Every year, no later than April 1, employers - companies and individual entrepreneurs submit 2-NDFL certificates for the past year to the tax office. They are also issued to employees who need certificates to prepare income declarations or to submit them to other authorities (for example, to a bank, or to apply for a housing subsidy). In order for the data to be indicated in accordance with the requirements of the law, all information must be correctly and reliably indicated, including citizenship (country code) in 2-NDFL.

What to follow when filling out

The main provisions are regulated by Chapter 23 of the Tax Code, which determines the procedure for recognizing income for personal income tax, the conditions for granting deductions and their amounts, tax rates, non-taxable amounts, and other conditions taken into account for taxation.

The 2-NDFL certificate itself is filled out in accordance with the order of the Federal Tax Service dated October 2, 2018 No. ММВ-7-11/ [email protected] For income for 2021, the forms submitted to the Federal Tax Service and issued to employees in 2021 differ from each other.

But both contain the “Citizenship” attribute. You cannot skip it, otherwise the certificate will be considered unreliable.

Signs 1 and 2 in the certificate

One of the difficult questions for the filler is which attribute to put.

A certificate with attribute 1 is filled out for each employee to whom the company paid funds and withheld tax from them, as well as for those funds for which it is impossible to withhold personal income tax. Submitted to the Federal Tax Service no later than April 1.

If it is impossible to collect personal income tax, then a separate certificate with sign 2 is drawn up. For example, if a gift worth more than four thousand was made to a person who is not an employee of the company. The certificate must be submitted before March 1 and indicate the amount of income from which it is impossible to withhold tax and the potential amount of tax.

Thus, if there is income on which it is impossible to pay tax, then you will have to draw up 2 certificates per person with characteristics 1 and 2. In the first, display all the income received by the employee, in the second, only those incomes on which it is impossible to pay tax.

What to indicate on the “Citizenship” line

By Decree of the State Standard of Russia dated December 14, 2001 No. 529-st, the list of all states - the “All-Russian Classifier of Countries of the World” (OCSM) - was put into effect and published for use. In addition to the names, it contains codes - each country has a unique letter and number designation.

The procedure for filling out the certificate requires that in the specially designated field of form 2-NDFL “Citizenship (country code)” a digital code number corresponding to the country of which the person in whose name the certificate is being generated is a citizen. The letter encoding for 2-NDFL is not used. If the person who received taxable income does not have citizenship, then the code of the country that issued the identity document is indicated on the certificate.

Read also: Taxpayer statuses in 2-NDFL

All-Russian Classifier of World Countries (OCSM)

| Code of the country | Short country name | Full title |

| 004 | AFGHANISTAN | Transitional Islamic State of Afghanistan |

| 008 | ALBANIA | Republic of Albania |

| 010 | ANTARCTICA | |

| 012 | ALGERIA | Algerian People's Democratic Republic |

| 016 | AMERICAN SAMOA | |

| 020 | ANDORRA | Principality of Andorra |

| 024 | ANGOLA | Republic of Angola |

| 028 | ANTIGUA AND BARBUDA | |

| 031 | AZERBAIJAN | Republic of Azerbaijan |

| 032 | ARGENTINA | Argentine Republic |

| 036 | AUSTRALIA | |

| 040 | AUSTRIA | Republic of Austria |

| 044 | BAHAMAS | Commonwealth of the Bahamas |

| 048 | BAHRAIN | Kingdom of Bahrain |

| 050 | BANGLADESH | People's Republic of Bangladesh |

| 051 | ARMENIA | Republic of Armenia |

| 052 | BARBADOS | |

| 056 | BELGIUM | Kingdom of Belgium |

| 060 | BERMUDA | |

| 064 | BUTANE | Kingdom of Bhutan |

| 068 | BOLIVIA, | Plurinational State of Bolivia |

| 070 | BOSNIA AND HERZEGOVINA | |

| 072 | BOTSWANA | Republic of Botswana |

| 074 | BOUVE ISLAND | |

| 076 | BRAZIL | Federative Republic of Brazil |

| 084 | BELIZE | |

| 086 | BRITISH TERRITORY IN THE INDIAN OCEAN | |

| 090 | SOLOMON ISLANDS | |

| 092 | VIRGIN ISLANDS, BRITISH | British Virgin Islands |

| 096 | BRUNEI DARUSSALAM | |

| 100 | BULGARIA | Republic of Bulgaria |

| 104 | MYANMAR | Republic of the Union of Myanmar |

| 108 | BURUNDI | Republic of Burundi |

| 112 | BELARUS | Republic of Belarus |

| 116 | CAMBODIA | Kingdom of Cambodia |

| 120 | CAMEROON | Republic of Cameroon |

| 124 | CANADA | |

| 132 | CAPE VERDE | Republic of Cape Verde |

| 136 | CAYMAN ISLANDS | |

| 140 | CENTRAL AFRICAN REPUBLIC | |

| 144 | SRI LANKA | Democratic Socialist Republic of Sri Lanka |

| 148 | CHAD | Republic of Chad |

| 152 | CHILE | Republic of Chile |

| 156 | CHINA | People's Republic of China |

| 158 | TAIWAN (CHINA) | |

| 162 | CHRISTMAS ISLAND | |

| 166 | COCONUT (KEELING) ISLANDS | |

| 170 | COLOMBIA | Republic of Colombia |

| 174 | COMOROS | Union of Comoros |

| 175 | MAYOTTE | |

| 178 | CONGO | Republic of the Congo |

| 180 | CONGO, DEMOCRATIC REPUBLIC | |

| 184 | COOK ISLANDS | |

| 188 | COSTA RICA | Republic of Costa Rica |

| 191 | CROATIA | Republic of Croatia |

| 192 | CUBA | Republic of Cuba |

| 196 | CYPRUS | Republic of Cyprus |

| 203 | CZECH REPUBLIC | |

| 204 | BENIN | Republic of Benin |

| 208 | DENMARK | Kingdom of Denmark |

| 212 | DOMINICA | Commonwealth of Dominica |

| 214 | DOMINICAN REPUBLIC | |

| 218 | ECUADOR | Republic of Ecuador |

| 222 | EL SALVADOR | Republic of El Salvador |

| 226 | EQUATORIAL GUINEA | Republic of Equatorial Guinea |

| 231 | ETHIOPIA | Federal Democratic Republic of Ethiopia |

| 232 | ERITREA | |

| 233 | ESTONIA | Republic of Estonia |

| 234 | FAROE ISLANDS | |

| 238 | FALKLAND ISLANDS (MALVINAS) | |

| 239 | SOUTH GEORGIA AND SOUTH SANDWICH ISLANDS | |

| 242 | FIJI | Republic of Fiji |

| 246 | FINLAND | Republic of Finland |

| 248 | ELAND ISLANDS | |

| 250 | FRANCE | French Republic |

| 254 | FRENCH GUIANA | |

| 258 | FRENCH POLYNESIA | |

| 260 | FRENCH SOUTHERN TERRITORIES | |

| 262 | Djibouti | Republic of Djibouti |

| 266 | GABON | Gabonese Republic |

| 268 | GEORGIA | |

| 270 | GAMBIA | Republic of Gambia |

| 275 | PALESTINIAN TERRITORY, OCCUPIED | Occupied Palestinian Territory |

| 276 | GERMANY | Federal Republic of Germany |

| 288 | GHANA | Republic of Ghana |

| 292 | GIBRALTAR | |

| 296 | KIRIBATI | Republic of Kiribati |

| 300 | GREECE | Hellenic Republic |

| 304 | GREENLAND | |

| 308 | GRENADA | |

| 312 | GUADELOUPE | |

| 316 | GUAM | |

| 320 | GUATEMALA | Republic of Guatemala |

| 324 | GUINEA | Republic of Guinea |

| 328 | GUYANA | Republic of Guyana |

| 332 | HAITI | Republic of Haiti |

| 334 | HEARD ISLAND AND MACDONALD ISLANDS | |

| 336 | PAPAL THRONE (STATE – CITY) | |

| 340 | HONDURAS | Republic of Honduras |

| 344 | HONG KONG | Hong Kong Special Administrative Region of China |

| 348 | HUNGARY | Hungarian Republic |

| 352 | ICELAND | Republic of Iceland |

| 356 | INDIA | Republic of India |

| 360 | INDONESIA | Republic of Indonesia |

| 364 | IRAN, ISLAMIC REPUBLIC | Islamic Republic of Iran |

| 368 | IRAQ | Republic of Iraq |

| 372 | IRELAND | |

| 376 | ISRAEL | State of Israel |

| 380 | ITALY | Italian Republic |

| 384 | COTE D'IVOIRE | Republic of Cote d'Ivoire |

| 388 | JAMAICA | |

| 392 | JAPAN | |

| 398 | KAZAKHSTAN | The Republic of Kazakhstan |

| 400 | JORDAN | Hashemite Kingdom of Jordan |

| 404 | KENYA | Republic of Kenya |

| 408 | KOREA, DEMOCRATIC PEOPLE'S REPUBLIC | Democratic People's Republic of Korea |

| 410 | REPUBLIC OF KOREA | The Republic of Korea |

| 414 | KUWAIT | State of Kuwait |

| 417 | KYRGYZSTAN | Kyrgyz Republic |

| 418 | LAOTIAN PEOPLE'S DEMOCRATIC REPUBLIC | |

| 422 | LEBANON | Lebanese Republic |

| 426 | LESOTHO | Kingdom of Lesotho |

| 428 | LATVIA | Latvian republic |

| 430 | LIBERIA | Republic of Liberia |

| 434 | LIBYA | Libya |

| 438 | LICHTENSTEIN | Principality of Liechtenstein |

| 440 | LITHUANIA | Republic of Lithuania |

| 442 | LUXEMBOURG | Grand Duchy of Luxembourg |

| 446 | MACAO | Macau Special Administrative Region of China |

| 450 | MADAGASCAR | Republic of Madagascar |

| 454 | MALAWI | Republic of Malawi |

| 458 | MALAYSIA | |

| 462 | MALDIVES | Republic of Maldives |

| 466 | MALI | Republic of Mali |

| 470 | MALTA | Republic of Malta |

| 474 | MARTINIQUE | |

| 478 | MAURITANIA | Islamic Republic of Mauritania |

| 480 | MAURITIUS | Republic of Mauritius |

| 484 | MEXICO | Mexican United States |

| 492 | MONACO | Principality of Monaco |

| 496 | MONGOLIA | |

| 498 | MOLDOVA, REPUBLIC | The Republic of Moldova |

| 499 | MONTENEGRO | |

| 500 | MONTSERRAT | |

| 504 | MOROCCO | Kingdom of Morocco |

| 508 | MOZAMBIQUE | Republic of Mozambique |

| 512 | OMAN | Sultanate of Oman |

| 516 | NAMIBIA | Republic of Namibia |

| 520 | NAURU | Republic of Nauru |

| 524 | NEPAL | Federal Democratic Republic of Nepal |

| 528 | NETHERLANDS | Kingdom of the Netherlands |

| 531 | CURACAO | |

| 533 | ARUBA | |

| 534 | SAINT MARTIN (Dutch part) | |

| 535 | BONAIR, SINT ESTATIUS AND SABA | |

| 540 | NEW CALEDONIA | |

| 548 | VANUATU | Republic of Vanuatu |

| 554 | NEW ZEALAND | |

| 558 | NICARAGUA | Republic of Nicaragua |

| 562 | NIGER | Niger Republic |

| 566 | NIGERIA | Federal Republic of Nigeria |

| 570 | NIUE | Niue |

| 574 | NORFOLK ISLAND | |

| 578 | NORWAY | Kingdom of Norway |

| 580 | NORTHERN MARIANA ISLANDS | Commonwealth of the Northern Mariana Islands |

| 581 | SMALL PACIFIC REMOTE ISLANDS | |

| 583 | MICRONESIA, FEDERATED STATES | Federated States of Micronesia |

| 584 | MARSHALL ISLANDS | Republic of the Marshall Islands |

| 585 | PALAU | Republic of Palau |

| 586 | PAKISTAN | Islamic Republic of Pakistan |

| 591 | PANAMA | Republic of Panama |

| 598 | PAPUA NEW GUINEA | |

| 600 | PARAGUAY | Republic of Paraguay |

| 604 | PERU | Republic of Peru |

| 608 | PHILIPPINES | Republic of the Philippines |

| 612 | PITKERN | |

| 616 | POLAND | Republic of Poland |

| 620 | PORTUGAL | Portuguese Republic |

| 624 | GUINEA-BISSAU | Republic of Guinea-Bissau |

| 626 | TIMOR-LESTE | Democratic Republic of Timor-Leste |

| 630 | PUERTO RICO | |

| 634 | QATAR | State of Qatar |

| 638 | REUNION | |

| 642 | ROMANIA | |

| 643 | RUSSIA | Russian Federation |

| 646 | RWANDA | Republic of Rwanda |

| 652 | SAINT BARTHELEMY | |

| 654 | SAINT HELENA, ASCENSION ISLAND, | |

| 659 | SAINT KITTS AND NEVIS | |

| 660 | ANGUILLA | |

| 662 | SAINT LUCIA | |

| 663 | SAINT MARTIN | |

| 666 | SAINT PIERRE AND MIKELON | |

| 670 | SAINT VINCENT AND THE GRENADINES | |

| 674 | SAN MARINO | Republic of San Marino |

| 678 | SAO TOME AND PRINCIPE | Democratic Republic of Sao Tome and Principe |

| 682 | SAUDI ARABIA | Kingdom of Saudi Arabia |

| 686 | SENEGAL | Republic of Senegal |

| 688 | SERBIA | Republic of Serbia |

| 690 | SEYCHELLES | Republic of Seychelles |

| 694 | SIERRA LEONE | Republic of Sierra Leone |

| 702 | SINGAPORE | Republic of Singapore |

| 703 | SLOVAKIA | The Slovak Republic |

| 704 | VIETNAM | Socialist Republic of Vietnam |

| 705 | SLOVENIA | Republic of Slovenia |

| 706 | SOMALIA | Somali Republic |

| 710 | SOUTH AFRICA | South Africa |

| 716 | ZIMBABWE | Republic of Zimbabwe |

| 724 | SPAIN | The Kingdom of Spain |

| 728 | SOUTH SUDAN | Republic of South Sudan |

| 729 | SUDAN | Republic of Sudan |

| 732 | WEST SAHARA | |

| 740 | SURINAME | Republic of Suriname |

| 744 | SPITSBERGEN AND JAN MAYEN | |

| 748 | SWAZILAND | Kingdom of Swaziland |

| 752 | SWEDEN | Kingdom of Sweden |

| 756 | SWITZERLAND | Swiss Confederation |

| 760 | SYRIAN ARAB REPUBLIC | |

| 762 | TAJIKISTAN | The Republic of Tajikistan |

| 764 | THAILAND | Kingdom of Thailand |

| 768 | TOGO | Togolese Republic |

| 772 | TOKELAU | |

| 776 | TONGA | Kingdom of Tonga |

| 780 | TRINIDAD AND TOBAGO | Republic of Trinidad and Tobago |

| 784 | UNITED ARAB EMIRATES | |

| 788 | TUNISIA | Tunisian Republic |

| 792 | Türkiye | Turkish Republic |

| 795 | TURKMENIA | Turkmenistan |

| 796 | TURKS AND CAICOS ISLANDS | |

| 798 | TUVALU | |

| 800 | UGANDA | Republic of Uganda |

| 804 | UKRAINE | |

| 807 | REPUBLIC OF MACEDONIA | |

| 818 | EGYPT | Arab Republic of Egypt |

| 826 | UNITED KINGDOM | United Kingdom of Great Britain and Northern Ireland |

| 831 | GUERNSEY | |

| 832 | JERSEY | |

| 833 | ISLE OF MAN | |

| 834 | TANZANIA, UNITED REPUBLIC | United Republic of Tanzania |

| 840 | UNITED STATES | USA |

| 850 | VIRGIN ISLANDS, USA | United States Virgin Islands |

| 854 | BURKINA FASO | |

| 858 | URUGUAY | Eastern Republic of Uruguay |

| 860 | UZBEKISTAN | The Republic of Uzbekistan |

| 862 | VENEZUELA | Bolivarian Republic of Venezuela |

| 876 | WALLIS AND FUTUNA | |

| 882 | SAMOA | Independent State of Samoa |

| 887 | YEMEN | Yemen Republic |

| 894 | ZAMBIA | Republic of Zambia |

| 895 | ABKHAZIA | Republic of Abkhazia |

| 896 | SOUTH OSSETIA | Republic of South Ossetia |

How to find the code number

The numeric code has 3 digits. To avoid mistakes, you will need:

- open OKSM;

- find by name the country of citizenship of the taxpayer (the person about whose income you need to draw up a document);

- select a code by country name;

- enter it in the appropriate field of the form.

Most programs that offer to fill out 2-personal income tax make it possible to automatically select the desired code from a directory by country name. Those who fill out certificates manually will have to look for the number in the classifier themselves.

Filling out 2 personal income tax for a Russian citizen

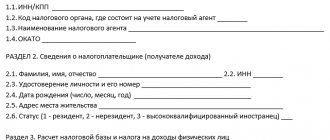

The form consists of several sections.

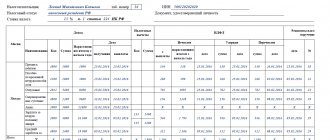

Help 2NDFL, part 1

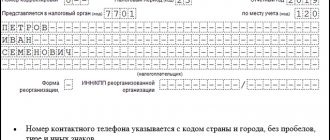

In this upper part there are 2 sections and the following details must be entered here:

- the name of the tax agent, that is, the organization that issues the certificate

- a sign indicating the possibility or impossibility of paying tax

- certificate number, as well as for what period and on what date it is drawn up

- territorial tax code where the company is registered

- correction number (zero means that no corrections have yet been made to the document)

- company telephone number with area code

- organization details: TIN, OKTMO and KPP (for individual entrepreneurs, a dash)

- TIN of the citizen for whom the form is being filled out

- Full name and date of birth of the employee

- taxpayer status (one for a Russian resident)

- RF code or country code where the employee came from

- code of the document used (twenty-one means passport) and its series, number

- the address where the employee lives

The second part of the certificate consists of three sections, which indicate monthly income, deductions and the amount of calculated tax and paid tax.

Help 2NDFL, part 2

Section three lists the coded types of income received. So in this example, the salary is displayed using the code 2000, vacation using the code 2012, and in the twelfth month 2720 the gift received. As for code 501, this is a standard maximum deduction of four thousand from the gift received. Everything above is subject to personal income tax.

The fourth section reflects deductions. So, deduction with code 126 is deductions for a child under eighteen years of age.

The fifth section for calculating personal income tax. Adding up all income for each month (including gifts), we get 282,000 rubles. Accordingly, according to deductions, it comes out to 23,000 + 4000 = 27,000 rubles. The total base from which the tax is calculated is 282,000 – 27,000 = 255,000 rubles. And the calculated tax is 255,000 * 13% = 33,150 rubles.

But in this example, the employee Vinnik quit her job on December 1 and, accordingly, the accountant in December does not have a basis for receiving tax on the value of the gift exceeding four thousand. After all, the deduction is given only in the amount of four thousand, and the gift costs 12,000, so the difference is 12,000 - 4,000 = 8,000 rubles. tax must be paid. But since Vinnik no longer works, this is impossible and the accountant writes in a special field the amount that could not be withheld, that is, 8,000 * 13% = 1,040 rubles. And in those fields where the withheld and transferred tax is indicated, the amount of the calculated tax is written, reduced by this tax, which cannot be collected.

Since a tax has been formed that is impossible to pay, you should additionally draw up 2 personal income taxes indicating sign 2. Where, in general, all the same data is entered, but only the cost of this gift is indicated in the income and the unpaid tax is calculated only on it.

Is this information required?

According to paragraph 5 of Article 169 of the Tax Code of the Russian Federation, one of the points that must be indicated in the invoice of goods is the country of origin. Moreover, if a purchase was made abroad, then in the next column indicate the number of the customs declaration (clause 5 of article 169 of the Tax Code, clause 2 of the Rules, approved by Government Decree No. 1137 of December 26, 2011).

An exception to this requirement is specified in the letter of the Ministry of Finance dated November 27, 2017 No. 03-07-09/78220. If you purchase goods abroad and sell individual parts of them in the Russian Federation, you do not need to indicate the country of origin on the invoice. It is required to put a dash in both column No. 10 “Country of origin of the goods” and in column No. 11 “Registration number of the customs declaration.”

In addition, it is not required to indicate it for goods produced on the territory of the Russian Federation for sale within its borders. This is confirmed by the information in subparagraphs K and L of clause 2 of the Rules for filling out an invoice, approved by Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137.

Other features of filling out the title page

The document has the right to be drawn up not only by the applicant for a tax deduction, but also by his representative. To display this fact in the part of the title page signed as “accuracy and completeness of information,” you need to indicate the number 1 or 2, thereby indicating the status of the individual confirming the correctness of the above information. If it is the taxpayer himself, it is necessary to write one, and if his representative - two.

In addition, we recommend that persons who enter information on the first sheet of the tax return pay attention to the following aspects:

- The top of the sheet. At the top of the title page there are twelve empty cells in which an individual must enter the digits of the identification code, and below them three more, intended for affixing the sheet number. In this case it is the first page. To number it correctly, you need to enter zeros in the first two cells, and the number one in the third.

- Number of pages of this 3-NDFL form. When checking a declaration, it is convenient for the tax inspector to immediately see how many pages the received form consists of. Therefore, after the field in which an individual must indicate his contact phone number, there is a line intended to indicate the number of sheets. If the tax return includes seven pages, then such information is displayed as follows: “007”.

- Empty fields. Sometimes some cells, for example, district, locality or taxpayer address outside the Russian Federation, do not need to be filled out. In order to make it clear to the tax inspector that these fields were left empty and not forgotten, a dash must be placed in each cell.

- Date of. There is a rule regarding entering the date in the declaration, as well as in some other documents, which implies compliance with a certain sequence - first you must write the date, then the month and then the year (everything is indicated using numbers). If the serial number of the day or month is less than ten, then zero is written first, and then the number itself.

- Address. In addition to writing by an individual the name of the city, street and other coordinates of the address, he must indicate whether we are talking about the address of his stay (code 2) or residence (code 3).

It should be noted that if, along with the declaration form, an individual sends some other documents to the tax service, then he needs to count the total number of pages of these papers and note the result obtained on the title page (next to the number of pages of the 3-NDFL form).