwinner (as well as alimony) can be withheld from income with code 3, and these are the only deductions that can be made from them.

How to indicate income codes in Accounting

A field for income codes has appeared in the payment screen form. For some operations it is filled in automatically:

- Code 1 - payments of wages, advance payments, dividends, vacation pay, income under GPC agreements - create a separate payment slip with this code;

- Code 2 - payment of social charges (children's and maternity benefits, financial assistance) and alimony - create a separate payment slip with this code and the operation "Payment of salaries" for benefits or "Payment of alimony".

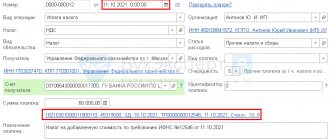

In other cases, when paying income to an individual, the field is not filled in; you need to indicate the income code yourself. When paying an employee's salary, the service will tell you which codes you used to pay last month.

You have already paid an advance, so in the “Amount” field the service will show the amount that needs to be paid to the employee: this is the salary minus personal income tax and the advance. In our example, this is 6,700 rubles.

Below the “Amount” field, the service will tell you which codes were charged in the previous month. In our example, we see an accrual for code 1 in the amount of 8,700 rubles (salary 10,000 minus personal income tax of 1,300 rubles) and for code 2 in the amount of 3,000 rubles. The entire salary that the employee will receive on the card is 11,700 rubles. In May, he already received an advance of 5,000 rubles, and the service deducted it from his salary.

We see the balance due in the “Amount” field - it’s 6,700 rubles. It will need to be divided into as many payments as the number of codes used in the previous month:

- using code 2, pay the entire amount: in our example it is 3,000 rubles;

- according to code 1, subtract the amount of the advance from the amount of accruals for May using this code (it can be viewed in SALT): in our example it is 8700 - 5000 = 3700 rubles; Another calculation option: from the amount “Own to the employee”, which is indicated already taking into account the advance payment, subtract the accruals with code 2: 6700 - 3000 = 3700 rubles.

Income code 2300 with decoding

Using code 2300 in personal income tax reporting, temporary disability benefits are indicated. This code must be assigned not only to the benefit that is paid in case of illness of the employee himself, but also to those amounts that are transferred in the case of caring for sick children or other family members.

REFERENCE. Formally, maternity benefits also fall under this code, since the basis for its accrual is sick leave. But since maternity benefits are not subject to personal income tax (clause 1 of article 217 of the Tax Code of the Russian Federation), this payment may not be recorded at all in the registers and certificate 2-NDFL (clause 1 of article 230 of the Tax Code of the Russian Federation, letter of the Ministry of Finance dated April 2, 2019 No. 03- 04-05/22860).

Create electronic registers and submit them to the Social Insurance Fund via the Internet

Is income in the form of sick leave included in the certificate?

Sometimes, when filling out a document, the accountant is asked whether sick leave is reflected in 2-NDFL, and if so, on what line.

Temporary disability benefits are not subject to insurance premiums, but are included in the tax base for personal income tax. If you are in doubt whether sick leave is included in the 2-NDFL certificate, check the “Reason of disability” section, where a two-digit number is indicated. All values, with the exception of “05” - maternity benefits, are included in the income tax base, and the sick leave income code in the 2-NDFL certificate is assigned the value “2300”.

The benefit amount consists of two parts:

- the first 3 days, paid at the expense of the employer;

- the remaining days are paid at the expense of the Social Insurance Fund.

If you don’t know where to look at the sick leave code in the 2-NDFL certificate in 2021, pay attention to section 3:

The benefit amount is indicated on a separate line for the month in which the sick leave accrual and tax withholding were made. So, in this example, the employee received half a month’s salary and a taxable benefit in May.

Some types of benefits are fully compensated from the Social Insurance Fund. Regardless of the source of payment of funds, the sick leave code at the expense of the employer in the 2-NDFL certificate and the benefit paid at the expense of the Social Insurance Fund have the same value - “2300”.

Revenue codes 2762 and 2760 with decoding

Using code 2762 in tax registers and 2-NDFL certificates, you must indicate the entire amount of financial assistance issued to the employee at the birth of a child. Let us remind you that such financial assistance is not subject to personal income tax up to 50 thousand rubles. for each child, provided that the payment is transferred no later than one year after his birth (clause 8 of article 217 of the Tax Code of the Russian Federation).

When paying employees of other types of financial assistance, the code 2760 is used. In this case, the basis for the transfer of money does not matter. So, if the company decides to issue financial aid for vacation, then this amount must be separated from the main “vacation pay” and reflected with code 2760. This code must also be assigned to financial aid paid to former retired employees. Let us remind you that such income is not subject to personal income tax up to 4,000 rubles. per year (clause 28 of article 217 of the Tax Code of the Russian Federation).

Are daily allowances subject to income tax?

Art. 168 of the Labor Code of the Russian Federation states that an employer who sends a specialist on a business trip is obliged to compensate him for additional expenses associated with living away from home - to pay daily allowance. Their size is set by the company independently based on financial capabilities and ideas about fairness. It is fixed in the internal acts of the organization, for example, in a collective agreement.

Art. 217 of the Tax Code of the Russian Federation, indicates that daily allowances are not subject to personal income tax, provided that they do not exceed the following limits:

- 700 rub. – for traveling around the country;

- 2.5 thousand rubles. – for business trips abroad.

Art. 217 of the Tax Code of the Russian Federation obliges the company to withhold personal income tax from business trips in excess of the norm. To do this, the accountant acts according to the following algorithm:

- Calculates the amount of excess of paid daily allowances over the limits specified in the Tax Code of the Russian Federation.

- Determines the amount of personal income tax using the appropriate rate: 13% for residents of the Russian Federation, 30% for non-residents.

According to the provisions of the Tax Code of the Russian Federation, the accountant is obliged to calculate income tax during the month when the advance report prepared by the traveler was approved. Personal income tax is withheld from the specialist at the time of the next salary payment and is transferred to the state treasury no later than the day following this date.

Business trips in 2021: we arrange and pay for them

Income code 2720 with explanation

Code 2720 is used in personal income tax reporting to include the cost of gifts for employees. In particular, it should be used for gifts for the New Year, birthday, etc.

ATTENTION. According to the rules of paragraph 28 of Article 217 of the Tax Code of the Russian Federation, gifts worth no more than 4,000 rubles are exempt from personal income tax. in a year. This income must be reflected in the tax registers, regardless of the amount of the gift. But in the 2-NDFL certificates the cost of gifts does not exceed 4,000 rubles. for a year, you don’t have to show it (letters from the Federal Tax Service dated 07/02/15 No. BS-4-11/ [email protected] and dated 01/19/17 No. BS-4-11/ [email protected] ).

Also see: “Tax accounting for gifts and bonuses, or what an accountant should do after February 23 and March 8.”

Income code “Travelling” in certificate 2-NDFL

Mandatory payments to employees sent on business trips are provided for in Art. 167-168 Labor Code of the Russian Federation. These transfers to specialists are reflected in the 2-NDFL certificate. There are special income codes for them:

- 2000 – for the amount of average earnings, which, according to Art. 167 of the Labor Code of the Russian Federation, is necessarily reserved for the posted worker.

- 4800 – for the amount of daily allowance paid in excess of the norms established by Art. 217 of the Tax Code of the Russian Federation, and subject to income tax.

- 4800 – for compensation for accommodation, travel and other expenses not documented by the employee.

There is no special income code “Business trip” in the 2-NDFL certificate. Payments to a specialist, subject to income tax, are broken down by codes 2000 and 4800. Amounts within the limits that are exempt from taxation are not shown in the document.

Income codes 2400 and 1400 with decoding

To indicate rental income, you need to choose one of two codes (depending on the object that is transferred under the contract). Thus, income from the rental of any cars, as well as sea, river and aircraft, is reflected in personal income tax reporting using a special code 2400. It is necessary to show the fee for the rental of these types of transport, even if it is paid to the employee (including h. to the manager). The same code also covers income from other uses of vehicles. Therefore, it includes income from contracts for the provision of services for driving your own car, rental agreements with a crew, etc.

REFERENCE. Compensation for the use of a personal car, paid under an employment contract in the amount established by its parties, is not subject to personal income tax. There is no income code for this payment, and it does not need to be indicated in personal income tax reporting.

Also see: “How to more profitably register an employee’s use of his car (new edition).”

Draw up and print a vehicle rental agreement for free using a ready-made template

In addition, code 2400 applies to rental payments for fiber-optic and (or) wireless communication lines, and other means of communication, including computer networks.

Income from the rental of any other property (including real estate, including residential) must be reflected using code 1400. It does not matter who exactly receives this income from an organization or individual entrepreneur: a manager, an ordinary employee or an outsider.

For what incomes in payment cards have new codes been introduced?

Employers who have to work with the new rules naturally have a question: for what payments do they need to indicate codes in their payment slips?

Law No. 12-FZ does not specify a specific list of income for which codes are required in payment documents, although their groups are generally outlined. These include wages and other income, in respect of which Art. 99 of Law No. 229-FZ establishes restrictions, as well as income that cannot be levied under Art. 101 of Law No. 229-FZ.

This material talks about the maximum permissible deductions from citizens' salaries.

Directive of the Central Bank No. 5286-U provides three codes:

| Code | When to bet | Examples of payments |

| 1 | In income payments for which there is a limit on the amount of debt withholding (Article 99 of Law No. 229-FZ) |

|

| 2 | In payments for payments, from which deductions are not made, except for compensation for damage to health (Article 101 of Law No. 229-FZ) |

|

| 3 | In payments for the payment of compensation for harm to health, as well as for budgetary compensation to victims of radiation or man-made disasters (subclauses 1 and 4 of clause 1 of Article 101 of Law No. 229-FZ). These are amounts from which only alimony can be withheld. | |

*What is included in the salary for these purposes can be found in paragraph 1 of the List of income from which child support is withheld, approved. Decree of the Government of the Russian Federation dated July 18, 1996 No. 841.

Revenue code 2001 with decoding

Code 2001 is used for remuneration paid to directors on the board of directors and other members of the organization's collegial governing body.

ATTENTION. The salary of an executive under code 2001 is not “posted”, even if the corresponding position is called “director”. However, if the manager is a member of the board of directors (board, other collegial body) and receives additional remuneration for this, then this amount must be separated from the salary and reflected for personal income tax purposes using code 2001.

Wage type code: additional explanation

In addition to the listed salary codes, the order of the Federal Tax Service approved the following designations for income indicated in the 2-NDFL certificate:

1010 — dividends;

2001 - remuneration or similar payment to the company’s management structure;

2010 - payment based on a civil contract;

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

2530 - remuneration in kind;

2720 - income received as a gift;

2762 - payment of financial assistance to employees at the birth, adoption of a child.

Income code 2014 with explanation

The amounts of severance pay, as well as the average monthly earnings saved for the period of employment, are reflected in personal income tax reporting with the code 2014. This code applies only to that part of the payments that is subject to personal income tax (in total, it exceeds three times the average salary, and for “northerners” - sixfold). The income tax-free amount of severance pay and average earnings for the period of employment for personal income tax purposes is not fixed or coded.

Also see: “Payments when laying off an employee in 2019‑2020.”

Calculate a “complex” salary with coefficients and bonuses for a large number of employees Try for free

Salary codes in the payslip (or certificate 2-NDFL)

There are other salary codes that are also subject to indication in the 2-NDFL certificate:

2012 — vacation payments;

2300 — payment of sick leave;

2760 - payment of funds as financial assistance provided to an employee or former employee who retired due to disability or age;

4800 is a universal code that designates all payments that do not have a special code (for example, additional payments and compensation).

See also “Deciphering the codes in the 2-NDFL certificate.”

Expense codes for 2-NDFL in 2021: decoding

Some income specified in Art. 217 of the Tax Code of the Russian Federation, are taxed only to the extent that exceeds a certain limit. This non-taxable limit in the 2-NDFL certificate is called a deduction. The codes of such deductions must be indicated in the Appendix to the certificate in accordance with Appendix No. 2 to the Order of the Federal Tax Service of Russia dated September 10, 2015 N ММВ-7-11/, for example:

- 501 - deduction within 4,000 rubles. per year from gifts to individuals;

- 503 - deduction within 4,000 rubles. for a year with financial assistance to an employee or former employee who retired due to disability or age;

- 508 - deduction within 50,000 rubles. with one-time financial assistance to an employee upon the birth (adoption) of a child.

Read also

06.12.2019