Indicators for calculating imputed income

First of all, the amount of imputed income, on the basis of which UTII is calculated, depends on the type of activity transferred to this special regime. Or rather, on the physical indicator that characterizes such imputed activity. This could be the number of employees, the area of the sales floor, the number of retail places, etc. A complete list of physical indicators for different areas is contained in paragraph 3 of Article 346.29 of the Tax Code of the Russian Federation. Multidisciplinary organizations must keep separate records of physical indicators for each type of imputed activity (clauses 6 and 7 of Article 346.26 of the Tax Code of the Russian Federation).

In addition to physical indicators, to calculate you need to know:

- monthly basic profitability of a physical indicator (clause 3 of Article 346.29 of the Tax Code of the Russian Federation);

- the value of the deflator coefficient K1 (clause 4 of Article 346.29 of the Tax Code of the Russian Federation);

- the value of the correction coefficient K2 (clause 4 of Article 346.29 of the Tax Code of the Russian Federation).

The value of the K1 coefficient changes every year. For 2021, it is set at 1,798 (order of the Ministry of Economic Development of Russia dated October 20, 2015 No. 772).

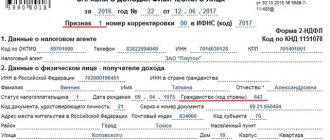

Title page

The title page contains general information about the taxpayer:

- TIN and KPP codes are indicated in accordance with the tax registration certificate. Since the TIN of an individual contains 2 characters more than that of a legal entity, for enterprises dashes are entered in the corresponding field in the two cells on the right.

- The adjustment number has the format 0—, 1—, etc. It indicates the “version” of the report—primary or modified.

- Tax period: for the third quarter - code 23.

- The reporting year is 2021.

- Tax office code in accordance with the certificate.

- Code of the place of submission of the report from Appendix 3 to the Procedure for filling out the declaration, approved. by order of the Federal Tax Service of Russia dated June 26, 2018 No. ММВ-7-3/ [email protected] (at the location/residence, activity, etc.).

- Full name of the organization or full name of the entrepreneur.

- The reorganization code and TIN/KPP of the reorganized organization are filled in if the report is submitted by the legal successor.

- The contact telephone number is indicated with the country and city code, without spaces, dashes or other characters.

- The number of sheets of the declaration itself and supporting documents.

- Name (full name) of the taxpayer or his representative, as well as the signature of the responsible person. If the report is submitted by a representative, then you must indicate the details of the power of attorney.

- Information about the receipt of the report is filled out by an employee of the Federal Tax Service. It includes information about the form for submitting the report, the number of sheets, registration number, date and signature of the specialist.

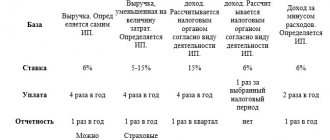

Calculation of imputed income (tax base)

Determine the tax base for the quarter depending on whether the organization used UTII throughout this period or not.

If the organization was a UTII payer for the entire quarter, then calculate the tax base using the formula:

| Tax base (imputed income) for the quarter | = | Basic profit per month | × | ( | The value of the physical indicator for the first month of the quarter | + | The value of the physical indicator for the second month of the quarter | + | The value of the physical indicator for the third month of the quarter | ) | × | K1 | × | K2 |

This procedure is provided for in paragraph 10 of Article 346.29 of the Tax Code of the Russian Federation.

If you switched to imputed tax in the middle of the quarter, then you need to calculate UTII starting from the date of registration as a single tax payer. First, calculate the tax base for the month in which the organization began to use UTII. Formula for calculating UTII:

| Tax base (imputed income) for the month in which UTII began to be applied | = | Basic profit per month | × | The value of the physical indicator ___________________________ | × | The actual number of days when activities were carried out using UTII, in the month in which the organization became a UTII payer | × | K1 | × | K2 |

| The number of calendar days in the month in which the organization became a UTII payer |

Next, determine the amount of imputed income for the remaining full months of the quarter. And add it to the amount of income received for the month in which UTII began to be applied. The result will be the tax base for the entire quarter (clause 10 of Article 346.29 of the Tax Code of the Russian Federation).

An important detail: if in one of the months the value of the physical indicator has changed, for example, the retail space of the hall has increased, then for this month take the new value to calculate the tax. Even if the change occurred in the middle of the month (clause 9 of Article 346.29 of the Tax Code of the Russian Federation).

Example of UTII calculation. The organization became a UTII payer in the middle of the quarter

The Alpha organization sells goods at retail through its own store with a sales area of 80 square meters. m. In the city where the organization operates, the use of UTII is provided for such activities. The UTII rate for retail trade is 15 percent. "Alpha" became a payer of UTII on January 28. In fact, in January the organization was a UTII payer for four days, in February and March for full months.

In 2021, the value of the deflator coefficient K1 is 1.798. Local authorities set the value of the correction factor K2 at 0.7.

The basic profitability for retail trade in the presence of trading floors is 1800 rubles/sq.m. m.

The imputed income for calculating UTII for January was: 1800 rubles/sq.m. m × 80 sq. m: 31 days. × 4 days × 0.7 × 1.798 = 23,386 rubles.

Imputed income for February–March was:

1800 rub./sq. m × (80 sq. m + 80 sq. m) × 0.7 × 1.798 = 362,477 rub.

Thus, the imputed income for calculating UTII for the first quarter is equal to 385,863 rubles. (RUB 23,386 + RUB 362,477).

UTII for the first quarter is equal to: 385,863 rubles. × 15% = 57,879 rub.

Now let’s talk about how to find out the amount of imputed income for the quarter in which the organization ceased its imputed activities. In this case, calculate the base from the first day of the quarter until the date of deregistration specified in the notification of the tax office. First, determine the tax base for the month in which the organization stopped using UTII using the formula:

| Tax base (imputed income) for the month in which UTII ceased to be used | = | Basic profit per month | × | The value of the physical indicator for the month in which the organization ceased to be a UTII payer | : | The number of calendar days in the month in which the organization ceased to be a UTII payer | × | The actual number of days of business activity using UTII in the month in which the organization ceased to be a UTII payer | × | K1 | × | K2 |

Next, determine the amount of imputed income for the remaining full months of the quarter. And add it to the amount of income received for the month in which UTII was no longer used. The result will be the tax base for the entire quarter (clause 10 of Article 346.29 of the Tax Code of the Russian Federation).

An example of calculating taxes on UTII. The organization ceased to be a UTII payer in the middle of the quarter

The Alpha organization sells goods at retail through its own store with a sales area of 80 square meters. m. In the city where the organization operates, the use of UTII is provided for such activities. The UTII rate for retail trade is 15 percent. Since March 21, the sales area in the Alpha store has exceeded 150 square meters. m, and the organization ceased to be a UTII payer.

In fact, in March, the organization was a UTII payer for 20 days.

In 2021, the value of the deflator coefficient K1 is 1.798. Local authorities set the value of the correction factor K2 at 0.7.

The basic profitability for retail trade in the presence of trading floors is 1800 rubles/sq.m. m.

The imputed income for calculating UTII for March was: 1800 rubles/sq.m. m × 80 sq. m: 31 days. × 20 days × 0.7 × 1.798 = 116,928 rubles.

Imputed income for January–February was:

1800 rub./sq. m × (80 sq. m + 80 sq. m) × 0.7 × 1.798 = 362,477 rub.

Thus, the imputed income for calculating UTII for the first quarter is equal to 479,405 rubles. (RUB 362,477 + RUB 116,928).

UTII for the first quarter of the year is equal to: 479,405 rubles. × 15% = 71,911 rub.

Situation: how to calculate the tax base for UTII when conducting retail trade through several outlets? During the quarter, some retail outlets were closed.

When calculating the imputed tax, take into account the months in which retail outlets were closed.

By closing individual retail outlets, the organization ceases its retail activities through these facilities. It is impossible to consider the liquidation of retail facilities as a change in the value of physical indicators (the area of sales floors or the number of retail places). Therefore, in this case, it will not be possible to take advantage of the provisions of paragraph 9 of Article 346.29 of the Tax Code of the Russian Federation, which allows you not to pay UTII for the months in which retail outlets were closed.

Paying tax in proportion to the actual duration of activity of closed retail outlets is also illegal. The fact is that the norms of paragraph 10 of Article 346.29 of the Tax Code of the Russian Federation, which provide for this option, are applied only in cases where an organization (entrepreneur) completely ceases its activities and is removed from tax registration as a UTII payer. This does not happen in this situation. Therefore, regardless of what dates of the month the activity of the retail facility was terminated, UTII for this month must be paid in full, without adjusting the tax base.

It is advisable to notify the tax office of the cessation of activity at individual retail outlets. To do this, use the application form, in which indicate code 4 “other” as the reason for deregistration. Based on this statement, the inspection will take note that trade is no longer carried out at a specific address, but the organization itself still remains a payer of UTII. Such clarifications are contained in letters of the Federal Tax Service of Russia dated February 1, 2012 No. ED-4-3/1500 (the document is approved by the Ministry of Finance of Russia and posted on the official website of the tax service), dated December 18, 2014 No. GD-4-3/26206 , as well as in the information dated June 27, 2014.

It should be noted that the letter of the Ministry of Finance of Russia dated October 30, 2013 No. 03-11-11/46223 reflects a different position. The authors of the letter qualify the closure of some retail outlets and the continuation of trading activities at other facilities as a change in the value of the physical indicator provided for in paragraph 9 of Article 346.29 of the Tax Code of the Russian Federation. Answering a question from an entrepreneur who closed a retail facility on August 25, representatives of the Russian Ministry of Finance explained that this facility must be excluded from the calculation of the tax base from August 1.

A situation where the Russian Ministry of Finance expresses directly opposite points of view on the same issue can be considered as an irremovable contradiction that should be interpreted in favor of taxpayers (clause 7 of Article 3 of the Tax Code of the Russian Federation). But to resolve this contradiction, you need to go to court. If the payer does not intend to take risks, he should adhere to the official explanations of the tax service.

However, some courts recognize that the absence of an application for deregistration in itself cannot be a reason for charging UTII for a non-existent outlet. Examples – decisions of the Arbitration Court of the West Siberian District dated October 7, 2015 No. F04-24010/2015, the Thirteenth Arbitration Court of Appeal dated October 16, 2015 No. A42-686/2015.

The essence of the disputes that the courts considered is the same: the sellers closed part of their retail facilities, but did not submit applications for deregistration as UTII payers. As a result, they were charged additional taxes for the period when the retail outlets were no longer operating and were subject to sanctions.

The courts overturned the inspectors' decisions. The court decisions reflect the following conclusions:

– the entrepreneur is not obliged to pay tax for a retail facility that is not in use - this approach contradicts the essence of the UTII system;

– closing a retail outlet does not mean a change in the physical indicator, but the cessation of activity (this thesis coincides with the position of the Federal Tax Service of Russia);

– documented termination of the activity of a retail outlet is equivalent to deregistration as a UTII payer, regardless of the submission of the corresponding application to the tax office.

Thus, if the circumstances of the closure of retail outlets are similar, the organization has a chance to win the dispute.